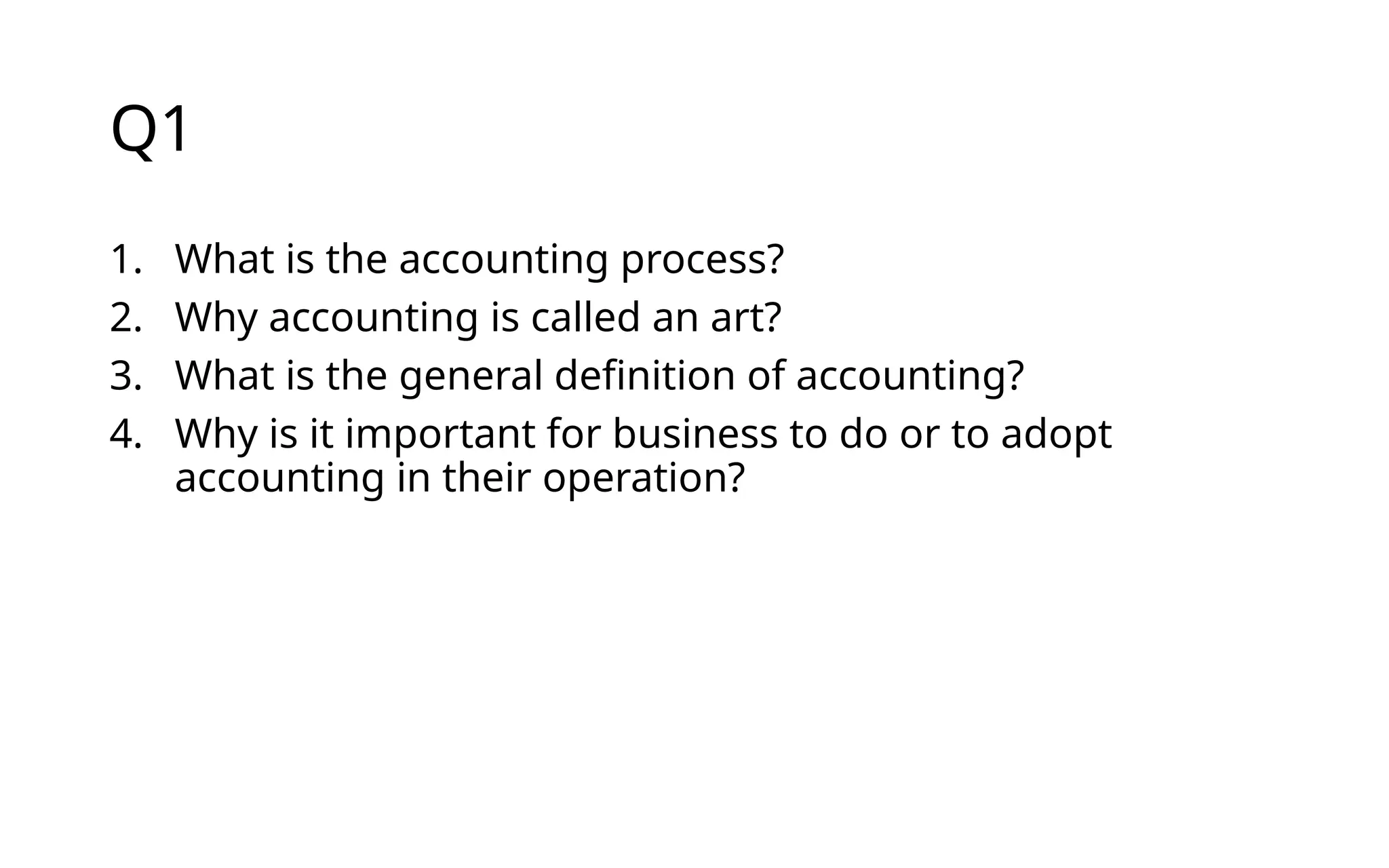

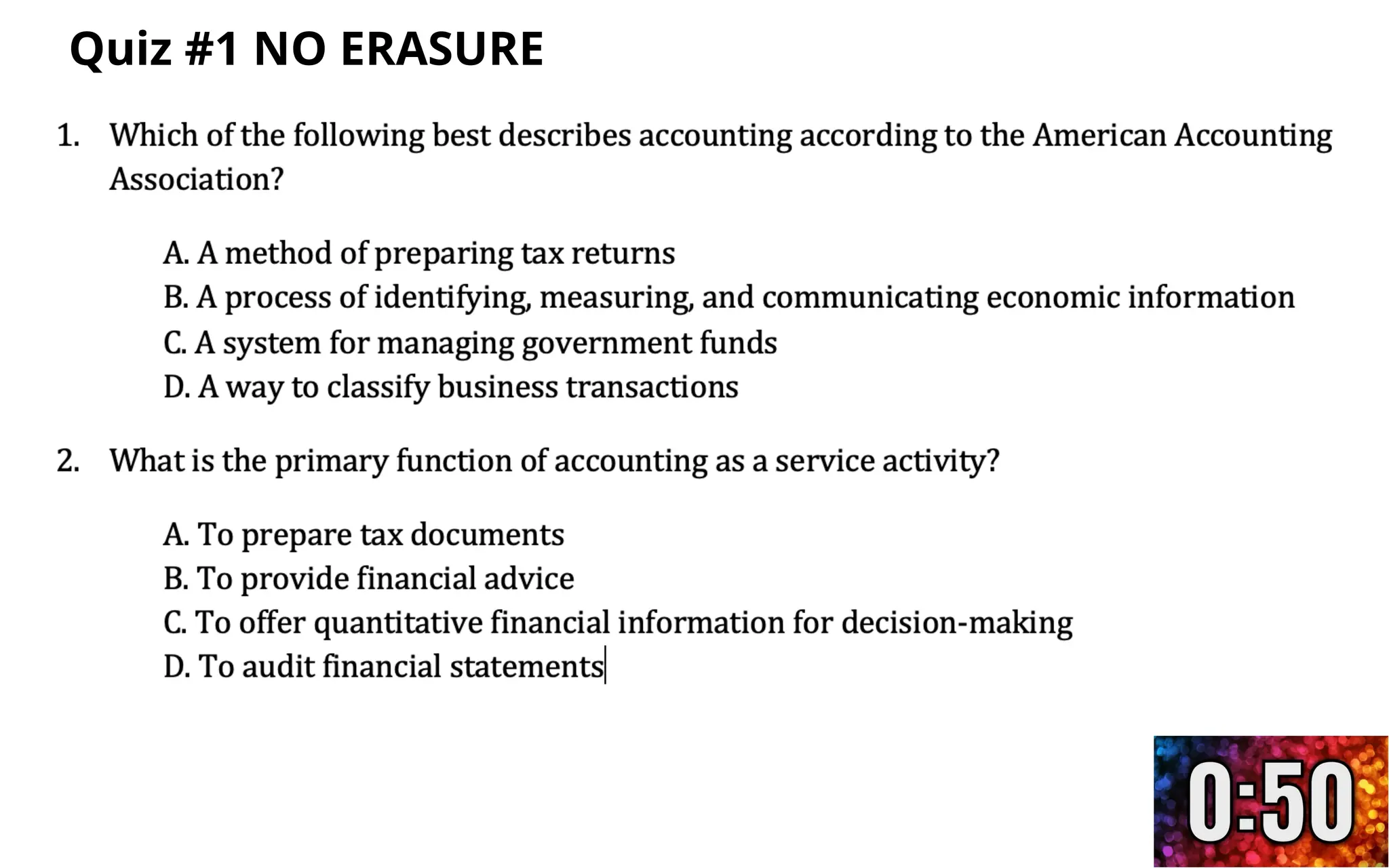

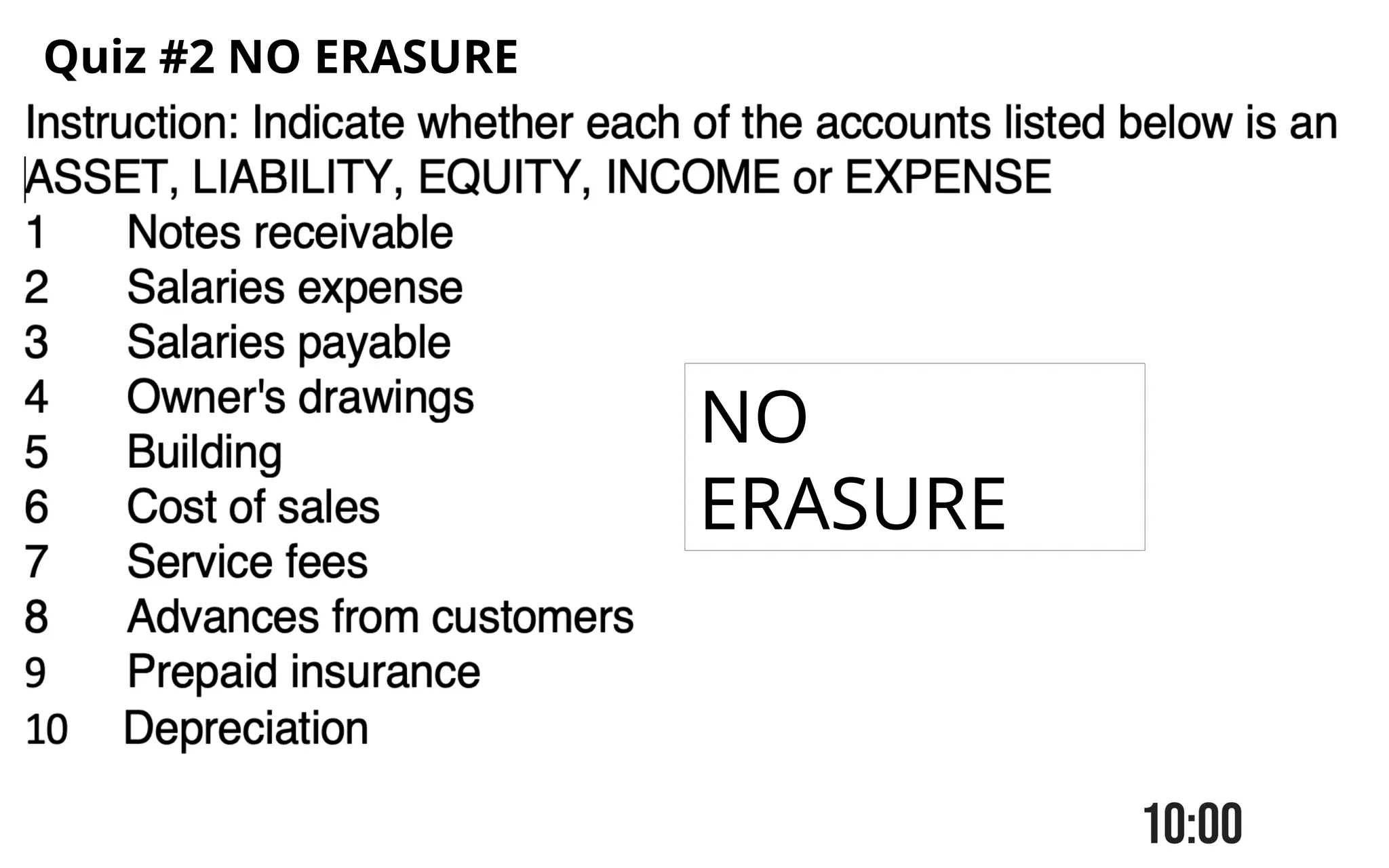

Q1

1. What isthe accounting process?

2. Why accounting is called an art?

3. What is the general definition of accounting?

4. Why is it important for business to do or to adopt

accounting in their operation?

5.

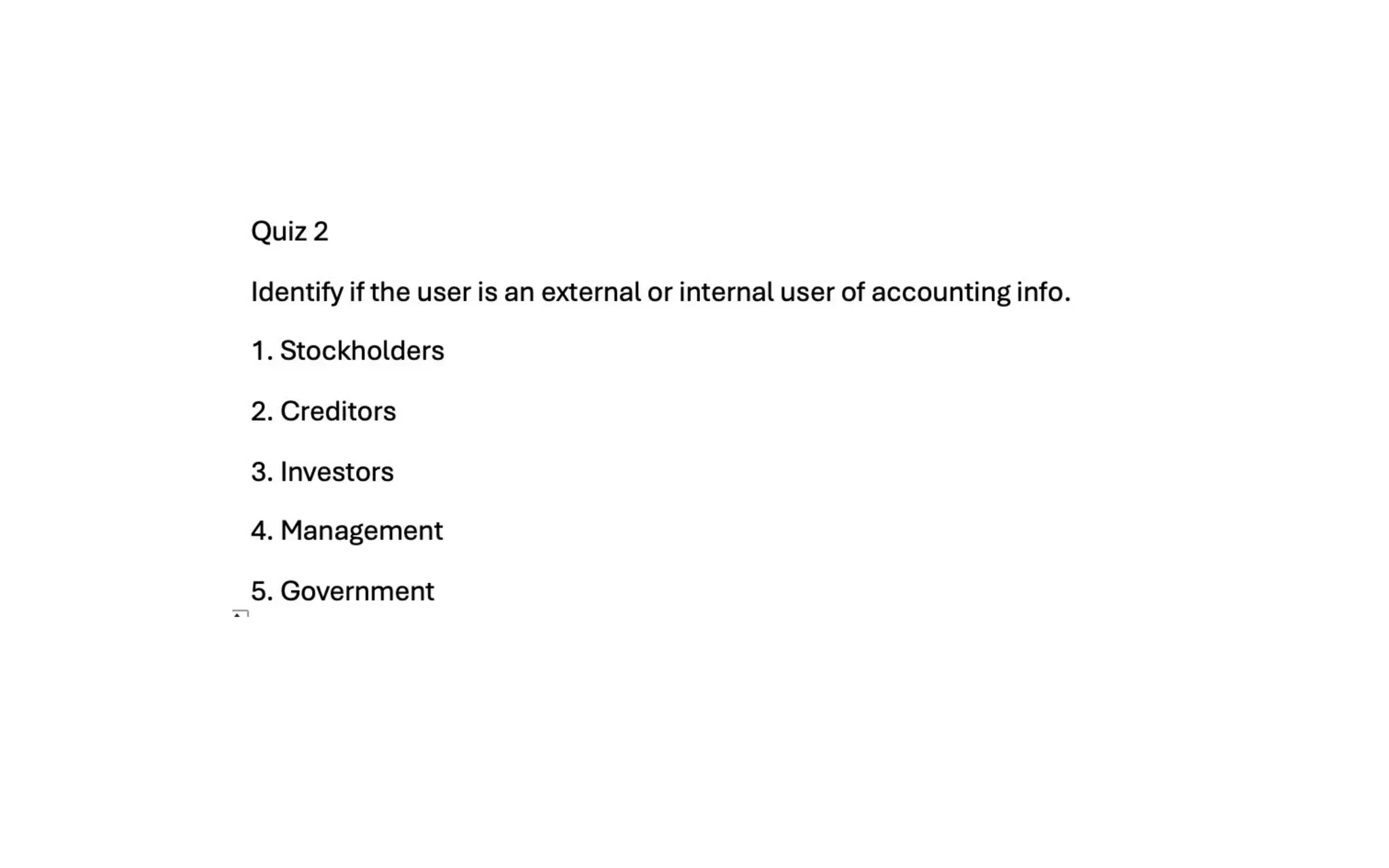

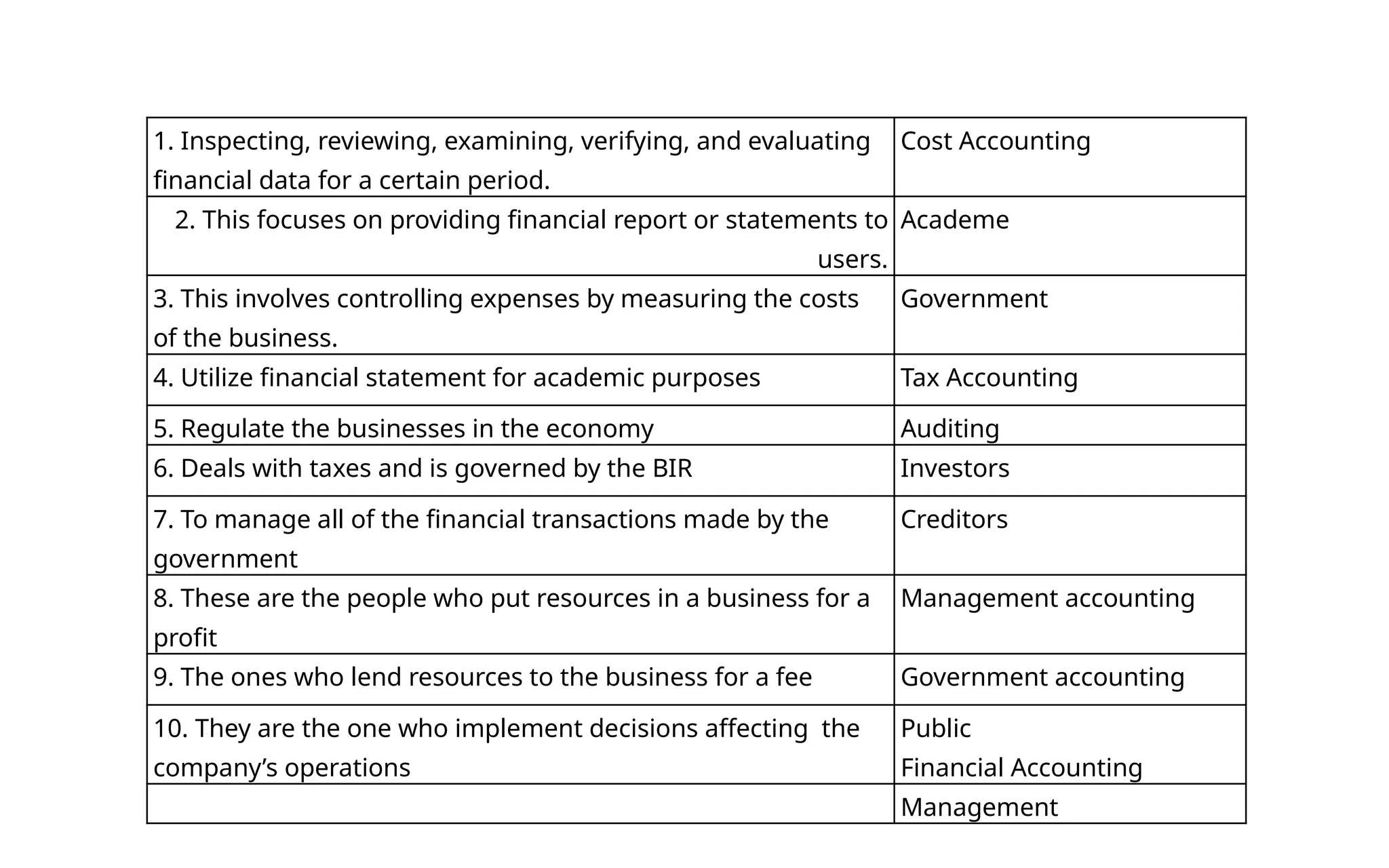

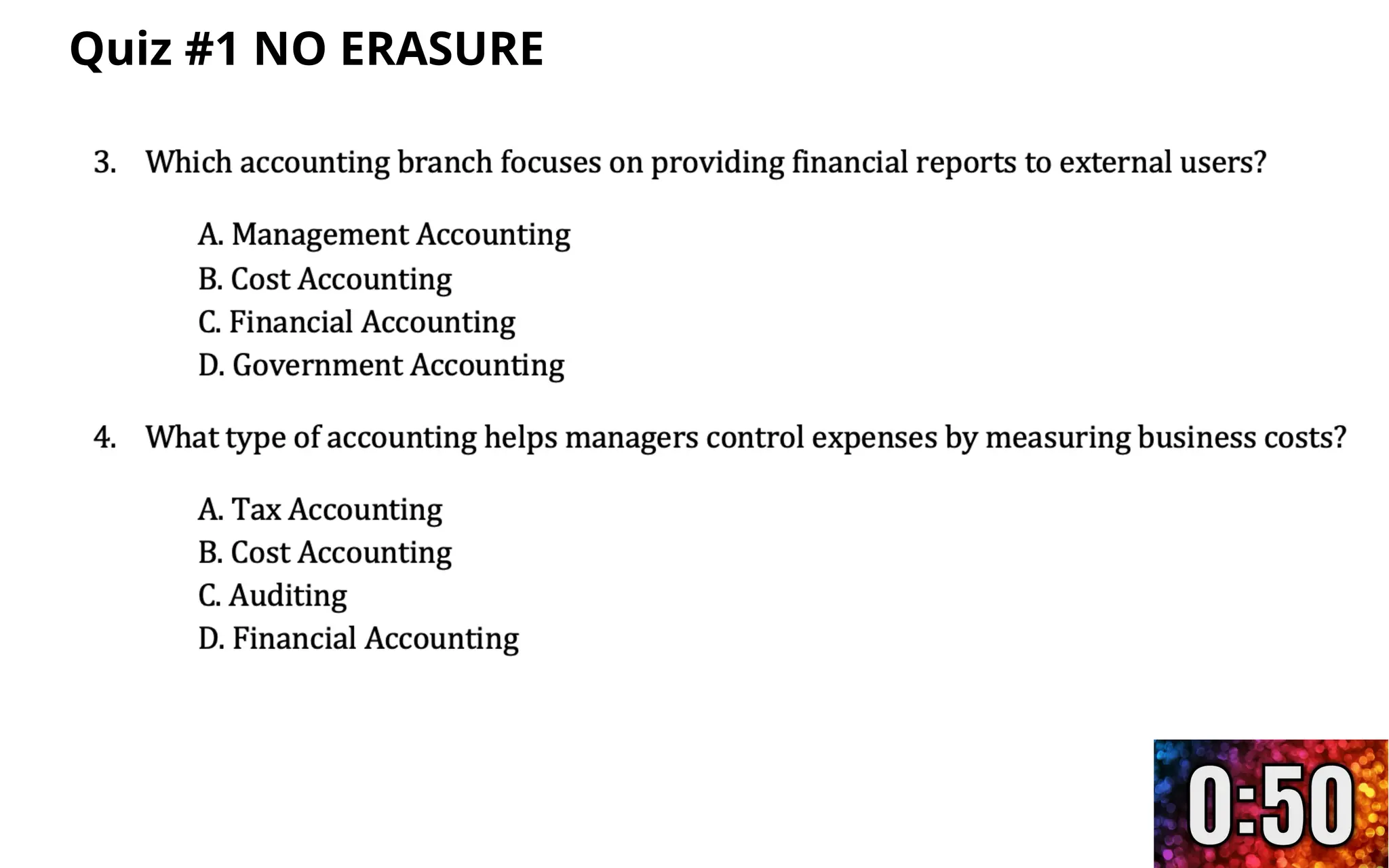

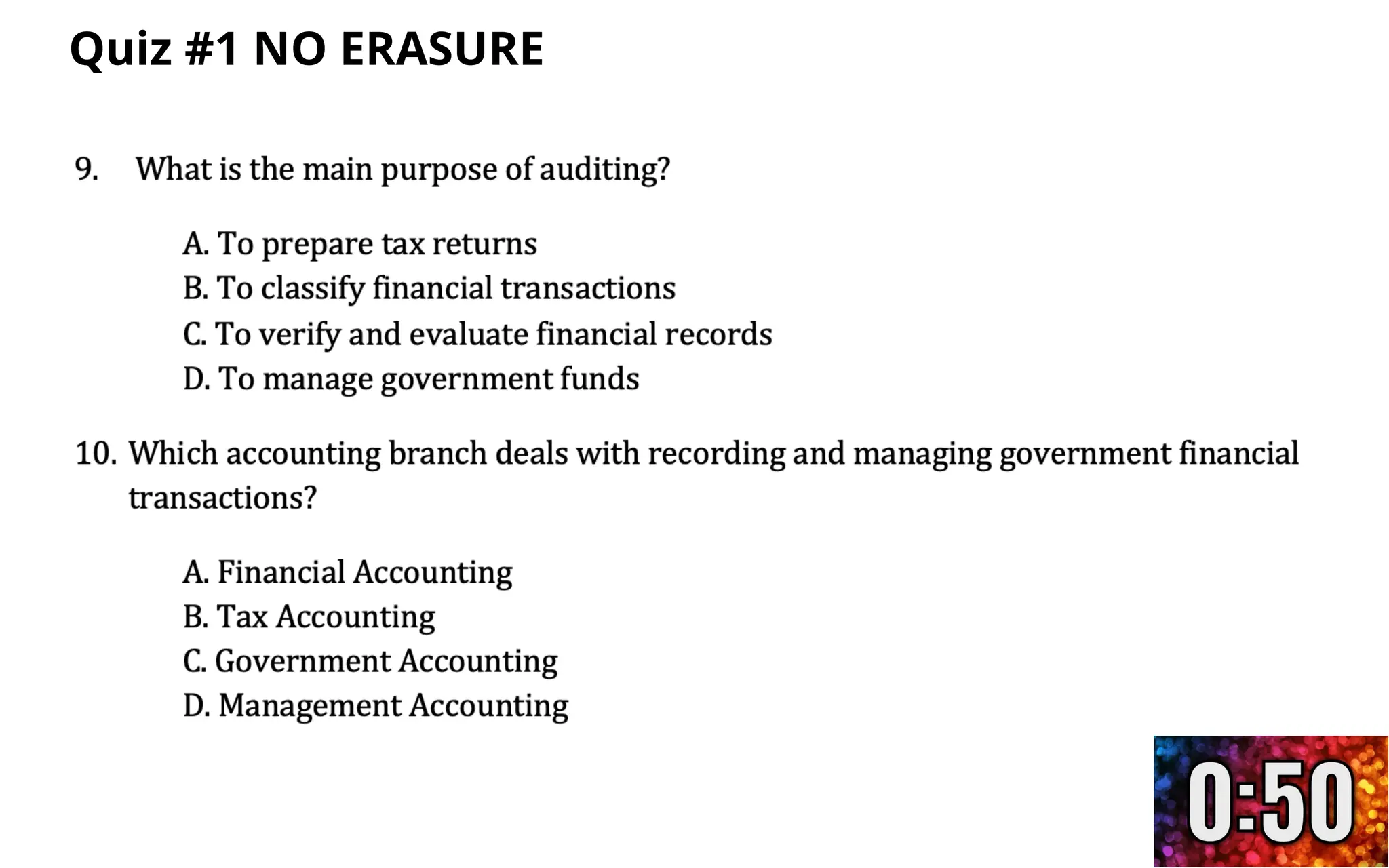

1. Inspecting, reviewing,examining, verifying, and evaluating

financial data for a certain period.

