1. One of a series of papers on the

Confident Retirement®

approach:

Planning for a confident retirement

You can create a confident retirement through planning and creating

a clear road map for the future.

The Ameriprise Financial Confident Retirement approach provides

a straightforward framework for advisors and clients to create

a sound retirement plan to provide income for a lifetime. This

approach is designed to help you plan for an income stream that

covers both essential and lifestyle expenses, reduce vulnerability to

the unexpected and help you leave the legacy you desire.

For many Americans, the dream of retirement is on the horizon.

Even after spending decades saving and prudently investing for

retirement, many people are asking themselves if they can afford

to retire and how to make their income last over time. This insecurity

is not surprising, as today’s consumers face unique challenges,

including a prolonged period of market uncertainty and longer lives.

With the Confident Retirement approach, advisors have an

opportunity to provide clients with concrete strategies to address

the risks and challenges they face, and to help them put a confident

retirement in place.

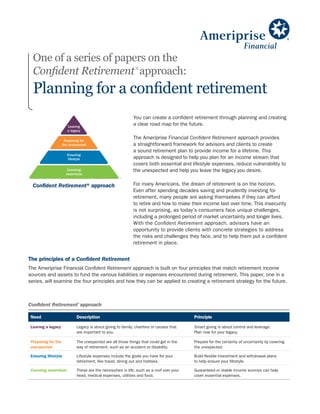

Confident Retirement®

approach

Need Description Principle

Leaving a legacy Legacy is about giving to family, charities or causes that

are important to you.

Smart giving is about control and leverage.

Plan now for your legacy.

Preparing for the

unexpected

The unexpected are all those things that could get in the

way of retirement, such as an accident or disability.

Prepare for the certainty of uncertainty by covering

the unexpected.

Ensuring lifestyle Lifestyle expenses include the goals you have for your

retirement, like travel, dining out and hobbies.

Build flexible investment and withdrawal plans

to help ensure your lifestyle.

Covering essentials These are the necessities in life, such as a roof over your

head, medical expenses, utilities and food.

Guaranteed or stable income sources can help

cover essential expenses.

The principles of a Confident Retirement

The Ameriprise Financial Confident Retirement approach is built on four principles that match retirement income

sources and assets to fund the various liabilities or expenses encountered during retirement. This paper, one in a

series, will examine the four principles and how they can be applied to creating a retirement strategy for the future.

Confident Retirement®approach

2. 2

Principle #1 — Covering essentials

The foundation of any retirement strategy is to cover all essential

expenses that are considered predictable and recurring. These are

the ongoing necessities in life such as housing, food, utilities, taxes

and medical expenses. Because financial markets are uncertain,

we believe essential expenses should be covered by solutions that

offer guaranteed or stable income. Virtually all retirees already have

one or multiple forms of guaranteed or stable income in place, most

notably Social Security. Some may have access to a defined benefit

plan as well. However, if those sources are not sufficient to cover

essential expenses, other solutions may include:

• Certificates of deposit that pay a fixed rate of interest.

Backed by banks and the Federal Deposit Insurance Corporation

(FDIC), CDs have long provided a guaranteed or stable source

of income. Consider a laddering strategy that will allow you to

reinvest this money into longer-term CDs over time to earn the

most competitive yields.

• Annuities. Either fixed or variable annuities can generate a reliable

stream of income throughout retirement. Annuities can provide

stable income for a desired period of time, or for life. As an

alternative to a living benefit rider (available at additional cost),

annuitization may provide higher cash flows for older retirees.

Annuities’ unique features offer opportunities for income for

life, future income growth and the ability to invest in the market.

In return for the benefits they provide, variable annuities carry a

mortality and expense fee and subaccount management fees.

Other fees may include optional rider fees, surrender charges

and an annual contract charge.

• Government securities. Securities such as U.S. Treasury bills,

bonds and notes, and Treasury Inflation-Protected Securities pay

a stated interest rate over a period of years. Investors can choose

to lock in payments for up to 30 years in a long-term government

bond, or they can consider a laddering strategy that spreads

money out in bills, notes and bonds with different maturities.

These instruments provide a stream of income that does not

change over time, so you can count on payments that occur monthly,

quarterly or annually depending on the investment. And they are

backed by the government (U.S. Treasuries) or financial institutions

with back-up from the government (FDIC) or the claims-paying ability

of the issuing insurance company (annuities) and do not apply to the

performance of the variable subaccounts, which will vary with market

conditions. Payment streams are reliable, and principal is protected

from a risk of loss if held to maturity, in the case of CDs and

government securities. The principal in some of these investments

may be subject to fluctuation if sold before maturity (in the case

of bonds) and some will not (such as non-negotiable CDs). These

are options to deliver a regular, reliable income stream to fund all

essential expenses. This is consistent with the concept of matching

liabilities or expenses to income sources or assets. Essential

expenses won’t go away. Neither should income sources that

fund them.

