Downloaded 160 times

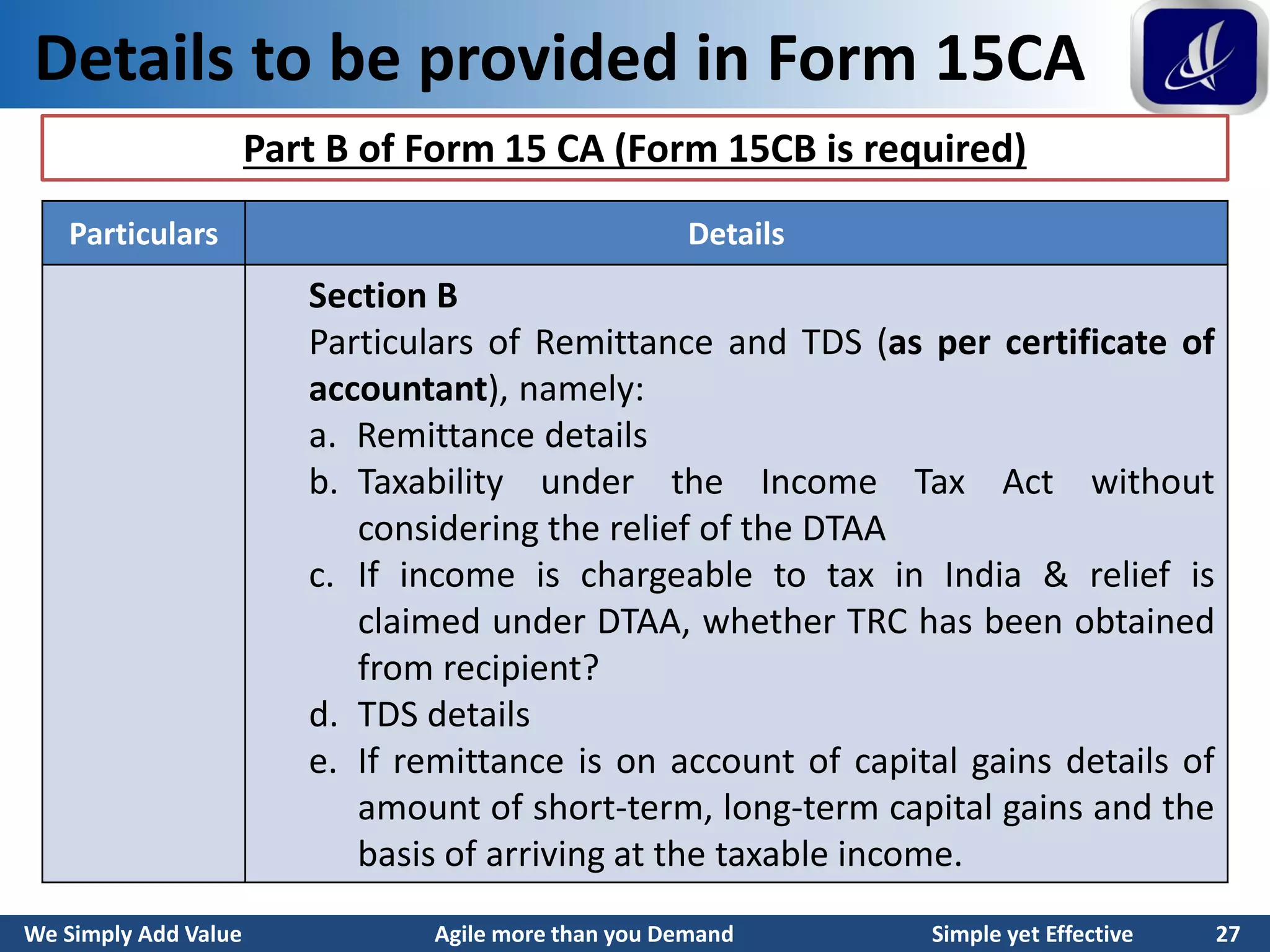

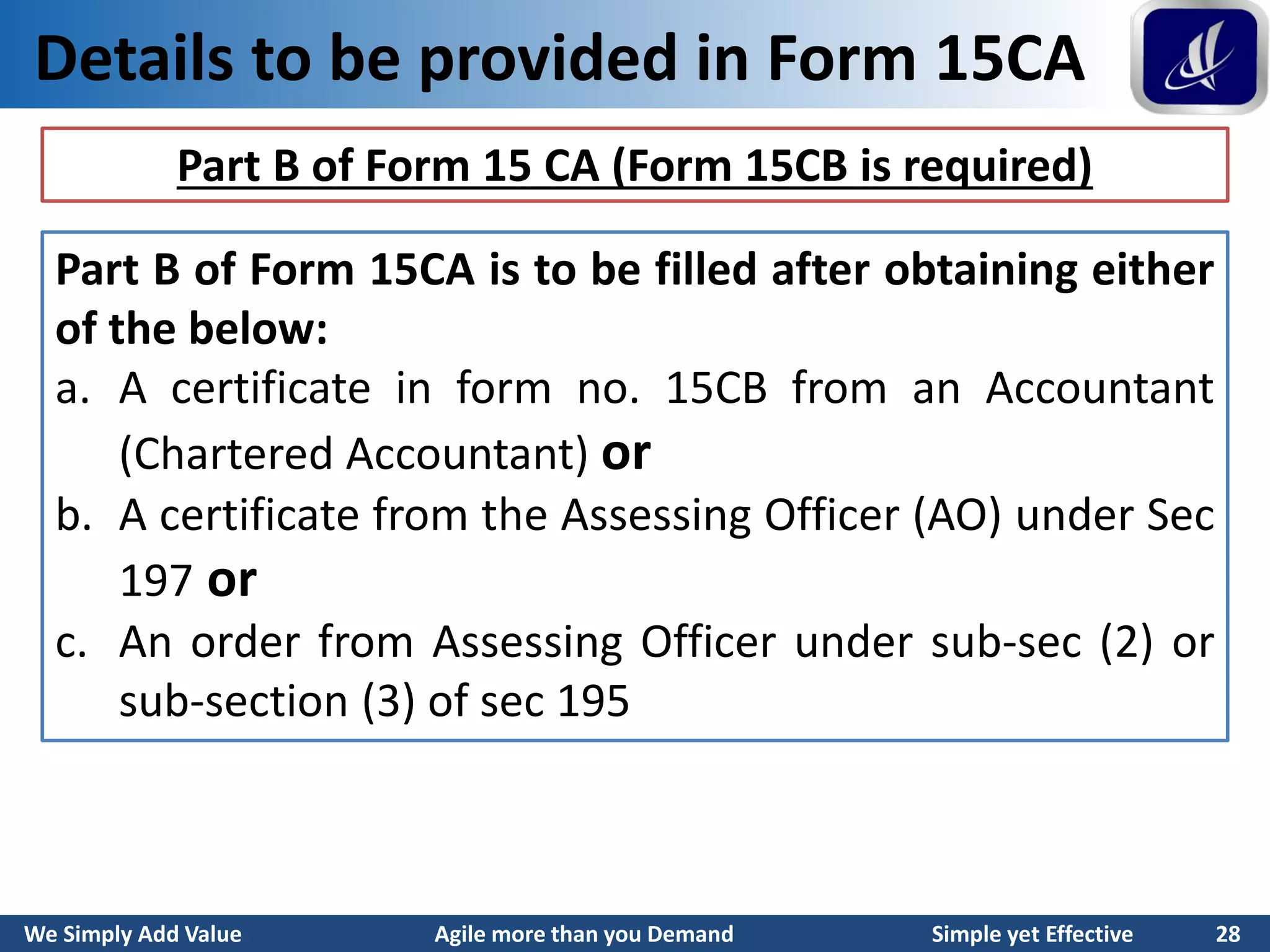

The document discusses the requirements and procedures for filing Form 15CA and Form 15CB for making payments to non-residents in India. Form 15CA is a declaration that must be filed by the remitter along with a certificate from a chartered accountant in Form 15CB when making remittances exceeding Rs. 50,000 or an aggregate of over Rs. 2,50,000 in a year. Form 15CA captures details of the remitter, recipient and remittance amount, while Form 15CB contains the chartered accountant's determination of taxability. Specific information to be provided in each form is outlined, including the remitter and recipient's identification details, bank transfer information