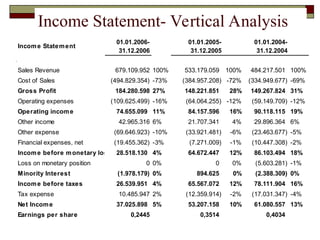

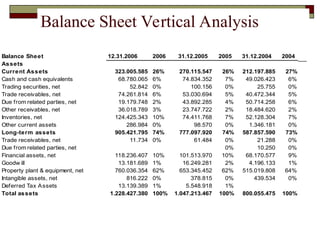

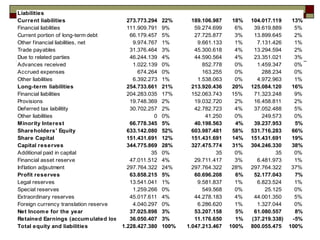

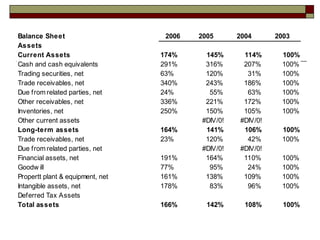

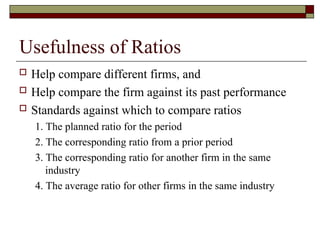

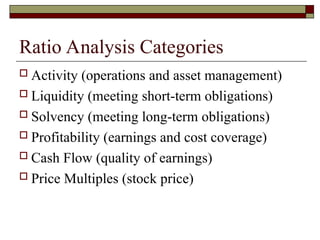

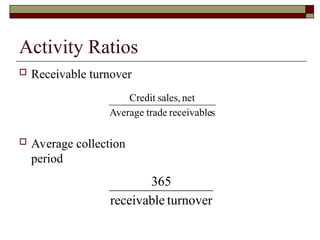

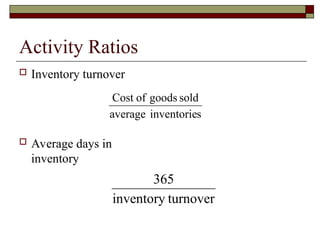

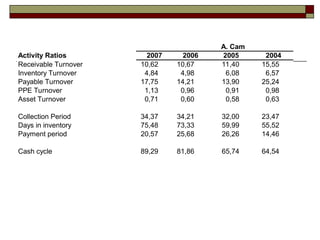

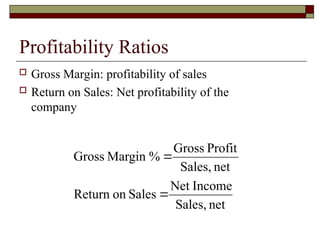

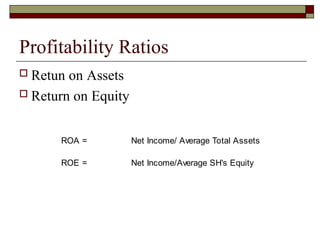

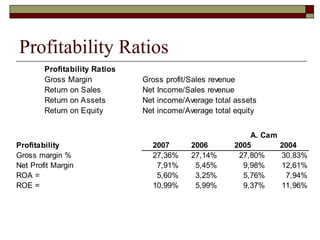

Chapter 14 discusses financial statement analysis, emphasizing its importance for managers, owners, lenders, and other stakeholders to assess a firm's profitability and risks. It outlines analytical tools such as vertical and horizontal analysis, ratio analysis, and highlights the significance of liquidity, solvency, and profitability ratios for comprehensive financial assessment. The document further details various financial metrics derived from income statements and balance sheets over multiple years.

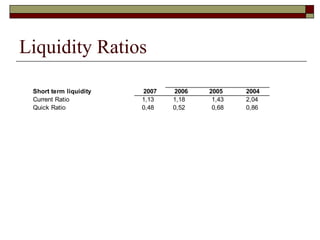

![Liquidity Ratios

Current ratio

Ability to meet short-term obligations

[Current assets/current liabilities]

Quick ratio

Remove less liquid assets

Keep cash, liquid investments, A/R

[(Cash+short-term investments + A/R)/current liabilities]](https://image.slidesharecdn.com/chapter14-5111-241203172931-44f57d0b/85/Chapter-14-511-1-ppt-financial-statments-21-320.jpg)

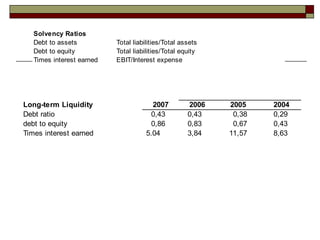

![Solvency Ratios

Debt to assets: Total liabilities/Total assets

Proportion of assets financed with debt

Could include interest bearing debt only

[(short term debt + noncurrent debt)/total assets]

Be aware that assets are recorded at historical

cost, which may be different from current

market value](https://image.slidesharecdn.com/chapter14-5111-241203172931-44f57d0b/85/Chapter-14-511-1-ppt-financial-statments-23-320.jpg)

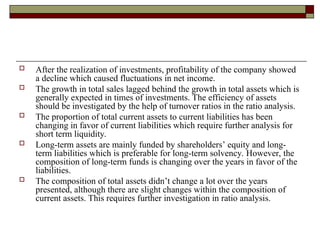

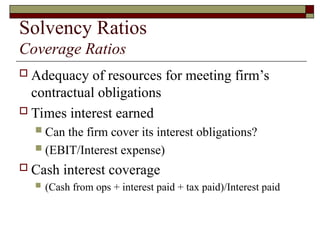

![Price Multiple Ratios

Market’s valuation of a firm’s common stock

P/E = Share price/Earnings per share

Price/book ratio compares stock’s price to the

recorded value of the net assets

[Share price/(Book value of equity/Share outstanding)]

Market Ratios 2007 2006 2005 2004

Price earnings ratio 12,73 46,67 16,93 11,16

price to book value 1,35 1,34 1,49 1,28](https://image.slidesharecdn.com/chapter14-5111-241203172931-44f57d0b/85/Chapter-14-511-1-ppt-financial-statments-32-320.jpg)