Downloaded 25 times

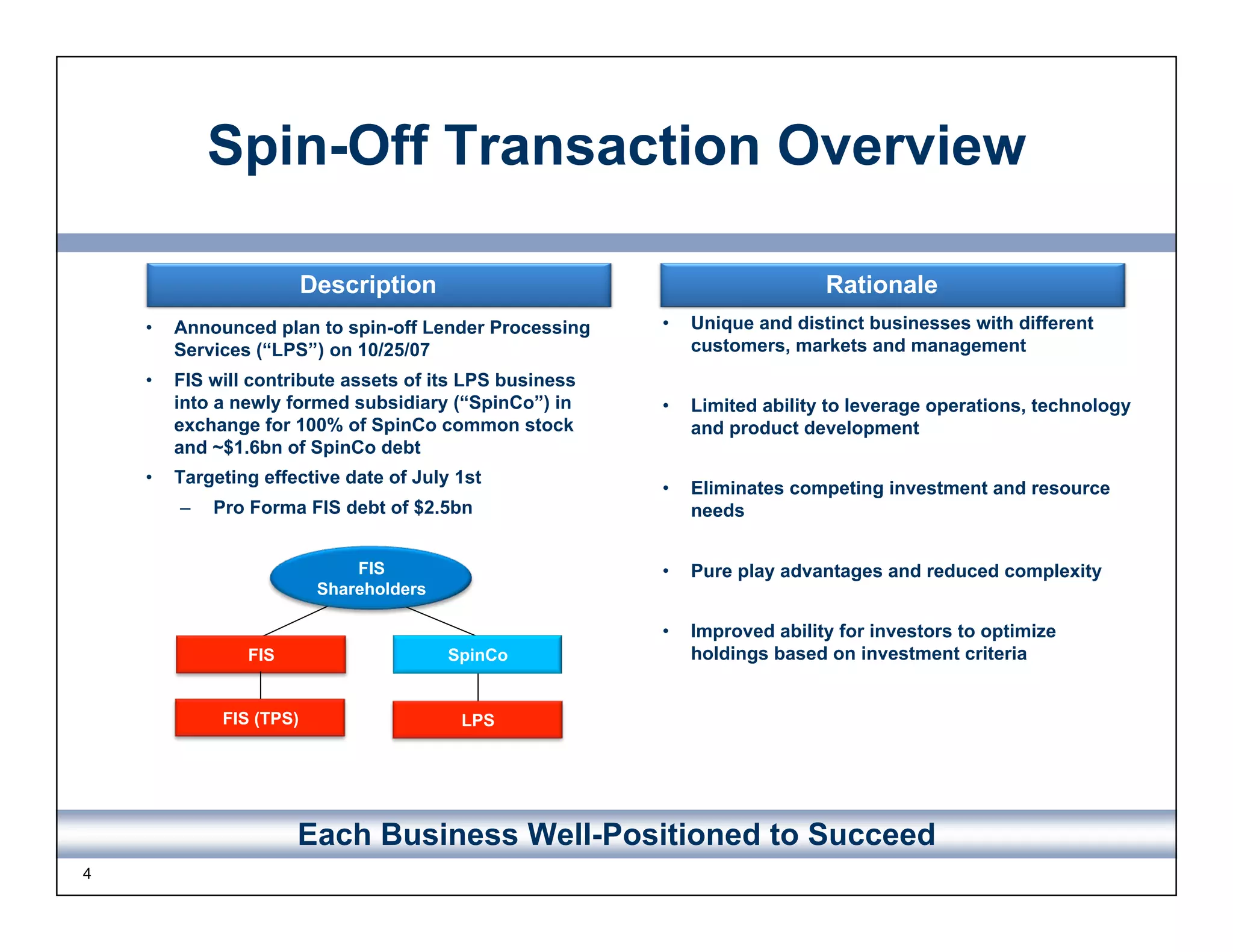

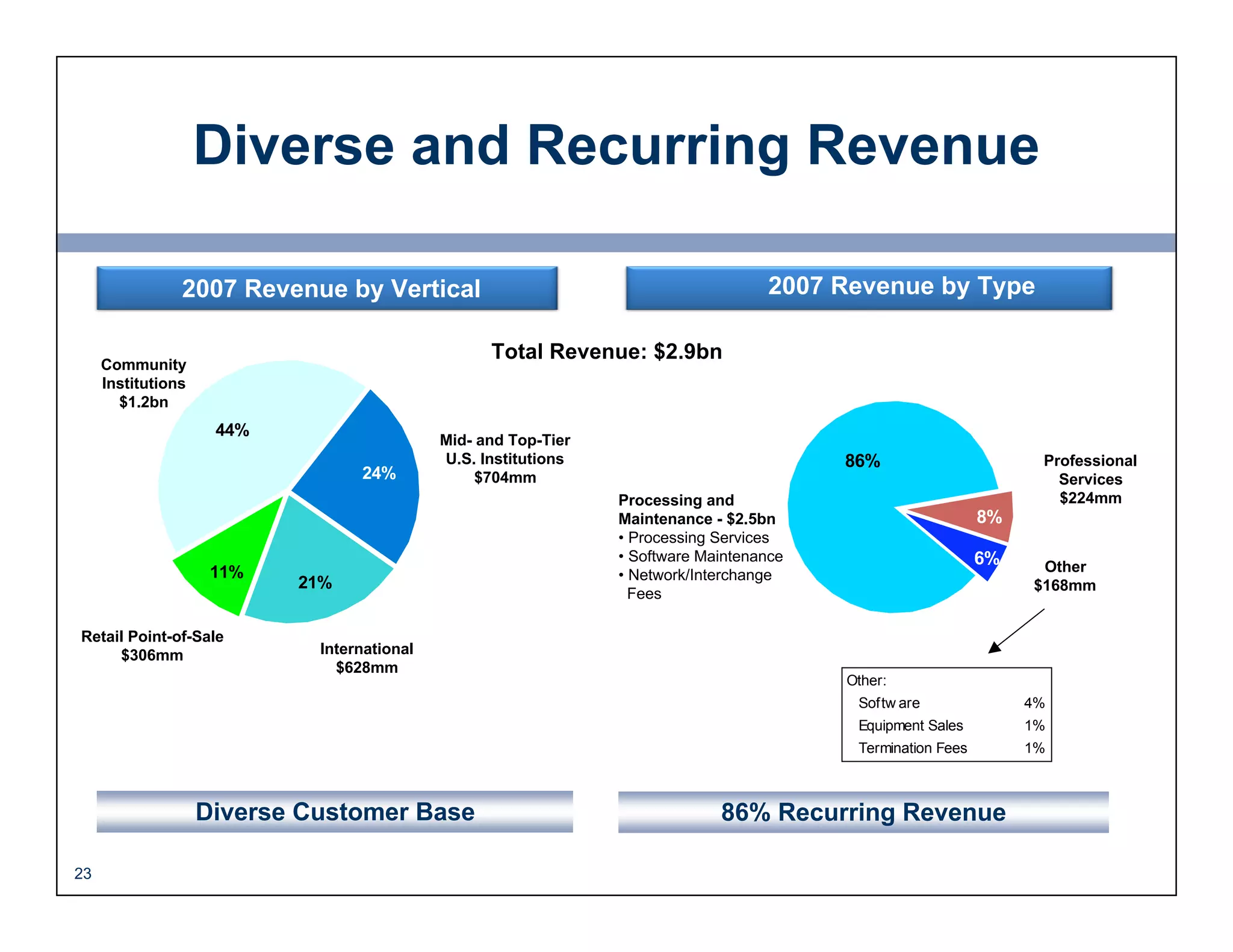

1) Fidelity National Information Services presented an investor presentation in June 2008 that discussed their planned spin-off of the Lender Processing Services segment. The spin-off was intended to create two pure play companies that could better focus resources and have improved investment profiles. 2) FIS overview highlighted their leadership in payments processing and core banking software, with $2.9 billion in annual revenues and significant scale across the US and international markets. 3) Financial highlights showed strong revenue growth, expanding margins, and increasing free cash flow that could be used to invest in growth, reduce debt, pursue acquisitions and return capital to shareholders.

![[参考情報]OSC広島のお知らせ](https://cdn.slidesharecdn.com/ss_thumbnails/20160730-osckyoto-tokaidolug-oschiroshima-160730051150-thumbnail.jpg?width=640&height=640&fit=bounds)