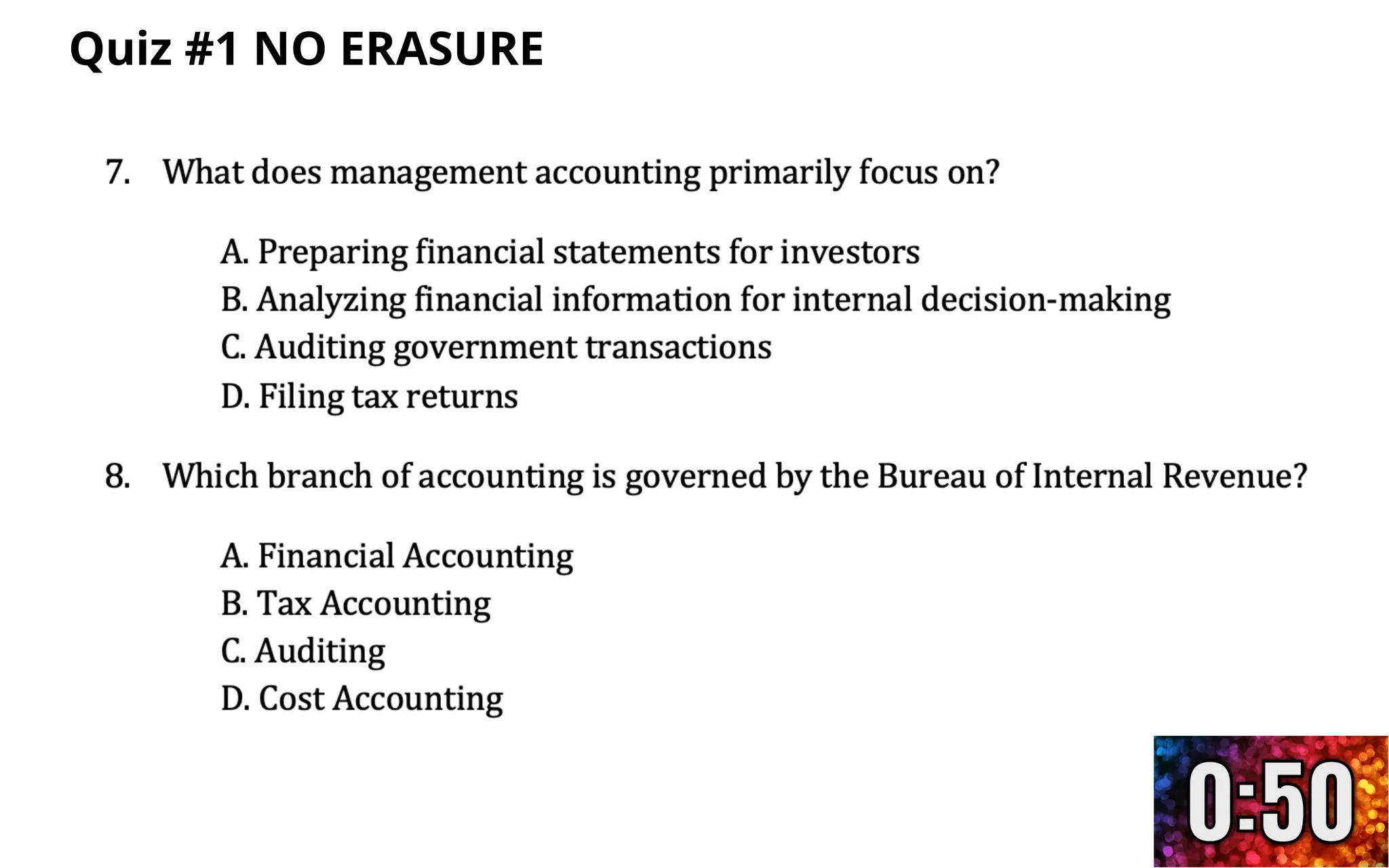

Cost Accounting

2. This focuses on providing financial report or statements to

users.

Academe

3. This involves controlling expenses by measuring the costs

of the business.

Government

4. Utilize financial statement for academic purposes Tax Accounting

5. Regulate the businesses in the economy Auditing

6. Deals with taxes and is governed by the BIR Investors

7. To manage all of the financial transactions made by the

government

Creditors

8. These are the people who put resources in a business for a

profit

Management accounting

9. The ones who lend resources to the business for a fee Government accounting

10. They are the one who implement decisions affecting the

company’s operations

Public

Financial Accounting

Management

8.

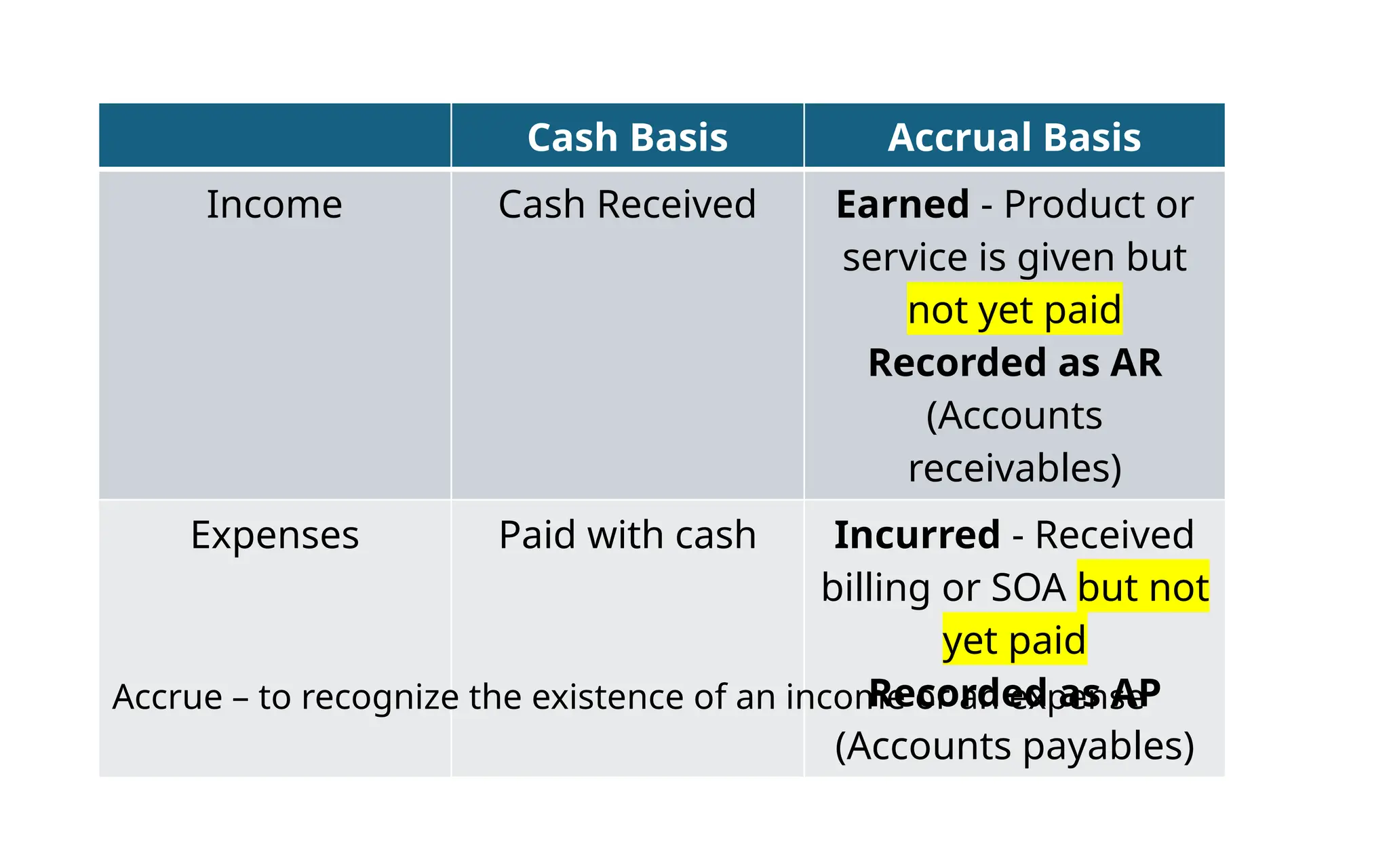

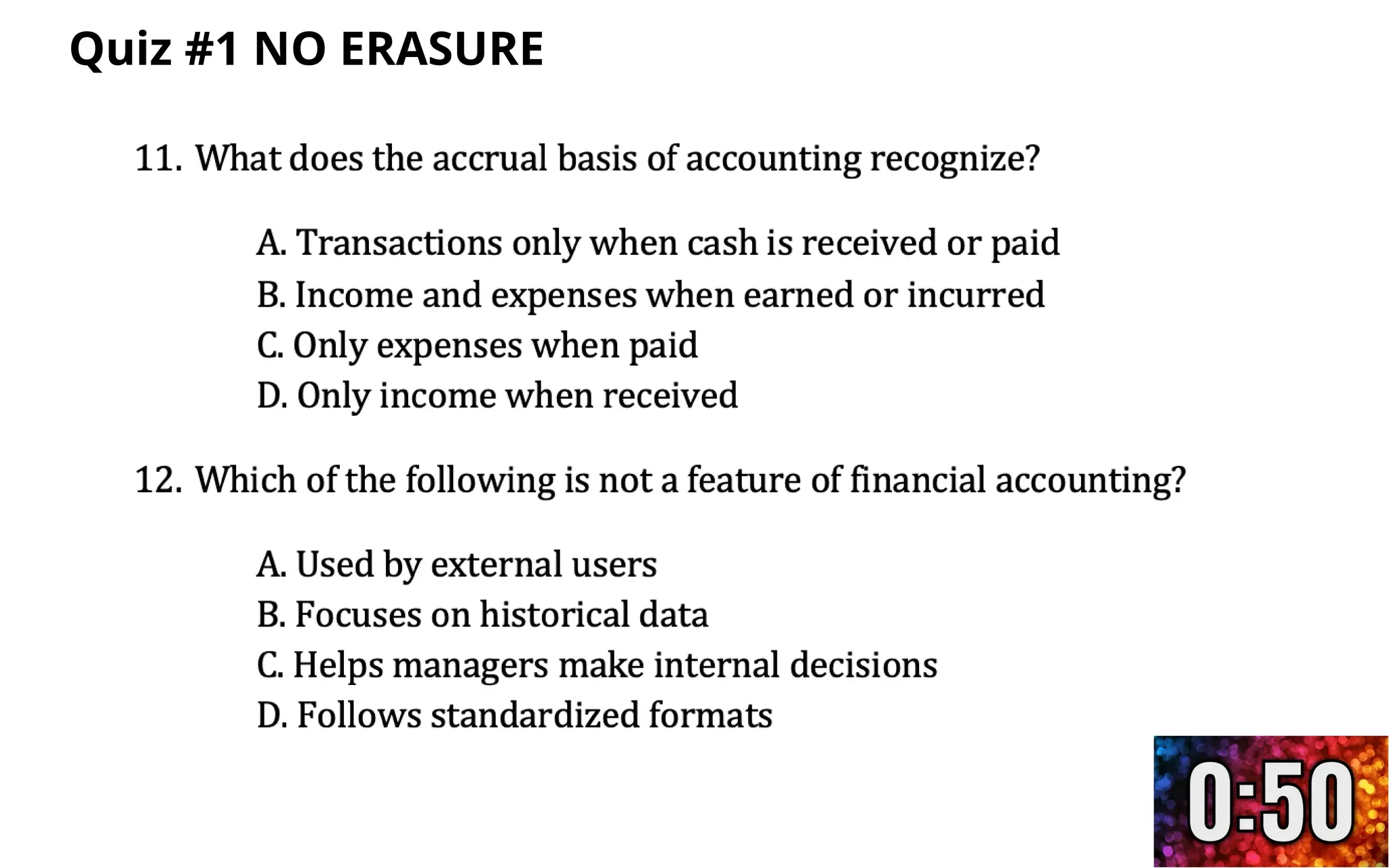

Cash Basis AccrualBasis

Income Cash Received Earned - Product or

service is given but

not yet paid

Recorded as AR

(Accounts

receivables)

Expenses Paid with cash Incurred - Received

billing or SOA but not

yet paid

Recorded as AP

(Accounts payables)

Accrue – to recognize the existence of an income or an expense

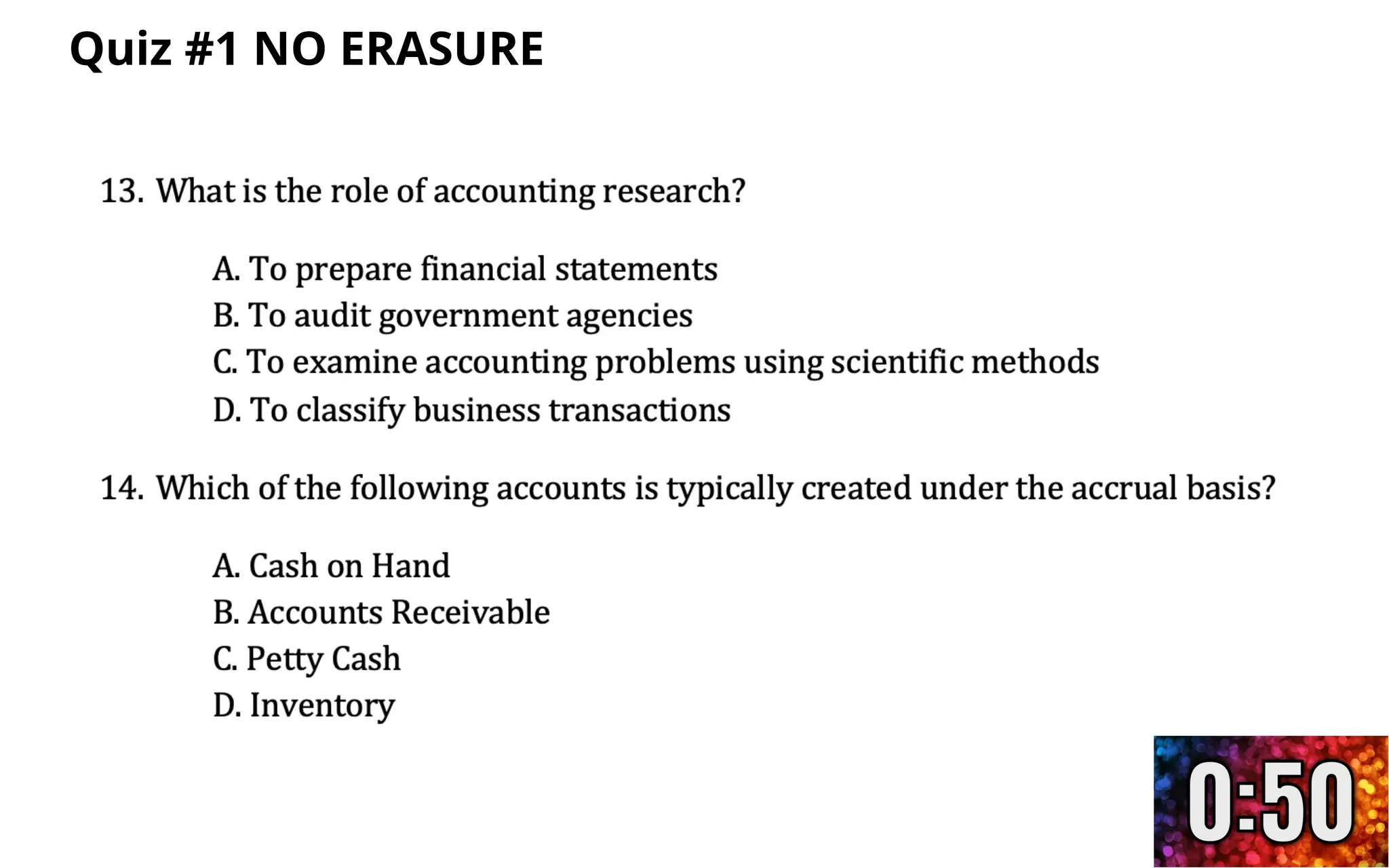

9.

