Financial project

•Download as PPT, PDF•

0 likes•215 views

This document analyzes various financial ratios of Triveni Engineering over a 10-year period from 2005-2015. It provides line charts and data for key ratios such as operating profit per share, operating profit margin, gross profit margin, cash profit margin, current ratio, quick ratio, interest coverage ratio, total debt to owners' fund, inventory turnover ratio, total assets turnover ratio, and material cost composition. The analysis shows most of these ratios trending downward over the 10-year period, with declining profitability, liquidity, and efficiency. The average inventory turnover ratio of 3.45 indicates inventory is not sold quickly.

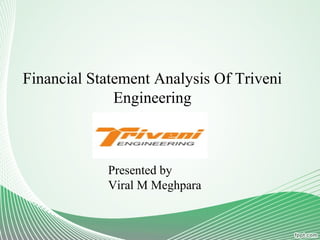

![Ratio And Trend Analysis

A] Investment Valuation Ratio

1] Operating Profit Per Share

This chart clearly show that company operating profit per share from 2005 to 2015,

which is very flexible in term of its profit. In 2005 it is 16.31% which comes down

to 8.02% in next year’s which again raises up to two years but after it continuously

showing A downward trend from 8.75% to 6.25% to 2.49% and finally at one point

of time it reaches even negative that is -0.70%.

Operating Profit 167.99 206.81 163.5 290.73 428.7 225.63 161.19 177.66 64.31 -18.08

Shares in issue (lakhs) 1,030.2

0

2,578.8

0

2,578.8

0

2,578.8

0

2,578.8

0

2,578.8

8

2,578.8

0

2,578.8

0

2,579.0

0

2,579.4

5

Operating Profit Per Share

(Rs)

16.31 8.02 6.34 11.27 16.62 8.75 6.25 6.89 2.49 -0.70

Industry comparison 21.09 22.29 17.40 18.29 25.98 20.62 29.22 17.62 9.42 6.67](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

Recommended

More Related Content

What's hot

What's hot (17)

Similar to Financial project

Similar to Financial project (20)

Financial project

- 1. Financial Statement Analysis Of Triveni Engineering Presented by Viral M Meghpara

- 2. Ratio And Trend Analysis A] Investment Valuation Ratio 1] Operating Profit Per Share This chart clearly show that company operating profit per share from 2005 to 2015, which is very flexible in term of its profit. In 2005 it is 16.31% which comes down to 8.02% in next year’s which again raises up to two years but after it continuously showing A downward trend from 8.75% to 6.25% to 2.49% and finally at one point of time it reaches even negative that is -0.70%. Operating Profit 167.99 206.81 163.5 290.73 428.7 225.63 161.19 177.66 64.31 -18.08 Shares in issue (lakhs) 1,030.2 0 2,578.8 0 2,578.8 0 2,578.8 0 2,578.8 0 2,578.8 8 2,578.8 0 2,578.8 0 2,579.0 0 2,579.4 5 Operating Profit Per Share (Rs) 16.31 8.02 6.34 11.27 16.62 8.75 6.25 6.89 2.49 -0.70 Industry comparison 21.09 22.29 17.40 18.29 25.98 20.62 29.22 17.62 9.42 6.67

- 3. B] Profitability Ratios 1] Operating Profit Margin(%) This line chart clearly indicate that the company overall operating profit margin throughout the period of ten years is falling from 17.41% from 2005 to 8.47 % in the year 2007 which is again going up for the another two years and at one point it has achieved the highest operating profit that is 22.26% which is highest among the entire ten year period, but thenafter, it came down to 10% and it continuously fell down and finally it end with A negative figure of -0.88 %. 1] Operating Profit 167.99 206.81 163.5 290.73 428.7 225.63 161.19 177.66 64.31 -18.08 Net Sales 964.64 1,191.9 8 1,929.4 6 1,611.9 7 1,925.8 3 2,256.6 6 1,707.7 6 1,859.4 5 3,153.3 6 2,061.0 1 Operating Profit Margin(%) 17.41 17.35 8.47 18.04 22.26 10.00 9.44 9.55 2.04 -0.88 Industry comparison 10.53 7.96 7.93 8.15 14.69 -2.06 -31.05 4.50 7.24 6.37

- 4. 2] Gross Profit Margin(%) This line chart show that the gross profit of triveni engineering in the year 2005 which is 16.13% is goes up to all time highest that is 18.91% in the year 2006 but then it fell down to 4.24% in 2007 and it again went up to 12.85% and 18.03% respectively in the year 2008 and 2009 and in 2009 it has achieved second highest gross profit. But soon after in next three years its gross profit margin fell down to 6.28% in the year 2010 followed by 4.68 and 5.16 % in the year 2011 and 2012. To make even worst its gross profit further fell to -1.72 and -3.75% in the year 2014 and 2015 respectively. 2] Gross profit 155.6 225.4 81.81 207.14 347.22 141.72 79.92 95.94 -54.23 -77.28 Net Sales 964.64 1,191.9 8 1,929.4 6 1,611.9 7 1,925.8 3 2,256.6 6 1,707.7 6 1,859.4 5 3,153.3 6 2,061.0 1 Gross profit Margin(%) 16.13 18.91 4.24 12.85 18.03 6.28 4.68 5.16 -1.72 -3.75 Industry comparison 12.09 9.38 7.98 10.06 13.33 -6.57 -24.37 -25.37 -10.07 1.39

