Downloaded 35 times

![Investment Opportunities under

India’s Mega Plans

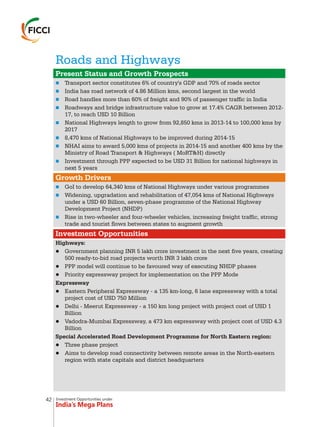

Economic Corridor (ECEC) with Chennai Vizag Industrial Corridor as the first phase of

the project (CVIC). A new 'National Industrial Corridor Development Authority' has

been created to coordinate, integrate, monitor and supervise development of these

Industrial Corridors. Work on the following corridors is underway:

Delhi-Mumbai Industrial Corridor: Work on 5 smart cities is in progress namely

Dholera, Shendra-Bidkin, Greater Noida, Ujjain and Gurgaon.

Chennai-Bengaluru Industrial Corridor: Master planning for 3 new Industrial

Nodes [Ponneri (TN), Krishnapatnam (AP), Tumkur (Karnataka)] is under progress.

The East Coast Economic Corridor (ECEC) with Chennai-Vizag Industrial Corridor:

Feasibility Study has been commissioned by Asian Development Bank.

Amritsar-Kolkata Industrial Corridor: Delhi-Mumbai Industrial Corridor

Development Corporation Limited (DMICDC) which is selected as the Nodal

Agency is conducting the feasibility study.

North-eastern part of India is planned to be linked with other Industrial Corridors

in cooperation with government of Japan.

New Industrial Clusters will be developed for promoting advance practices in

manufacturing.

21 Industrial projects have been approval under Modified Industrial Infrastructure

Upgradation Scheme with an emphasis on:

Use of recycled water through zero liquid discharging systems.

Central Effluent Treatment plants.

17 National Investment and Manufacturing zones have been approved

n

n

n

n

n

n

n

n

n

n

Bengaluru-

Mumbai

Economic

Corridor

(BMEC)

Chennai-

Bengaluru

Industrial

Corridor

(CBIC)

East Coast

Industrial

Corridor

(ECEC)

Amritsar-

Delhi-Kolkata

Insdustrial

Corridor

(AKIC)

Delhi-Mumbai

Industrial

Corridor

(DMIC)

Industrial

Corridors

15](https://image.slidesharecdn.com/ficcipaperonmegaplans-150311113804-conversion-gate01/85/FICCI-paper-on-Mega-Plans-21-320.jpg)

![Investment Opportunities under

India’s Mega Plans

Skill Development by Ministry of Human Resource Development

Ministry of Human Resource Development is taking forward the skill development

agenda through following programmes:

Vocationalisation of Secondary Education covering (6800 schools covered)

Polytechnics (1244) +Institutions for diploma in pharmacy (415), hotel

management (63), architecture(25)

Community Polytechnic Scheme (675 CPs)

Jan ShikshanSansthan (157 Vocational Training Centres run by NGOs offering more

than 250 courses )

National Institute of Open Schooling- Distance Vocational Education Programmes

offering [Practical training through Accredited Vocational Institutes (AVIs)]

Skill Development by Ministry of Information Technology

The Ministry of Information technology has visualized creating skill development

facilities in deprived areas through strengthening of National Institute of Electronics

and Information Technology (NIELIT). Under this scheme, capacity building in the

areas of Electronic Product Design and Production Technology has been initiated for

development of human resource at various levels including Certificate, Diploma, Post

Graduate and Research Professionals with adequate competence levels. The

programme targets training of 11,515 candidates in five years. The project further

aims at upgrading the competence of working professional in Indian industries and

knowledge/ skills of faculty of technical institutions.

Skill Development by Ministry of Tourism

Under the Scheme of "Capacity Building for Service Providers", the Ministry of Tourism

has decided to provide assistance to sponsored institutes to conduct Skill

Development Programmes called "HUNAR SE ROZGAAR". The Programme would offer

short but quality training courses covering (i) Food & Beverage Service and (ii) Food

Production. The programme would target persons with minimal means and in need to

acquire skills for basic employment.

Skill Development by Ministry of Housing & Urban Poverty Alleviation

The Ministry of Housing & Urban Poverty Alleviation (MHUPA) has announced to

undertake necessary skill development programmes for urban poor under

'DeenDayalAntyodayaYojana (DAY)'. Under DAY, the Ministry of HUPA intends to

undertake skill development of five lakh urban poor per year based on identified

market needs. This scheme will help in reducing poverty and vulnerability of the

urban poor households by enabling them to access gainful self-employment and

skilled wage employment opportunities, resulting in an appreciable improvement in

their livelihoods on a sustainable basis, through building strong grassroots level

institutions for the poor.

n

n

n

n

n

63](https://image.slidesharecdn.com/ficcipaperonmegaplans-150311113804-conversion-gate01/85/FICCI-paper-on-Mega-Plans-69-320.jpg)

The document discusses India's major policy reforms and investment opportunities under mega plans such as Make in India, Digital India, Smart Cities, Skill India, Swachh Bharat Abhiyan and Clean Ganga Mission. Key reforms include easing of FDI norms, proposed goods and services tax, labour reforms, and measures to boost manufacturing and improve ease of doing business. Major sectors highlighted for investment include automobiles, aviation, biotechnology, chemicals, construction, defence, electronics, food processing, IT/BPM, mining, pharmaceuticals, renewable energy, textiles, and tourism.