LEARNING

OUTCOMES

• Define financialliteracy

• Present ways on how to avoid financial crises and

scams

• Demonstrate understanding of insurance and

taxes

• Describe a financially stable person

• Determine ways on how to integrate financial

literacy in the curriculum

• Draw relevant life lessons and significant values

from personal experiences on financial crises and

scams

• Make a personal financial plan based on short-

term and long-term goals

3.

CONCEPT

EXPLORATION

In some instances,teachers are confronted with

issues and concerns on financial debt, being

victimized by fraud and other related scams, both

personal and electronic ways. More so, some

teachers are drowned by emergent financial needs

and unexpected debt, especially in difficult times,

sickness and inevitable circumstances and

calamities.

4.

Definition

What is Financial

Literacy?

Financialliteracy is a core life skill in an increasingly

complex world where people need to take charge of

their own finances, budget, financial choices, managing

risks, saving, credit, and financial transactions.

5.

Poor financial decisionscan have a long-lasting

impact on individuals, their families and the

society caused by lack of financial literacy. Low

levels of financial literacy are linked with low

standards of living, decreased psychological and

physical well-being and greater reliance on

government support. However, when put into

correct practice, financial literacy can strengthen

savings behavior, eliminate maxed-out credit

cards and enhance timely debt.

6.

Financial literacy isthe ability to make

informed judgments and make effective

decisions regarding the use and

management of money. Hence, teaching

financial literacy yields better financial

management skills.

7.

The importance ofstarting financial literacy

while still young.

National surveys show that young adults have

the lowest levels of financial literacy as

reflected in their inability to choose the right

financial products and lack of interest in

undertaking sound financial planning.

Therefore, financial education should begin

as early as possible and be taught in schools.

8.

Likewise, financial literacyis the

capability of a person to handle his/her

assets, especially cash more efficiently

while understanding how money works

in the real world.

9.

1. Calculating thenet worth. Net worth is the amount by which

assets exceed liabilities. In so doing, consider

(1) assets that entail one’s cash, property, investments, savings,

jewelry, and wealth; and

(2) liabilities that include credit card debt, loans, and mortgage.

Formula: total assets - minus total liabilities = current net worth.

FINANCIAL PLAN

Teachers need to have a deeper understanding and capacity to

formulate their own financial plan. It is wise to consider starting

bonuses and extra remunerations that they receive, including the

incentives, bonuses, and extra remuneration that they receive.

The following are steps in creating a financial plan.

10.

2. Determining cashflow. A financial plan is knowing where money

goes every month. Documenting it will help to see how much is

needed every month for necessities, and the amount for savings

and investment.

3. Considering the priorities. The core of a financial plan is the person’s

clearly defined goals that may include:

(1) Retirement strategy for accumulating retirement income;

(2) Comprehensive risk management plan including a review of life and

disability insurance, personal liability coverage, property and casualty

coverage, and catastrophic coverage;

(3) Long-term investment plan based on specific investment objectives

and a personal risk tolerance profile; and

(4) Tax reduction strategy for minimizing taxes on personal income

allowed by the tax code.

11.

Five Financial

Improvement

Strategies

1.Identify yourstarting point. Calculating

the net worth is the best way to

determine both current financial status

and progress over time to avoid financial

trouble by spending too much on wants

and nothing enough for the needs.

• Automate savings transfers.

• Prioritize saving before spending.

12.

Five Financial

Improvement

Strategies

2. Setyour priorities. Making a list of rated

needs and wants can help set financial

priorities. Needs are things one must have in

order to survive (i.e., food, shelter, clothing,

healthcare, and transportation); while wants

are things one would like to have but are not

necessary for survival. • Automate savings transfers.

• Prioritize saving before spending.

13.

Five Financial

Improvement

Strategies

3. Documentyour spending. One of the best

ways to figure out cash flow or what comes in

and what goes out is to create a budget or a

personal spending plan. A budget lists down

all income and expenses to help meet

financial obligations.

• Automate savings transfers.

• Prioritize saving before spending.

14.

Five Financial

Improvement

Strategies

4. Laydown your debt. Living with debt is

costly not just because of interest and fees,

but it can also prevent people from getting

ahead with their financial goals.

• Automate savings transfers.

• Prioritize saving before spending.

15.

