Funded Vacant Positions

•

0 likes•269 views

This is a March 2010 report by the city of Honolulu on vacant funded positions within city government.

Recommended

More Related Content

Similar to Funded Vacant Positions

Similar to Funded Vacant Positions (20)

More from Honolulu Civil Beat

More from Honolulu Civil Beat (20)

Funded Vacant Positions

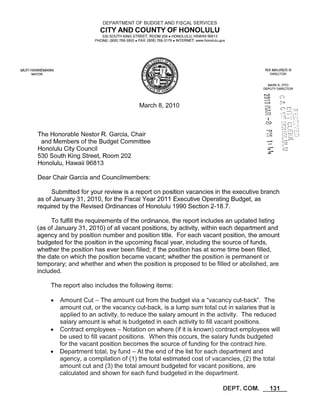

- 1. DEPARTMENT OF BUDGET AND FISCAL SERVICES CITY AND COUNTY OF HONOLULU 530 SOUTH KING STREET, ROOM 208 • HONOLULU, HAWAII 96813 PHONE: (808) 768-3900 • FAX: (808) 768-3179 • INTERNET: w~w.honoIuIu.gov MUFI HANNEMANN RIX MAURER III MAYOR DIRECTOR MARK K. OTO DEPUTY DIRECTOR ~C) March8,2010 ~ :7~ ~_:~7~ CO :~:c-~ The Honorable Nestor R Garcia, Chair and Members of the Budget Committee —~ Honolulu City Council 530 South King Street, Room 202 Honolulu, Hawaii 96813 Dear Chair Garcia and Councilmembers: Submitted for your review is a report on position vacancies in the executive branch as of January 31, 2010, for the Fiscal Year 2011 Executive Operating Budget, as required by the Revised Ordinances of Honolulu 1990 Section 2-18.7. To fulfill the requirements of the ordinance, the report includes an updated listing (as of January 31, 2010) of all vacant positions, by activity, within each department and agency and by position number and position title. For each vacant position, the amount budgeted for the position in the upcoming fiscal year, including the source of funds, whether the position has ever been filled; if the position has at some time been filled, the date on which the position became vacant; whether the position is permanent or temporary; and whether and when the position is proposed to be filled or abolished, are included. The report also includes the following items: • Amount Cut The amount cut from the budget via a “vacancy cut-back”. The — amount cut, or the vacancy cut-back, is a lump sum total cut in salaries that is applied to an activity, to reduce the salary amount in the activity. The reduced salary amount is what is budgeted in each activity to fill vacant positions. • Contract employees Notation on where (if it is known) contract employees will — be used to fill vacant positions. When this occurs, the salary funds budgeted for the vacant position becomes the source of funding for the contract hire. • Department total, by fund At the end of the list for each department and — agency, a compilation of (1) the total estimated cost of vacancies, (2) the total amount cut and (3) the total amount budgeted for vacant positions, are calculated and shown for each fund budgeted in the department. DEPT. COM. 131

- 2. The Honorable Nestor R. Garcia, Chair and Members of the Budget Committee March 8,2010 Page Two Additionally, the information included here represents a “snapshot” of each department and agency’s best estimate for filling vacant positions in FY 2011, based on its vacancies as of January 31, 2010. The actual filling of vacant positions is very dynamic and dependent on (1) the department and agency’s operational needs and priorities, which fluctuate due to changes in program requirements during the course of a fiscal year, and (2) the availability of funding in the department, via budgeted funds, or from funds due to future vacancies. Therefore, the actual filling of positions in FY 2011 may not result exactly as listed on the attachment. If you have any questi call me at 768-3901. RM/DC:jkk Attachments FORWARDED: Kirk W.Caldwell Managing Director