Guarantee, as used in this material, depends

upon the ability of the issuing entity to honor

and pay the amount you may be entitled to.

U.S. Government bonds are backed by the

full faith and credit of the U.S. Government.

Certificates of deposit are FDIC-insured up

to $250,000 per depositor. Insurance and

annuity products are backed only by the

continued claims-paying ability of the issuing

company. It is possible that an issuing entity

may not be financially able to meet income

guarantee obligations.

3. 3

Principle #2 — Ensuring lifestyle

While covering essential expenses is a foundational first step, most

people who are planning for retirement have additional goals they

wish to pursue. These can include travel, hobbies that may have

associated expenses (such as golfing or sailing), purchasing a

second home, and so on. In the most basic sense, these must be

considered “optional” expenses. As such, retirees could tap other

assets in their portfolio, outside of guaranteed or stable sources

like those used to pay essential expenses.

Using multiple product types (e.g. annuities, managed accounts,

individual securities, mutual funds, alternative investments and cash

value life insurance), provides flexibility and choice to address future

income needs. Product diversification goes a step further than asset

allocation to combine financial products with different features that

work together to help manage risk in volatile markets. For example,

an annuity can be used to create a guaranteed income floor. With

this in place, the balance of the portfolio can potentially be invested

more aggressively to help generate sufficient growth to meet income

needs well into the future.

Advice-embedded solutions use sophisticated, active investment

management that includes asset allocation, investment selection,

risk management and dynamic reallocation. These attributes can

make them particularly appropriate for retirees by potentially reducing

emotionally driven decisions by investors during fluctuating markets.

Advice-embedded solutions are available to meet such specific goals

as growth, preservation and income. There are even tax-sensitive

advice embedded solutions. Portfolios can be dynamically managed

in alignment with an investor’s risk tolerance and time horizon.

At Ameriprise, we believe that investments to

support lifestyle expenses should be arranged

in three categories:

• Strategic cash — We recommend keeping sufficient

assets in cash to cover up to three years of lifestyle

expenses. This can help prevent the need to sell off

investment assets at inopportune times. Examples

include savings and checking accounts, certificates

of deposit (CDs), and money market mutual funds.

• Income investments — Meeting at least some

of the lifestyle needs through income-generating

investments helps reduce susceptibility to steep

withdrawals and allows for greater confidence in

meeting long-term objectives. Set aside a portion of

assets in income-generating securities to generate

at least some of the lifestyle need. This can balance

the need to grow the lifestyle income stream with

inflation, and protect against downside risk. This

can also help reduce the possibility of excessive

asset sales to produce needed income, especially

in down markets. Examples include bonds and bond

funds, managed accounts with an income focus and

fixed annuities.

• Growth investments — In order to maintain

purchasing power and drive long-term growth,

allocate a portion of the assets to securities

that have the potential to grow over time.

Examples include stocks, equity-based mutual

funds, managed accounts with a growth focus,

alternative investments, variable annuities and

cash value life insurance.

Covering the first 3–5 years with

flexible assets and/or

stable investments should

allow you to manage cash

flows through recessionary

periods similar to those

we’ve seen in the past.

4. 4

The question of withdrawal rates

How much money will you need for lifestyle expenses and

will that base of assets be sustainable over time? Most

people should assume they will spend 25 to 30 years in

retirement given that the average 65-year-old lives to 84.1

Therefore, depending on your lifestyle choices, you will need

an appropriate base of assets.

A general rule of thumb is that this base of assets, properly

diversified, can last 30 years if you withdraw 4% or less

(adjusted annually for 3% inflation).

Of course, individual circumstances will vary. Investors must

recognize that changes in market conditions and performance

of specific investments chosen could alter this calculation.

Because both the markets and a retiree’s expenses can be

unpredictable, it is vital to conduct a review at least annually.

Four reviews per year may be more suitable depending on

the depth of issues to be addressed.

If expenses exceed the sustainable withdrawal rate,

adjustments should be considered. Major expenses,

such as an expensive vacation, can be delayed or reduced.

Alternatively, supplemental income sources can be identified

to overcome a shortfall.