Five Financial

Improvement

Strategies

5. Secureyour financial future/Retirement is

an uncontrollable stage in a worker’s life, of

which counterpart are losing the job,

suffering from an illness or injury, or be

forced to care for a loved one that may lead

to an unplanned retirement.

• Automate savings transfers.

• Prioritize saving before spending.

16.

Key Concepts of

FinancialLiteracy

Budgeting:

Creating a plan for how you

will spend and save your

money.

Saving:

Setting aside money for

future needs and

emergencies.

Investing:

Using money to generate

additional income or growth

over time.

Debt Management:

Understanding how to

handle and repay debt

responsibly.

17.

FINANCIAL GOAL

PLANNING ANDSETTING

Setting goals is a very important part

of life, especially in financial planning.

Before investing money, consider

setting personal financial goals.

Financial goals are targets, usually

driven by specific future financial

needs, such as saving for a

comfortable retirement, sending

children to college, or enabling a

home purchase.

18.

There are threekey areas in setting

investment goals for consideration.

A. Time horizon. It indicates the

time when the money will be

needed. To note, the longer the

time horizon, the more risky

(and potentially more lucrative)

investments can be made.

19.

There are threekey areas in setting

investment goals for consideration.

B. Risk tolerance. Investors may

let go of the possibility of a large

gain if they knew there was also

a possibility of a large loss (they

are called risk averse); while

others are more willing to take

the chance of a large loss if there

were also a possibility of a large

gain (they are called risk

seekers). The time horizon can

affect risk tolerance.

20.

There are threekey areas in setting

investment goals for consideration.

C. Liquidity needs. Liquidity

refers to how quickly an

investment can be converted

into cash (or the equivalent of

cash). The liquidity needs usually

affect the type of chosen

investment to meet the goals.

21.

There are threekey areas in setting

investment goals for consideration.

D. Investment goals: Growth, income and

stability. Once determined the financial

goals and how time horizon, risk tolerance,

and liquidity needs affect them, it is time to

think about how investments may help

achieve those goals. When considering any

investment, think about what it offers in

terms of three key investment goals: (1)

Growth (also known as capital appreciation),

an increase in the value of an investment;

(2) Income, of which some investments

make periodic payments of interest or

dividends that represent investment income

and can be spent or reinvested; and (3)

Stability, or as capital preservation or

protection of principal.

22.

Budget and

Budgeting

1.A budgetis an estimation of revenue and expenses over a

specified future period of time and is usually compiled and re-

evaluated on a periodic basis. Budgets can be made for a

variety of individual or business needs. Budgeting, on the other

hand, is the process of creating a plan to spend money.

Budgeting, on the other hand, is the process of creating a plan

to determine in advance whether he/she will have enough

money to do the things he/she needs or likes to do.

• Automate savings transfers.

• Prioritize saving before spending.

23.

Seven Steps toGood

Budgeting

Step 1: Set realistic goals. Goals for the money will help make smart

spending choices upon deciding on what is important.

Step 2: Identify income and expenses. Upon knowing how much is

earned each month and where it all goes, start tracking the

expenses by recording every single cent.

Step 3: Separate needs from wants. Set clear priorities and the

decisions become easier to make by identifying wisely those that

are really needed or just wanted.

• Automate savings transfers.

• Prioritize saving before spending.

24.

Step 4: Designyour budget. Make sure to avoid spending more

than what is earned. Balance budget to accommodate everything

needed to be paid for.

Step 5: Put your plan into action. Match spending with income

payday. Non-reliance to credit for the living expenses will protect

one from debt.

Step 6: Plan for seasonal expenses. Set money aside to pay for

unplanned expenses so to avoid going into debt.

Step 7: Look ahead. Having a stable budget can take a month or

two, so, ask for help if things are not getting well.

• Automate savings transfers.

• Prioritize saving before spending.

25.

Spending

1.If budget goalsserve as a financial wish list, a spending

plan is a way to make those wishes a reality. Turn them

into an action budget goals and spending plan. The

following are practical strategies in setting and

prioritizing budget goals and spending plan:

• Automate savings transfers.

• Prioritize saving before spending.

26.

Savings

1.In order toget out of debt, it is important to set some

money aside and put it into a savings account on a

regular basis. Savings will also help in buying things that

are needed or wanted without borrowing.

• Automate savings transfers.

• Prioritize saving before spending.

27.