- 5. This line chart indicate that the company is facing problem in maintaining its cash profit margin from the last two year which is showing negative figure in the year 2015 and 2014 with -4.44 and -1.94% respectively. When we compare it with its previous year we can say that the company has achieved some of the highest cash profit margin that is 18.54%, followed by 12.78%, 12.12% and 11.63% in the years 2006, 2009, 2005 and 2008. 3] Cash Profit Margin(%) 3] Cash+cash equivalents 27.01 47.35 22 50.89 83.11 31.16 26.66 23.84 -21.07 -38.3 Current Liabilities 222.92 255.42 462.36 437.58 650.32 541.93 416.52 414.6 1,085.8 9 862.51 Cash Profit Margin(%) 12.12 18.54 4.76 11.63 12.78 5.75 6.40 5.75 -1.94 -4.44 Industry comparison 4.95 7.40 7.13 0.77 11.40 9.24 15.87 11.70 5.30 4.44

- 6. C] Liquidity And Solvency Ratios 1] Current Ratio This line chart clearly indicate that the company had made A consistency when it come to current ratio starting from 2.15 in 2005 to 2.02 followed by 2.21,2.04,2.32 and 2.09 throughout the period of ten years of its operations 1] Total CA, Loans & Advances 594.24 619.82 878.54 1,152.2 1 1,187.1 0 1,258.8 3 1,107.9 9 1,222.4 5 1,999.0 2 1,984.8 0 Total CL & Provisions 276.63 306.92 513.92 522.12 747.73 618.49 478.15 472.36 1,166.8 1 950.63 Current Ratio 2.15 2.02 1.71 2.21 1.59 2.04 2.32 2.59 1.71 2.09 Industry comparison 2.49 1.71 1.77 2.33 4.79 7.21 1.45 7.39 1.97 2.08

- 7. 2] Quick Ratio This chart clearly shows that the acid test ratio of this company is quite flexible. When we look at different years like 2012, 2011, 2010 and 2008, it is above satisfactory level, that is (1:1) which is considered satisfactory as A firm can easily meet all current claims. But when we explicit these years and look at other years, we can see that it is below satisfactory level, which indicate that A large part of the current asset is tied up in slow moving and unsalable inventories and slow paying debts. 2] Total CA, Loans & Advances 594.24 619.82 878.54 1,152.2 1 1,187.1 0 1,258.8 3 1,107.9 9 1,222.4 5 1,999.0 2 1,984.8 0 Inventories 435.45 406.18 425.42 547.48 459.65 491.16 393.62 538.3 1,402.0 6 1,234.3 4 Total CL & Provisions 276.63 306.92 513.92 522.12 747.73 618.49 478.15 472.36 1,166.8 1 950.63 Quick Ratio 0.57 0.70 0.88 1.16 0.97 1.24 1.49 1.45 0.51 0.79 Industry comparison 1.33 0.98 1.12 1.69 4.19 6.42 4.85 6.42 0.71 0.69

- 8. D] Debt Coverage Ratio 1] Interest Cover This line chart clearly indicate that in the initial year of 2005, the company interest coverage ratio was 5.35 which goes up to all time highest that is 9.28 which indicate that how easily A company can pay interest on outstanding debt. After 2006 the entire scenario change and it start falling from 9.28 to 1.15 in the year 2007. It slightly increases in the next couple of years with 2.33 and 3.07 respectively. But thenafter, it went down to 1.19 in 2011 followed by O.41, -0.3 and -0.39 in the year 2012, 2014 and 2015. 1] PBDIT 171.81 237.18 165.77 310.46 430.38 263.65 193.94 131.53 113.78 11.68 Depreciation 12.35 23.65 81.53 80.02 76.15 83.81 81.25 81.55 118.78 59.22 Interest 29.83 23 73.34 98.96 115.47 84.6 94.81 122.77 185.23 122.08 Interest Cover 5.35 9.28 1.15 2.33 3.07 2.13 1.19 0.41 -0.03 -0.39 Industry comparison 12.11 12.92 21.45 24.46 15.59 8.59 10.09 6.21 3.98 4.95

- 9. 2] Total Debt To Owners Fund This line chart clearly indicate that throughout the phase of 10 years, the company has an ability to pay its debt when we compare it with its owner fund which gives the assurity to shareholders that its money is in safe even if the company get bankrupt. 2] Total Debt 450.09 402.61 999.5 1,168.7 6 833.83 934.16 696.33 856.4 1,013.4 0 1,350.1 0 Networth 192.9 552.38 689.66 792.12 936.3 983.5 1056.0 8 1000.7 9 824.28 658.51 Total Debt to Owners Fund 2.33 0.73 1.45 1.48 0.89 0.95 0.66 0.86 1.23 2.05 Industry comparison 0.93 1.57 2.18 1.93 1.53 1.82 2.08 1.62 -0.44 1.03