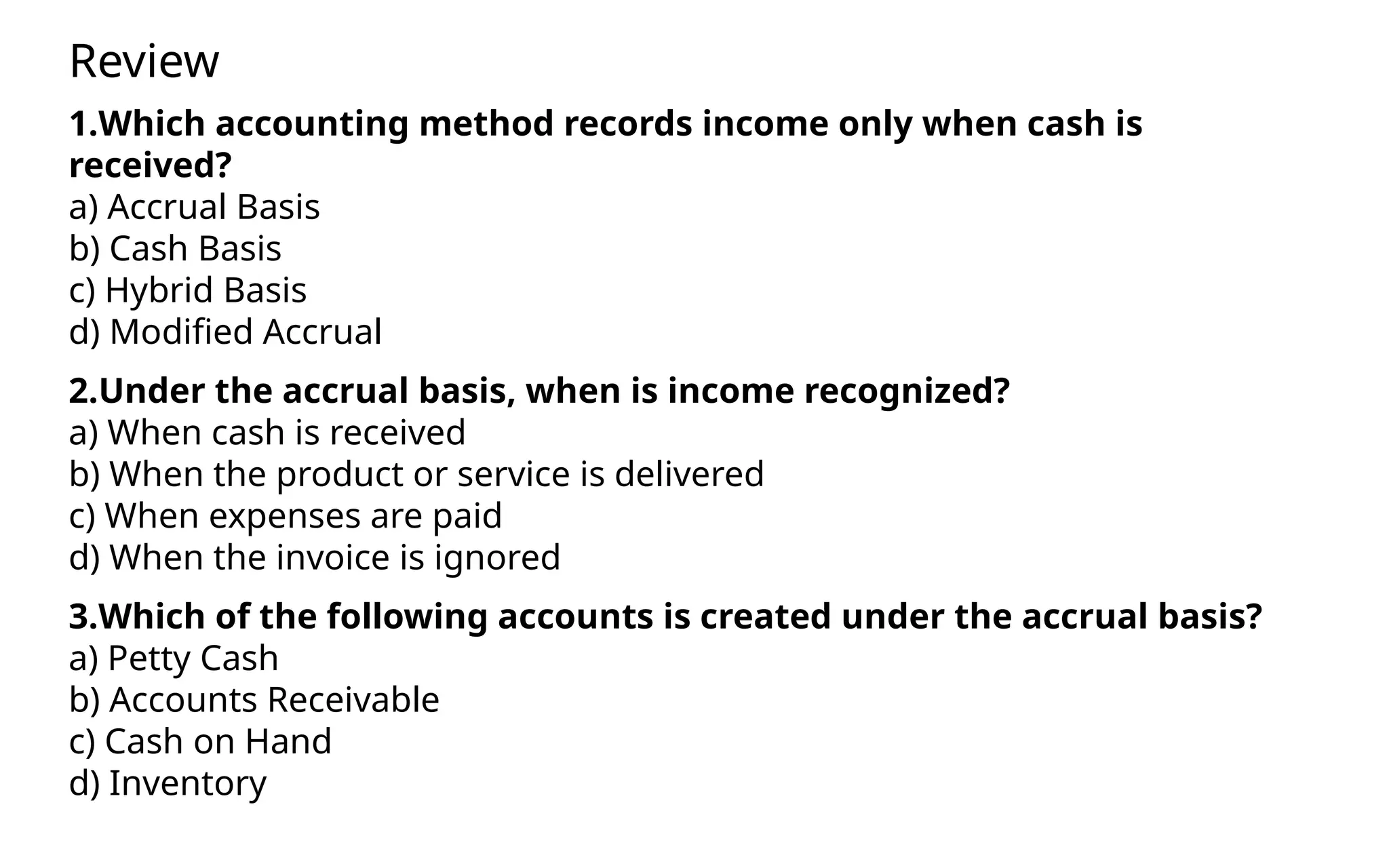

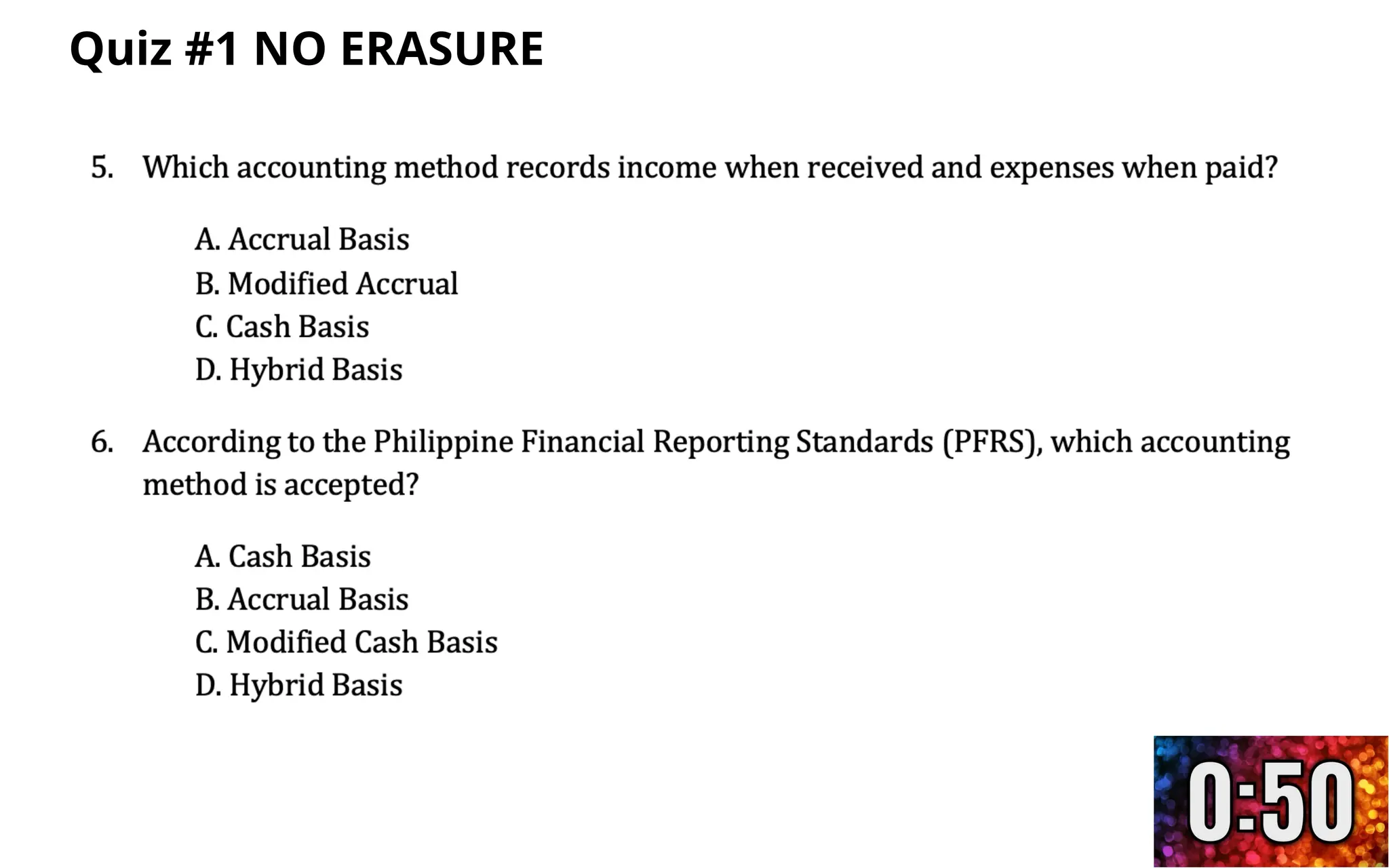

1.Which accounting methodrecords income only when cash is

received?

a) Accrual Basis

b) Cash Basis

c) Hybrid Basis

d) Modified Accrual

2.Under the accrual basis, when is income recognized?

a) When cash is received

b) When the product or service is delivered

c) When expenses are paid

d) When the invoice is ignored

3.Which of the following accounts is created under the accrual basis?

a) Petty Cash

b) Accounts Receivable

c) Cash on Hand

d) Inventory

Review

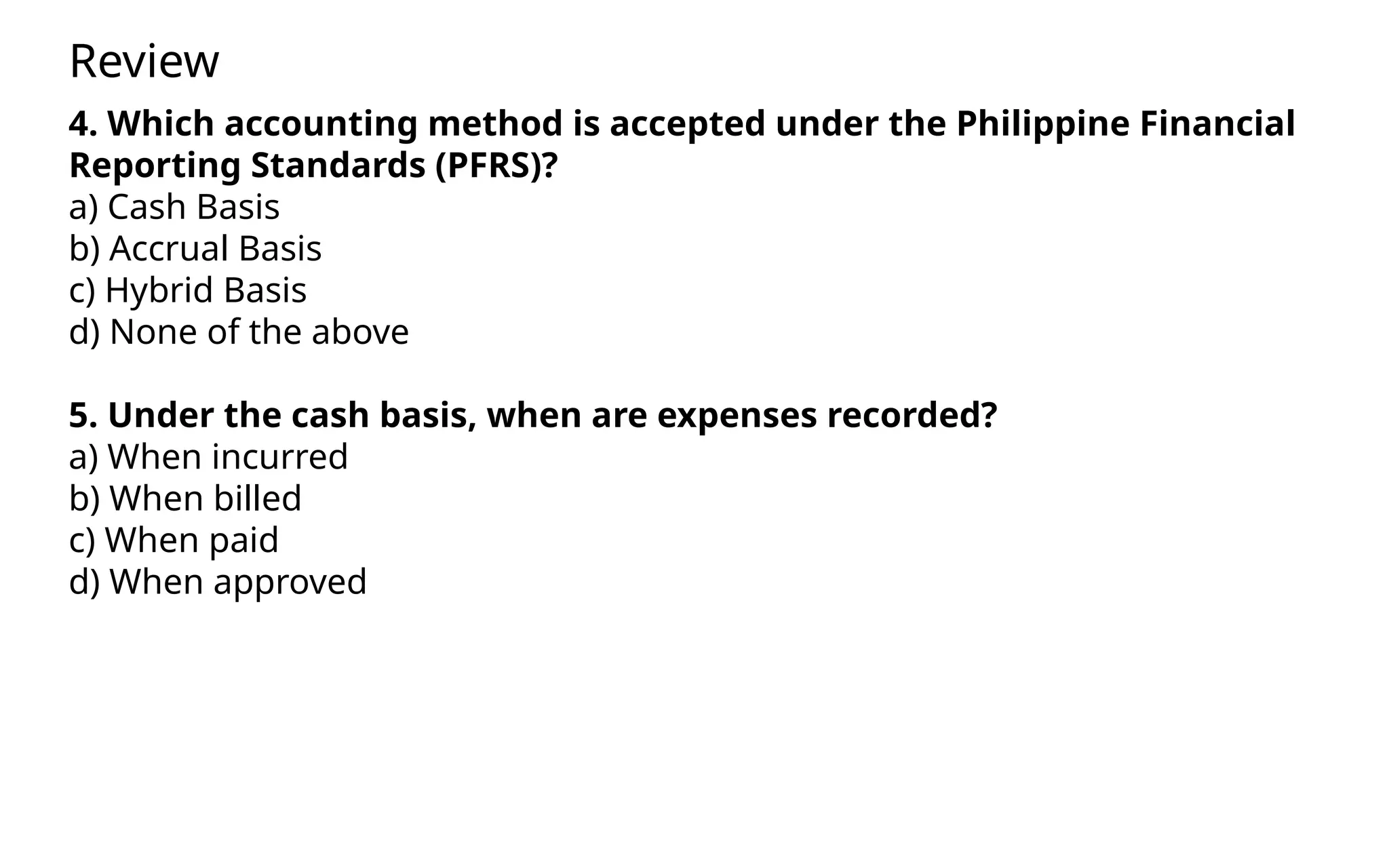

10.

4. Which accountingmethod is accepted under the Philippine Financial

Reporting Standards (PFRS)?

a) Cash Basis

b) Accrual Basis

c) Hybrid Basis

d) None of the above

5. Under the cash basis, when are expenses recorded?

a) When incurred

b) When billed

c) When paid

d) When approved

Review

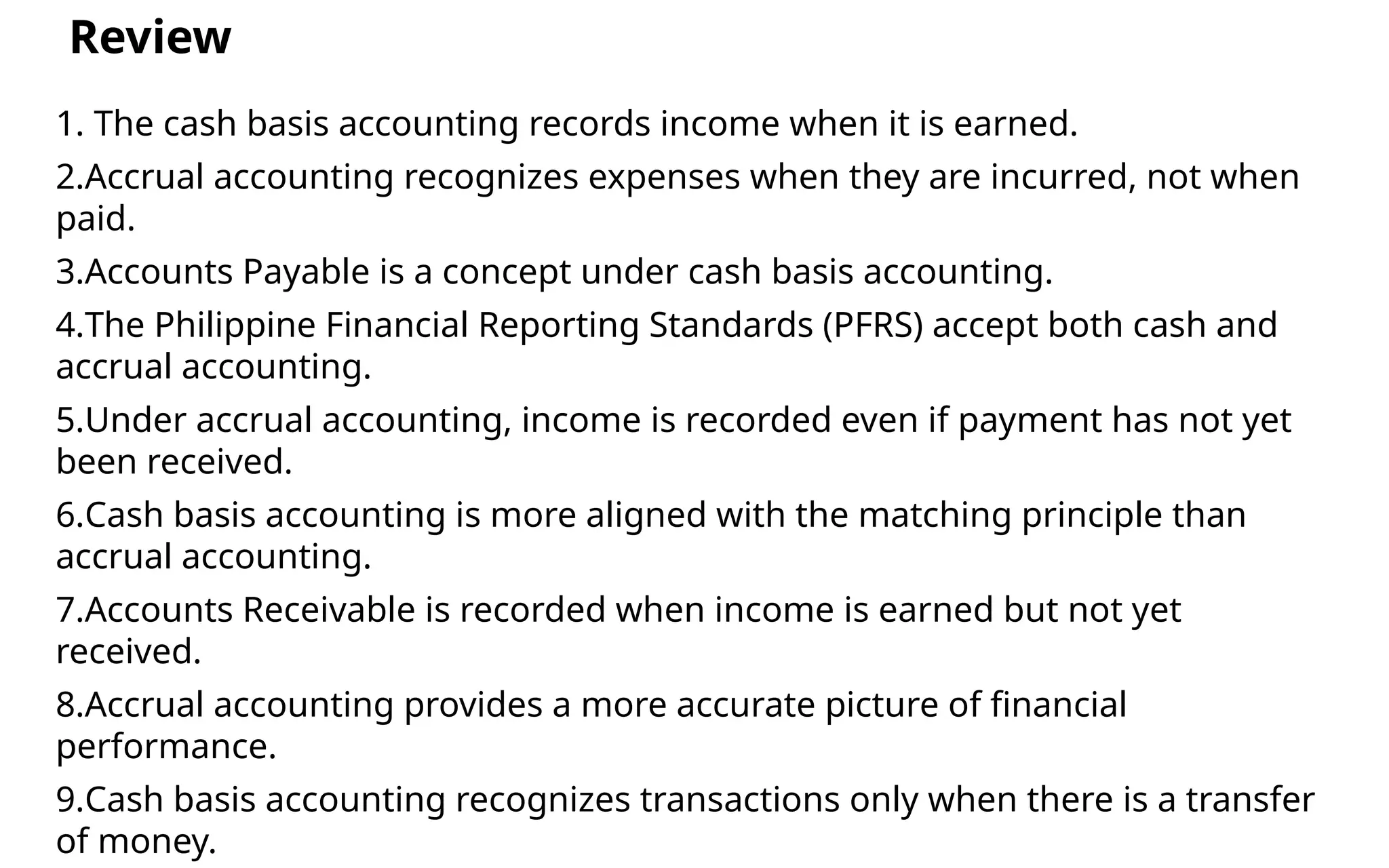

11.

1. The cashbasis accounting records income when it is earned.

2.Accrual accounting recognizes expenses when they are incurred, not when

paid.

3.Accounts Payable is a concept under cash basis accounting.

4.The Philippine Financial Reporting Standards (PFRS) accept both cash and

accrual accounting.

5.Under accrual accounting, income is recorded even if payment has not yet

been received.

6.Cash basis accounting is more aligned with the matching principle than

accrual accounting.

7.Accounts Receivable is recorded when income is earned but not yet

received.

8.Accrual accounting provides a more accurate picture of financial

performance.

9.Cash basis accounting recognizes transactions only when there is a transfer

of money.

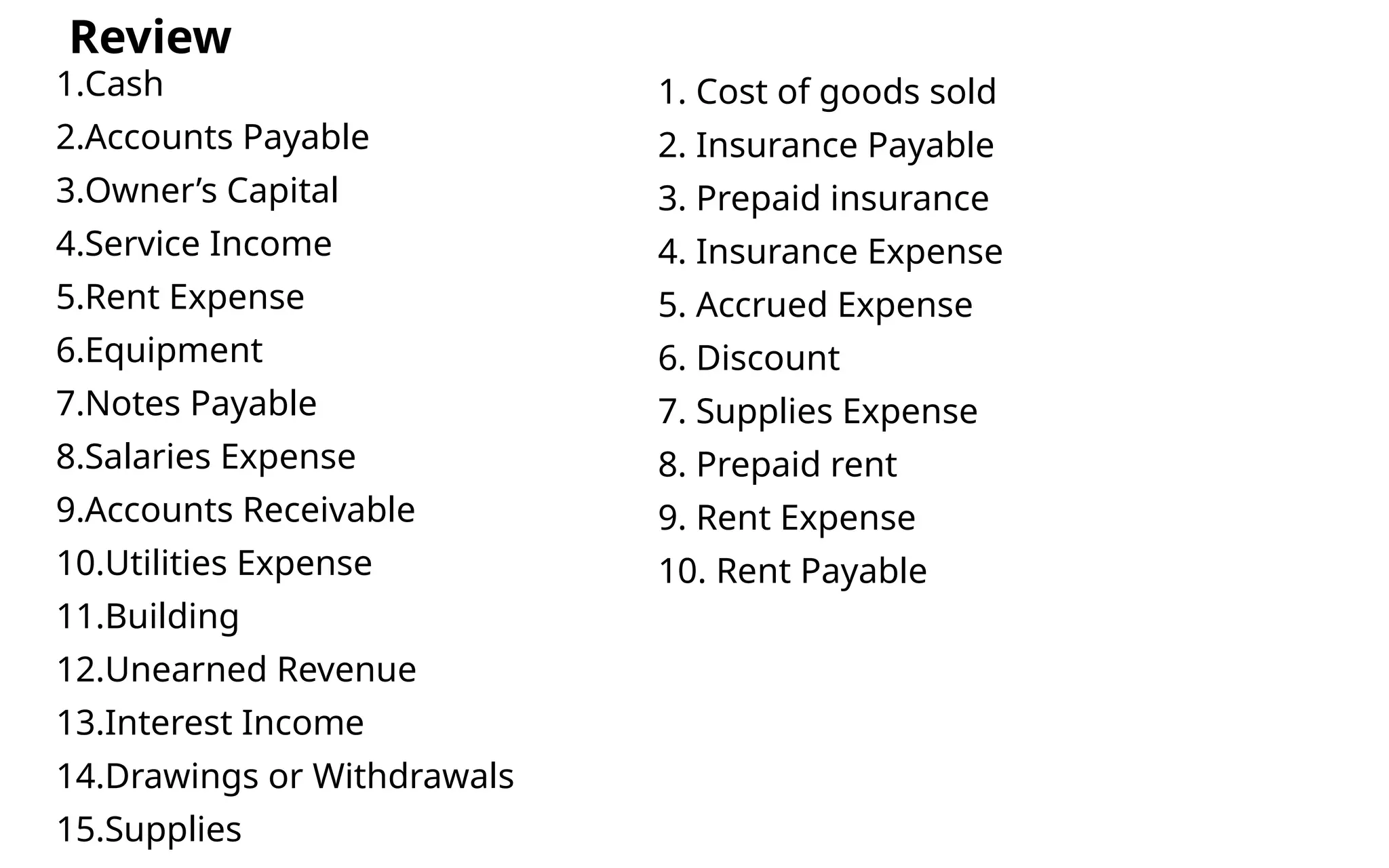

Review

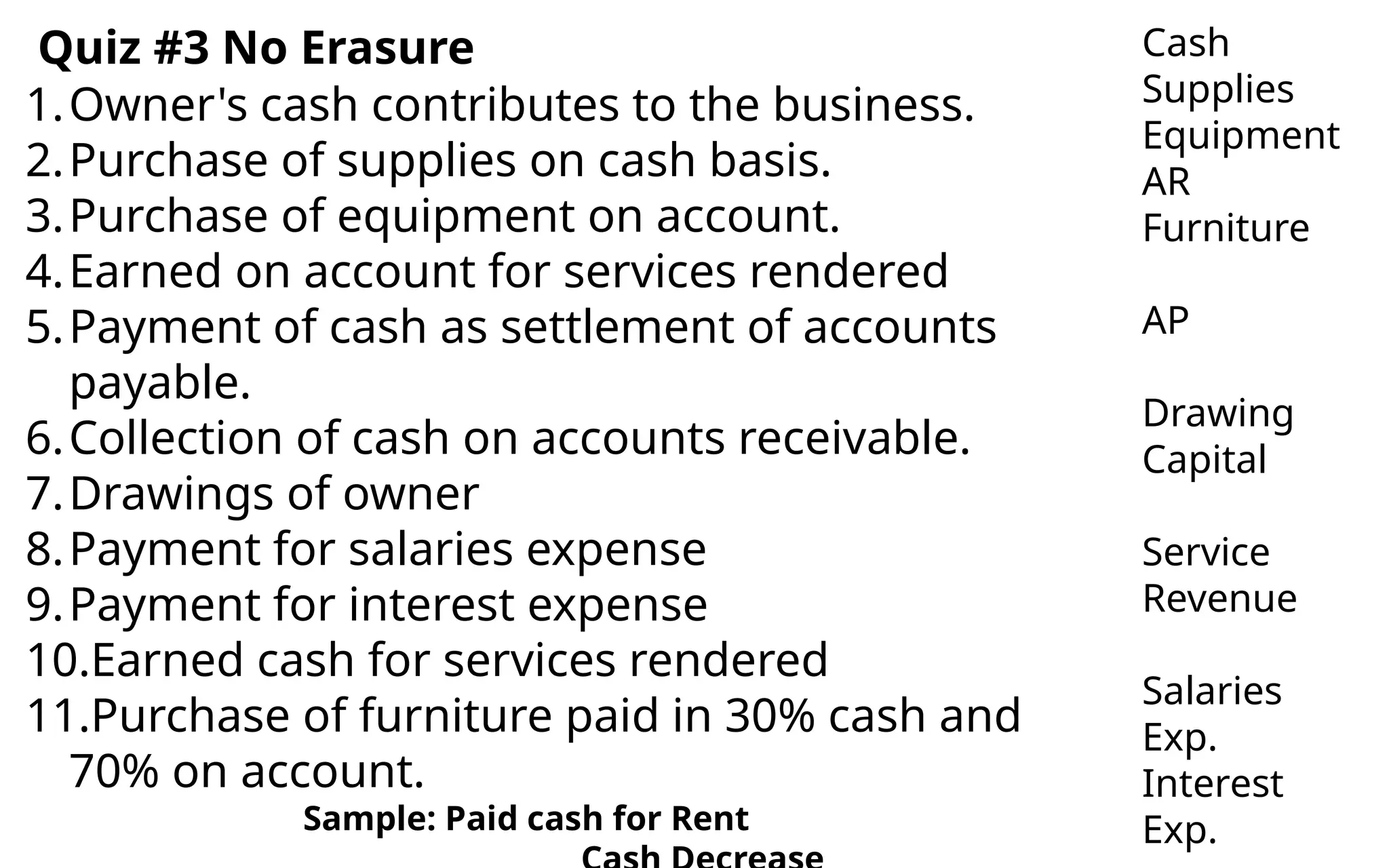

1.Owner's cash contributesto the business.

2.Purchase of supplies on cash basis.

3.Purchase of equipment on account.

4.Earned on account for services rendered

5.Payment of cash as settlement of accounts

payable.

6.Collection of cash on accounts receivable.

7.Drawings of owner

8.Payment for salaries expense

9.Payment for interest expense

10.Earned cash for services rendered

11.Purchase of furniture paid in 30% cash and

70% on account.

Sample: Paid cash for Rent

Cash

Supplies

Equipment

AR

Furniture

AP

Drawing

Capital

Service

Revenue

Salaries

Exp.

Interest

Exp.

Quiz #3 No Erasure

25.

The following aretransactions for the month of

Nov.

1. Owner’s P4,000 cash contributes to the

business.

2. Purchase of P500 worth of supplies on cash

basis.

3. Purchase of equipment on account worth

P4,000.

4. Earned P500 on account for services rendered

5. Payment of P2,000 for settlement of accounts

payable.

6. Collected P100 for accounts receivable.

7. Drawings of owner is worth P3,000

8. Payment for salaries expense worth P1,500

9. Paid P450 for interest expense

Cash

Supplies

Equipment

AR

Furniture

AP

Drawing

Capital

Service Revenue

Salaries Exp.

Interest Exp.

NO

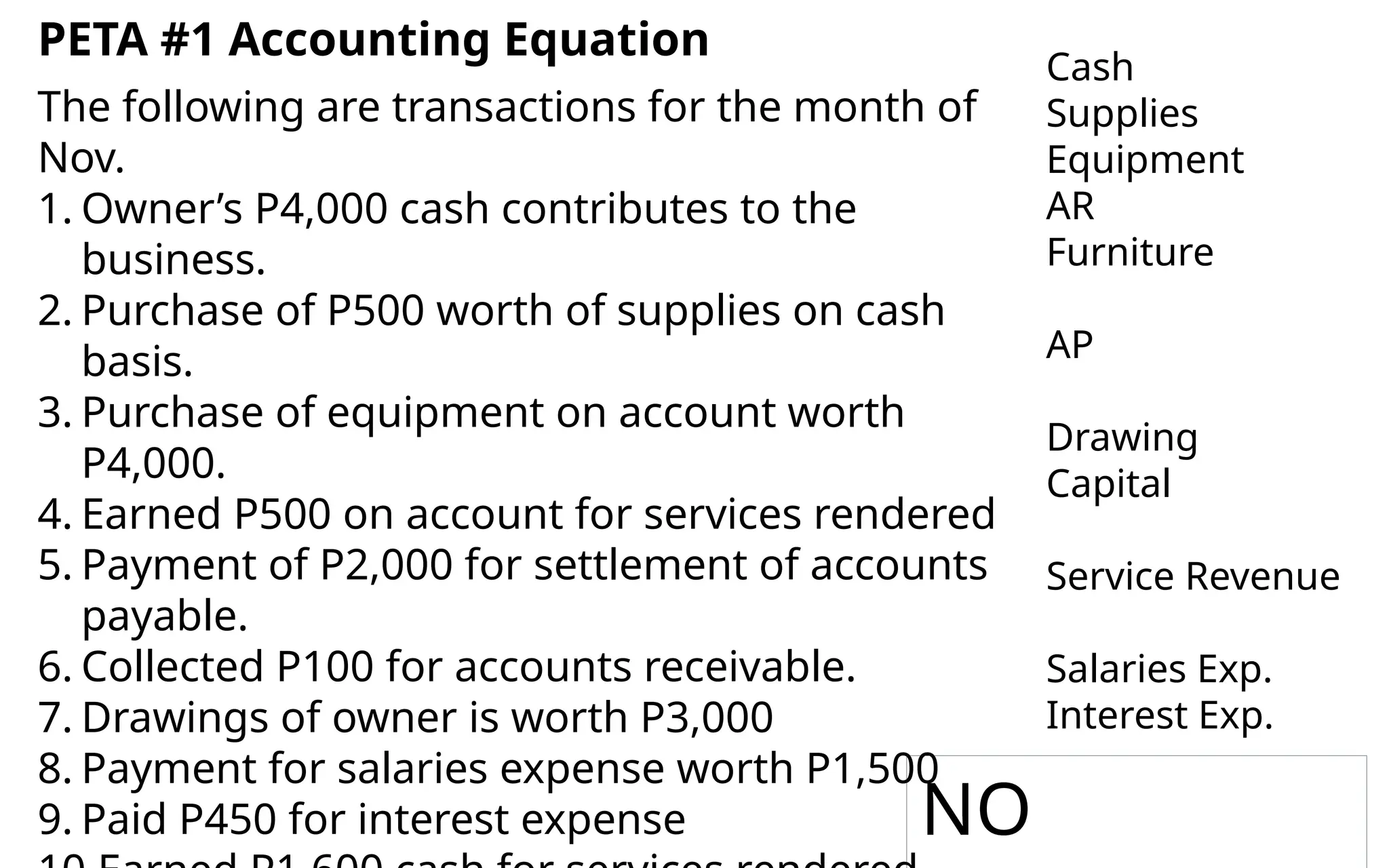

PETA #1 Accounting Equation

26.