EMERGENCY

SAVINGS FUND.

1.Start asearly, setting aside a little money for emergency

savings fund. If you receive a bonus from work, an

income tax refund or earnings from additional or side

jobs, use them as an emergency fund.

• Automate savings transfers.

• Prioritize saving before spending.

28.

10 Reasons WhySave MoneyWith credit so easy to get, here

are ten practical reasons why it is important to save money

that everyone, including teachers, must know.

1. To become financially

independent. Financial

independence is not having to

depend on receiving a certain

pay but setting aside an amount

to have savings that can be relied

on.

2. To save on everything you buy.

With savings, you can buy things

when they are on sale and can

make better spending choices,

without being compromised on

credit card interest charges.

3. To buy a home or a car. Savings

can be used in buying a home in

full or down payment, especially

in times of promo deals, bids and

inevitable sale and at a

reasonable interest rate.

29.

10 Reasons WhySave MoneyWith credit so easy to get, here

are ten practical reasons why it is important to save money

that everyone, including teachers, must know.

4. To prepare for the

future. Through savings,

you can be confident to

face the future without

worrying on how you will

survive.

6. To augment annual

expenses. In order to

attain a good, stress-

free financial life, there

is a need to save for

annual expenses in

advance.

5. To get out of

debt. If you want

to get out of debt,

you have to save

money.

30.

10 Reasons WhySave MoneyWith credit so easy to get, here

are ten practical reasons why it is important to save money

that everyone, including teachers, must know.

7. To settle unforeseen

expenses. Savings can

respond to unforeseen

expenses in times of

need.

9. To mitigate losing your job

or getting hurt. Bad things

can happen to anyone, such

as losing a job, business

bankruptcy, or crisis, being

injured or becoming too sick

to work.

8. To respond to emergencies.

Emergencies may happen

anytime and these can be

expensive so, there is a need to

get prepared rather than

potentially become another

victim of an emergency.

31.

10 Reasons WhySave MoneyWith credit so easy to get, here

are ten practical reasons why it is important to save money

that everyone, including teachers, must know.

10. To have a good life. Putting

aside some money to spend

when needed can bring about

quality and worry-free life at all

times.

32.

Common Financial

Scams toAvoid

Financial fraud can happen to anyone,

including the teachers at any time.

While some forms of financial fraud,

such as massive data breaches, are

out of one’s control, there are many

ways to proactively get rid of financial

scams and identify theft.

33.

A. PHISHING

Using thiscommon tactic, scammers

send an email that appears to come

from a financial institution, such as a

bank, and asks you to click on a link to

update your account information. If you

receive any correspondence that asks

for your information, never click on the

links or provide account details. Instead,

visit the company’s website, find official

contact information, and call them to

verify the request.

34.

B. Social Media

Scams.

Scammersare adept at using social

media to gather information about the

traveling habits of potential victims.

They also have phishing tactics,

including posts seeking charity

donations with bogus links that allow

them to keep your money.

35.

C. Phone Scams.

Anotherprevalent tactic is scamming

phone calls. The scammers post as a

government agency, such as the Bureau

of Internal Revenue or local law

enforcement agencies, and use scare

tactics to acquire your personal

information and account numbers.

Never provide your account information

over the phone. Look for the agency’s

contact information, and call them to

verify any request.

36.

D. Stolen Credit

CardNumbers.

There are numerous ways that

scammers can obtain your credit card

information, including hacking,

phishing, and the use of skimming

devices, such as small card readers

attached to unmanned credit card

readers (i.e. ATMs, gas pumps, and

more). These small devices pull data

from your card when you swipe it.

Before you use an ATM or swipe your

card, look for suspicious devices that

may be attached to the card reader.

37.

E. Identify Theft

Dependingon the amount of

information a scammer is able to obtain,

identity may extend beyond

unauthorized charges on a debit or

credit card. If scammers are able to

obtain your Social Security number, date

of birth, and other personal information,

they may be able to open new accounts

in your name without your knowledge.

Be aware of an information you share

and with whom, and be sensitive

information before disposing it.

38.

10 Tips toAvoid

Common Financial

Scams

Prioritize high-interest debt

repayment.

Every year, fraud cases are getting worse, leaving countless

victims in trouble and danger through online scams.

Unfortunately, new data breaches, identity theft and fraudsters

are on edge, making it easier than ever for scam artists to nab

financial data from unsuspecting consumers (Bell, 2019).

