FINAL MATTERS - AUDITING STUDY NOTES

The document discusses final matters related to auditing, including written representations, subsequent events, and facts discovered after the auditor's report. It defines written representations as written statements from management to confirm certain matters or support audit evidence. It outlines the representations required by ISAs regarding management responsibilities, financial statements, and specific assertions. It describes the auditor's course of action if oral or written representations are provided, including evaluating the reliability of written representations. It also outlines steps the auditor would take if written representations are not provided. The document explains the auditor's responsibility regarding events between the financial statement date and the auditor's report date. It lists procedures for the auditor to fulfill this responsibility, such as inquiring with management

Recommended

More Related Content

What's hot

What's hot (20)

Similar to FINAL MATTERS - AUDITING STUDY NOTES

Similar to FINAL MATTERS - AUDITING STUDY NOTES (20)

More from MUHAMMAD HUZAIFA CHAUDHARY

More from MUHAMMAD HUZAIFA CHAUDHARY (20)

Recently uploaded

Recently uploaded (20)

FINAL MATTERS - AUDITING STUDY NOTES

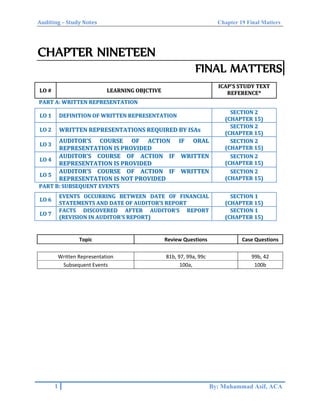

- 1. Auditing – Study Notes Chapter 19 Final Matters CHAPTER NINETEEN FINAL MATTERS LLOO ## LLEEAARRNNIINNGG OOBBJJCCTTIIVVEE IICCAAPP''SS SSTTUUDDYY TTEEXXTT RREEFFEERREENNCCEE** PPAARRTT AA:: WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN LLOO 11 DDEEFFIINNIITTIIOONN OOFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN SSEECCTTIIOONN 22 ((CCHHAAPPTTEERR 1155)) LLOO 22 WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONNSS RREEQQUUIIRREEDD BBYY IISSAAss SSEECCTTIIOONN 22 ((CCHHAAPPTTEERR 1155)) LLOO 33 AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF OORRAALL RREEPPRREESSEENNTTAATTIIOONN IISS PPRROOVVIIDDEEDD SSEECCTTIIOONN 22 ((CCHHAAPPTTEERR 1155)) LLOO 44 AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN IISS PPRROOVVIIDDEEDD SSEECCTTIIOONN 22 ((CCHHAAPPTTEERR 1155)) LLOO 55 AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN IISS NNOOTT PPRROOVVIIDDEEDD SSEECCTTIIOONN 22 ((CCHHAAPPTTEERR 1155)) PPAARRTT BB:: SSUUBBSSEEQQUUEENNTT EEVVEENNTTSS LLOO 66 EEVVEENNTTSS OOCCCCUURRRRIINNGG BBEETTWWEEEENN DDAATTEE OOFF FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS AANNDD DDAATTEE OOFF AAUUDDIITTOORR’’SS RREEPPOORRTT SSEECCTTIIOONN 11 ((CCHHAAPPTTEERR 1155)) LLOO 77 FFAACCTTSS DDIISSCCOOVVEERREEDD AAFFTTEERR AAUUDDIITTOORR’’SS RREEPPOORRTT ((RREEVVIISSIIOONN IINN AAUUDDIITTOORR’’SS RREEPPOORRTT)) SSEECCTTIIOONN 11 ((CCHHAAPPTTEERR 1155)) Topic Review Questions Case Questions Written Representation 81b, 97, 99a, 99c 99b, 42 Subsequent Events 100a, 100b 1 By: Muhammad Asif, ACA

