Rajarshi Shahu Mahavidyalaya,Latur

(Autonomous)

Department Of Commerce

Financial Accounting I

B.Com I (Sem I)

Miss. S. N. Bagwan

M. Com., NET, SET.

2.

Introduction to Accountancy

Introduction

Inall activities and in all organisations which require money and other

economic resources accounting is required to account for these

resources.

In other words ,wherever money resource is involved accounting is

required to account for it.

3.

Meaning and Definition

Bookkeeping

Bookkeepingis a process of recording business transaction in the books of

accounts in very systematic manner.

According to J. R. Batliboi, “bookkeeping is an art of recording business

dealings in a set of books”

Accountancy

Accountancy refers to a systematic knowledge of accounting. It explains

‘why to do’ and ‘how to do’ of various aspects of accounting. It tells us why

and how to prepare the books of accounts and how to summarise the

accounting information and communicate it to the interested parties.

According to Kohler, “Accountancy refers to the entire body of theory and

process of accounting”.

4.

Accounting

Accounting is oftencalled as a language of a business. The basic

function of any language is to serve as a means of communication

accounting is also serve this function by communicating information to

the users.

According to American Accounting Association, 1966, “Accounting is

the process of identifying, measuring, and communicating economic

information to permit informed judgements and decisions by uses of

information.”

5.

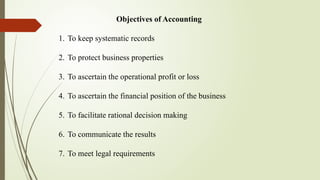

Objectives of Accounting

1.To keep systematic records

2. To protect business properties

3. To ascertain the operational profit or loss

4. To ascertain the financial position of the business

5. To facilitate rational decision making

6. To communicate the results

7. To meet legal requirements

6.

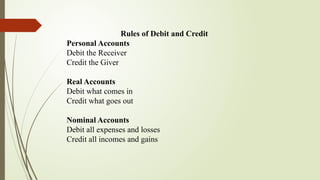

Rules of Debitand Credit

Personal Accounts

Debit the Receiver

Credit the Giver

Real Accounts

Debit what comes in

Credit what goes out

Nominal Accounts

Debit all expenses and losses

Credit all incomes and gains