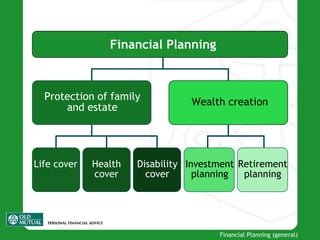

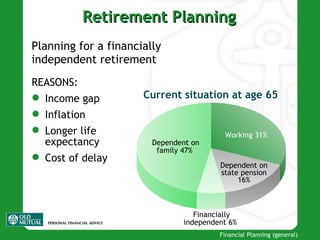

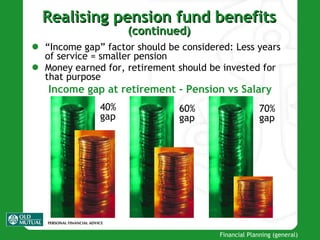

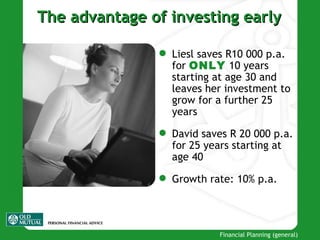

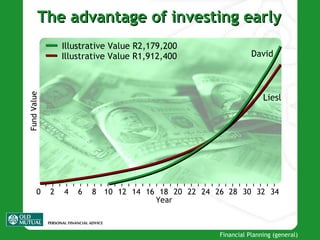

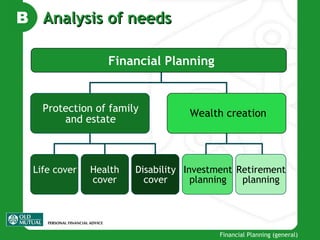

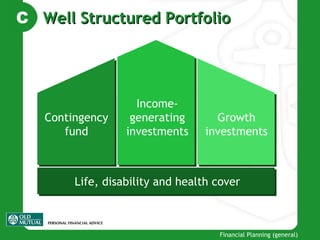

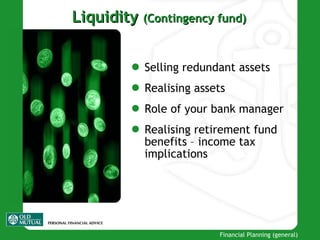

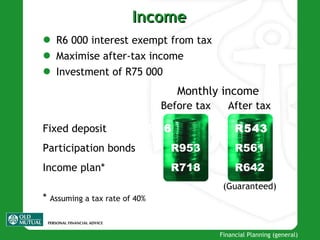

The document discusses various topics related to financial planning including retirement planning, investments, life and disability cover, structuring investment portfolios, and the advantages of starting to invest and plan for retirement early. It emphasizes the importance of seeking qualified financial advice, analyzing one's needs both currently and for the future, and creating a well-structured portfolio to meet one's financial goals and achieve financial security.