- 2. Auditing – Study Notes Chapter 19 Final Matters PART A – WRITTEN REPRESENTATION LLOO 11:: DDEEFFIINNIITTIIOONN OOFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN:: Definition of written representations: A written statement by management provided to the auditor to confirm certain matters or to support other audit evidence. Objective of written representation is: 1. To obtain acknowledgement from management and TCWG that they have fulfilled their responsibilities in an audit. 2. To support certain matters for which representation is crucial in obtaining evidence. Use of Written Representation as Audit Evidence: Written Representation is an evidence, however, it is not a sufficient appropriate audit evidence unless corroborated by other evidence which is expected to exist. It is only a supporting evidence and does not affect nature, timing and extent of other evidence to be obtained. Form and Date of written representations: Written representations shall be: addressed to auditor. in the form of a letter signed by persons responsible for preparation of financial statements e.g. CEO and CFO. dated as near as possible, but not after, the date of auditor’s report. CONCEPT REVIEW QUESTION The audit of Three Stars Limited (TSL) for the year ended December 31, 2014 was completed and initial report was issued on February 15, 2015. The meeting of the board of director was held on February 22, 2015 to approve the accounts and thereafter, being an auditor, you have been required to issue signed auditor’s report for the purposes of issuing financial statements to shareholders. As per the provisions of International Standards on Auditing, you also need to obtain a written representation from your client (TSL) before issuing the signed auditor’s report. Required: In the light of the given situation, answer the following: (i) Briefly explain the term “written representation”. Why does an auditor need to obtain a written representation from management and those charged with governance. (04 marks) (ii) What is the most commonly used form of a written representation and what should be the date of written representation in the above scenario? Discuss in the light of ISA – 580. (04 marks) (iii) Who is responsible to provide the written representation on behalf of the company. (02 marks) (ICMAP – 2015 August) LLOO 22:: WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONNSS RREEQQUUIIRREEDD BBYY IISSAAss:: Written Representation about Management’s Responsibilities: Representations about Financial Statements: Management has fulfilled its responsibility for the preparation of financial statements in accordance with the AFRF, as agreed in the terms of the audit engagement. Representations about Information Provided to Auditor: a) Management has provided the auditor with all relevant information and access, as agreed in the terms of the audit engagement, and b) All transactions have been recorded in financial statements. 2 By: Muhammad Asif, ACA

- 3. Auditing – Study Notes Chapter 19 Final Matters Written Representation about Specific Assertions: Representations about Financial Statements: 1. Significant assumptions and accounting estimates are reasonable. (ISA 540) 2. Related party relationships and transactions have been appropriately accounted for and disclosed in accordance with the requirements of AFRF. (ISA 550) 3. All events subsequent to the date of financial statements for which AFRF requires adjustment or disclosure, have been adjusted or disclosed. (ISA 560) 4. The effects of uncorrected misstatements are immaterial, both individually and in the aggregate, to the financial statements as a whole. (ISA 450) Representations about Information Provided to Auditor: 1. We have disclosed to you the results of our assessment of the risk that the financial statements may be materially misstated as a result of fraud. (ISA 240) 2. We have disclosed to you all information in relation to fraud or suspected fraud that we are aware of and that affects the entity involving management, employees or others. (ISA 240) 3. We have disclosed to you the identity of the entity’s related parties and all the related-party relationships and transactions of which we are aware. (ISA 550) 4. We have disclosed to you all known instances of non-compliance or suspected non- compliance with laws and regulations affecting financial statements. (ISA 250) Auditor may also obtain additional representations if he considers necessary. CONCEPT REVIEW QUESTION What are the situations in which written representation from the management is mandatory? (07 marks) (CA Final – Winter 2008) Representations by management are considered as audit evidence. Describe the basic elements of a management representation letter. (04 marks) (CA Inter – Spring 2009) LLOO 33:: AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF OORRAALL RREEPPRREESSEENNTTAATTIIOONN IISS PPRROOVVIIDDEEDD:: Although oral representation is an evidence, however it is less reliable than written representation. Auditor should document oral representation but should also request management to provide representation in written. LLOO 44:: AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN IISS PPRROOVVIIDDEEDD:: Evaluating Reliability of written representation: If management provides written representation to auditor, auditor is required to evaluate reliability of representations made by management. To evaluate reliability of written representation, auditor considers following matters: Consistency with other representations and other evidence from different sources. Competence, integrity, ethical values or diligence of management. Whether individual making written representation is well informed on such matters. Accuracy of representations made in the past. If reliability of written representation is doubtful: If written representation is inconsistent with other evidence: Auditor should consider: 3 By: Muhammad Asif, ACA