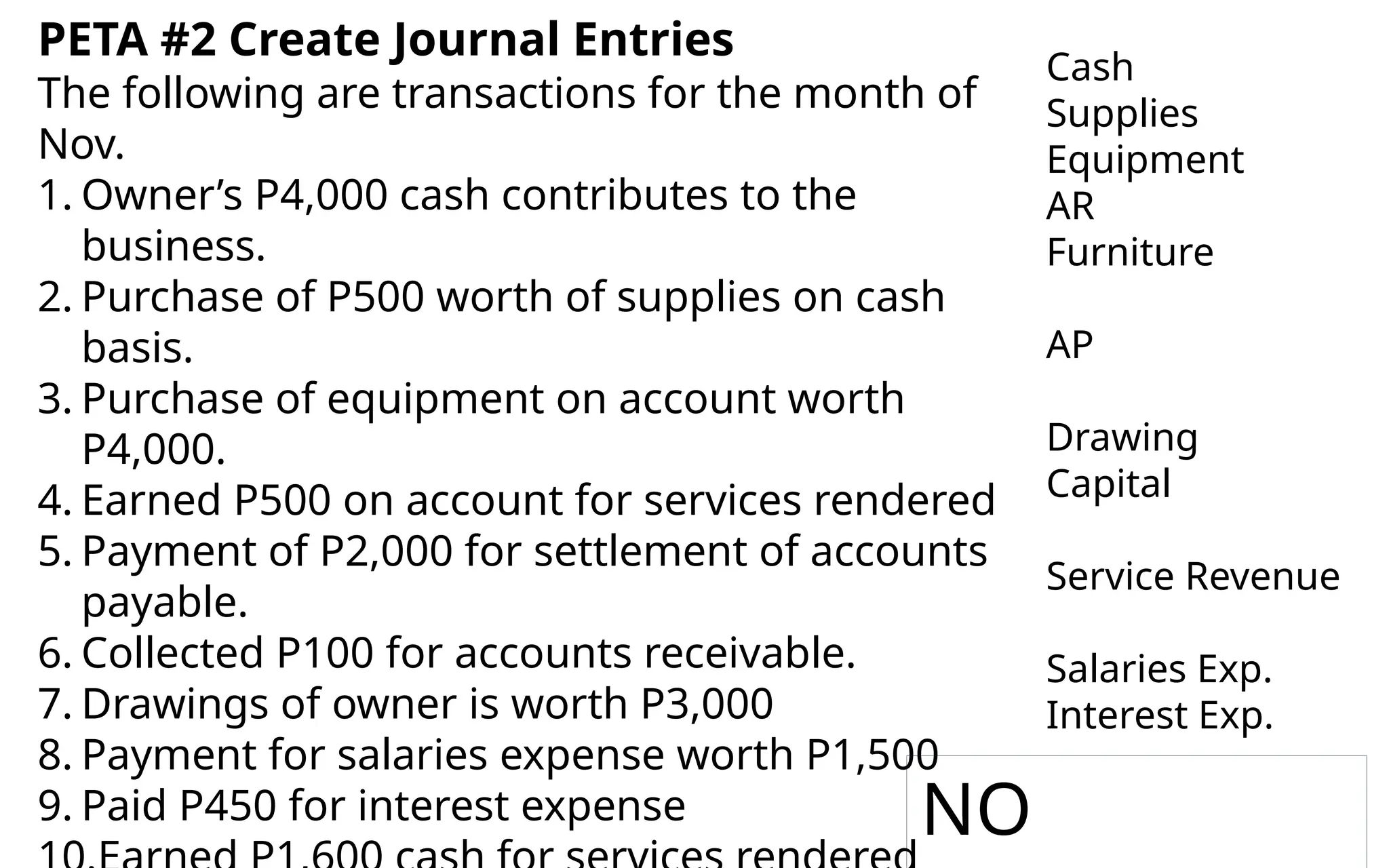

The following aretransactions for the month of

Nov.

1. Owner’s P4,000 cash contributes to the

business.

2. Purchase of P500 worth of supplies on cash

basis.

3. Purchase of equipment on account worth

P4,000.

4. Earned P500 on account for services rendered

5. Payment of P2,000 for settlement of accounts

payable.

6. Collected P100 for accounts receivable.

7. Drawings of owner is worth P3,000

8. Payment for salaries expense worth P1,500

9. Paid P450 for interest expense

Cash

Supplies

Equipment

AR

Furniture

AP

Drawing

Capital

Service Revenue

Salaries Exp.

Interest Exp.

NO

PETA #2 Create Journal Entries

27.

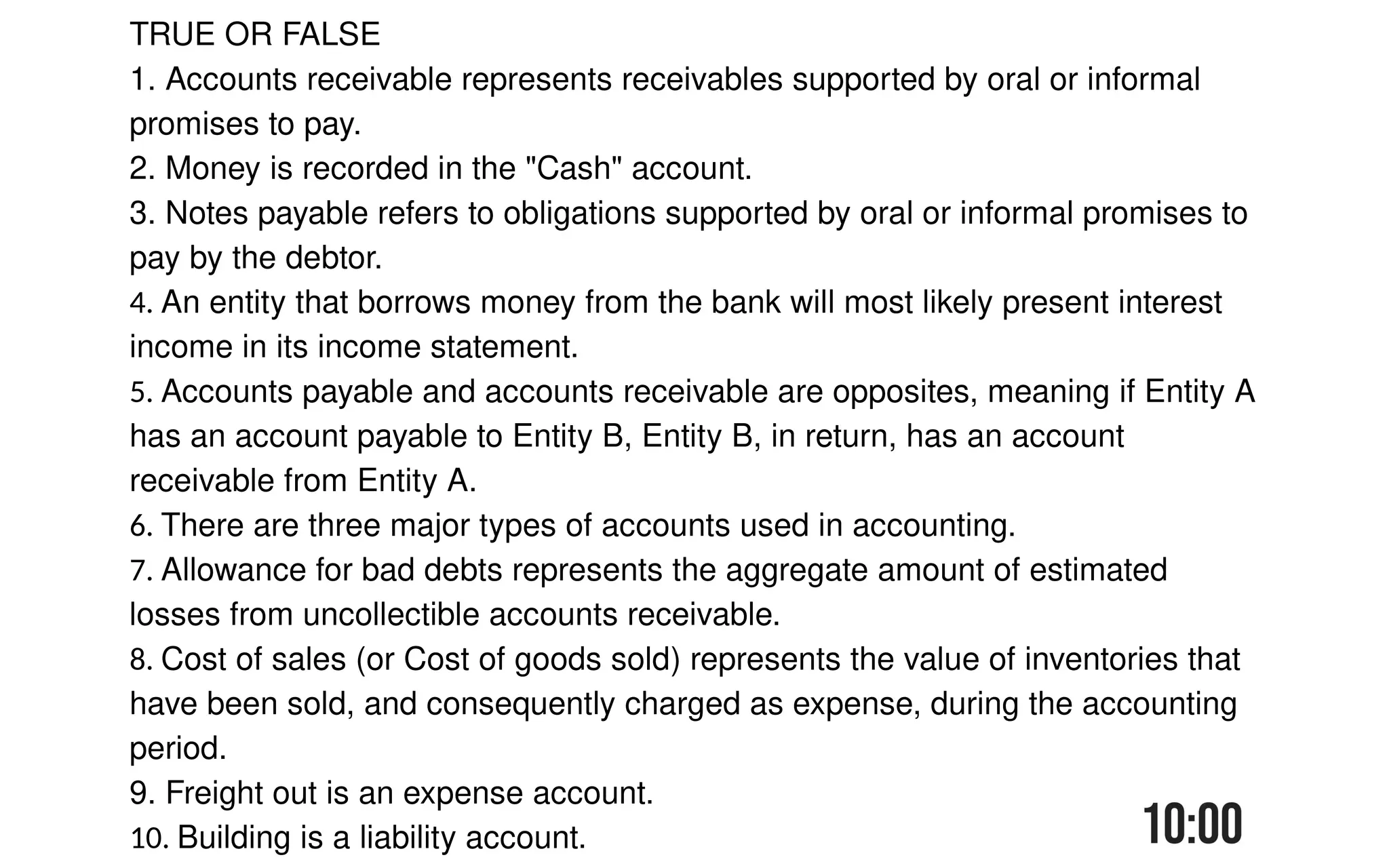

TRUE OR FALSE

1.Accounts receivable represents receivables supported by oral or informal

promises to pay.

2. Money is recorded in the "Cash" account.

3. Notes payable refers to obligations supported by oral or informal promises to

pay by the debtor.

4. An entity that borrows money from the bank will most likely present interest

income in its income statement.

5. Accounts payable and accounts receivable are opposites, meaning if Entity A

has an account payable to Entity B, Entity B, in return, has an account

receivable from Entity A.

6. There are three major types of accounts used in accounting.

7. Allowance for bad debts represents the aggregate amount of estimated

losses from uncollectible accounts receivable.

8. Cost of sales (or Cost of goods sold) represents the value of inventories that

have been sold, and consequently charged as expense, during the accounting

period.

9. Freight out is an expense account.

10. Building is a liability account.

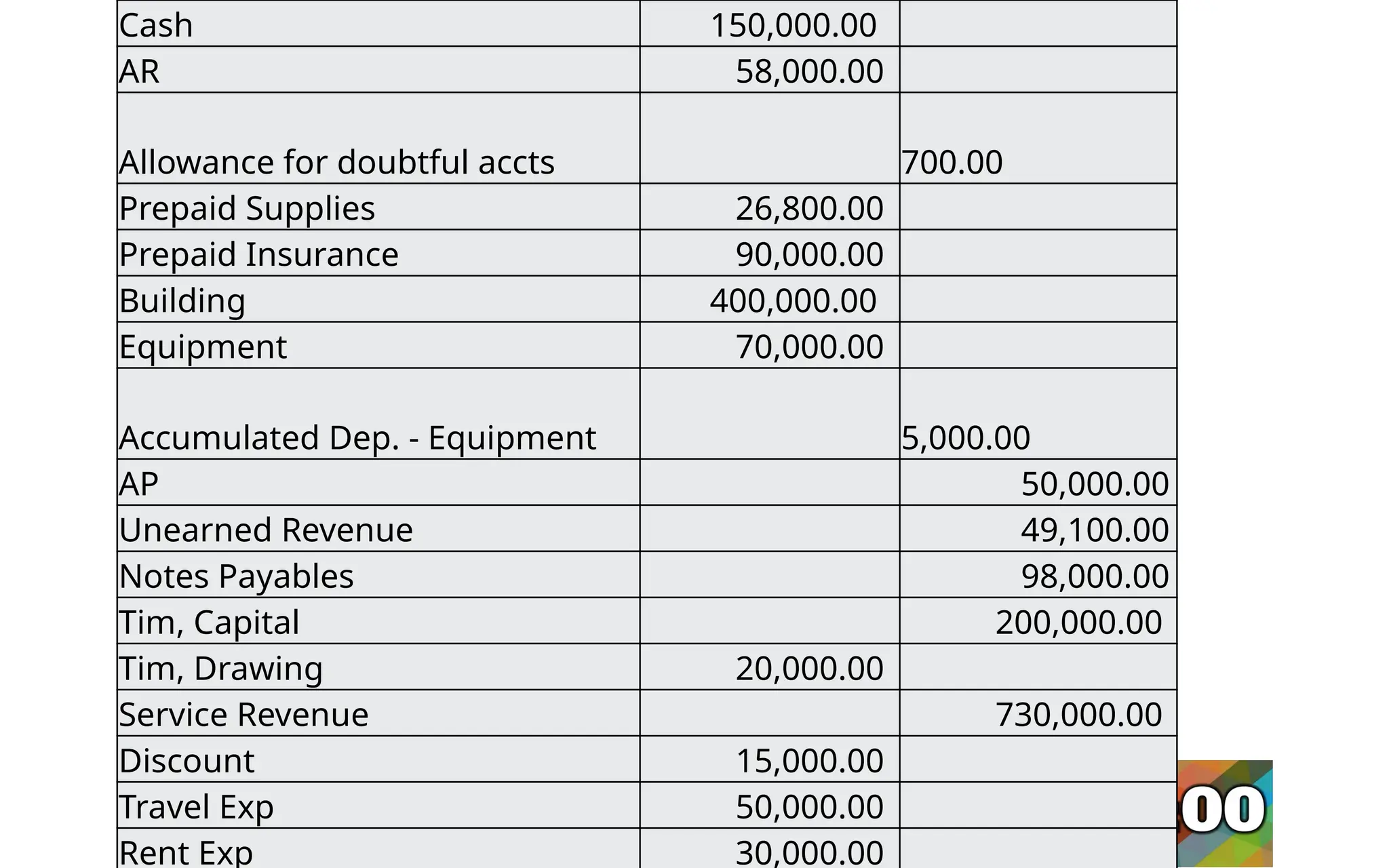

28.

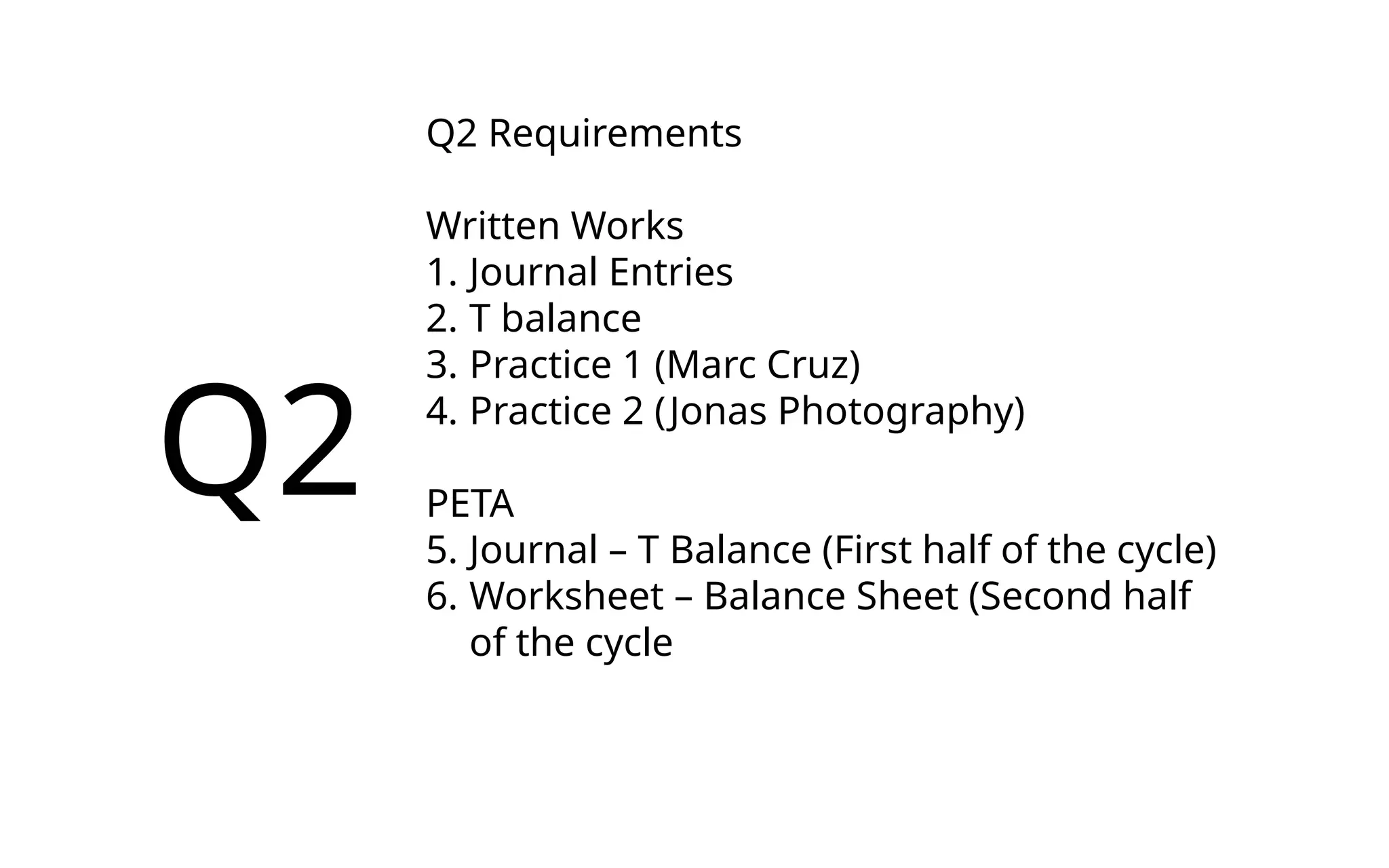

Q2

Q2 Requirements

Written Works

1.Journal Entries

2. T balance

3. Practice 1 (Marc Cruz)

4. Practice 2 (Jonas Photography)

PETA

5. Journal – T Balance (First half of the cycle)

6. Worksheet – Balance Sheet (Second half

of the cycle

29.

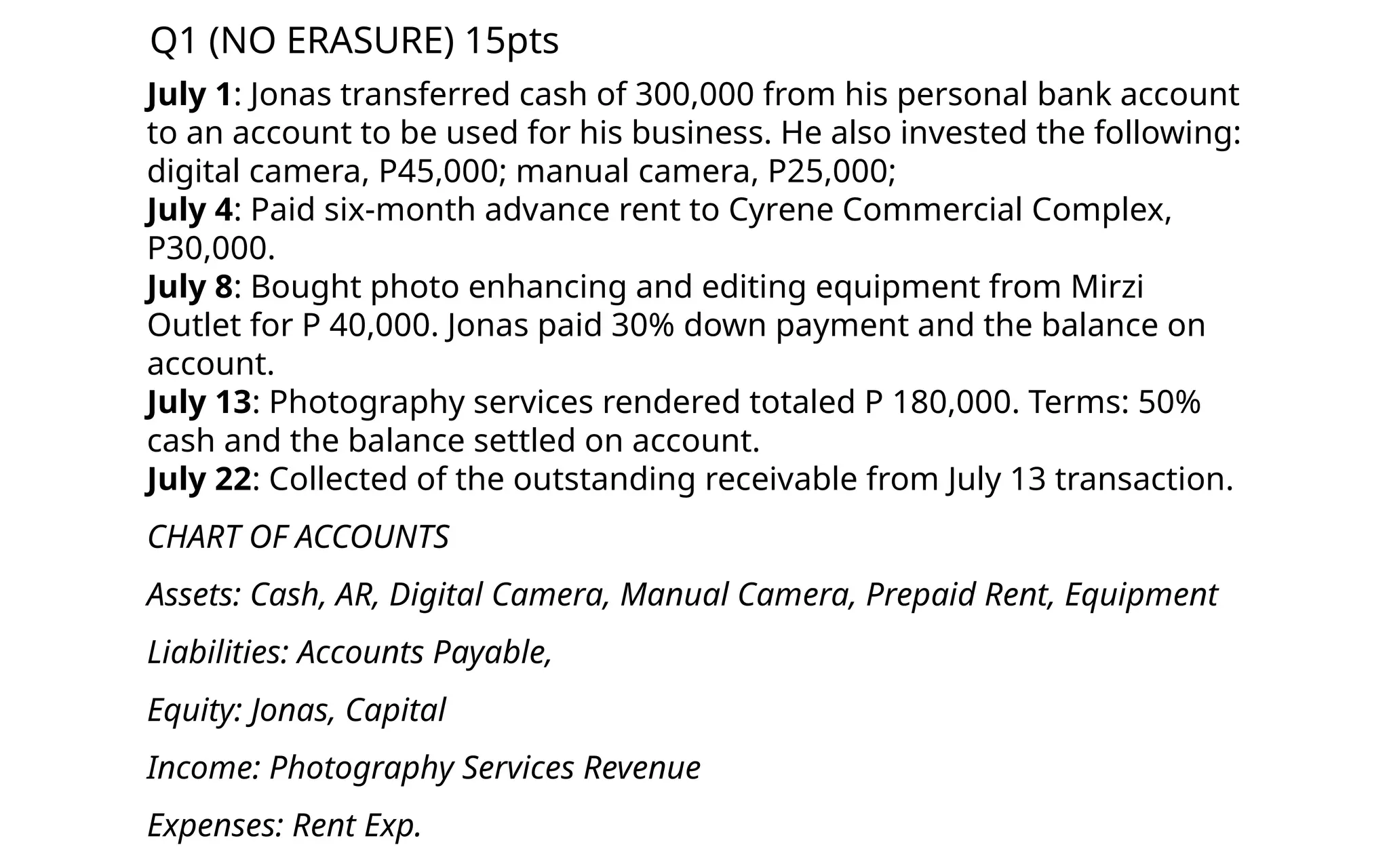

Q1 (NO ERASURE)15pts

July 1: Jonas transferred cash of 300,000 from his personal bank account

to an account to be used for his business. He also invested the following:

digital camera, P45,000; manual camera, P25,000;

July 4: Paid six-month advance rent to Cyrene Commercial Complex,

P30,000.

July 8: Bought photo enhancing and editing equipment from Mirzi

Outlet for P 40,000. Jonas paid 30% down payment and the balance on

account.

July 13: Photography services rendered totaled P 180,000. Terms: 50%

cash and the balance settled on account.

July 22: Collected of the outstanding receivable from July 13 transaction.

CHART OF ACCOUNTS

Assets: Cash, AR, Digital Camera, Manual Camera, Prepaid Rent, Equipment

Liabilities: Accounts Payable,

Equity: Jonas, Capital

Income: Photography Services Revenue

Expenses: Rent Exp.