- 3. LIST OF VACANT POSITIONS AS OF 1/31/2010 FUND SCHED/ CLASSIFICATION TITLE POS DATE OF PERMI ESLc~~LLAMOUNT AMOUNT r~ FILL POS JABOLISH POS GRADE NUM VACANCY TEMP OF VACANCY CUT BUDGETED (YIN) (MO/YR) (YIN) (MO/YR) ~ NF= NEVER L FILLED DEPARTMENT OF BUDGET AND FISCAL SERVICES __I __ 4CTIVITY: ADMINISTRA TION SENIOR CLERK TYPIST DF4301 2/17/1999 P $ 27,756 $ - - — Y 7/il_____ GN I SR26 ACCOUNTANT VI — DF568 ________ $ 55,488 $ ~Y6Ii1_4 TOTAL GENERAL FUND= $ 83,244 $ (83,24~ 4Cr! VITY: ACCC UNTING & FISCAL SERVICES GN SR24 ACCOUNTANT V DF192 11123/2009 I $ 57,708 $ 42,145 Y 10/10 N GN SRi 5 PRE-AUDIT CLERK III DF231 1/4/2010 P $ 46,188 $ 46,188 Y 2/10 N ________ GN SR13 PRE-AUDIT CLERK II DF243 12/31/2003 P $ 31,212 PRE-AUDIT CLERK I DF246 6/30/2009 P $ 28,836 GN SR13 PRE-AUDIT CLERK II _____ DF261 _________ 12/31/2003 P $ 31,212 v~1tiijt~ ACCOUNTANT VI ___________ __________ DF305 _________ 2/1/2010 P $ 82,128 $ 55,500 Y 4/10 N GNISR22 ACCOUNTANT IV __________ DF306 10/29/2007 T P $ 45,576 G~3 PRE-AUDIT CLERK II __________ DF366 12/18/2006 P $ 31,212 GN SR13 SENIOR ACCOUNT CLERK DF186 12/31/2003 L 31,212 GN SR28 FISCAL OFFICER II DF187 12/31/2003 P ~ 62,424 GN SR22 ACCOUNTANT IV ~~9J~/1/201O P $ 67,488 $ 45,576 Y 4/10 N ________ GN SR2O ACCOUNTANT III DF369 6/1/2007 P $ 42,132 $ 42,132~ Y _____ GN SR2O ACCOUNTANT III DF549 2/1/2005 P $ 42,132 GN SR2O ACCOUNTANT III DF666 12/1/2009 P $ 55,488 TO [AL GENERAL FUND =1 $ ~9~~42~A407) ACTIVITY: PURCHASING GENERAL SERVICES & GN SR12 PROCUREMENT & SPECIFICATIONS CLERK II DF172 7/8/2008 P -- 30,036 GN ] SR2O PROCUREMENT & SPECIFICATIONS SPECLALIST III ~ñ~T9Ii6/2008 I P $ 45,576 GN SR2O PROCUREMENT & SPECIFICATIONS SPECIALIST III DF228 8/1/2009 P 62,424 GN SR13~PURCHASING CLERK II DF233 ~200~JP -~ 31,212 GN SR2O PERSONAL PROPERTY MANAGEMENT SPECIALIST I DF238 5/14/2008 P $ 42,132 ~ —:T-_~ ___ TO [AL GENERAL FUND = $ 211,380 (215,009) ~iii ~3~) ____ ACTIVITY: TREA~~JRY GN GN SR26 ACCOUNTANT VI SR22 ACCOUNTANT IV ___________ DF134 DF151 6/612008 12/1/2006 P P $ $ 55,488 45,576 $ $ - - N N ___N —Hr GN 5R13 SENIOR ACCOUNT CLERK DF263 5/16/2009 P $ 31,212 $ 31,212 Y 4/101 N I -j $ GN GN GN EMO7 ASST CHIEF OF TREASURY SRI3 SENIOR ACCOUNT CLERK SR13 SENIOR ACCOUNT CLERK DF571 DF578 DF737 12/1/2007 10/1/2009 6/3012009 P P P 82,176 32,424 31,212 $ $ 3~424 - 31,212 I N Y Y ~N 4/10 N T 1 of 82

