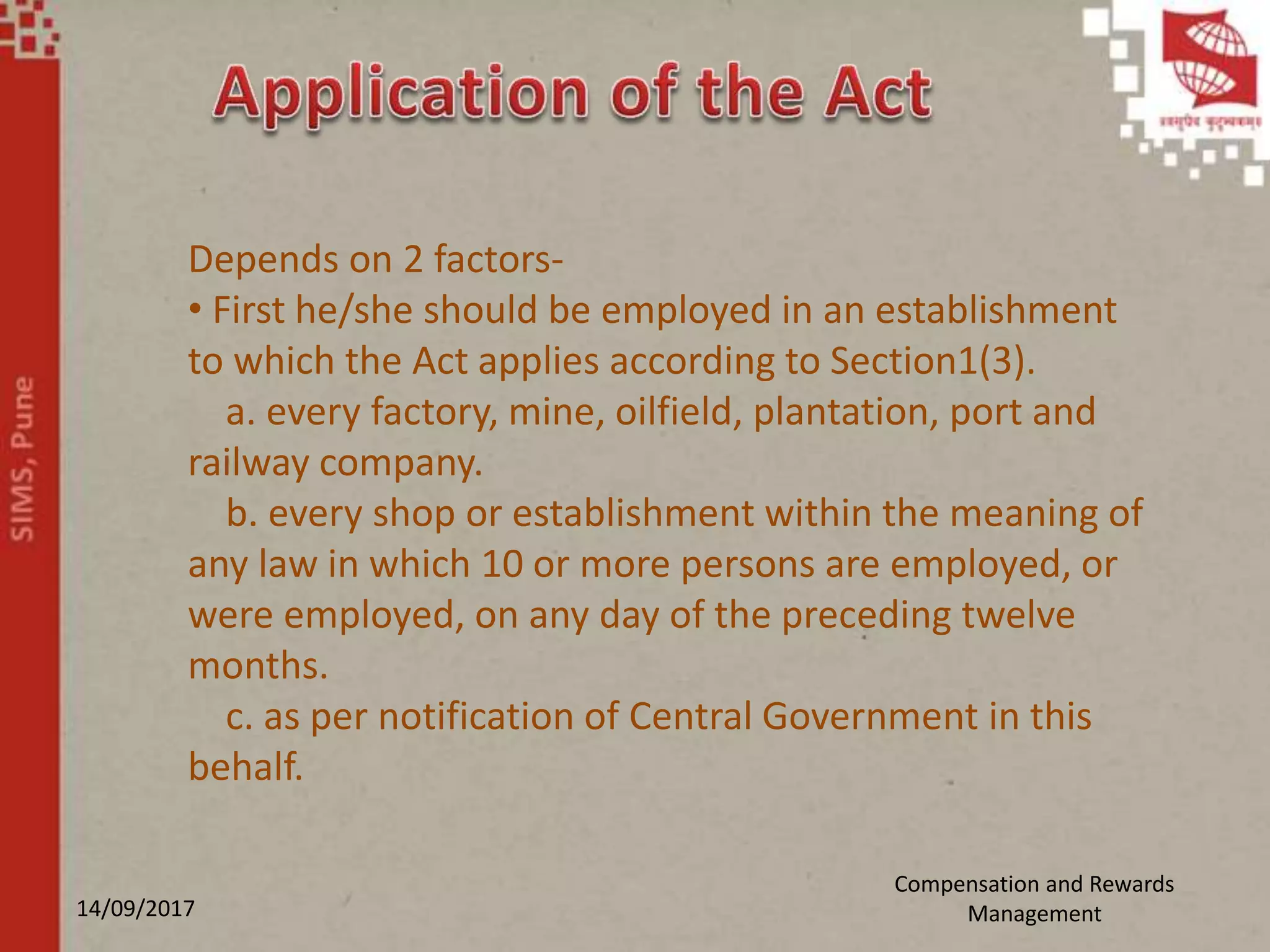

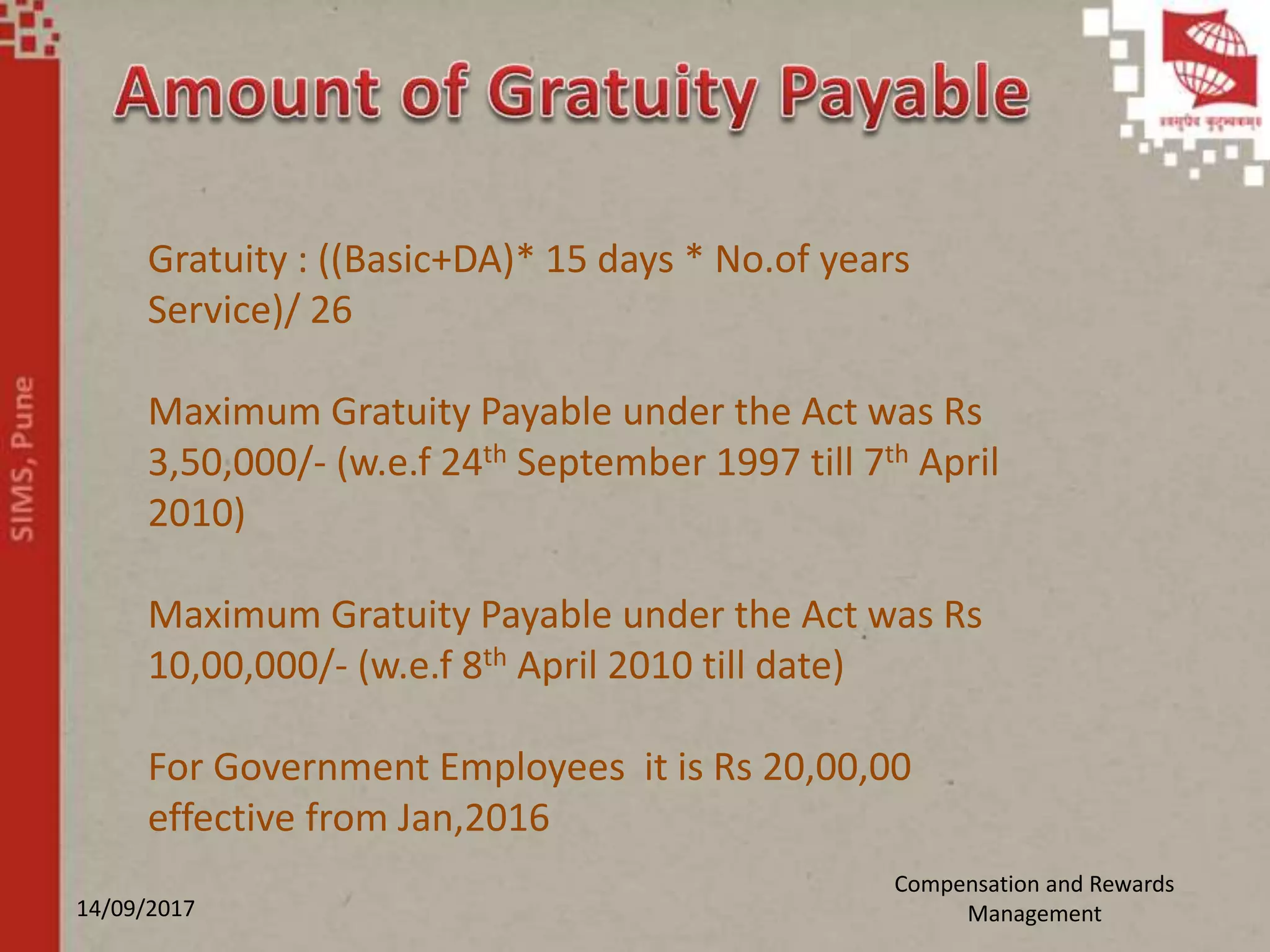

The document discusses the Payment of Gratuity Act of 1972 in India. It defines gratuity as a lump sum reward paid by an employer to employees at the end of their employment after 5 continuous years of service. It outlines who is eligible for gratuity, how the amount is calculated at 15 days wages for each completed year of service up to Rs. 10 lakhs, exceptions for disability or death, obligations of employers to determine and pay gratuity within 30 days, and income tax exemptions on gratuity amounts. Recent amendments increased the maximum tax-free gratuity to Rs. 20 lakhs for government and private employees.

![The Employee State Insurance[ESI] Act,1948](https://cdn.slidesharecdn.com/ss_thumbnails/88da15d1-bff6-4d25-b9fd-32a6fe52ebb4-150415044419-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)