- 4. Auditing – Study Notes Chapter 19 Final Matters Whether his risk assessment of that area is still appropriate. If not, revise risk assessment. Consider need to revise nature, timing and extent of audit procedures to respond to revised risk. If auditor has concerns about integrity of management, he may take further action as described below. If auditor has concerns about integrity of management: Auditor shall: determine effect of such concerns on reliability of other representations and audit evidence in general. document the concerns and should consider withdrawing from engagement in extreme cases, unless TCWG take appropriate actions. If withdrawal is not possible, he may express disclaimer of opinion. CONCEPT REVIEW QUESTION One of the objectives of obtaining a written representation from management is to ensure that the management knows and acknowledges its responsibility for the preparation of the financial statements and for the completeness of the information provided to the auditor. Required: Specify the situations which may create doubts as to the reliability of written representations. What course of action would the auditor take in such a situation? (07 marks) (CA Inter – Spring 2011) You are the audit partner of XYZ & Company, Chartered Accountants. The following matters are under your consideration: (a) Asif Limited has made certain investments and has classified them as long term investments. The management has also provided written representation in this regard. However, before the finalization of financial statements the company disposed of some of the said investments. (04 marks) (b) Mansoor Limited has entered into significant related party transactions during the year which are approved by the Board of Directors and appropriately disclosed. The management has also agreed to provide a written representation but you have not received it yet. (03 marks) Required: Analyse the above situations and explain how you would proceed in the above matters. (CA Inter – Spring 2016) LLOO 55:: AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN IIFF WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN IISS NNOOTT PPRROOVVIIDDEEDD:: If management refuses to provide written representation to auditor, auditor shall perform following procedures. Discussion with management: Auditor shall discuss the matter with management and shall inquire reason for refusal. Impact on different aspects of audit: Auditor shall: Re-evaluate integrity of management and consequently revise risk of material misstatement, including risk of fraud. Take appropriate actions, including considering effect on other audit procedures (including other representations and evidence provided by management). If auditor has serious concerns about integrity of management, consider withdrawing from the audit. Impact on audit report: Not providing representation is a scope limitation. Auditor may express qualified opinion (if possible effect is material) or disclaimer of opinion (if possible effect is pervasive). 4 By: Muhammad Asif, ACA

- 5. Auditing – Study Notes Chapter 19 Final Matters CONCEPT REVIEW QUESTION As part of the audit process, the management provides written representations to confirm certain matters in connection with the audit. Required: (a) State the matters that you will consider as an auditor while assessing the reliability of representations made by the management. (05 marks) (b) Describe the course of action available to an auditor if the management refuses to provide representation on a particular issue. (05 marks) (CA Inter – Spring 2012) PART B – SUBSEQUENT EVENTS LLOO 66:: EEVVEENNTTSS OOCCCCUURRRRIINNGG BBEETTWWEEEENN DDAATTEE OOFF FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS AANNDD DDAATTEE OOFF AAUUDDIITTOORR’’SS RREEPPOORRTT:: Auditor’s Responsibility/Purpose: Auditor’s responsibility is to perform audit procedures to obtain sufficient appropriate audit evidence that all events occurring between the date of the financial statements and the date of the auditor’s report have been identified by management and have been adjusted or disclosed in financial statements, as appropriate. To meet his responsibility, auditor performs Active Review of subsequent events (i.e. auditor actively searches for significant subsequent events). Auditor’s Procedures to fulfill responsibility: 1) Inquiring of management and TCWG as to whether any subsequent events have occurred which might affect the financial statements (auditor may make specific inquiries relating to adjusting events or non-adjusting events) e.g. a. New borrowings b. Significant sales of assets c. New shares or debentures issued d. Assets destroyed by fire, flood etc or appropriated by government. 2) Obtaining an understanding of procedures established by management to identify subsequent events. 3) Reading minutes of subsequent meetings of the entity’s owners, management and TCWG and inquiring about matters discussed at any such meetings for which minutes are not yet available. 4) Reading the entity’s subsequent interim financial statements, if any. 5) Requesting management to provide written representation that “all events subsequent to the date of the financial statements requiring adjustment or disclosure have been adjusted or disclosed”. CONCEPT REVIEW QUESTION (a) Briefly describe the extent of auditor’s responsibility relating to subsequent events occurring between the date of the financial statements and the auditor’s report. (03 marks) (b) Identify any five procedures that the auditor may undertake to fulfill the responsibility as discussed in (a) above. (05 marks) (CA Inter – Autumn 2013) 5 By: Muhammad Asif, ACA