- 4. LIST OF VACANT POSITIONS AS OF 1/31/2010 ~ I I FUND SCHED/ CLASSIFICATION TITLE POS DATE OF FERM/ EST. COSTJ~~OUNT AMOUNT FILL POS ABOLISH POS GRADE NUM VACANCY I TEMP OF VACANCY CUT BUDGETED (YIN) (MO/YR)jy~~jJ(MO/YR) NF= NEVER . FILLED DEPARTMENT OF BUDGET AND FISCAL SERVICES - - — - - - -- - GNL SR2O ~ACCOUNTANT III I DF742 2/1/2010 F 62,424 $ 62,424 Y L 5/10 N - GN I SR2OIACCOUNTANTIII NEW NF P 42,132 $ - N N TOTAL GENERAL FUND = 382,644 $ (225,372) $157,272 — I I___ I ~ -- --- - ACTIVITY: REAL PROPERTY —~ -~______ I — GN SR12 TAX CLERK ~4~F435 7/8/2008 P 30,036 $ 30,036 Y T~7io N GN JT~ PROFESSIONAL TRAINEE I DF438 8/17/2006 P 36,024 $ 3~024 Y ~7~fö~ N GN 1SR2~PROPERTY VALUATION ANALYST III DF441 P Th7~7~o~T 67,488 $ - N GN I SR16 REALPROPERTYAPPRAISERIV DF470 8/11/2009 P 60,036 $ 36,024 Y 4/10 N 1 5R16 REAL PROPERTY APPRAISER IV DF477 9/1/2009 P 62,424 $ 36,024 Y 4/10 I N GN 5R22 REALPROPERTYAPPRAISERIV — DF480 I 2R7~öThTI~ 49332 —— $ 360241 Y 4/10 L~ ~ REAL PROPERTY APPRAISER ASST II DF559 12/1/2009 P $49,932 — $30,0~1_ Y 5/10 N GN SRO9 DRAFTING TECHNICIAN I DF614 4/1/1993 P 26,700 $ - I N I N GN SR12 REALPROPERTYAPPRAISERASSTI — DF622 6/16/2009 P 30,036 $ 30,036J Y 4/10 N GN SR21 SUPVG DRAFTING TECHNICIAN DF443 12/31/2002 P 42,684 $ — I 42,684 Y* 7/10 N GN SR17 DRAFTINGTECHNICIANV DF445 6/1/2009 P 36,516 $ 3ëi~I~1 ~* 7/10 N GN SR17 DRAFTINGTECHNICIANV DF447 i2/3i7~ö~~~ 36,516 $ -- N GN SR11 - DRAFTING TECHNICIAN II DF448 i2I3~9~1~ 28,836 $ - N -~ N GN SR17 GIS CARTOGRAPHIC TECH I DF449 12/1/2009 P 48,048 $ 36,516~~~ 4/10 N GNJSR15 DRAFTING TECHNICIAN IV —~________ DF450 12/31/2004 P — 33,756 $ N~J, N GN DRAFTINGTECHNICIANII 5Rli J3F451 1~7I&200~~ 28,836 - $ - N N GN ~5Ri5DRAFTING TECHNICIAN IV DF454 8/24/1998 $ JTh 33,756 I $ - N I N GN SR17 GIS CARTOGRAPHIC TECH I DF455 9/9/2008~ P $ ~ $ 36,516 Y 47öJN GN SR11 DRAFTING TECHNICIAN II DF615 11/18/2000 P 28,836 I $ - N N GN SRO8 CLERK TYI~ST — — DF460 37~20öJ~~ - 25,668 -- $ - N --_____ JI~ TAX CLERK DF492 5/1/2005 P $ 30036 $ — N N GN I SR12 TAX CLERK DF494 5/19/2009 P $ 30~I36 L $ - 3,635 Y 5/li N GNJ~T~ TAX CLERK DF496 6/16/2009 P $ 30,0361 $- N N GN SRO8 CLERK TYPIST ~I DF516 3/24/2008 P $ 25,668 - N I — TOTAL_GENERAL FUND = $ 907,752 $ (517,681) $ 390~D71 J -— ACTIVITY_LIQUOR COMMISSION - - — 1~ LC SR24 SUPVG LIQUOR CONTROL INVESTIGATOR I DF280 7/1/2006 P $ 48,048 $ 4~048 Y* I 10/10 N LC SR21 LIQUOR CONTROL INVESTIGATOR III DF283 4/16/2002 P $ 42,684 $ 42,684 L lII1?L10 N LC SR21 LIQUOR CONTROL INVESTIGATOR III DF288 3/8/2007 P $ 42,684 $ 42,684 L Y* 12/10 N LC SR18 LIQUOR CONTROL INVESTIGATOR II DF289 ~7~0ö~7 P $ 37,968 $ 37,968 Y* 9/10 N LC SRI6 LIQUORCONTROLINVESTIGATORI DF291 12/23/20~çJ~ $ 35,076 $18,584 Y I 12/10 N LC SR16 LIQUOR CONTROL INVESTIGATOR I DF292 6/6/2007 P $ 35,076 $ - J~ N 2 of 82

