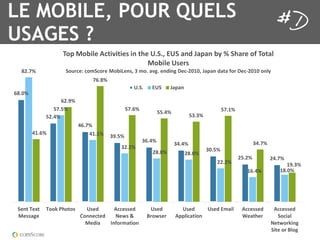

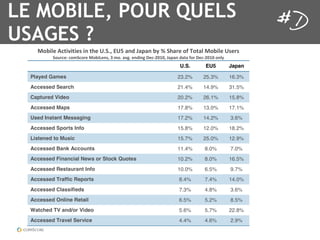

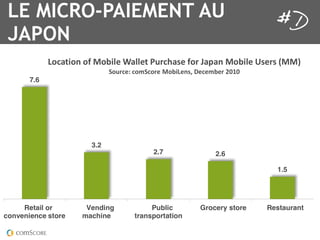

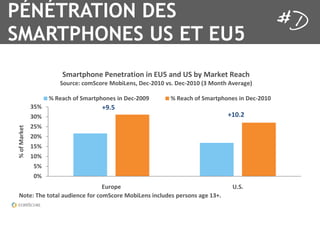

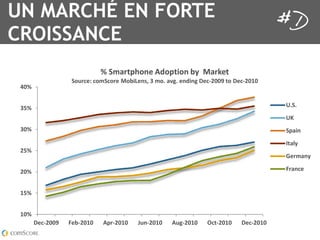

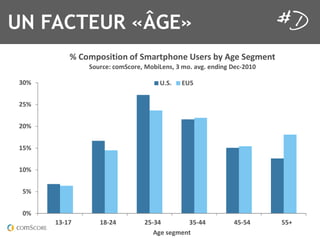

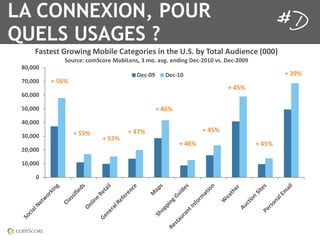

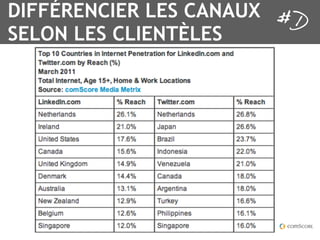

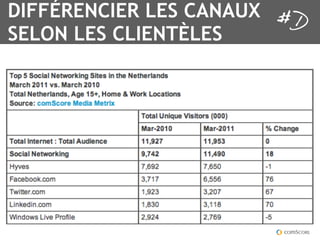

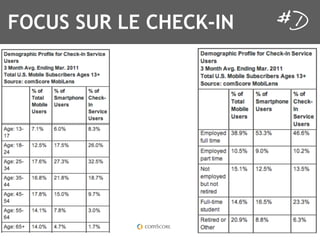

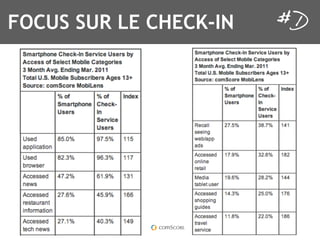

The document discusses the evolving landscape of mobile technology and its impact on tourism, emphasizing the significance of mobile strategies for enhancing customer experiences and territorial engagement. It presents data on mobile usage trends across different countries, with a focus on smartphone penetration and user behaviors in the EU, U.S., and Japan. The document also highlights the importance of mobile applications, social networking, and location-based services for engaging tourists and improving marketing strategies.