- 10. E] Management Efficiency Ratio 1] Inventory Turnover Ratio This line chart clearly indicate that the average inventory turnover ratio for the last ten years is 3.45, which clearly indicate that A company is not able to sell its inventory fast and stay on the shelf or in the warehouse for A long time. This will create A huge impact on company quick ratio where its liquidity position will affect. 1] Sales Turnover 1,024.8 8 1,270.2 4 2,074.2 8 1,728.7 2 1,985.7 0 2,345.4 1 1,707.7 6 1,859.4 5 3,256.9 4 2,128.0 2 Inventories 435.45 406.18 425.42 547.48 459.65 491.16 393.62 538.3 1,402.0 6 1,234.3 4 Inventory Turnover Ratio 2.35 3.13 4.88 3.16 4.32 4.78 4.34 3.45 2.32 1.72 Industry comparison 1.80 2.52 5.60 3.32 2.46 2.32 2.11 1.49 2.23 2.75

- 11. 4] Total Assets Turnover Ratio This line chart clearly indicate that the company total asset turnover in the period of ten years shows A consistent rate where at an average it is more than the ratio 1:1 which indicates that every one rupee of net sales company has more than one rupee of total asset which gives the assureity to the creditors that the company is liable to pay all its debts. 4] Net Sales 964.64 1,191.9 8 1,929.4 6 1,611.9 7 1,925.8 3 2,256.6 6 1,707.7 6 1,859.4 5 3,153.3 6 2,061.0 1 Total Assets 643 954.99 1,689.1 5 1,960.8 7 1,770.1 2 1,917.6 5 1,752.4 0 1,857.2 1 1,837.6 9 2,008.9 1 Total Assets Turnover Ratio 1.61 1.49 1.46 0.88 1.03 1.22 0.93 1.03 1.71 1.07 Industry comparison 1.12 0.85 0.83 0.74 0.84 0.93 0.89 0.80 0.79 0.91

- 12. F] Profit & Loss Account Ratios Material Cost Composition Here we can see that the company has very less flexibility throughout the period of ten year when it comes to material cost composition which indicate that every 100 rupees of company income, on an average 73.18 rupees are used in purchase of raw material Raw Materials 603.76 762.07 1,434.0 7 1,157.9 2 979.75 1,870.7 9 1,212.5 4 1,465.3 8 3,252.1 8 1,492.4 1 Net Sales 964.64 1,191.9 8 1,929.4 6 1,611.9 7 1,925.8 3 2,256.6 6 1,707.7 6 1,859.4 5 3,153.3 6 2,061.0 1 Material Cost Composition 62.59 63.93 74.32 71.83 50.87 82.90 71.00 78.81 103.13 72.41 Industry comparison 53.52 52.12 73.11 69.46 58.56 84.26 67.53 92.62 93.34 77.95

- 13. G] Cash Flow Indicator Ratios 1] Dividend Payout Ratio Net Profit This chart clearly see that the company has retain most of his earnings for reinvestment purpose and they provide only less dividend to their shareholder throughout the tenure of five years, only in the year 2010 and 2011 they give some extra portion of his earnings in the form of dividend. 1] Equity Dividend 8.32 12.89 15.47 15.47 25.79 19.34 5.16 2.58 0 Reported Net Profit 99.46 154.86 68 121.98 174.36 69.75 22.22 -52.29 - 176.33 - 152.06 Dividend Payout Ratio Net Profit 8.37 8.32 22.75 12.68 14.79 27.73 23.22 -4.93 0 0 Industry comparison 7.08 5.87 3.85 9.66 10.60 11.06 -18.51 5.00 1.63 27.03

- 14. 2] Earning Retention Ratio This line chart clearly indicates that from the beginning itself it kept back almost more than 75% in the business as retained earnings. The retention ratio refers to the percentage of net income that is retained to grow the business, rather than being paid out as dividends. 2] Reported Net Profit 99.46 154.86 68 121.98 174.36 69.75 22.22 -52.29 -176.33 -152.06 Equity Dividend 8.32 12.89 15.47 15.47 25.79 19.34 5.16 2.58 0 0 91.14 141.97 52.53 106.51 148.57 50.41 17.06 -54.87 -176.33 -152.06 Reported Net Profit 99.46 154.86 68 121.98 174.36 69.75 22.22 -52.29 -176.33 -152.06 Earning retention ratio 91.63 91.68 77.25 87.32 85.21 72.27 76.78 104.93 100 100 Industry comparison 55.51 69.56 65.05 68.58 70.55 66.43 94.74 75.99 71.79 39.62

- 15. India's sugar sector is running from bad phase where almost all other companies is making losses from the last three years. The biggest problem for the industry is the strict state control on every aspect of the business, right from the purchase price of sugarcane to how much each mill can sell in the open market. The company profitability ratio shows a huge negativity which is a warning sign for the company that they have to make thing work out before it get worse. The company is facing difficulties in selling their finished goods which directly shows its impact on its management efficiency ratio. CONCLUSION I