- 5. LIST OF VACANT POSITIONS AS OF 1/31/2010 I r~ ~ 1~ FUND SCHED/ - — CLASSIFICATION 1TLLE jj~OS DATE OF PERM/J EST. COST AMOUNT AMOUNT FILL POS ABOLISH POS GRADE NUM VACANCY ~TEMP I OF VACANCY CUT BUDGETED [(YIN) (MO/YR~’7~ii[~MO/YR) NF= NEVER I ~ FILLED DEPARTMENT OF BUDGET AND FISCAL SERVICES 1/19/2005 — P LC SR16 LIQUOR CONTROL_INVESTIGATOR I DF294 $ 35~376______ Y~ I. 5/10 LC I SR22 LIQUOR CONTROL AUDITOR II — DF295 6/1/2005 P -~ 45~5~J 45,57~JY*I — 10/10 N — LC SR16 LIQUOR CONTROL INVESTIGATOR I DF296 6/5/2007 P $ 35,076 7 Y~ I 12/10 !L ACCOUNTANT Ill _________ DF297 6/1/2007 P -j~ 42,i32~ — !~ 42,i32t Y LiLi~ ~ LC SR21 LIQUOR CONTROL INVESTIGATOR III DF298 1/4/2002 $ 42,684 $ 42,684 - I 3/10 N — LC SR21 LIQUOR CONTROL INVESTIGATOR III DF299 2/8/2007 I$ 42,684 - $ 42,684t ~* 7/10 N LC SR16 LIQUOR CONTROL INVESTIGATOR I DF339 5/10/2008 P $ 35,076 35,076 ~ ~Iö N LC SROB CLERK TYPIST DF342 I 3/24/2008 P - ~ 25,668 $ 25,668 Y 3/10 N LC EMO1 ADMINISTRA11VE SERVICES OFFICER I _____ DF346J 3/24/2009 P $ 61,320 $ 61,320 Y* 9/10 N LC SR18 LIQUOR CONTROL INVESTIGATOR II DF371 2/23/2009 P $ 37,956 $ 37,956 Y - 5/10 L±L - ±c1 I LC SR2O SR21 LIQUOR CONTROL AUDITOR I LIQUOR CONTROL INVESTIGATOR III -. DF522 DF586 6/1/2005 2/29/2008 P 42,132 $ $ 42,132 42,684 - Y* _____________ N 12/10 10/10 I ____________ N — 42,684 LC SRi 6 SECRETARY III DF669 6/1/2009 P 35,076 $ 35,076 Y 6/10 __________ N - LC SRi 6 LIQUOR CONTROL INVESTIGATOR I -~ DF714 2/10/2008 P $ 35,076 $ - N ___ N LC SRi 6 LIQUOR CONTROL INVESTIGATOR I -~ DF723 2/1 0/2008 T $ 35,076 $ N -- LC SR16 LIQUOR CONTROL INVESTIGATOR I DF724 4/16/1999 T $ 35,076 $ - N N TOTAL LIQUOR COMMISSION FUND= ~ 869,904 $ (156,796) $ 713,108I_ - ACTIVITY: FISCAUCIP ADMINISTRATION GN I SR24 FISCAL ANALYST II DF966 8/2/2008 __~~ P ~$ 51,312 $ 15,237 Y 3/il ~_ N T0 AL GENERAL FUND = $ 51,312 ________ !~ (36,075) $ 15,237 ______ CD I SR22 PLANNER IV DF972 I 1/27/2006 P I$ 45,576 $ 45,576 5/10 N CD SR26 PLANNER VI NE’A~f NF ~ I$ 55,500 j~ 55,500 5/10 TOTAL COMMUNITY DEVELOPMENT FUND = $ 101,076 $ ~ 101,076 _ H1 EST. COST OF VACANCY AMOUNT CUT AMOUNT BUDGETED GENERAL I $ 2,291,280 $ (1,500,788) $ 790,492 LIQUOR I $ 869,904 $ (156,796) $ 713,108 -i COMMUNITY DEVELOPMENT DEPT TO L ______ I$ I 101.076 I $ 3.262.260 $ (1.657.584) $ 101,076 $ 1.604.676 -r - - COMMENTS: _________ ADMINISTRATION ___________ _______ ____________ _________ ________ _____ _______ GN SR1O DF430 - Senior Clerk Typist- If budget allows, position will be filled to handle increase workload due to Advantage HR and Security Access requirements. ________ GN SR26 DF568 - Accountant VI - If budget allows, position will be filled to provide support for the C2HERPS financial system. I I 3 of 82