39.

1. Never wiremoney to a stranger. Although it is one of the

oldest Internet scams, there are still consumers who fall for this

rip-off or some variations of it.

2. Don’t give out financial information. Never reveal sensitive

personal financial information to a person or business you don’t

know, thru phone, text or email.

3. Never click on hyperlinks in emails. If you receive an email

from a stranger or company asking you to click on a hyperlink

or open an attachment and then, enter your financial

information, delete the email immediately.

40.

4. Use difficultpasswords. Hackers can easily find passwords

that are simple number combinations. Create passwords that

have eight characters long and that include some lower and

upper case letters, numbers and special characters. You should

also use a different password for every website you visit.

5. Never give your social security number. If you receive an

email or visit a website that asks for your Social Security

number, ignore it.

41.

6. Install Antivirusand Spyware protection. Protect the sensitive

information stored on your computer by installing the antivirus,

firewall and spyware protection. Once you make the program,

turn on the auto-updating feature to make sure the software is

always up-to-date.

7. Don’t shop with unfamiliar online retailers. When it comes to

online shopping, only do business with familiar companies, to

online product from an unfamiliar retailer, do some research to

ensure the business is legit and reputable.

42.

8. Don’t downloadsoftware from pop-up windows. When you

claim are online, do not trust pop-up windows that appear and

are unsafe. If you click on the link in the pop-up, your computer

is scan or some other programs, malicious to start the “system”

as “malware” could damage your operating system.

9. Make sure the websites you visit are safe. Before you enter

your financial information on any website, double-check the

website’s privacy rules. Also, make sure the website uses

encryption, which is usually symbolized by a lock to the left of

the web address which means it is safe and protected against

hackers.

43.

10. Donate toknown charities only. If you receive a call or an

email for solicitation of charity donations, critically examine it.

Some scammers create bogus charities to steal credit card

information.

(https://www.investopedia.com/articles/

44.

Financial Scams amongStudents. Students can also be

susceptible to different financial scams and fraud. Learning how

to manage finances and being aware of financial scams are

skills that every student should master.

The following are common financial scams that students should

watch out for, and learn to protect one’s identity and finances.

45.

A. Fake scholarships.While it is beneficial for students to apply

for as many scholarships, it is important to become aware of

related scams and frauds. Students should thoroughly check

scholarship sources before applying to verify legitimacy. Never

apply for a scholarship that asks for money in return.

B. Diploma mills. There are schools that offer fake degrees and

diplomas in exchange for a fee. Check from government

education agencies the prospective school to enroll in if it is

government-recognized, legitimate or accredited.

C. Online book scams. While students often go for the best

deals on textbooks online, scammers can use this opportunity

to get students’ credit card information. When buying anything

online, be sure to do it on a credible site.

46.

D. Credit cardscams. Oftentimes, credit card companies go to

school campuses to convince students to fill out card

applications. Scammers may also grab this chance to steal

students’ information. It is important to visit a local credit union

or bank for credit card application. Also, regularly check the

credit card statement and once there are any unrecognized

charges, contact your banking institution immediately.

(https://www.ecl.org/resources/financial-scam-safety/)

47.

Insurance and

Taxes

Insurance isa contract (in the form of a policy)

between the policyholder and the insurance

company, whereby the company agrees to

compensate for any financial loss from specific

insured events. In exchange for the financial

protection offered, policyholder agrees to pay a

certain sum of money, known as premiums to the

insurance company. There are various types of risks

management against uncertain loss, insurance,

health insurance, motor insurance, such as life

insurance entails tax benefit claim on the paid

premiums.

48.

1. Employer-Sponsored Insurance.

Idealif working in a company with 50

or more full-time employees, the

employer is required to provide

employee-only insurance that meets

minimum guidelines.

49.

2.Marketplace plans areavailable

based on an area of residence and

income upon meeting minimum

coverage requirements. Marketplace

plans come in three tiers: bronze, silver

and gold. Generally, bronze plans offer

the least coverage at the lowest

premiums, while gold plans provide the

most coverage at the highest price.

50.

2.Marketplace plans areavailable

based on an area of residence and

income upon meeting minimum

coverage requirements. Marketplace

plans come in three tiers: bronze, silver

and gold. Generally, bronze plans offer

the least coverage at the lowest

premiums, while gold plans provide the

most coverage at the highest price.