- 6. Auditing – Study Notes Chapter 19 Final Matters LLOO 77:: FFAACCTTSS DDIISSCCOOVVEERREEDD AAFFTTEERR AAUUDDIITTOORR’’SS RREEPPOORRTT ((RREEVVIISSIIOONN IINN AAUUDDIITTOORR’’SS RREEPPOORRTT)):: Auditor’s Responsibility/Purpose: Auditor has no responsibility to perform any audit procedures regarding financial statements after the date of auditor’s report. However, auditor is responsible to respond appropriately to facts which affect financial statements and auditor’s report but that become known to the auditor after the date of the auditor’s report. For this purpose, auditor performs Passive Review of subsequent events (i.e. auditor does not search subsequent events actively; rather he relies on information from management) Auditor’s Procedures to fulfill responsibility: If after the date of auditor’s report, auditor becomes aware of a misstatement in financial statements (e.g. an error/fraud in financial statements), auditor shall: Discuss with management to determine whether financial statements need amendment. If amendment is required, auditor shall inquire whether management agrees to amend financial statements or not. If management agrees to amend financial statements If management does not agree to amend financial statements When financial statements have not been issued Management’s Responsibilities: –Management shall amend financial statements before issuance. Auditor’s Responsibilities: Auditor shall: –Carry out necessary audit procedures on the amendment. –Provide a new audit report (on the amended financial statements). 1. If auditor’s report has not been provided to entity, auditor shall modify the opinion. 2. If auditor’s report has been provided to entity, auditor shall notify management and TCWG not to issue the financial statements to third parties. When financial statements have been issued Management’s Responsibilities: –Management take necessary steps to ensure that users do not rely on previously issued financial statements. –Management shall amend financial statements to re-issue them. These financial statements shall include an additional note to explain the reason for the amendment. Auditor’s Responsibilities: Auditor shall: – Review the steps taken by management to ensure that users do not rely on previously issued financial statements. –Carry out necessary audit procedures on the amendment. –Provide a new audit report (on amended financial statements) that shall include an Emphasis of Matter Paragraph or Other Matter Paragraph, referring to the note in financial statements that explains reason for the amendment in financial statements, or earlier report provided by the auditor. Auditor shall take appropriate action to ensure that users are informed not to rely on financial statements and auditor’s report. 6 By: Muhammad Asif, ACA

- 7. Auditing – Study Notes Chapter 19 Final Matters CONCEPT REVIEW QUESTION Describe the auditor’s responsibility for subsequent events occurring between: (i) The year-end date and the date the auditor’s report is signed; and (ii) The date the auditor’s report is signed and the date the financial statements are issued. (05 marks) (ACCA December 2011) ABC, Chartered Accountants released a qualified audit report on financial statements of Normal Limited due to a disagreement on tax provisions. Before issuance of financial statements and audit report to the shareholders, the management revised the financial statements on the basis of subsequent decisions announced by the appellate authorities. The adjustment made in revised financial statements now agrees with the previously suggested audit adjustments. The revised financial statements have been provided to ABC for fresh audit report. Required: List the steps which ABC, Chartered Accountants should take before issuing a revised (unqualified) audit report. (06 marks) (CA Inter – Spring 2008) Masoom & Co. Chartered Accountants have audited the financial statements of Cunning Limited. The financial statements have been issued after getting proper approval of the Board of Directors and audit report signed by the auditors. After some time, the auditors came to know that a major lawsuit was decided against the company subsequent to the year-end but before the audit report was signed by the auditors. The issue existed at the balance sheet date. The outcome of the lawsuit was not brought to the knowledge of the auditors. Had it been known to the auditors, the financial statements would have required proper adjustments in this respect. State auditors’ responsibilities in this situation. Also analyze the situation, if the issue of financial statements for the following period is imminent. (06 marks) (CA Inter – Spring 2004) 7 By: Muhammad Asif, ACA