- 6. LIST OF VACANT POSITIONS AS OF 1/31/2010 P I I -T I FUND SCHEDI - — CLASSIFICATION TITLE -— POS DATE OF PERM/ EST. COST p AMOUNT -- —- AMOUNT L -- FILL POS ABOLISH POS I I GRADE — NUM VACANCY ~jO~ACANCY CUT BUDGETED I (YIN) (MO/YR) (YIN) (MO/YR) NF= NEVER I P~ FILLED DEPARTMENT OF BUDGET AND FISCAL SERVICES H - - P - -- - —J -- ACCOUNTING&FISCAL SERVICES -- - - — -- -- I -- I - - - ~ SR15 DF231- Pre-Audit Clerk III - Position filled in February 2010. DF305 - Accountant VI - Waiting for approval of exemption to fill. This is a critical position in the payroll section. Incumbent had over 30 years with the City. Anticipate filling position at a lower step. ~ —_________ -- — J L - GN SR22 DF220 - Accountant IV- Request to fill approved. Waiting for list of candidates from DHR. Incumbent retired with over 30 years of service with the City. Anticipate fillingpositionatalowerstep. —_______ — -- I I - GN SR2O DF369 - Accountant Ill - Interviews have been scheduled. I I I I - - F -_ II L - PURCHASING — -—______ I_____ — - ~J - -- GN SR2O DFI73 - Procurement & Specifications Specialist Ill - Interviews conducted and selection made. GN 5R20 DF228 - Procurement & Specifications Specialist III - Interviews conducted and selection made. I I ~ii11H_ I I II -- - - TREASURY -- -- - — —~ -- - -- G~1J SR26 DF134 - Accountant VI - Position will be filled as soon as funds are available. Needed for City investments and financing. GN I SR22 DFi5i- Accountant IV - Position will be filled as soon as funds are available. Only specialist for bond financing. SR13 DF263 - Senior Account Clerk - Recruiting for position. Expect to fill in April 2010. — I I IIIIIILIIIIIIII[1 - — - - —— ON I EMO7 DF571- Asst Chief of Treasury - Position will be filled as soon as funds are available. Needed to support Treasury operations. -_____________ -~ — GN 1 SR13 DF578 - Senior Account Clerk - Recruiting for position. Expect to fill in April 2010. 1 REALPROPERTY ~lluiiE~fl_~iIf~ GNT SR16 DF438 - Professional Trainee I- Waiting on recruitment and pending interviews. Expect to fill in July 2010 ~i~ii~i — - j — DF441- Property Valuation Analyst III - position needed to fulfill inter-governmental agreement (IGA) with neighbor islands. I SR16 DF470 DF477 - - Real Real Property Appraiser Property Appraiser IV - Recruitmentwill be at entry level Real Property Appraiser I. Expect to fill in April 2010. IV - Recruitmentwill be at entry level Real Property Appraiser I. Expect to fill in April 2010. - J~IJ~ I . - GN[ SR22 DF480 - Real Property Appraiser V-Recruitment will be at entry level Real Property Appraiser I. Expect to fill in April 2010. — - I SR14 DF559 - Real Property Appraiser Asst II - Recruitment will be at entry level Real Property Appraiser Ass~TJJ J~TLL SR12 DF622 - Request to fill approved, awaiting external list. I I I —I——— -- — -______ — —— GN SRI7 DF449 - GIS Cartographic Tech I- Request to fill approved and pending list for interviews. Expect to fill by April 2010. - ON SR17 DF455-GIS Cartographic Tech I - Request to fill approved and pending list for interviews. Expect to fill by April 2010. —_______ —______ covered by interim contract *p~5itions I -_____ —— -- —- ** Anicipated savings from future vacancies will be utilized to cover the cost of filling positions - I I I. -- -- -. - - - - -_ 4 of 82

- 7. LIST OF VACANT POSITIONS AS OF 1/31/2010 I - I 1 FUND I SCHED/ CLASSIFICATION TITLE POS DATE OF PERM/ EST. COST AMOUNT AMOUNT FILL POS ABOLISH POS GRADE NUM VACANCY TEMP OF VACANCY CUT BUDGETED I (YIN) (MO/YR) I(Y/N) (MO/YR) NF= NEVER I FILLED ~ DEPARTMENTOFCOMMUMTYSERVICES T liii - I~I~ iii ACTIVITY:_ADMINISTRATION — - - - 3110 GN[ EMO3 1ADMINISTRATIVES~Yj~ESOFFICERII HR716 L~I~22~ P $ 67,60~r $ 56,764 V L~ N ~rI SR1OISENIORCLERKTYPIST HR547 T 11/17/2009 T - $ 27,756 $ - NI I N . I I TOTAL GENERAL FUND = $ 95,364 $ (38,600) $ 56,764 . ii Th~ ACTIVITY:_OFFICE OF SPECIAL PROJECTS I GN EMO8 EXECUTIVEASSTII (APPROX.80%GENERALFUND) HR608 I 1/16/2008 P $ 69,014 I$ 45,452 Y 07/10 N ON SR2O PLANNER Ill HR476 F 1/21/2006 TOTALGENERALFUND= P - $ $ 42,132 111,146 $ J~ $ (65~94) $ - 45,452 ~J Y~ 01/li N CD EMO8 EXECUTIVEASSTII (APPROX. 20% CDBG FUND) HR608 1/16/2008 P $ 17,254 $ 17,254 Y 07/10 N CD SR26 PLANNER VI HR519 12/1/2000 T $ 55,500 $ 55,500 N 06/10 N CD SR24 PLANNER V HR515 12/1/2009 - T $ 51,312 51,312 Y 04/10 N CDJ~SR19 PLANNERI NEW NF F $ 36,027 36,027 Y 07/10 N CD SRI9 PLANNER I NEW NF P $ 36,027 36,027 N 07/10 N TOTAL CDBG FUN~ $ 196,120 $ - $ 196,120 FG LSR22 PLANNER IV NEW NF P $ 45,576 $ 45,576 Y 07/10 N FG SR2O COMMUNITYSERVICESSPECIALISTIII —- HR526 I 12/31/2009 I $ 42,132 42,132-- Y* 07/10 N FG SR16 COMMUNITYSERVICESSFECIALISTI NEW NF J I $ Y* 07/10 FG SRO8 CLERKTYPIST HR517 10/1/2009 r I $ 36,024 25,668 J 36,024 25~68 ~P1 N N FG SR22 COMMUMTYSERVICESSPECIALISTIV - --______ HR533 ~1iI6/2008 $ ~1 45 ~Lj_______ ±L FG SR2O COMMUNITY SERVICES SPECIALIST II HR534 6/16/2009 T $42,132 $42,132 - N N FG SR2O — COMMUNITY SERVICES SPECIALIST Ill HR535 10/1/2009 T $ 42,132 I 42,132 N N FG SR2O PLANNER III NEWII NF T $ 42,132 42,132 N N FG SR2O PLANNER III NEW NF T $ 42,132 - 42,132 N - N FG SR26 COMMUNITY SERVK~ESSPECIALIST VI HR357 3/31/2000 — P $ 55,500 $ 55,500 N N FG SR2O COMMUNITY SERVICES SPECIALIST Ill — HR523 12/31/2009 T $ 42,132 - - $ 42,132 N N FG FG SR24 SRI8 COMMUNITYSERVICESSPECIALISTV PLANNER II — HR525 NEW ~ 11/6/2008 1 $51,312 $ 38,988 — $ $ ~ 1~Th Y* 7/10 N — - 38,988 FG SR1O SENIORCLERKTYPIST NEW NF TOTAL FEDERAL GRANTS FUND =1 I $27,756 $ 579,192 ~$ - $ $ 27,756 579,192 Y* 7/10 N ACTIVITY:_OAHUWORKFORCEINVESTMENTBOARD ~_____ ~J FG SR22 PLANNER IV NEW NF T $ 45,576 $ 45,576 N I N FG SR1O SENIORCLERKTYPIST ~JJJ~JJ~ T $ 27,756 $ -- 27,756 N -- N FG SR2O OFFICE MANAGER I NEW NF I T $ 42,132 $ 42,132 N F I N 5 of 82