51.

Life Insurance

Life insuranceis a type of

insurance that compensates

beneficiaries upon the death

of the policyholder. The

company will guarantee a

payout for the beneficiaries in

exchange of premiums. This

compensation is called “death

benefit”

52.

Depending on thetype of

insurance one may have, these

events can be anything from

retirement, to major injuries,

to critical illness or even to

death.

1. Preferred Plus– The policyholder is in excellent

health, with normal weight, no history of smoking,

chronic illnesses, or life-threatening disease.

2. Preferred – The policyholder is in excellent health

but may have minor issues on cholesterol or blood

pressure but under control.

3. Standard Plus – The policyholder is in very good

health but some factors, like high blood pressure or

being overweight impede a better rating

55.

4. Standard –Most policyholders belong to this

category, as they are deemed to be in healthy and

have a normal life expectancy although, they may

have a family history of life-threatening diseases or

few minor health issues.

5. Substandard – Those with serious health issues,

like diabetes or heart disease are placed on a table

rating system, from highest to lowest. On average,

the premiums will be similar to Standard with an

additional 25% lower claim on table ratings.

6. Smokers – Due to an added risk of smoking, the

policyholders in this category are guaranteed to pay

more. Aside from health class, age is also a critical

factor in determining premiums. Therefore, older

people pay more expensive premiums.

1. It paysfor medical and funeral costs. Life

insurance helps solve the incurred expenses for

medical and funeral services to lessen the grief

among family and relatives for being unprepared.

2. For financial support. Life insurance can become a

source of temporary income during the difficult

period of adjusting and coping with the loss of a

loved one, especially if he/she is the breadwinner.

58.

3. For fundingvarious financial goals. Life insurance

offers additional benefits through the form of fund

accumulation for specific future financial goals.

4. Acts as a retirement secured conform. Modern life

insurance also serves as a tool that principal holders

can use to get in a better financial position in the

future.

5. It covers costs incurred from taxes and debt. Life

insurance can serve as protection since the premium

can be used to pay for unsettled debts and taxes.

59.

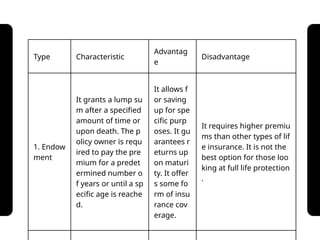

Types of Life

Insurance

Thetable below shows a comparative analysis of different

types of life insurance along characteristics, advantages and

disadvantages that may serve as a reference.

60.

Type Characteristic

Advantag

e

Disadvantage

1. Endow

ment

Itgrants a lump su

m after a specified

amount of time or

upon death. The p

olicy owner is requ

ired to pay the pre

mium for a predet

ermined number o

f years or until a sp

ecific age is reache

d.

It allows f

or saving

up for spe

cific purp

oses. It gu

arantees r

eturns up

on maturi

ty. It offer

s some fo

rm of insu

rance cov

erage.

It requires higher premiu

ms than other types of lif

e insurance. It is not the

best option for those loo

king at full life protection

.

61.

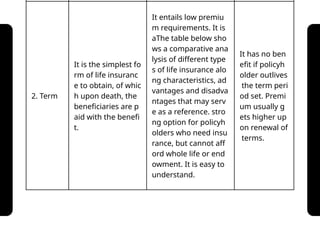

2. Term

It isthe simplest fo

rm of life insuranc

e to obtain, of whic

h upon death, the

beneficiaries are p

aid with the benefi

t.

It entails low premiu

m requirements. It is

aThe table below sho

ws a comparative ana

lysis of different type

s of life insurance alo

ng characteristics, ad

vantages and disadva

ntages that may serv

e as a reference. stro

ng option for policyh

olders who need insu

rance, but cannot aff

ord whole life or end

owment. It is easy to

understand.

It has no ben

efit if policyh

older outlives

the term peri

od set. Premi

um usually g

ets higher up

on renewal of

terms.

63.

Like anyone else,teachers also

aim to become financially

stable if not today, maybe in

the future. Being financially

stable means confidence with

the financial situation,

worriless paying the bills

because of available funds,

debt-free, money savings for

future goals and enough

emergency funds.

FINANCIAL

STABILITY

64.