31.

Q2 T Balance

PRACTICE#2

Using your Journal entries in Practice #2

Create T accounts

Create T Balance

Submit the following

1. Journal

2. T accounts

3. T balance

32.

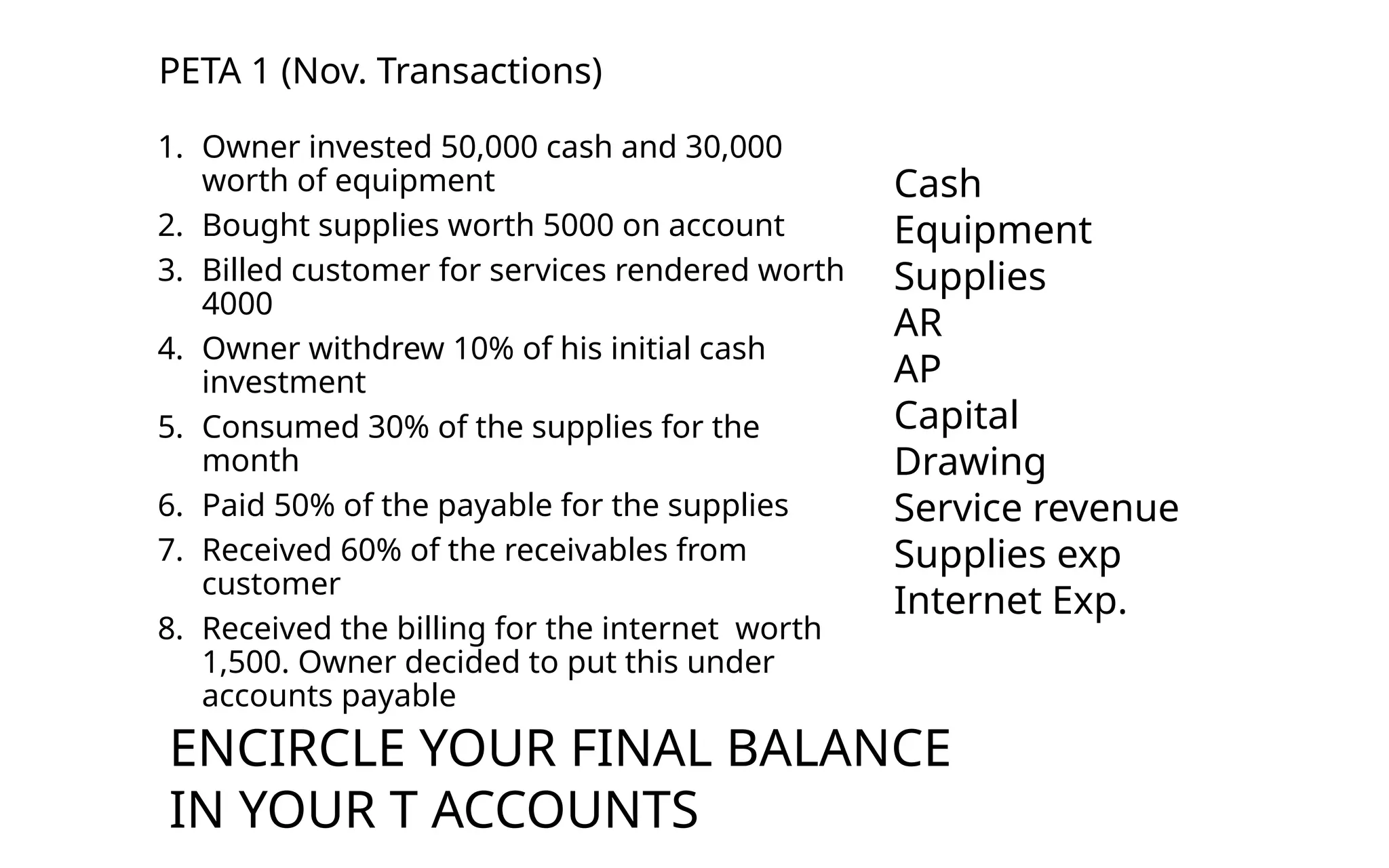

PETA 1 (Nov.Transactions)

1. Owner invested 50,000 cash and 30,000

worth of equipment

2. Bought supplies worth 5000 on account

3. Billed customer for services rendered worth

4000

4. Owner withdrew 10% of his initial cash

investment

5. Consumed 30% of the supplies for the

month

6. Paid 50% of the payable for the supplies

7. Received 60% of the receivables from

customer

8. Received the billing for the internet worth

1,500. Owner decided to put this under

accounts payable

Cash

Equipment

Supplies

AR

AP

Capital

Drawing

Service revenue

Supplies exp

Internet Exp.

ENCIRCLE YOUR FINAL BALANCE

IN YOUR T ACCOUNTS

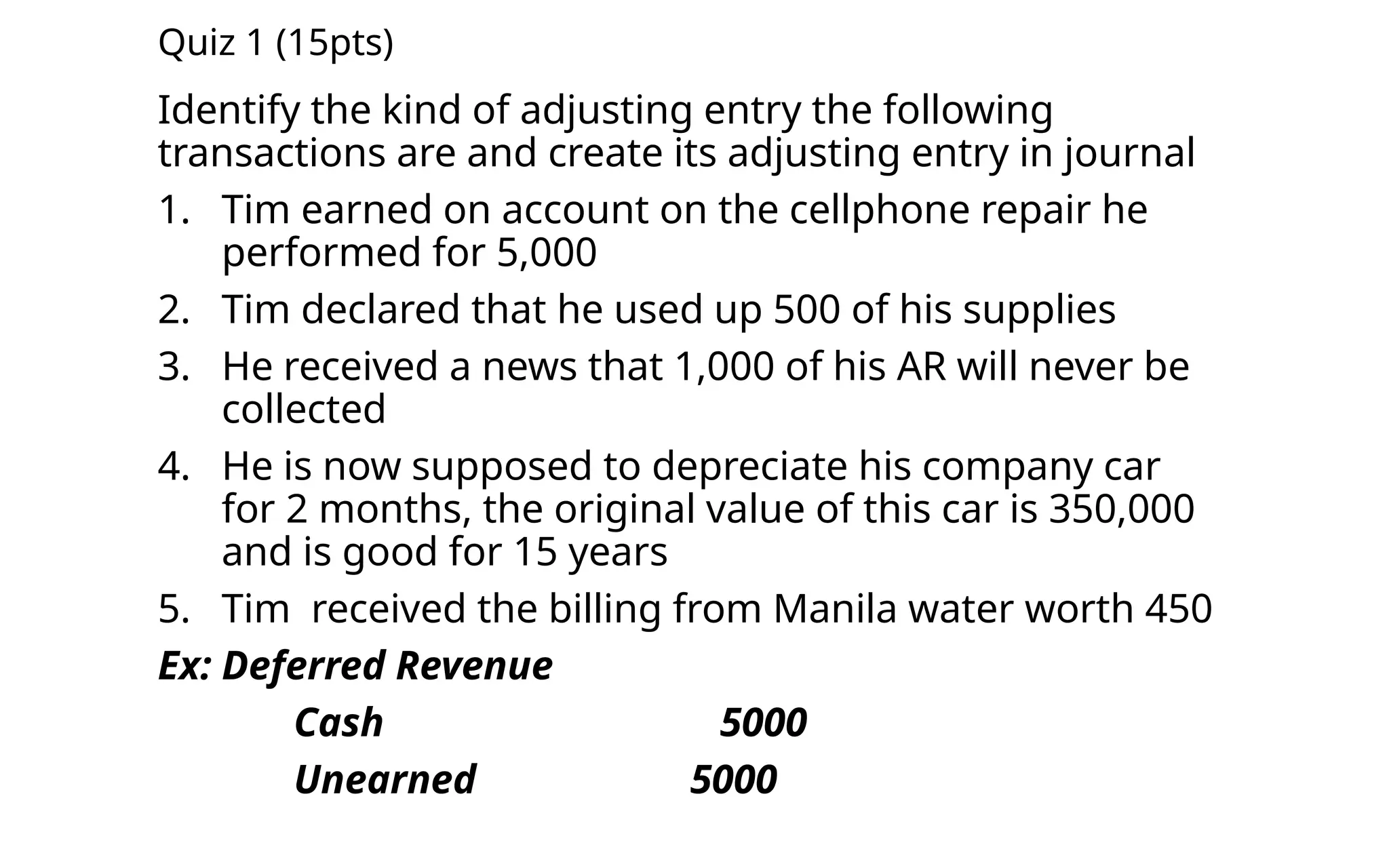

Quiz 1 (15pts)

Identifythe kind of adjusting entry the following

transactions are and create its adjusting entry in journal

1. Tim earned on account on the cellphone repair he

performed for 5,000

2. Tim declared that he used up 500 of his supplies

3. He received a news that 1,000 of his AR will never be

collected

4. He is now supposed to depreciate his company car

for 2 months, the original value of this car is 350,000

and is good for 15 years

5. Tim received the billing from Manila water worth 450

Ex: Deferred Revenue

Cash 5000

Unearned 5000

37.

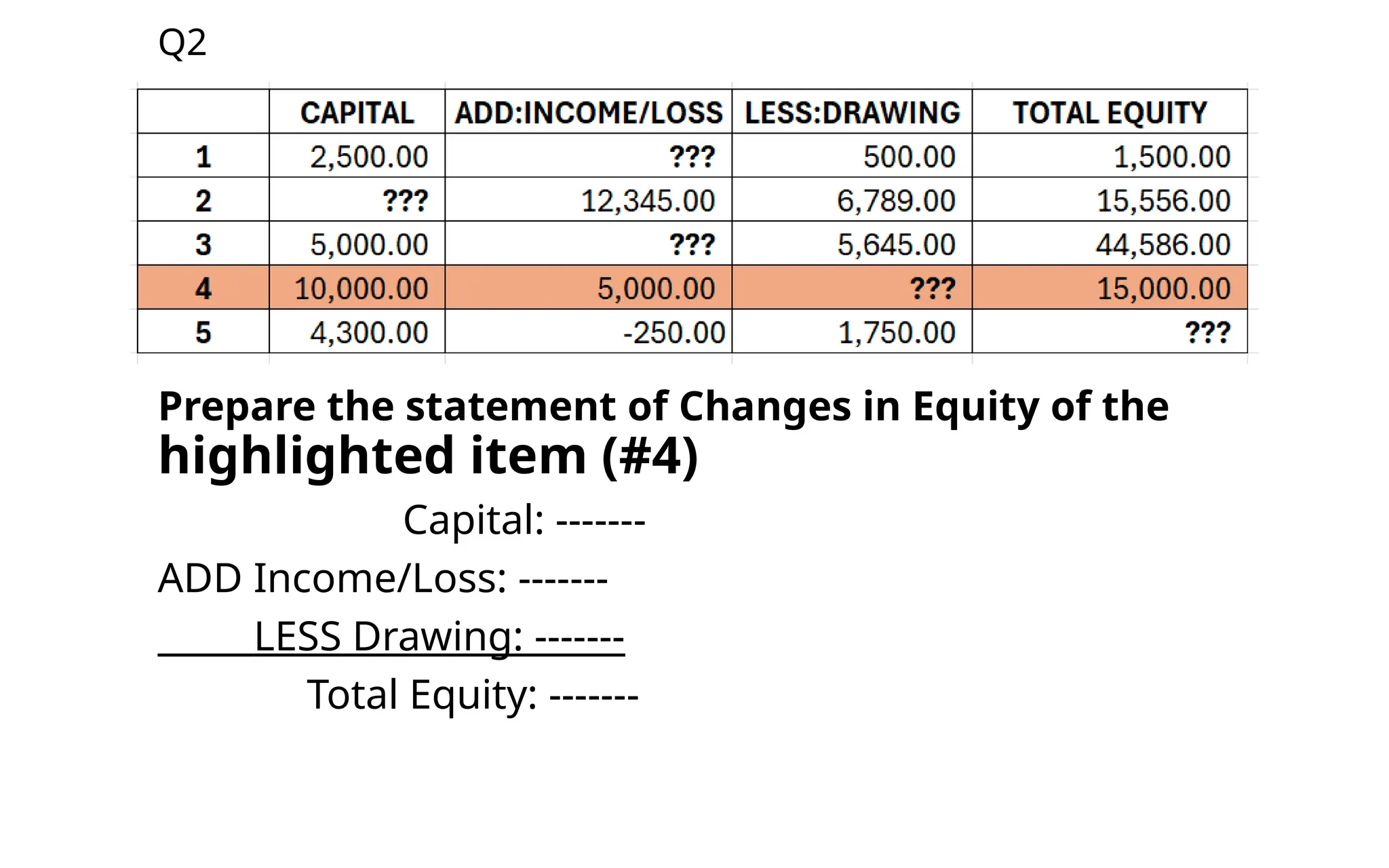

Q2

Prepare the statementof Changes in Equity of the

highlighted item (#4)

Capital: -------

ADD Income/Loss: -------

LESS Drawing: -------

Total Equity: -------

38.

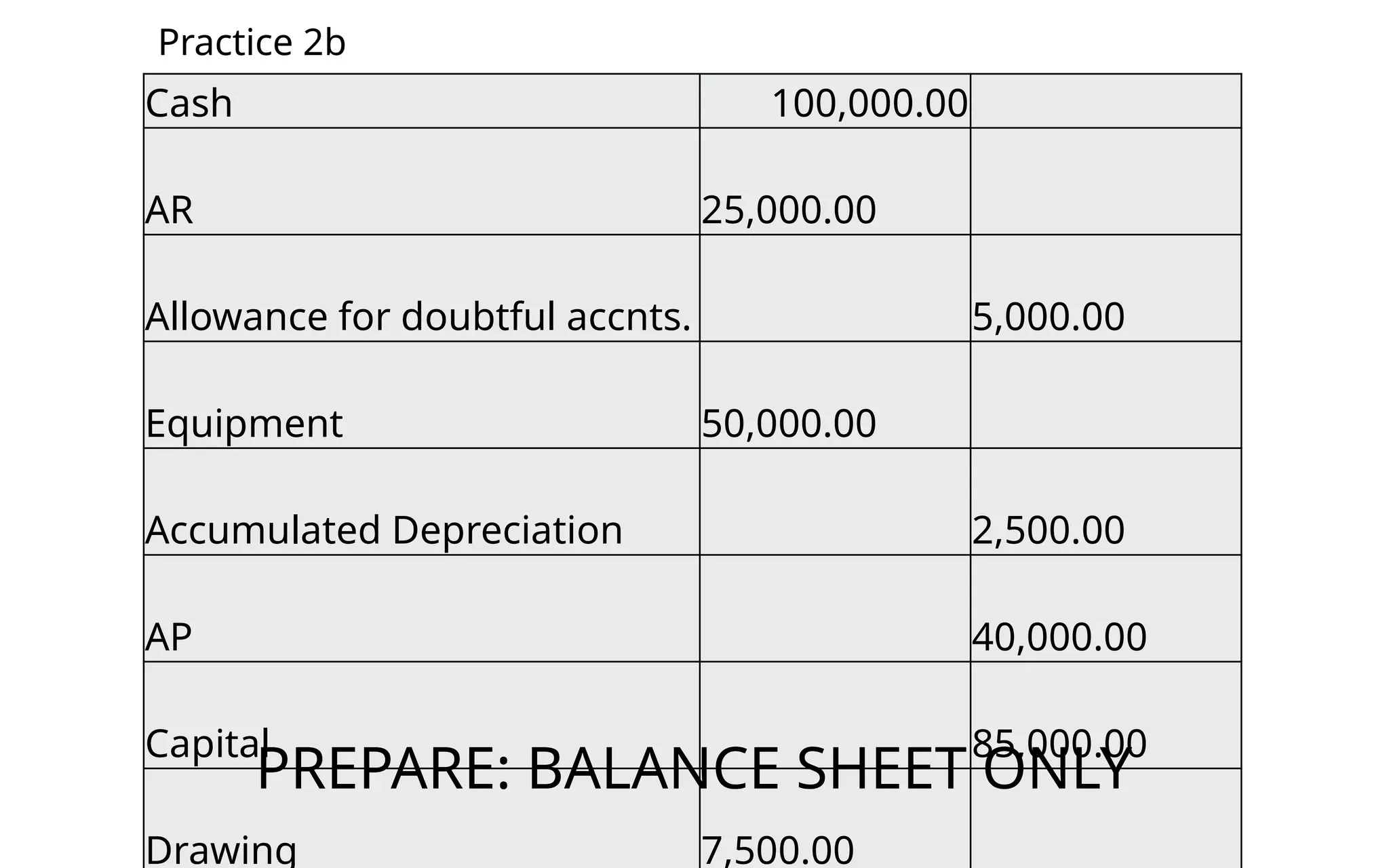

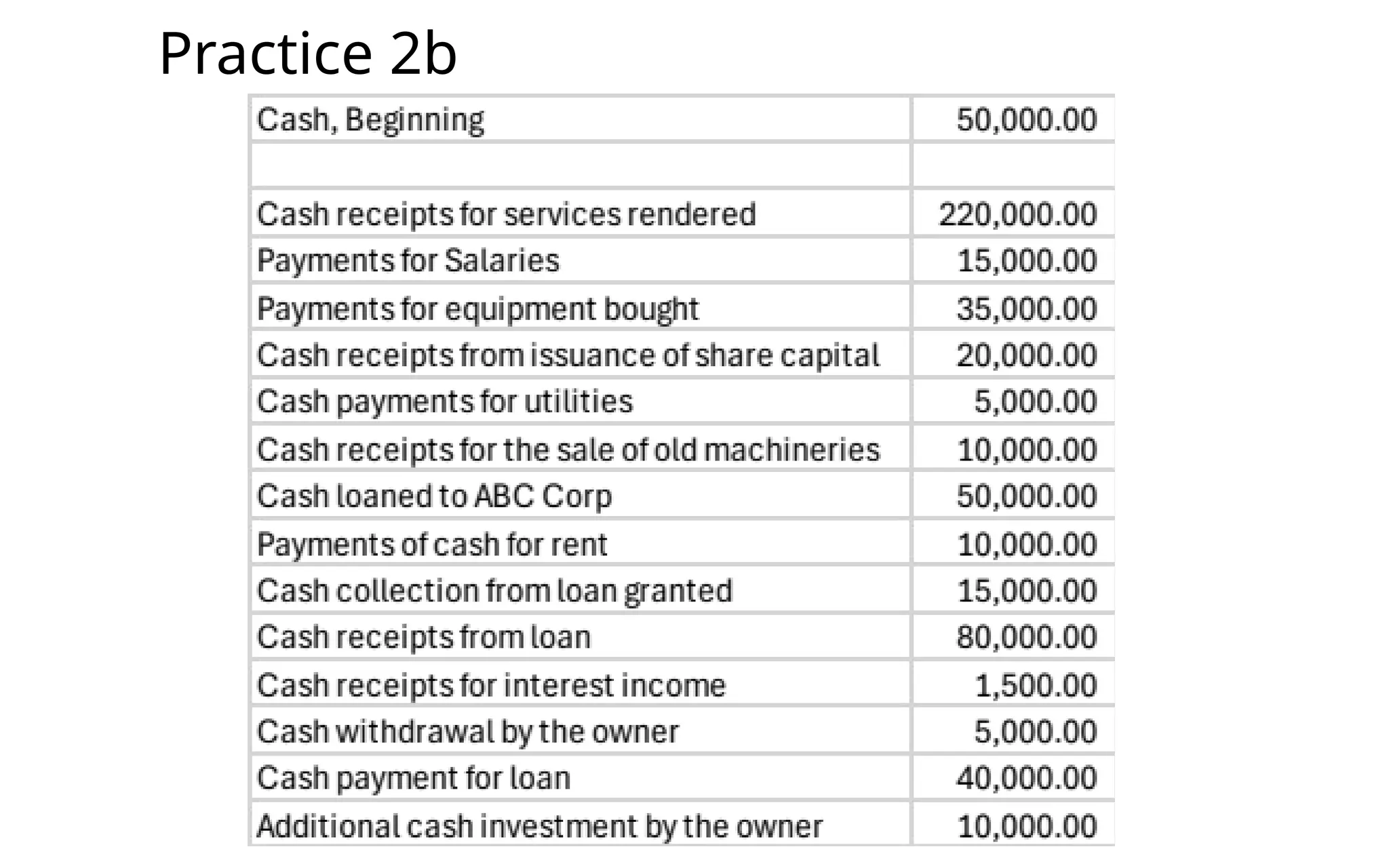

Practice 2b

Cash 100,000.00

AR25,000.00

Allowance for doubtful accnts. 5,000.00

Equipment 50,000.00

Accumulated Depreciation 2,500.00

AP 40,000.00

Capital 85,000.00

Drawing 7,500.00

PREPARE: BALANCE SHEET ONLY

39.

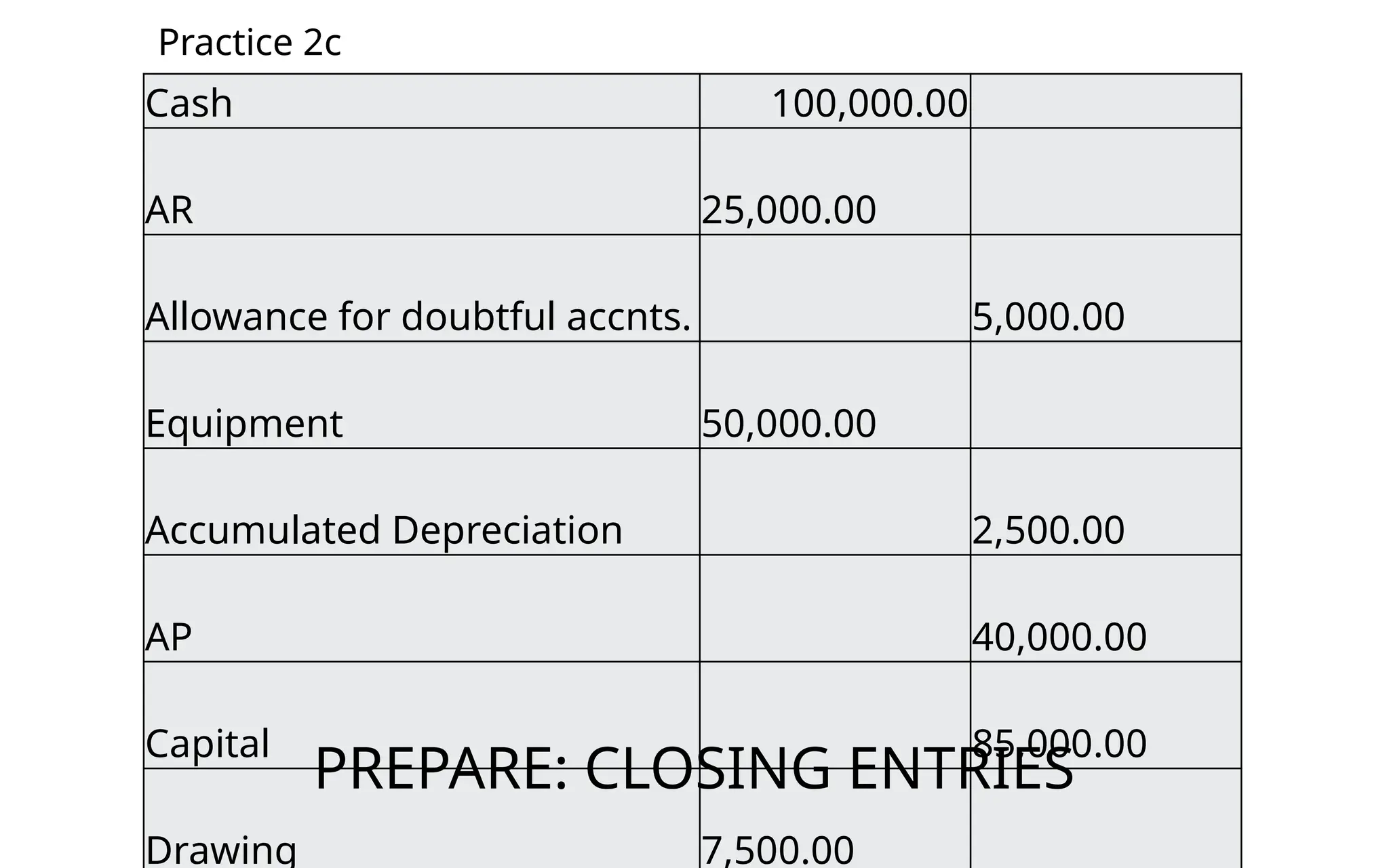

Practice 2c

Cash 100,000.00

AR25,000.00

Allowance for doubtful accnts. 5,000.00

Equipment 50,000.00

Accumulated Depreciation 2,500.00

AP 40,000.00

Capital 85,000.00

Drawing 7,500.00

PREPARE: CLOSING ENTRIES

40.