- 8. LIST OF VACANT POSITIONS AS OF 1/31/2010 — ~I -- - 1 - I I - - FUNDr SCHED/ CLASSIFICATION TITLE POS DATE OF PERM/ EST. COST AMOUNT AMOUNT I FILL POS ABOLISH POS J GRADE — — NUM VACANCY TEMP OF VACANCY CUT BUDGETED I(YIN) (MO/YR)1 (Y/NiJ (MO/YR) I NF= NEVER FILLED I ARTM OF COMMUNITY SERVICES - - -—_______ - --_______ - - -_________ FG SR24 PLANNER V NEW NF I $ 51,312 I$ 51,312 N I N fI1io~ FG SR22 Deptl Staff Asst PLANNER IV -- NEW NF NF I — T $ $ 74,556 45,5761 - JI$$ 74,556 45,576 Y* N - 7/10 -— —J ~ — - -— FG SRO8 CLERKTYPIST — — NEW -~ - NF JT ~ i~P~~J~JJJ 25668 N1 — LN TOTAL FEDERAL GRANTS FUND = $ 312,576 $ - $ 312,576 ACT! VITY: ELDERLYSERVICES I I I GN SRO7 COMMUNITY SERVICE AID HR707 7/1/2008 T $ 12,324 J$ - N N GN SRO7 COMMUNITY SERVICE AID — HR737 ~ 9/1/2009 — T - $ 12,324 ~ 4,180 Y 3/il — N - - - TOIALGENERALFUND= $ 24,648 $ (20,468)J$ 4,180 SP~ SRO7 COMMUNITYSERVICEAHJ —~ HR424 .j8/16/2008 I $ 24648~ -~ $ 24648JY 7/10 N SF SF I SRO7 SRO7 COMMUNITY SERVICE AID COMMUNITY SERVICE AID HR505 HR507 I 4/30/2005 6/3/2005 1 T $ $ 24,648 24,648 $24,648 $ 24,648 L~ Y 7/10 7/10 — N N SUPVG COMMUNITY SERVICE AID - ~T7Th7~ö~ I $ 31,2l~~ - ~ 31,212 Y4 7/10 - I — - TOTAL SPECIAL PROJECTS FUND = -~ $ 105,156 1$ - - $ 105,156 I I - -- — 1 ~1 I FG SR22 SR22 PLANNER P1 PLANNER IV —- NEW HR715 I NF - 7/1/2009 I P $ $ 45,576 45,576 I $ $ 45,576 45,576 Y 7/10 Y 7/10 - N N FG SR24 PLANNER V HR718 9/26/2009 F $ 51,312 $ 51,312 V 3/10 N FG SRO8 CLERKTYPIST — ~ $ 25,668 - - $ 25,668 Y N 1 ~J~20 PLANNER Ill - HR485 12/31/2006 P $ 42,132 $ 42,132 Y 7/10 N - - TOTAL FEDERAL GRANTS FUND— - - $ 210,264~$ - - $ 210,264 ~ ACTIVI~:WORKHAWAII - FG SR2O HOUSING ASSISTANCE SPECIALIST Ill NEW NF I $ 42,132 $ 42,132 — Y I 12/10 N FG SR18 HOUSINGASSISTANCESPECIALISTH NEW I NE T $ 38,988 - $ 38,988 Y r I —______ FG SR1O SENIOR CLERKTYPIST NEW NF I $ 27,7561 $ 27,756 N 12/10 N FG SR2O JOB RESOURCE SPECIALIST Ill HR330 I 1/7/2010 T $ 42,132 I $ 42,132 Y 12/10 - N FG SR22 JOB RESOURCE SPECIALIST IV HR344 I 8/31/2002 - P $ 45,576 F $ 45,576 V 12/10 N EG SR22 JOB RESOURCE SPECIALIST IV HR356 I 7/1/2009 P $ 45~76 1 - F$ 45,576 Y J12/10 N FG SR12 SUPVG CLERK — - HR409 8/1/2008 P - $ 30,036 $ 30,036 Y J 12/10 N FG SR12 STATISTICSCLERKU I-1R410 12/11/2007 - P $ 30,0361 1~ 3Q036 Y 12/10 N FG SR2O JOB RESOURCE SPECIALIST Ill HR448 J 12/31/2009 1 $ 42,132 5 42,132 Y 12/10 N FG SR2O JOB RESOURCE SPECIALIST Ill HR461 3/7/2009 1 $ 42,132 - — - 1$ 42,132 N ~ FG SR2O COMMUNITYSERVICESSPECIALISTIII HR463 2/1/2008 1 $ 42,132 42,132 N N EG SR2O COMMUNITY SERVICES SPECIALIST Ill HR~Th/6/~j I $ 42~~~Jj 42132 N - N 6 of 82