Just like anygoal, getting the

finances stable and becoming

financially successful requires

the development of good

financial habits. Babauta (2007)

suggests 10 habits toward

financial stability and success

10 Strategies in

Reaching Financial

Stability

65.

1. Make savingsautomagical. Savings should be

made a top priority, especially as an emergency fund

and a bill payment from the account, like an online

savings.

2. Control your impulsive spending. Control your self

from impulsive spending on eating out, shopping

and online purchases that may ruin your finances

and budget.

66.

3. Evaluate yourexpenses and live frugally. Analyze

how you spend your money, see what you can

reduce and determine expenses that are necessary

and eliminate the unnecessary.

4. Invest in your future. Start preparing and

investing for your future retirement while still young

in your career field.

5. Keep your family secure. Save for an emergency

fund, so that you have some to spend if anything

happens with the family emergency.

67.

6. Eliminate andavoid debt. Eliminate credit cards,

personal loans, or other debt forms as it does not

work on you but even pull you down and make you

drowned with obligations that may even resort to

surrendering your properties, jewelry and

investments as payment.

68.

7. Use theenvelope system. Set aside three amounts

in your budget each payday, withdraw those

amounts and put them in three separate envelopes.

In that way, you can easily track how much remains

for each of the expenses or if you already run out of

money.

8. Pay bills immediately. One good habit is to pay

bills as soon as they come in and try to get your bills

to be paid through automatic deduction.

9. Read about personal finances. The more you

educate yourself, the better the finances will be.

69.

10. Look togrow your net worth. Do whatever you

can to improve your net worth, either by reducing

your debt, increasing your savings, or increasing

your income, or all of the above.

(https://zenhabits.net/10-habits-to-develop-for-

financial/)

70.

Signs of BeingFinancially

StableTeachers, like any one

else, often work to the extent

to earn more even through

additional jobs on the side just

for their desire for financial

stability.Rose (2019) presents

some signs of a financially

stable person.

You never overdraw your

checking account.

Signs of Being

Financially

StableTeachers,

71.

1. you neveroverdraw your

checking account.

2. You don’t lose sleep over

finances.

3. You use credit cards for

convenience and rewards but

never out of necessity.

4. You don’t worry about losing

your job.

Signs of Being

Financially

StableTeachers,

72.

5. You payyour bills ahead of

time.

6. People ask your opinion

about financial matters and

you inspire them.

7. You’re generally happy with

your financial situation.

8. You finance your cars over

five years or less if you take

loans at all.

Signs of Being

Financially

StableTeachers,

73.

9. You contributemore to your

retirement.

10. You don’t feel guilty when

you’re out for special

occasions.

11. You can afford to buy the

things you really want.

Signs of Being

Financially

StableTeachers,

74.

12. Recreation spending

doesn’tappeal to you.

13. You’re a natural saver.

14. You’re generous with

money when it comes to

charities or helping others.

15. You’re confident about your

future.

16. Your net worth grows

Signs of Being

Financially

StableTeachers,

75.

16. Your networth grows

significantly from year to year.

17. You have substantial equity in

your home.

18. You consistently live beneath

your means.

19. You could survive for months

without a paycheck.

20. You feel in control of your

finances and never dominated by

them.

Signs of Being

Financially

StableTeachers,

76.

Integrating Financial Literacyinto the Curriculum

FINANCIAL EDUCATION in schools should be part of a collaborative

national strategy to ensure relevance and long-term sustainability.

The education system and profession should be involved in the

development of the strategy.

IN SUPPORT, BARRY (2013) underscored that financial literacy has a

wide repercussion outside the family circle and more precisely, the

school. Hence, administrators and professors need to develop a

curriculum that would provide students insights on having the

value of financial literacy including the effect it can bring them.

77.

FINANCIAL EDUCATION shouldideally be a core part of the school

curriculum. It can be integrated into other subjects like

mathematics, technology and home economics, values, economics,

social studies, technology.

TEACHERS should be adequately trained and resourced, made

aware of the importance of financial literacy and relevant

pedagogical methods and they should receive continuous support

to teach it or integrate in their lesson. MORE so, there should be

easily accessible, objective, high-quality and effective learning tools

and pedagogical resources available to the level of study.

STUDENTS’ SCHOOLS AND TEACHERS that are assessed through

various high impact modes. PROGRESS should also be assessed

through various high impact modes.