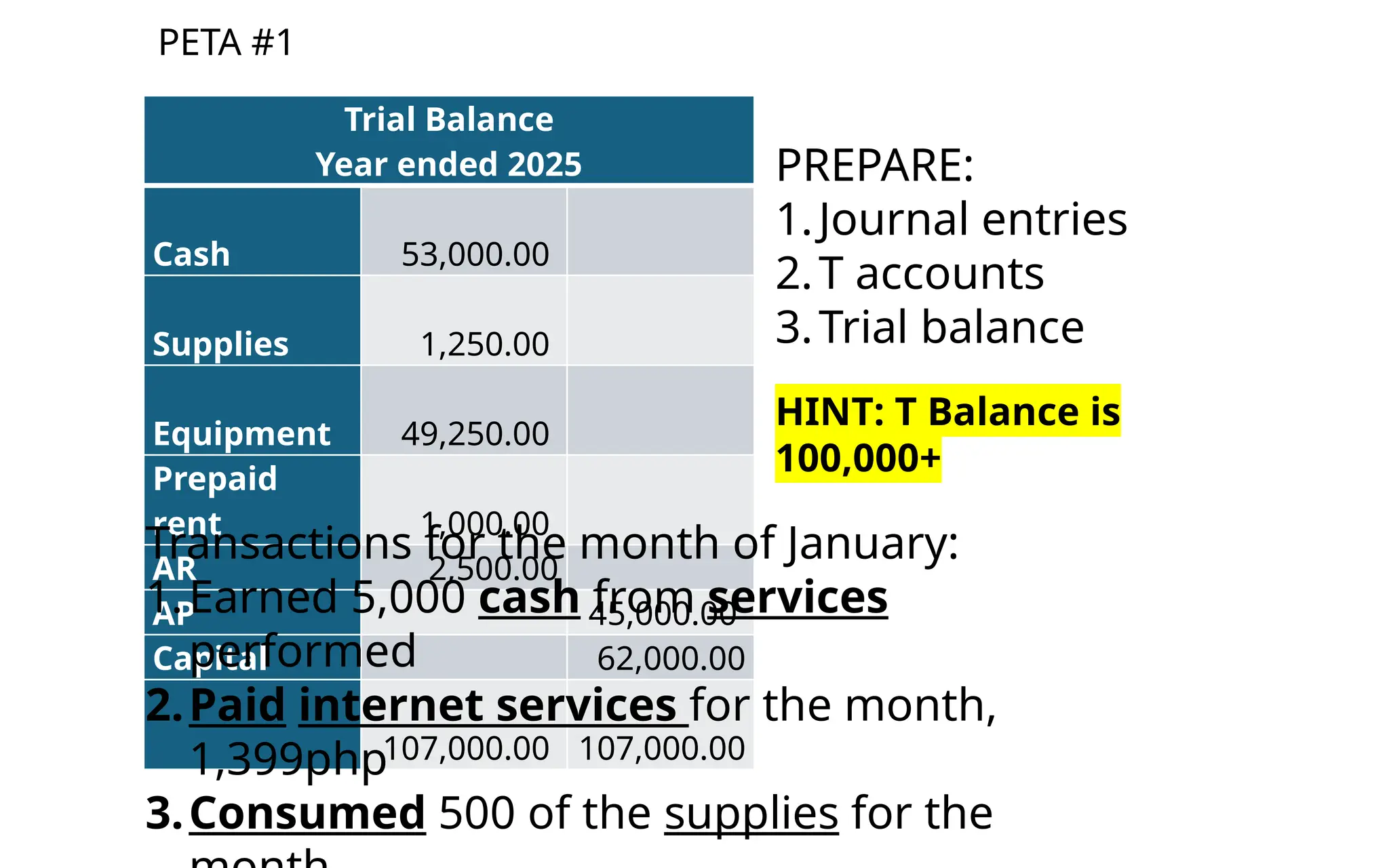

PETA #1

Trial Balance

Yearended 2025

Cash 53,000.00

Supplies 1,250.00

Equipment 49,250.00

Prepaid

rent 1,000.00

AR 2,500.00

AP 45,000.00

Capital 62,000.00

107,000.00 107,000.00

PREPARE:

1.Journal entries

2.T accounts

3.Trial balance

HINT: T Balance is

100,000+

Transactions for the month of January:

1.Earned 5,000 cash from services

performed

2.Paid internet services for the month,

1,399php

3.Consumed 500 of the supplies for the

41.

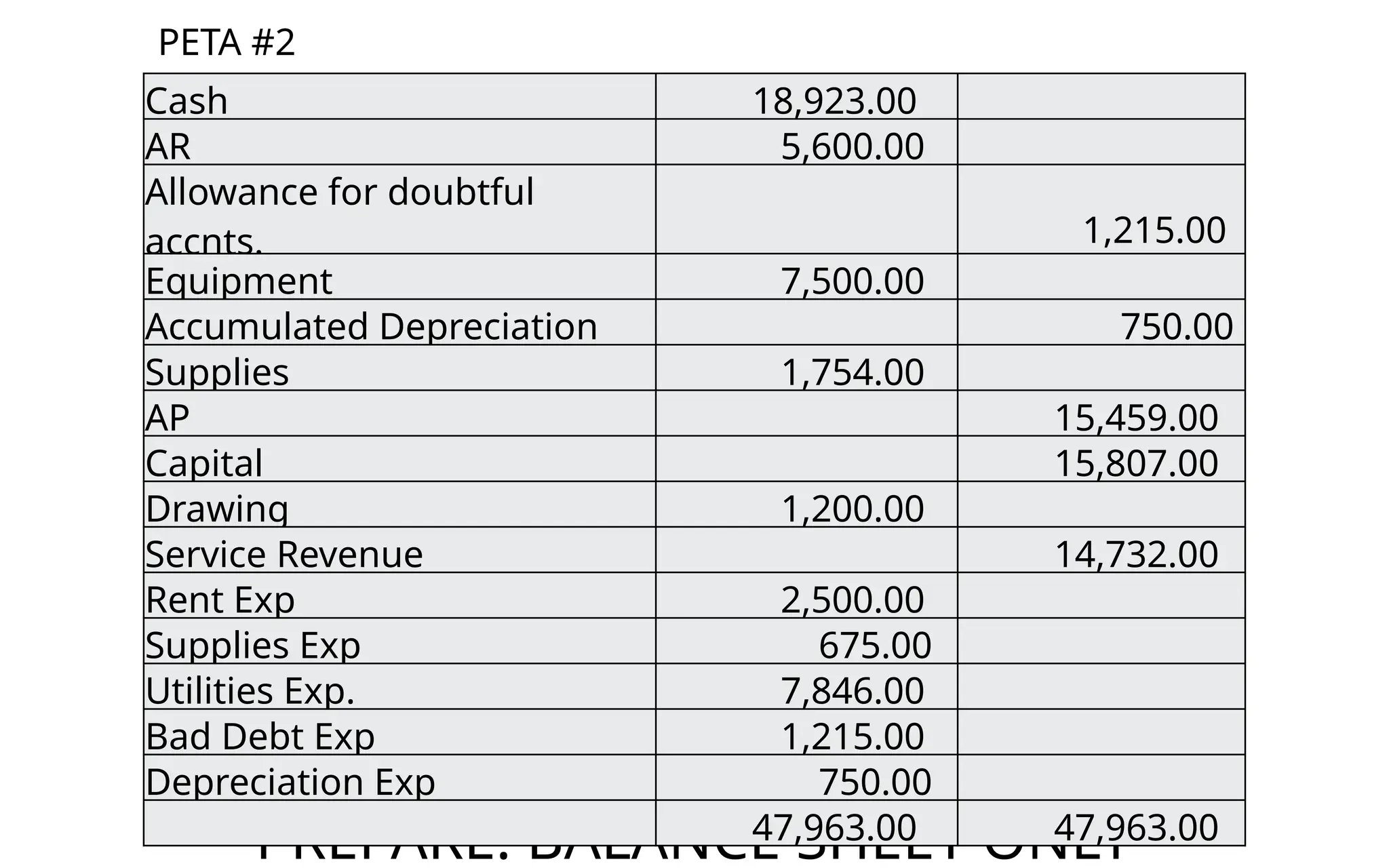

PETA #2

PREPARE: BALANCESHEET ONLY

Cash 18,923.00

AR 5,600.00

Allowance for doubtful

accnts. 1,215.00

Equipment 7,500.00

Accumulated Depreciation 750.00

Supplies 1,754.00

AP 15,459.00

Capital 15,807.00

Drawing 1,200.00

Service Revenue 14,732.00

Rent Exp 2,500.00

Supplies Exp 675.00

Utilities Exp. 7,846.00

Bad Debt Exp 1,215.00

Depreciation Exp 750.00

47,963.00 47,963.00

42.