- 9. LIST OE VACANT POSITIONS AS OF 1/31/2010 — I -- - 1 I I - I SCHED/ - -- CLASSIFICA11ON TITLE -- POS DATE OF FERM/ EST. COST AMOUNT AMOUNT FILL POS J —ABOLISH ~LGRADE — -- - TEMP OF VACANCY CUT .IBUDGET~Y/~JMO/YR) ~N~MO/YR~ DEPARTMENT OF COMMUNITY SERVICES _____ b __ EG SR2O PLANNER Ill HR557 N/F T $ 42,132 I L~ 42,132 Y* 12/10 N FG SR22 _____ JOB RESOURCE SFECIALIST IV HR559 - N/F I ~ 45,576 L~ 45,576 /1 N EG SR24 PLANN ER V HR843 12/1/2000 F $ 51,312 I~ - . ~ 1/10 - N FG SR2O JOB RESOURCE SPECIALIST III HR809 — N/F I 42,1321 $ 42,132 ~~Yi !1Q L N EG SR2O JOB RESOURCE SPECIALIST Ill HR81O N/F $ 42,132 F — I$ 42,132 Y J 6/10 N EG SR2O JOB RESOURCE SPECIALIST III HR81 I N/F I $ 42,132 I$ 42,132 V 12/10 N EG SR2O JOB RESOURCE SPECIALIST Ill HR812 N/F T $ 42,i32~ $ 42,132 Y 12/10 N -----r 42,132 EG SR2O JOB RESOURCE SPECIALIST III HR813 N/F I $ 42,132 5 N EG SR2O -- JOB RESOURCE SPECIALIST Ill HR814 N/F I $ 42,132 $ 42,132 N EG SR2O JOB RESOURCE SPECIALIST Ill -~ HR815 N/F I $ 42,i32~ ~~__ — $ 42,132 y~~~j_ 12/10 N EG SR2O JOB RESOURCE SPECIALIST Ill HR816 N/F I $ 42,132 $ 42,132 - V 12/10 N EG SR2O JOB RESOURCE SPECIALIST III HR817 N/F - I $ 42,132 F_ -- 5 42,132 Y - 12/10 N EG SRO8 CLERK TYPIST HR973 N/F I $ 25,668 $ 25,668 2/10 N EG SR2O JOB RESOURCE SFECIALIST III NEW NF I ~!.. 42,132 $ 42,132 Y 12/10 N EG SR2O JOB RESOURCE SPECIALIST Ill NEW 1 NE I $ 42,132 I $ 42,132 Y 12/10 N FB SRi 8 JOB RESOURCE SPECIAL 1ST II NEW _____ NE I $ 38,988 $ 38,988 Y 12/10 N TOTAL ~EDERALGRANTS FUND $ 1,137,888 F $ _$ 1,137,888 T ACTIVITY: COMfy UNITY ASSISTANCE GN EMO8 HOUSING SERVICES ADMIN HR9O1 1i2/31/2009 P $_ 86,268 -— $ 86,268 Y 4/10 N GN SR26 REHABILITATION LOAN OFFICER HR911 — 12/31/2009 F ~ 55,500 I — 5 28,984 Y I 4/10 N TOTAL GENERAL FUND = $ 141,768$ (26,516) !~.. 115,252 SP SR22 REHAB LOAN SPECIALIST I NEW NE I ~ 45,576 I i~ 45,576 Y 9/10 N SF SRO6 ASST CLERK TYPIST NEW NE I 5 25,668 $ 25,668 Y I 9/10 N TOTAL S ~ECIALPROJECTS FUND = $ 71,244 SE I SR22 -. FLANNER IV ___________ - HR496 I 12/31/2006 F $ 45,576 $ 45,576 Y* 12/10 N SE I SR18 COMMUNITY SERVICES SPECIALIST II HR509 f 7/16/2007 P $ 38,988 I $ 38,988 Y* 12/10 N SE SR2O COMMUNITY SERVICES SPECIALIST III HR512 - I 12/31/2009 P $ 42,132 $ 42,132 Y 12/10 N • SE SR18 JOB RESOURCE SPECIAIJST II -— HR521 12/11/2007 P $ 38,988 1 $ 38,988 YJ 12/10 N SE SR24 PLANNER V HR556 — 12/1/2009 P $ 51,312 $ 51,312 Y ] 3/10 N SE I SR28 HOUSING ASSISTANCE SPECIALIST VII HR921 2/1/2010 P 62,424 I —- $ 62,424f ~ N SE I SR19 URBAN REHABILITATION INSPECTOR I HR938 3/1/2008 F 39,480 ~ 1 x I~ SE I SR1O SENIOR CLERK TYPIST HR955 8/1/2009 P 27,756 $ 27,756 I 3/10 N SE ~ SR1O SENIOR CLERK TYPIST HR956 10/1/2009 P 5 27,756 $ 27,756 V 3/10 N SE I SRO8 CLERK TYPIST HR958 11/17/2009 P 5 25,668 $ 25,668 Y 5/10 Nf~ 7 of 82

