Recommended

More Related Content

Similar to HIDDEN GOODWILL.pptx

Similar to HIDDEN GOODWILL.pptx (20)

Recently uploaded

Recently uploaded (20)

HIDDEN GOODWILL.pptx

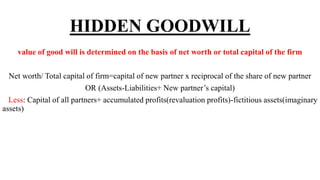

- 1. HIDDEN GOODWILL value of good will is determined on the basis of net worth or total capital of the firm Net worth/ Total capital of firm=capital of new partner x reciprocal of the share of new partner OR (Assets-Liabilities+ New partner’s capital) Less: Capital of all partners+ accumulated profits(revaluation profits)-fictitious assets(imaginary assets)

- 2. A & B are partners sharing profits in the ratio of 3:2.Their capitals are 160000 and 100000.They admit Somesh for 1/5 th share. He brought 120000 as his capital. Calculate value of goodwill. Total capital of firm=capital of new partner X reciprocal of share = 120000 x 5/1=60000 Less: Capital of all Partners(160000+100000+120000) =380000 VALUE OF GOOD WILL OF THE FIRM= 600000-380000 =220000

- 3. 34. Total capital of firm=70000 x 4/1=280000 Less: Capital of partners(60000+120000+70000)=250000 Good will=280000-250000 =30000

- 4. Accounting of Accumulated losses and reserve • Accumulated losses and reserve shared by old partners in their old ratio Journal entry for sharing of accumulated losses Partners Capital Account Dr To Profit and loss account’ Journal entry for sharing of reserve General Reserve account Dr To Partners Capital account