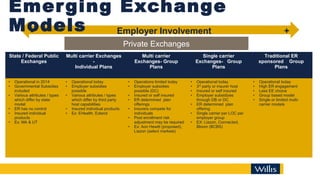

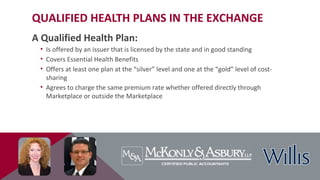

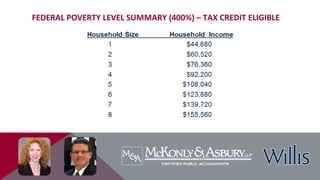

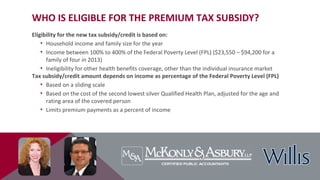

The document outlines the Patient Protection and Affordable Care Act (ACA) and its implications for health insurance exchanges, highlighting public and private marketplaces, eligibility for federal assistance, and employer requirements. It details the enrollment process, including the need for employers to notify employees about the exchanges, the availability of tax credits, and the essential health benefits covered under qualified plans. The document also discusses penalties for non-compliance for employers and individuals without minimum essential coverage, as well as resources for assistance in navigating the ACA's provisions.