- 10. LIST OF VACANT POSITIONS AS OF 1/31/2010 T I FUND SCHED/ CLASSIFICATION TITLE P05 DATE OF I FERM/ EST. COST AMOUNI AMOUNT I FILL POS ABOLISH POS — -- L GRADE —— NUM VACANCY [TEMP OFVACANOYI CUT I BUDGETED I (YIN) (MO/YR) (YIN) (MO/YR) F NEZ NEVER I FILLED DEPARTMENT OF COMMUNITY SERVICES SE SR22 JOB RESOURCE SPECIALIST IV HR967 7/1/2009 P $ 45,576 $ 45,576 Y* 12/10 N TOTAL SECTION 8fUND =1 $ 445,656 $ -s 445,656J~ -H -.- - -- r ___ ____ ACTIVITY: COMMUNITY BASED DEVELOPMENT EMO8 HOUSING DEVELOPMENT ADMIN —. i_i HR964 12/31/2009 P $ 86,268 $ 37,241 Y 12/10 N TOTAL GENERAL FUND~ $ 86,268 $ (49,027)I $ 37,241 IRK TYPIST HR560 i0/1/?009 I 25,668 $ 25,668 L I - N - !.~ ~ 10/10 ~IORCLERK TYPIST HR561 11/17/2009 L I $ 27,756 $ 27,756 Y* I 07/10 — - N TOTALCDBGFUND=J $ 53,424 $ - $ 53,424 — .- 1. ____ EST COST OF VACANCY AMOUNT CUT AMOUNT BUDGETED - I - - -J__ GENERAL $ 459,194 $ (200,305) $ 258,889 $ 249,544 0’ 5 249,544 SECTION 8 $ 445,656 Q 445,656 SPECIAL PROJECTS $ 176,400 0 $ 176,400 FEDERAL GRANTS $ 2,239,920 0 $ 2,239,920 DEFT TOTAL $ 3,570,714 $ (200,305) $ 3,370,409 ~The13 positions with an asterisk are currently covered by contract_staff. _____ ADMINISTRATION __________ ______ __________ -— 1. HR716 list received, pending interview and selection — — — 2. HR547 pending availability of General Funds —- _________ OFFICE OF SPECIAL PROJECTS ______ 1. HR608 incumbent to return to position —— 1 2. HR476 pending request to fill to DHR; anticipated savings from other vacancies will be utilized cover the cost of filling this position. I 3 HR519 pending request to fill to DHR r ________________ 4. HR515 list received, pending interview and selection I ________________ 1 ______ 5. NEW pending request to create and fill position to DHR __________ _____________ 6. NEW pending request to create and fill position to DHR ______________ —— __________ ——_________ 7. NEW pending request to create and fill position to DHR ______ _______ ____________ -- 8. HR526 position tobe filled by contract ________________-. .1 — - _______ — ________ 9. NEW position to be filled by contract 8 of 82