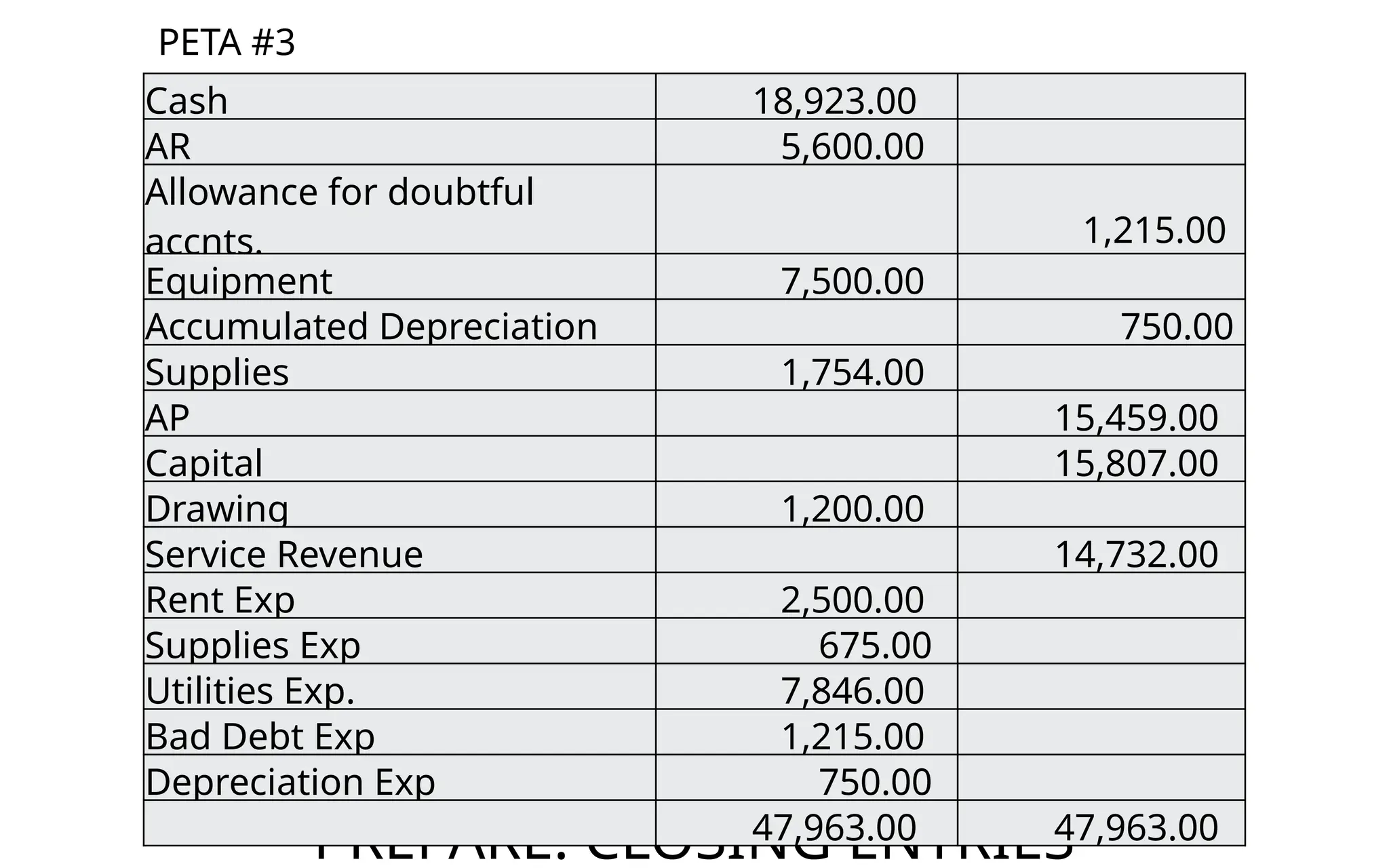

PETA #3

PREPARE: CLOSINGENTRIES

Cash 18,923.00

AR 5,600.00

Allowance for doubtful

accnts. 1,215.00

Equipment 7,500.00

Accumulated Depreciation 750.00

Supplies 1,754.00

AP 15,459.00

Capital 15,807.00

Drawing 1,200.00

Service Revenue 14,732.00

Rent Exp 2,500.00

Supplies Exp 675.00

Utilities Exp. 7,846.00

Bad Debt Exp 1,215.00

Depreciation Exp 750.00

47,963.00 47,963.00

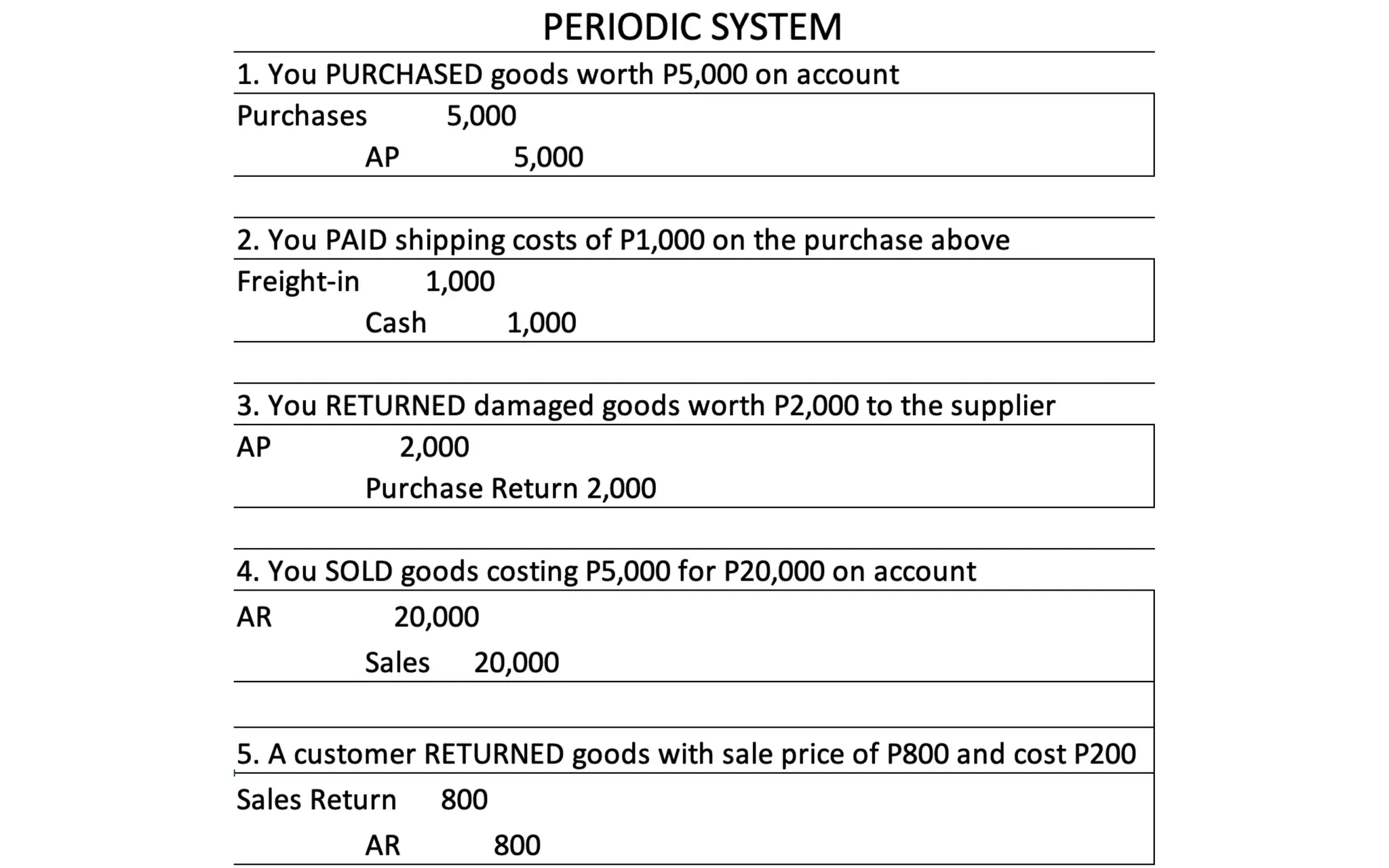

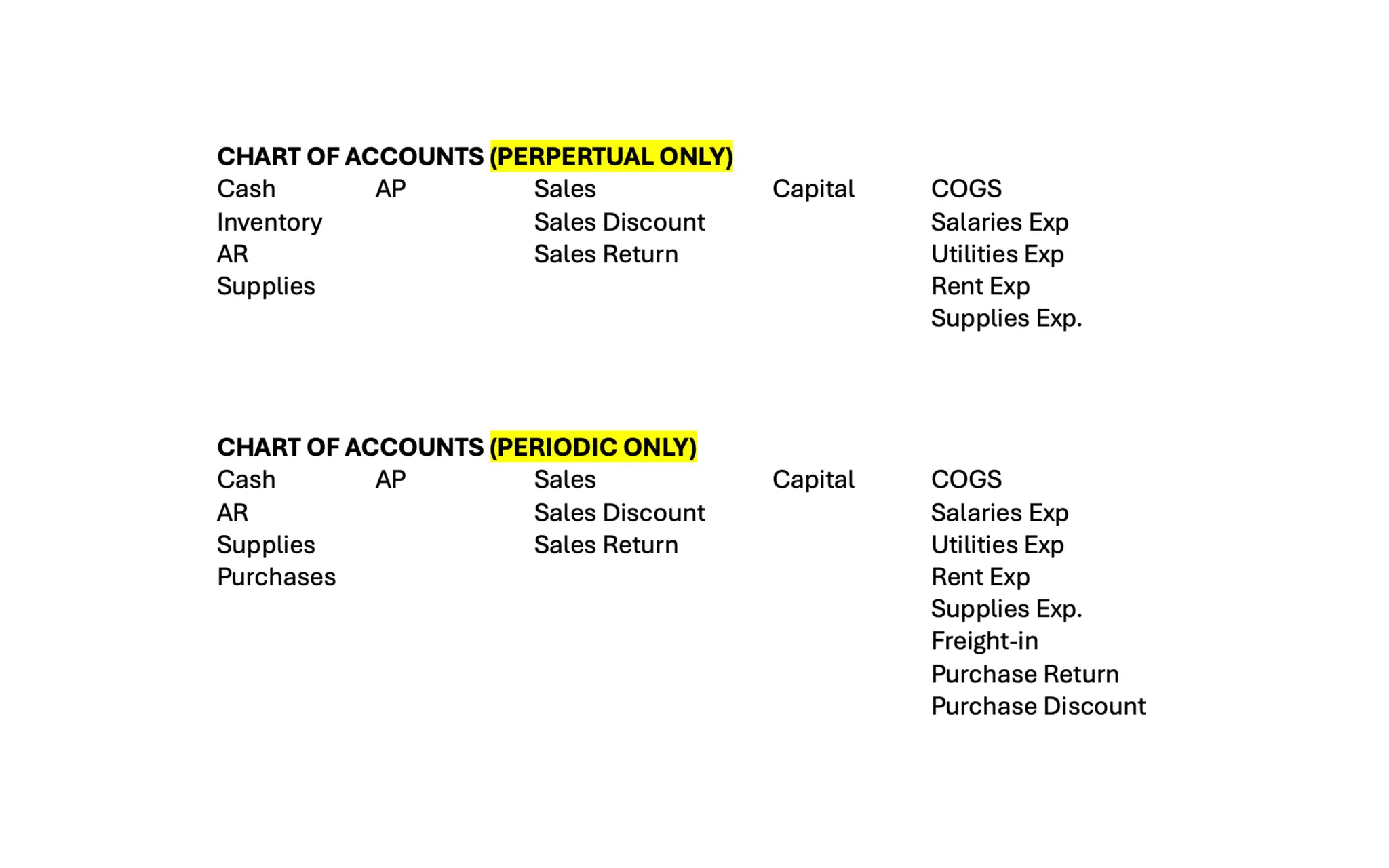

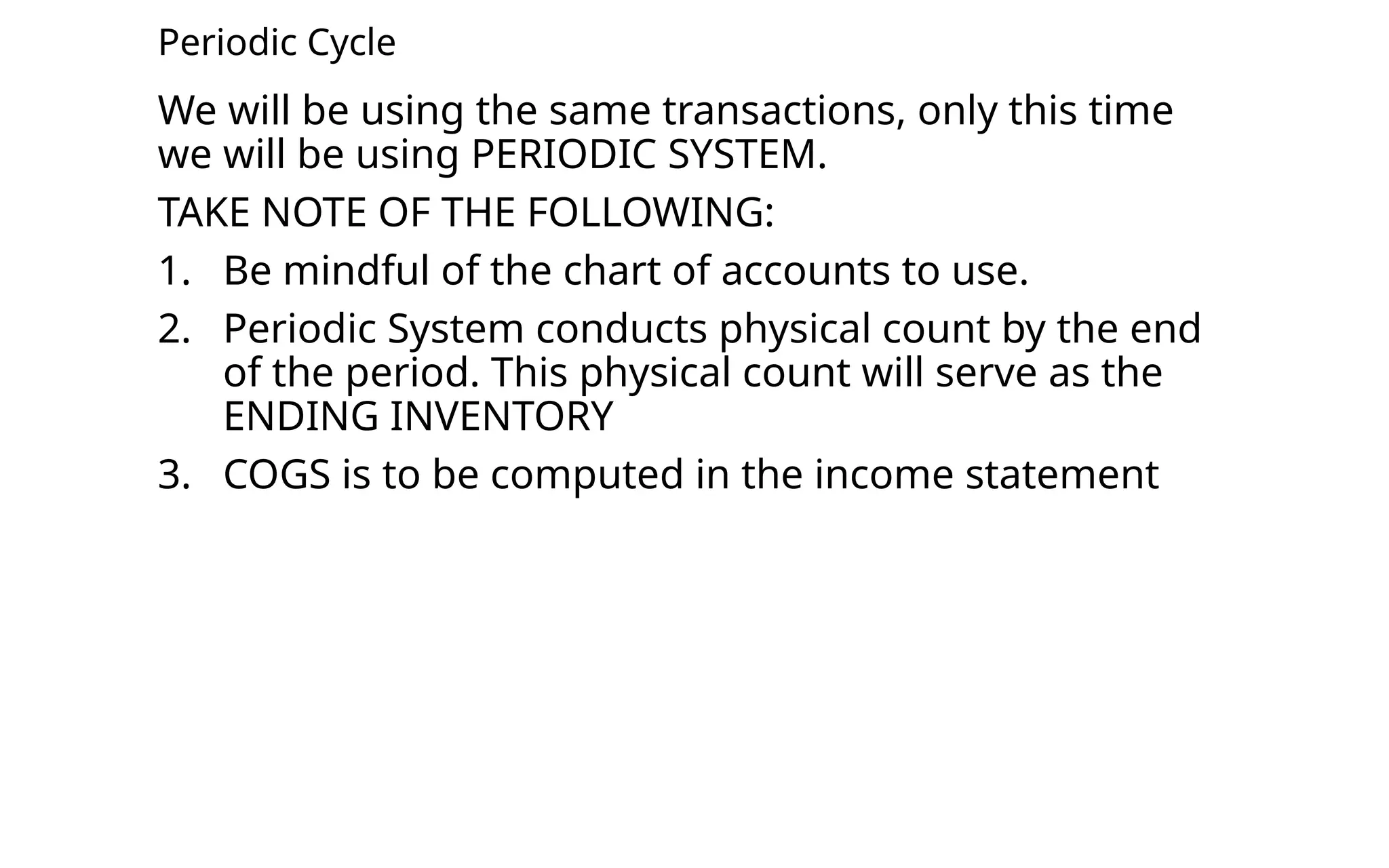

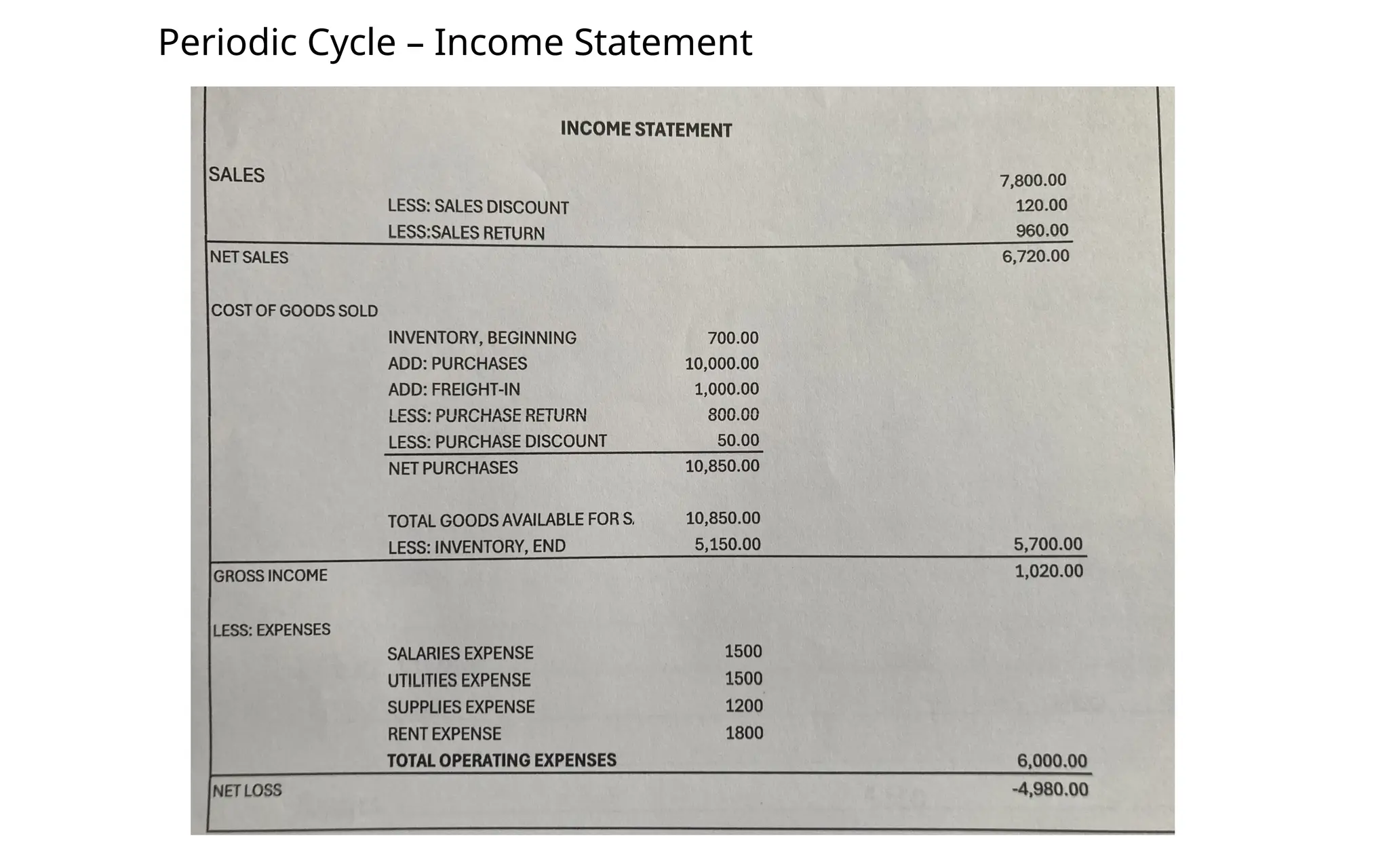

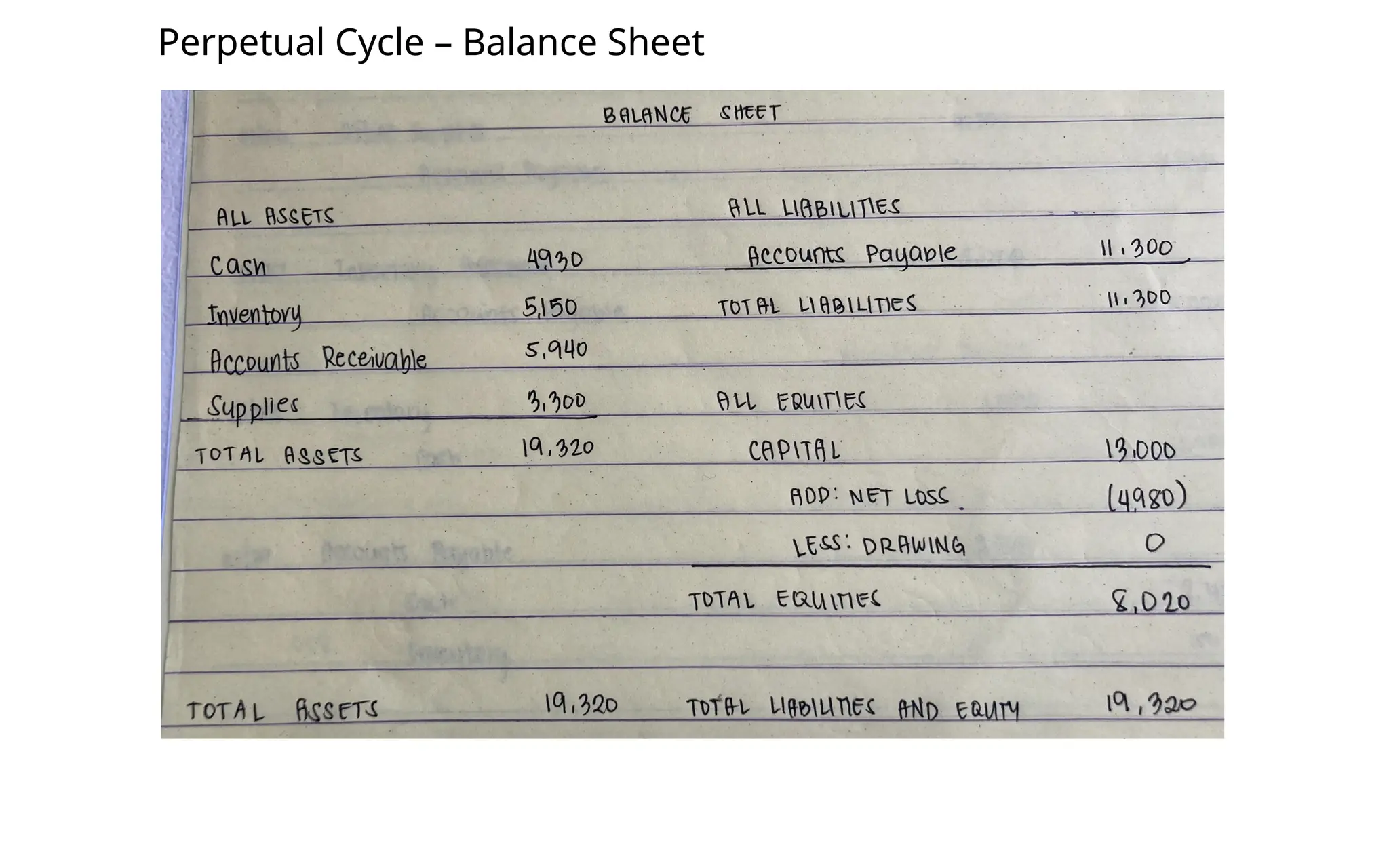

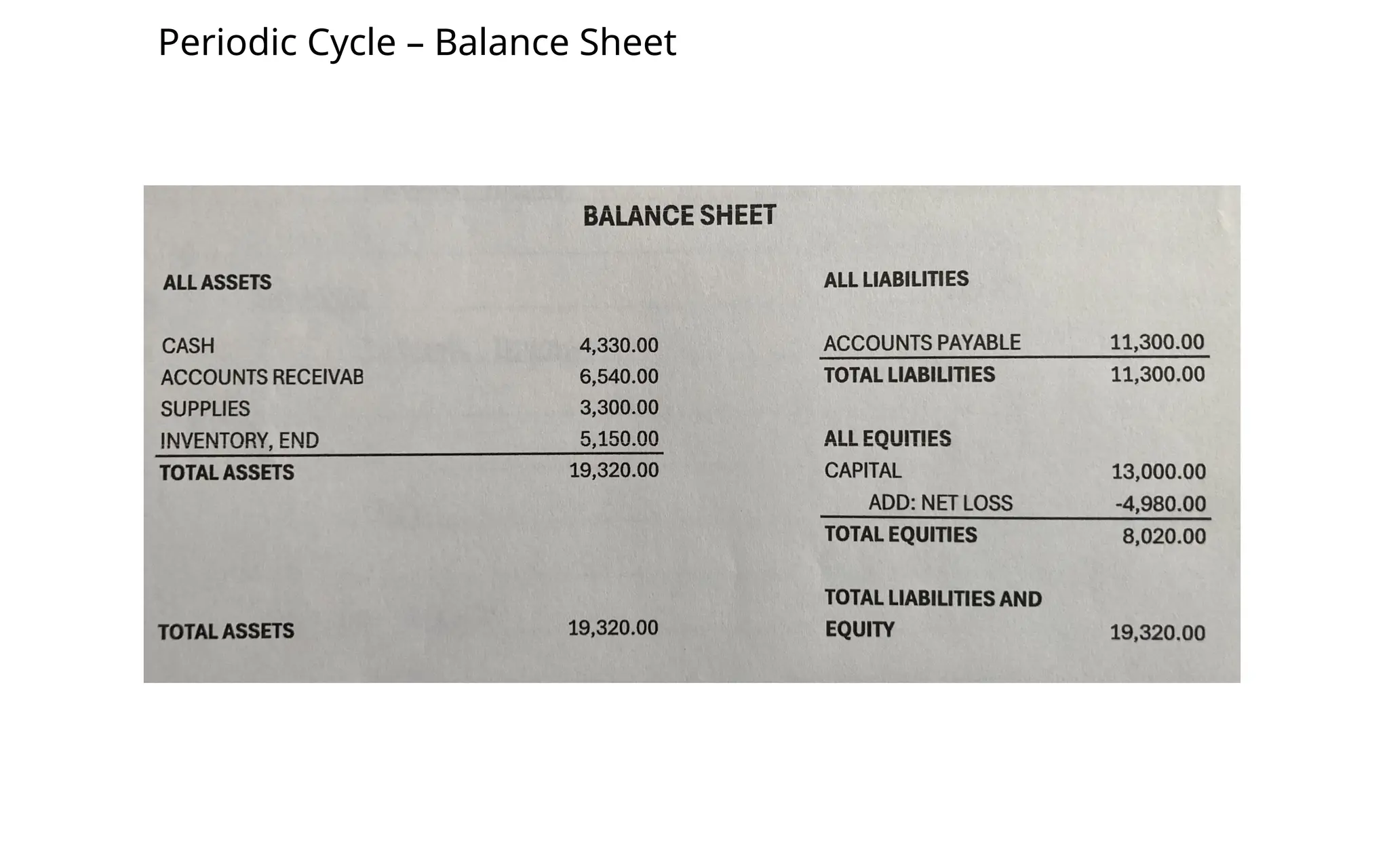

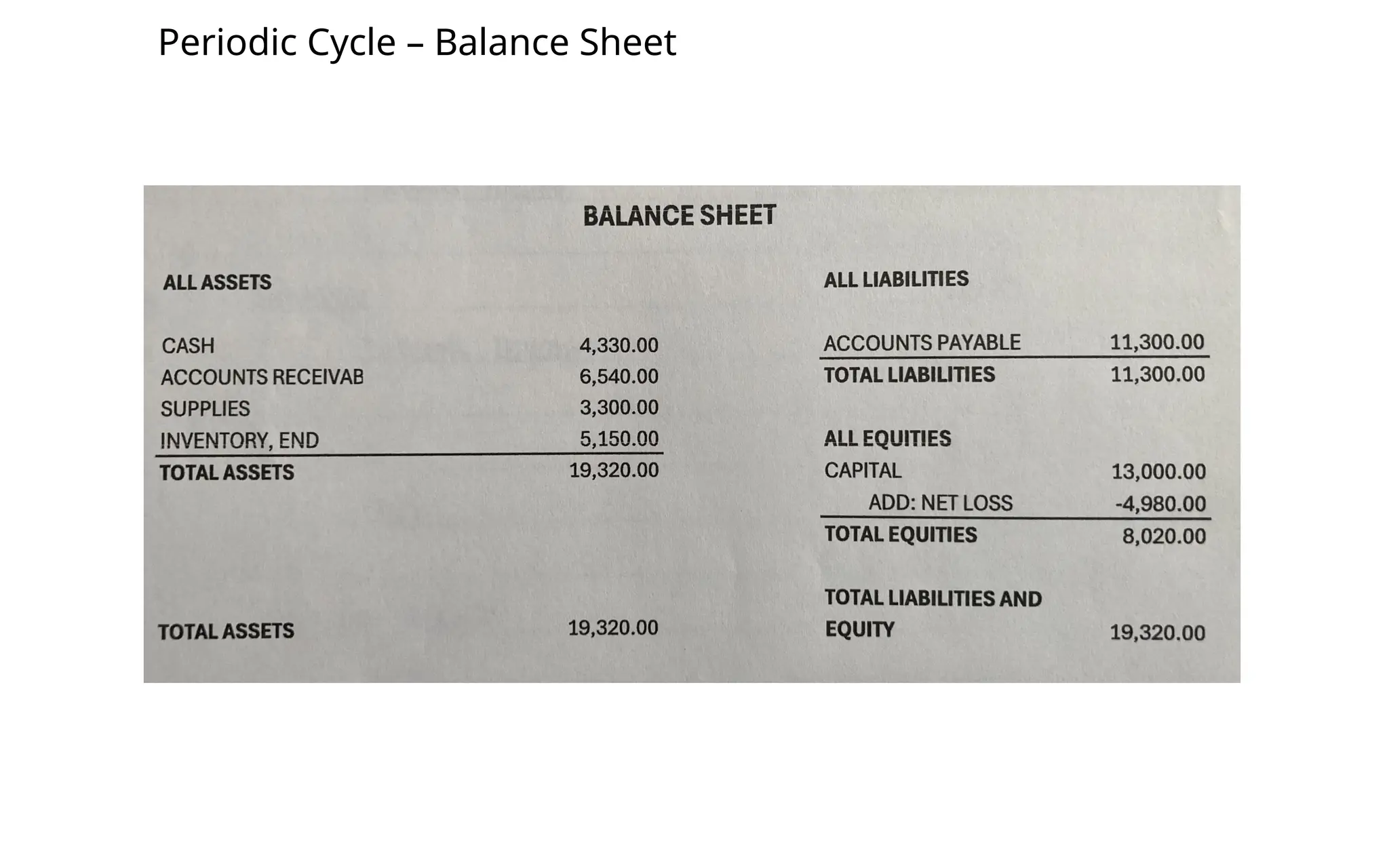

Periodic Cycle

We willbe using the same transactions, only this time

we will be using PERIODIC SYSTEM.

TAKE NOTE OF THE FOLLOWING:

1. Be mindful of the chart of accounts to use.

2. Periodic System conducts physical count by the end

of the period. This physical count will serve as the

ENDING INVENTORY

3. COGS is to be computed in the income statement

47.

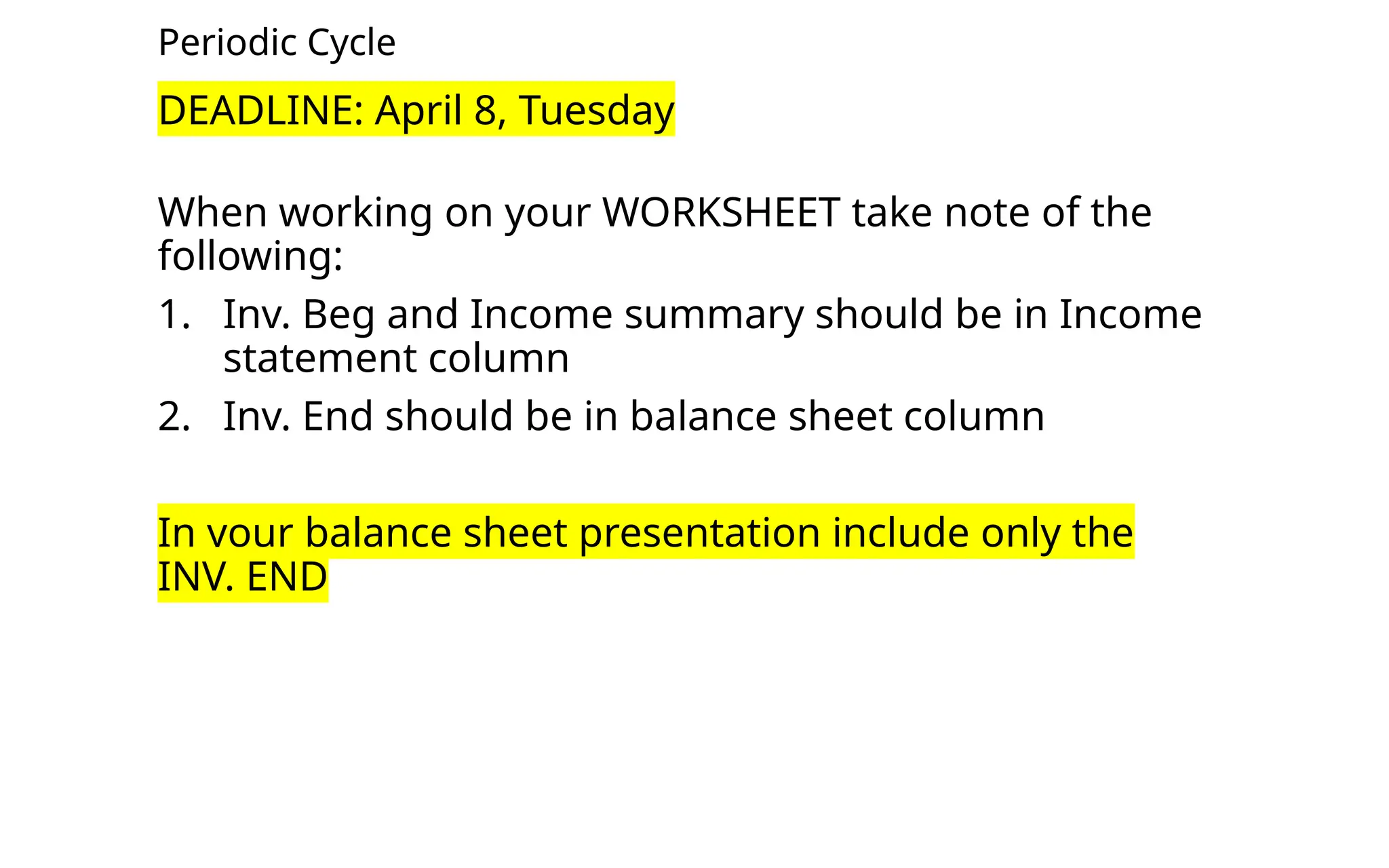

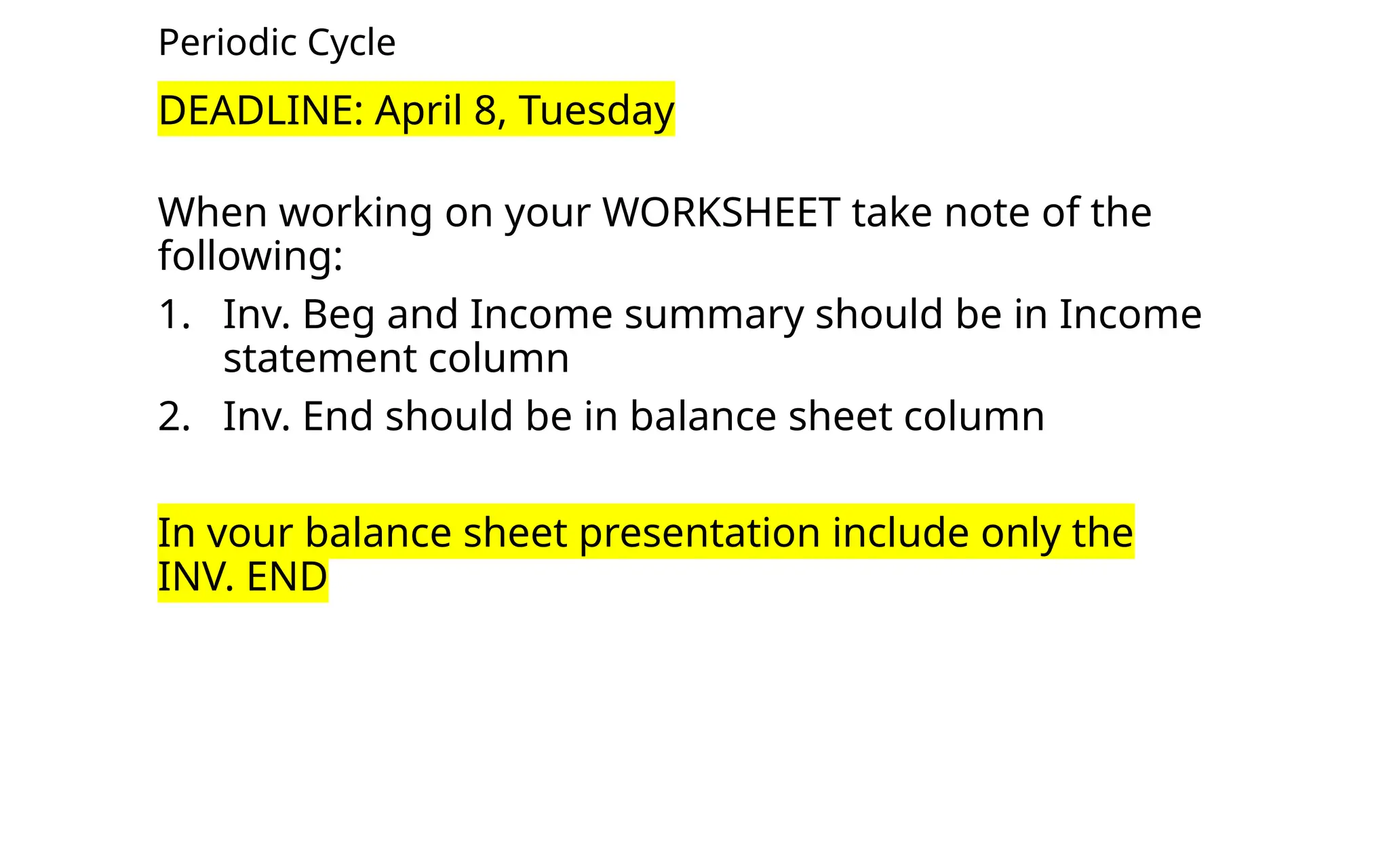

Periodic Cycle

DEADLINE: April8, Tuesday

When working on your WORKSHEET take note of the

following:

1. Inv. Beg and Income summary should be in Income

statement column

2. Inv. End should be in balance sheet column

In your balance sheet presentation include only the

INV. END

48.