This analysis was created using probability modeling

to determine the likelihood that inflation-adjusted

withdrawals can be sustained over 30 years.

Probability modeling uses statistical samples of

values for inflation and investment growth rates to

run many different trials. The historical returns were

from 1960 through 2011 for hypothetical portfolios.

The hypothetical portfolio is assumed to have a

moderate allocation as follows: 10% cash, 40%

bonds and 50% equities. The indices used were:

Cash: U.S. 30-day Treasury Bill; Bonds: 1960-1975

U.S. Intermediate Government Debt plus the median

premium for the Barclays Capital U.S. Aggregate Bond

Index, 1976-2011 Barclays Capital U.S. Aggregate

Bond Index; Equity: Center for Research in Security

Prices (CRSP) includes the New York Stock Exchange,

American Stock Exchange and NASDAQ Stock Market,

Deciles 1-10: Inflation: U.S. Department of labor – U.S.

Consumer Price Index – Not Seasonally Adjusted. Indices

are unmanaged and do not incur management fees or

other expenses. You cannot invest directly in an index.

Past performance is no guarantee of future results.

There is no guarantee that investment objectives will

be satisfied or that return expectations will be met.

The data assumes reinvestment of dividends and

does not account for taxes.

Withdrawal rates vs. success

Withdrawal rate

Probability of your

money lasting 30 years

4% 92%

5% 71%

6% 44%

7% 22%

8% 9%

9% 3%

1

Health United States, 2011, U.S. Dept. of Health

and Human Services, Centers for Disease Control

and Prevention, National Center for Health Statistics.

5. 5

2

U.S. Department of Health and Human

Services, National Clearing House for

Long Term Care Information, October 2008.

3

2012 Alzheimer’s Disease Facts and

Figures, Alzheimer’s Association.

4

What is the Distribution of Lifetime Health

Care Costs from Age 65?, Center for

Retirement Research at Boston College,

March 2010.

5

Overcoming Retirement Income Challenges

Facing Women, Insured Retirement

Institute, July 2012.

Principle #3 — Preparing for the unexpected

Unexpected events can have a devastating impact on retirement

plans. At this stage of life, retirees typically lack the financial

flexibility to make up for consequences to their retirement if an

unplanned event results in significant expense. The Confident

Retirement approach leverages specific solutions to mitigate

events that can have a big impact on a retirement plan.

The most significant concerns include:

• Protecting against expenses associated with long-term care

needs that can drain lifetime savings. Research shows that

about 70% of those age 65 and older will need some type of

long-term medical assistance.2

About half of those still alive at

age 85 will encounter Alzheimer’s disease, dementia or some

form of cognitive impairment.3

• Preparing for medical expenses in retirement. Data indicates

that insurance premiums (such as Medicare Parts B and D and

Medicare Supplement insurance), deductibles, co-insurance

costs and out-of-pocket expenses will add up to $200,000 or

more for the average American couple in retirement.4

• Insuring against personal liability risks with home, auto and

umbrella insurance policies. As individuals enter retirement,

they most often have the lifetime maximum amount of financial

assets they will ever have. These assets need to be protected in

our litigious society.

• Providing adequately for a surviving spouse or dependents in the

event of an untimely death. Remember, cash flows will change

at the death of a spouse. Survivor Social Security benefits,

survivor options, if any on a pension, and annuity payouts may all

be affected. And some expenses, such as real estate taxes, won’t

change when one member of a couple dies but others, such as

many lifestyle expenses, probably will.

Considering these risks, there are solutions and

strategies to mitigate these potential issues.

• A discussion of long-term care expenses is critical

considering the high percentage of retirees who

will need such assistance. Two ways of addressing

this risk should be considered — stand-alone

long-term care insurance, and a rider (available at

additional cost) on a life insurance policy that allows

an advance payment of a large portion of the death

benefit if it is used for long-term care expenses.

• Medicare is the primary medical-care plan for most

retirees. In addition to Medicare, most retirees will

need to examine Medicare supplemental policies,

or Medigap plans, that will cover the deductibles

and co-insurance amounts not paid for by Medicare.

There are many plans to choose from, so some time

and care should be taken examining the options.

• Consider a full review of property/casualty coverage

and a personal-liability umbrella policy. An uncovered

claim due to a lawsuit at this stage in life could

devastate the best-laid plans.

Women need to set aside considerably

more savings for health care in

retirement than men. This is due to

living to an older age and the rapidly

rising cost of health care.5

6. 6

Principle #4 — Leaving a legacy

Ensuring the wealth that you have accumulated is used to provide

for the individuals or causes that you care about most is an

important part of planning for a confident retirement. After accounting

for essential, lifestyle and unexpected expenses, the next step is to

create a legacy plan for any remaining assets. Effective legacy plans

address two critical features — control and leverage.

