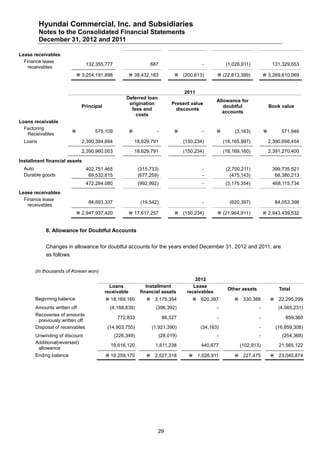

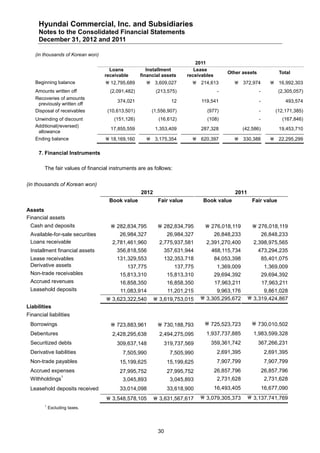

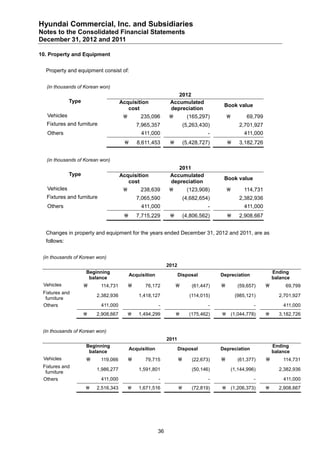

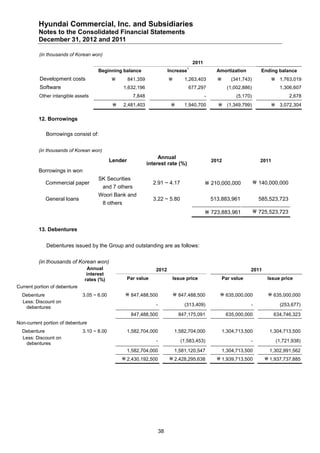

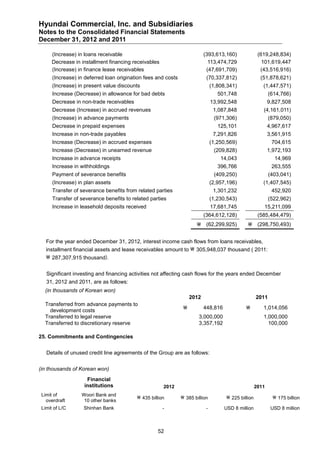

This document provides the consolidated financial statements of Hyundai Commercial, Inc. and its subsidiaries for the years ended December 31, 2012 and 2011. It includes the consolidated statements of financial position, comprehensive income, changes in equity, and cash flows for 2012 and 2011, as well as notes to the financial statements. The report of the independent auditors expresses an unqualified opinion that the consolidated financial statements present fairly the financial position, results of operations and cash flows of Hyundai Commercial, Inc. and its subsidiaries in accordance with Korean IFRS.