Download to read offline

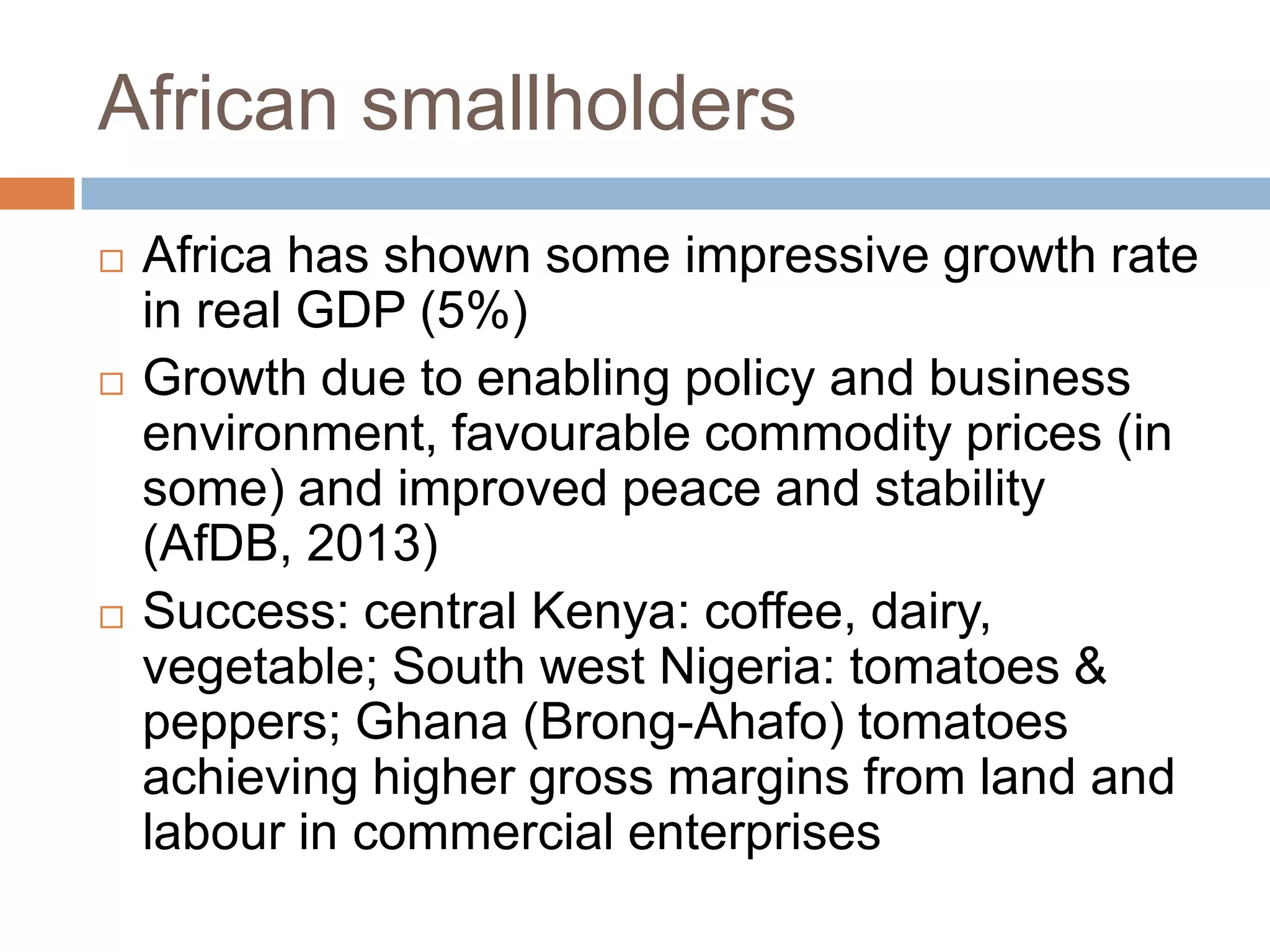

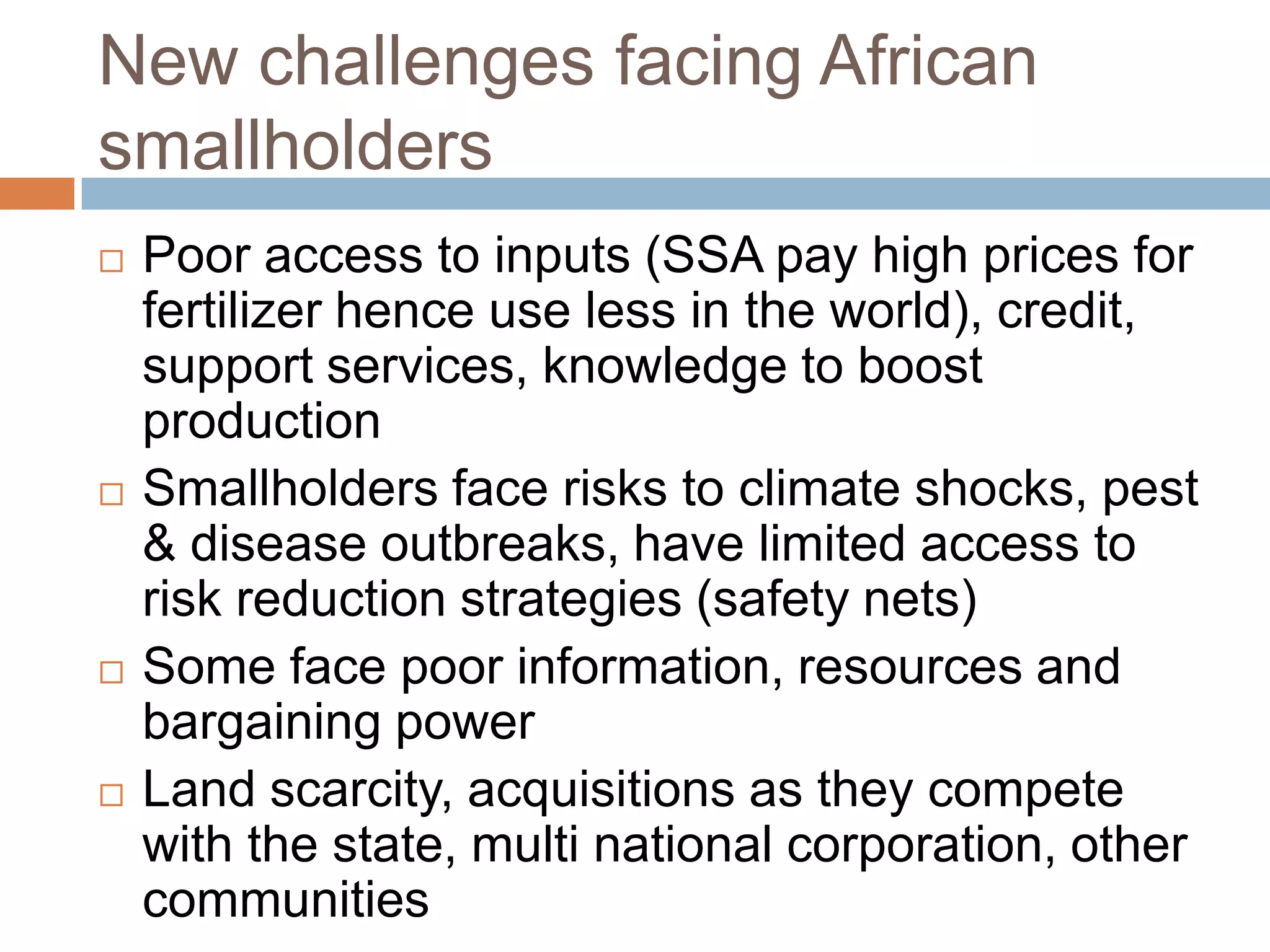

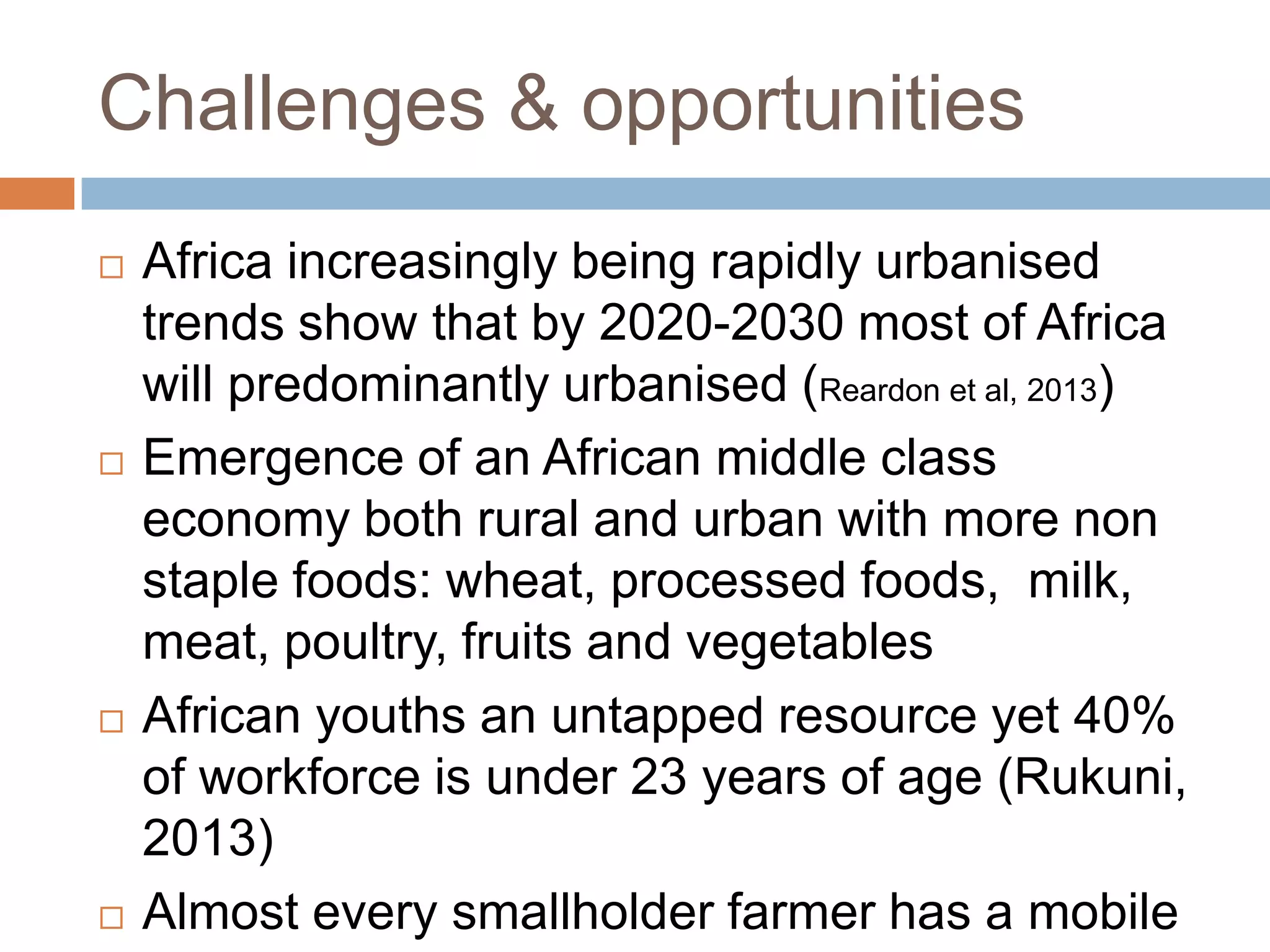

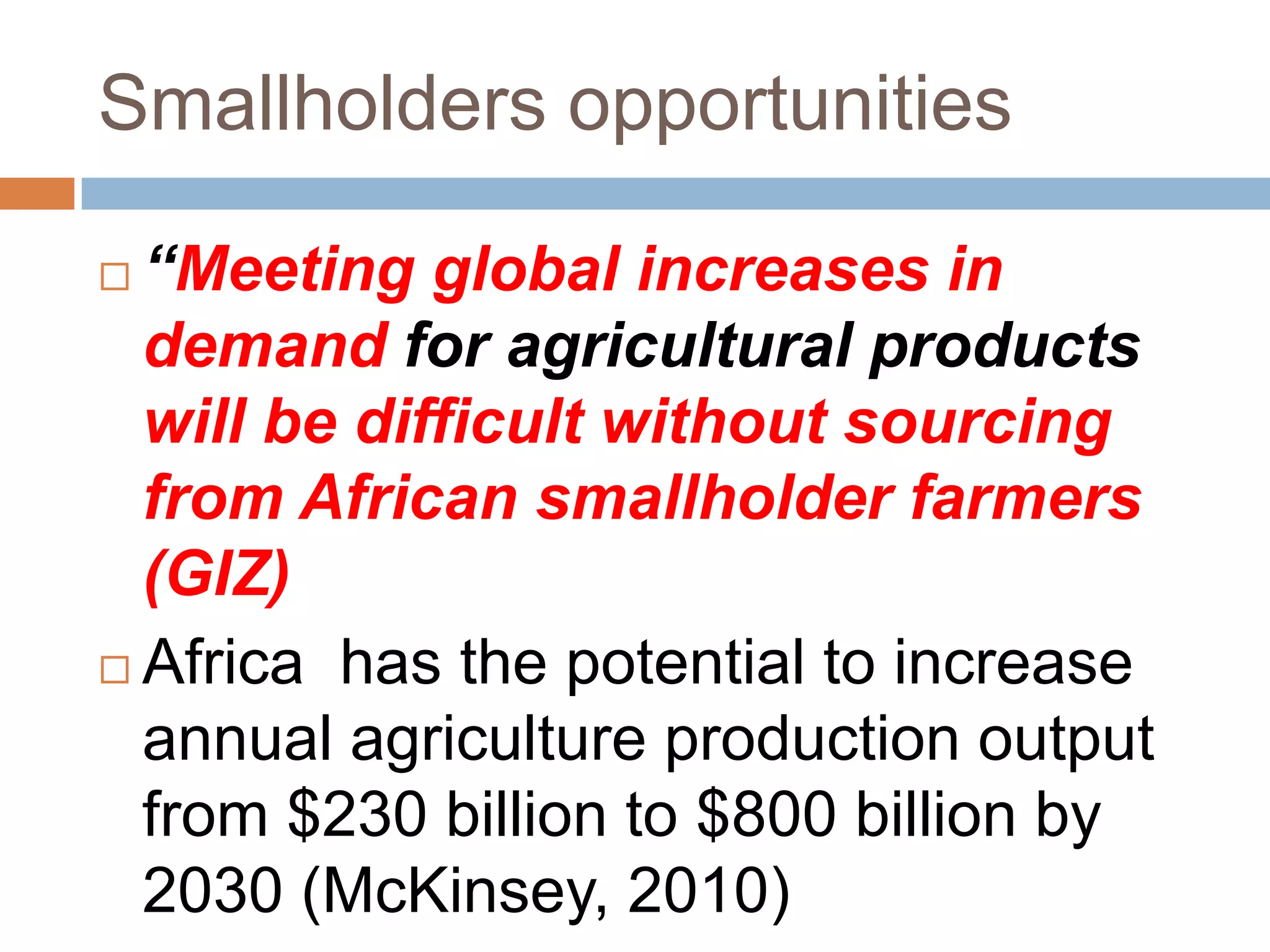

Smallholder farmers in Africa face challenges in achieving food security and income growth despite some countries experiencing economic growth. While Africa has great potential in agriculture, only a small percentage of smallholders have been able to access lucrative export markets. New opportunities exist for smallholders through partnerships with the private sector and adding value locally. For smallholder agriculture to transform, priority must be given to diversifying crops, increasing competitiveness across value chains, and developing human and technological capital.