Control during retirement

As we age, the potential for some types of impairment rise, and as

a result you may not be able to exercise prudent control of your own

assets. Three documents — limited financial power of attorney, a

health care directive, and a living will — can ensure that assets are

utilized according to your wishes, even if you are unable to exercise

that direct control.

It’s also important to review how assets are titled. Up-to-date

beneficiary designations for financial accounts, a will and the use of

trusts, if appropriate, can help reposition assets to minimize taxes

due upon death.

Control beyond retirement

Wills, trusts and estate planning can be used to control the

use of assets beyond retirement. Planning for tax positioning of

assets upon death can both control where the assets go as well as

maximize the amount that passes to heirs or charities. The wrong

positioning can reduce the amount of funds that actually go to

legacy causes by up to 50% due to income, state and federal

estate taxes.

Leverage

Leverage is about ensuring that the maximum amount of assets

actually go to funding legacy goals, and minimizing the drain on

those assets from income and estate taxes. Life insurance is a

unique solution for providing leverage in any legacy plan, as it not

only provides a death benefit in excess of the premium, but the

death benefit passes income tax-free to the beneficiaries.

6

2012 Retirement Confidence Survey,

Employee Benefit Research Group.

• Those still a few years from retirement rely on their

income to build up their retirement nest egg. Yet 50%

of Americans find themselves retiring unexpectedly.

Of those, 51% leave the workforce due to health

problems or disability.6

Disability insurance is a key

way to mitigate this risk and should be considered

if it’s not already in place.

• There are numerous life insurance options for

meeting the income needs of survivors, meeting

unexpected costs and funding legacy wishes. Those

with a life insurance need can add a long-term care

rider to most permanent products (for an additional

fee) allowing a large portion of the policy’s death

benefit to be advanced to pay for qualified long-term

care expenses.

Ameriprise offers a special

beneficiary restriction option

for IRAs that provides more

control than a traditional

beneficiary designation.

It’s also less complex and

more affordable than a

formal trust agreement.

7. 7

Several common uses of life insurance

in legacy planning include:

• Addressing the tax burden of tax-deferred

qualified assets — Assets remaining in tax

deferred qualified plans (e.g. IRAs, annuities,

401(k)s) at your death are subject to income tax

on the beneficiary. If the beneficiary is a taxable

individual, as most family members typically are,

they will owe tax as they withdraw those assets.

On the other hand, if a legacy plan calls for both

individual and charitable giving, it is often most tax

efficient to leave the remainder of the qualified plan

to the charity which does not pay income tax, and

fund the individual legacy with life insurance —

which will be received tax free by the individual.

This solution can provide significant leverage by not

only providing for a charity but for an heir as well.

• Maximizing wealth transfer — For those fortunate

to have excess assets now that they can reposition,

life insurance can provide leverage for legacy

planning. Repositioning assets from taxable

accounts (e.g. brokerage, wrap accounts) to a

permanent life insurance policy can provide a death

benefit that can be several times the amount of

the assets repositioned. Plus they will pass to the

beneficiary free of income and possibly estate tax,

further maximizing the benefit to the legacy plan.

Consider your goals when evaluating the features

of individual life insurance plans.

For example:

• Cash value solutions can provide ongoing access to

assets during retirement

• Death benefit-only products can often maximize the

death benefit amount but limit access to the cash

value during retirement

• Adding a long-term care rider on a life insurance policy

(at an additional cost) can provide a tax-free benefit

to fund long-term care needs in retirement

Getting started

Enjoying a confident retirement is part of the American

dream. It’s taken planning and hard work to get this far

on the journey. Yes, there are still challenges to meet

as we live longer lives and cope with an uncertain

environment. But a confident retirement is within reach.

It all starts with a conversation. A simple conversation that

can help you feel more confident about:

• Covering your everyday essentials

• Ensuring your lifestyle goals

• Preparing for the unexpected

• Leaving a meaningful legacy

Contact your Ameriprise financial advisor today to begin

your conversation.

Additional papers in this

series include:

• A Confident Retirement

approach: Covering essentials

• A Confident Retirement

approach: Ensuring lifestyle

• A Confident Retirement

approach: Preparing for the

unexpected

• A Confident Retirement

approach: Leaving a legacy

Four simple principles. Practical solutions.

Working together, we can figure this out.