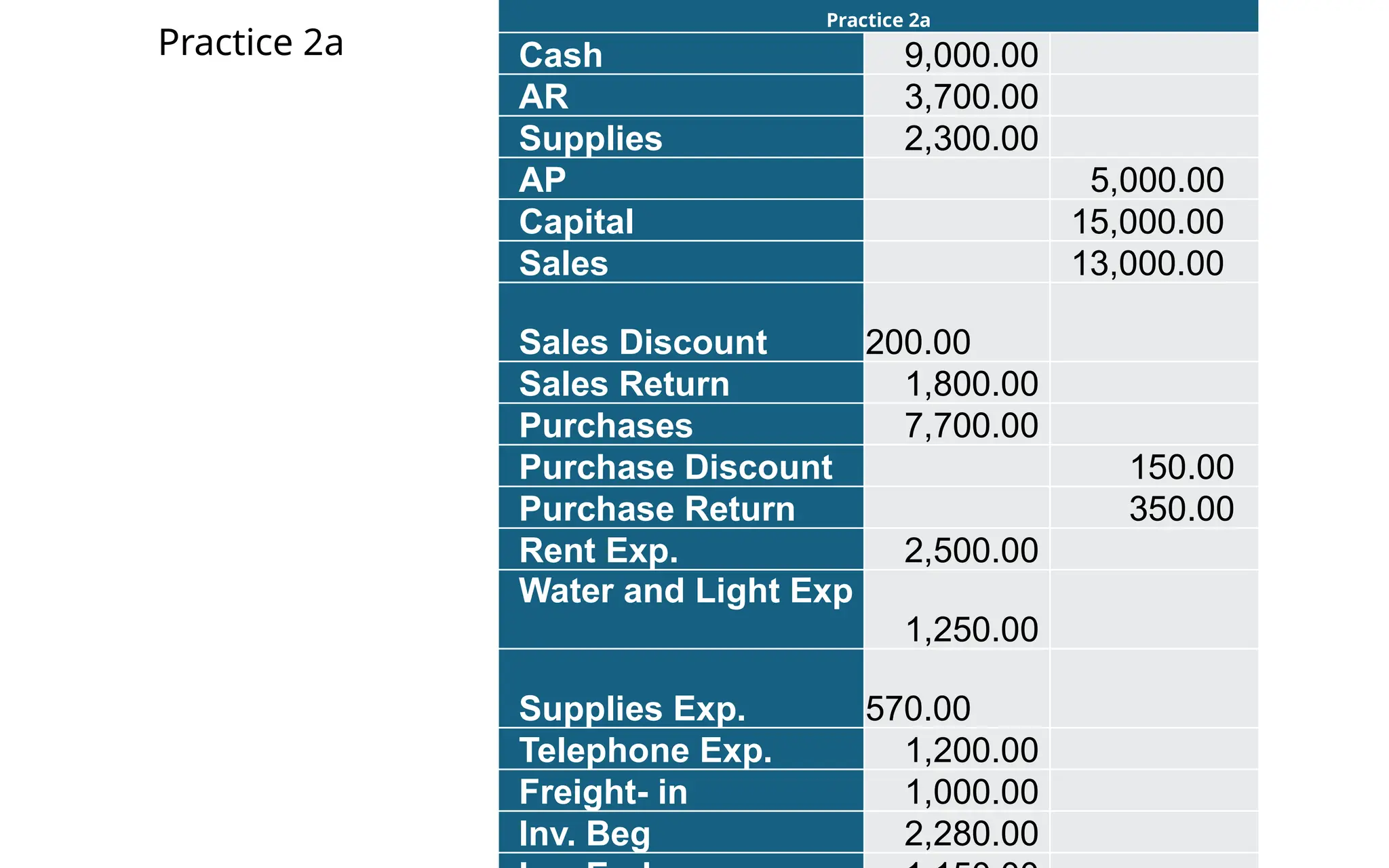

Practice 2a

Practice 2a

Cash9,000.00

AR 3,700.00

Supplies 2,300.00

AP 5,000.00

Capital 15,000.00

Sales 13,000.00

Sales Discount 200.00

Sales Return 1,800.00

Purchases 7,700.00

Purchase Discount 150.00

Purchase Return 350.00

Rent Exp. 2,500.00

Water and Light Exp

1,250.00

Supplies Exp. 570.00

Telephone Exp. 1,200.00

Freight- in 1,000.00

Inv. Beg 2,280.00

50.

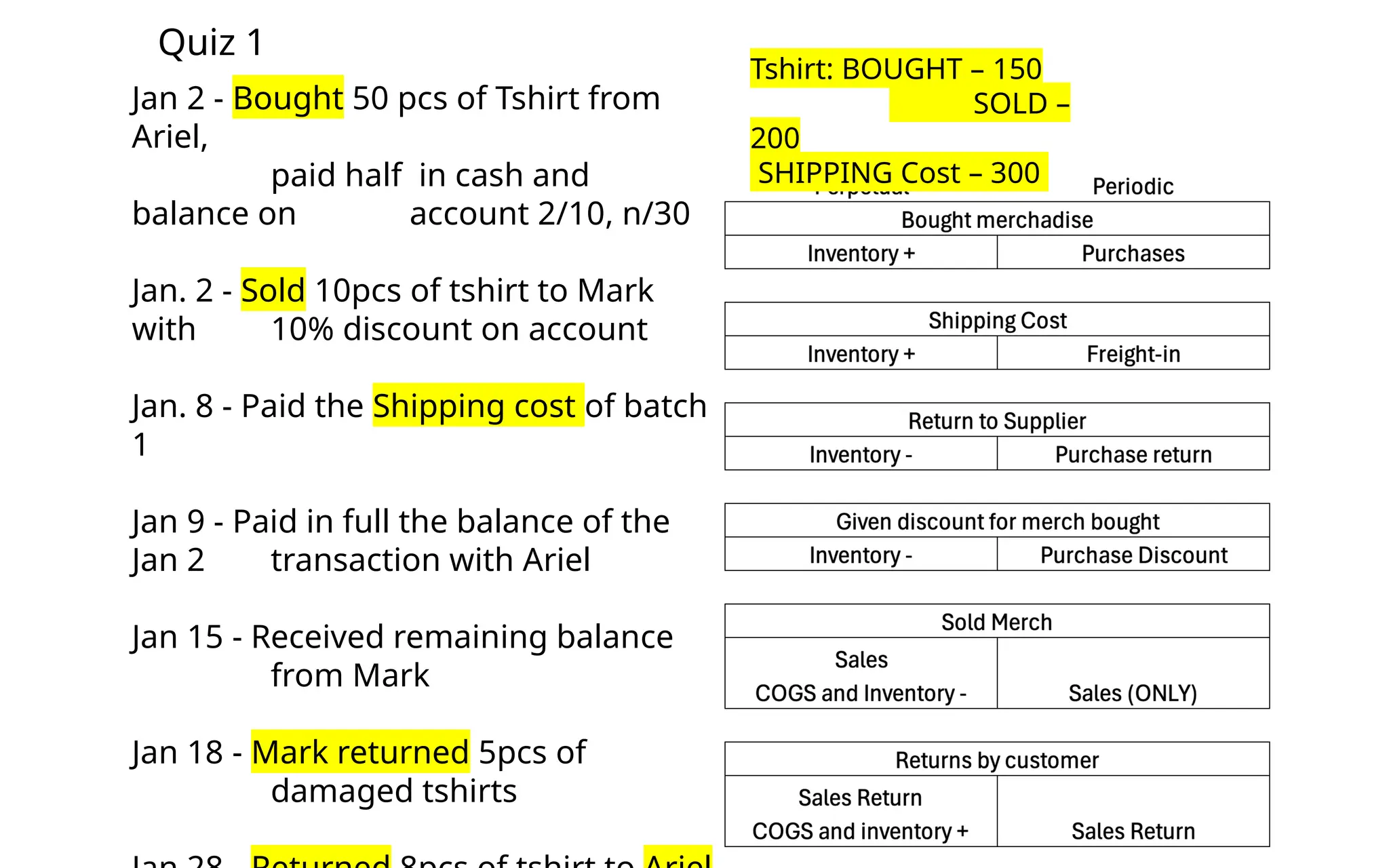

Quiz 1

Jan 2- Bought 50 pcs of Tshirt from

Ariel,

paid half in cash and

balance on account 2/10, n/30

Jan. 2 - Sold 10pcs of tshirt to Mark

with 10% discount on account

Jan. 8 - Paid the Shipping cost of batch

1

Jan 9 - Paid in full the balance of the

Jan 2 transaction with Ariel

Jan 15 - Received remaining balance

from Mark

Jan 18 - Mark returned 5pcs of

damaged tshirts

Tshirt: BOUGHT – 150

SOLD –

200

SHIPPING Cost – 300

51.

Periodic Cycle

DEADLINE: April8, Tuesday

When working on your WORKSHEET take note of the

following:

1. Inv. Beg and Income summary should be in Income

statement column

2. Inv. End should be in balance sheet column

In your balance sheet presentation include only the

INV. END

52.

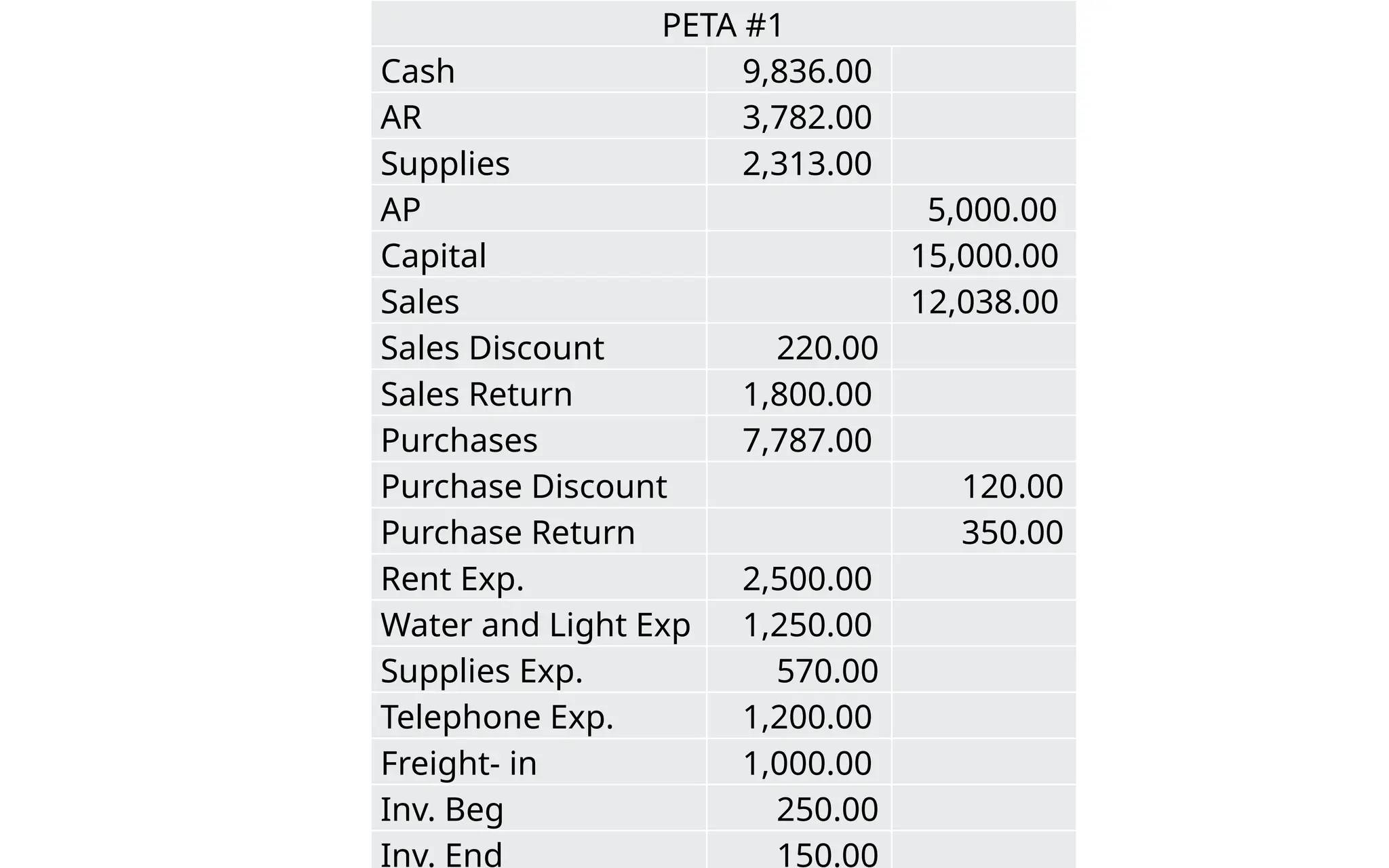

PETA #1

Cash 9,836.00

AR3,782.00

Supplies 2,313.00

AP 5,000.00

Capital 15,000.00

Sales 12,038.00

Sales Discount 220.00

Sales Return 1,800.00

Purchases 7,787.00

Purchase Discount 120.00

Purchase Return 350.00

Rent Exp. 2,500.00

Water and Light Exp 1,250.00

Supplies Exp. 570.00

Telephone Exp. 1,200.00

Freight- in 1,000.00

Inv. Beg 250.00

Inv. End 150.00

53.

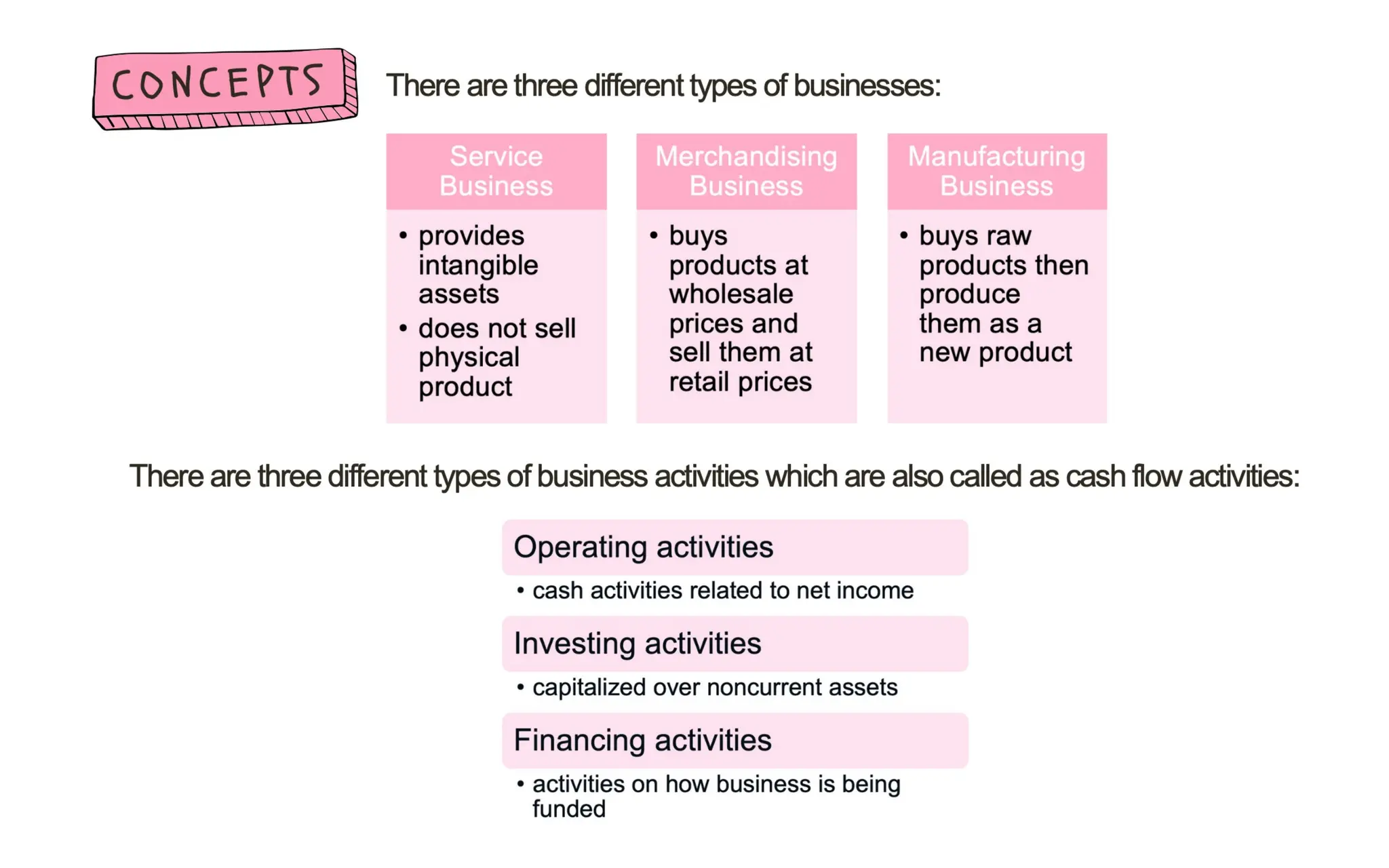

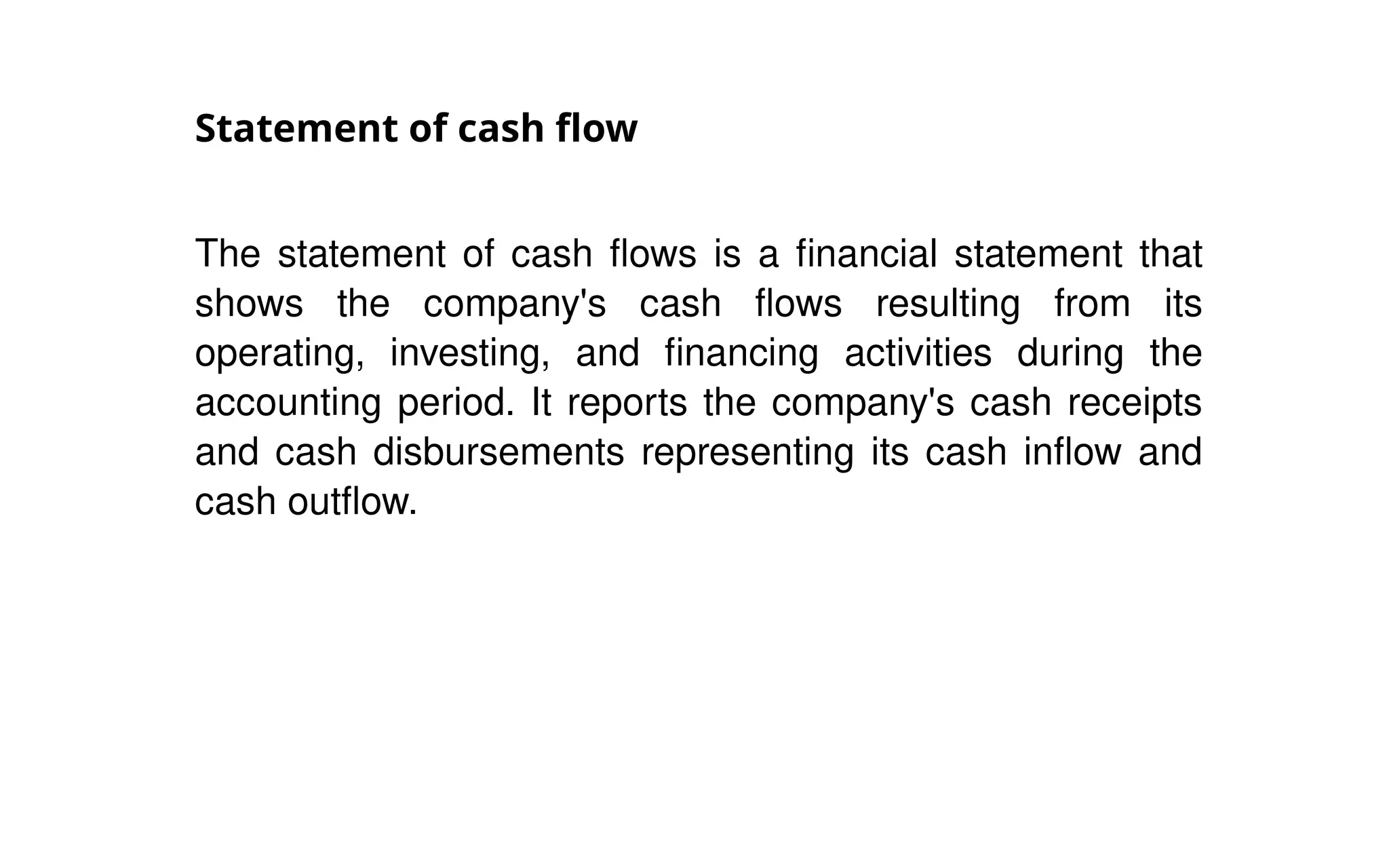

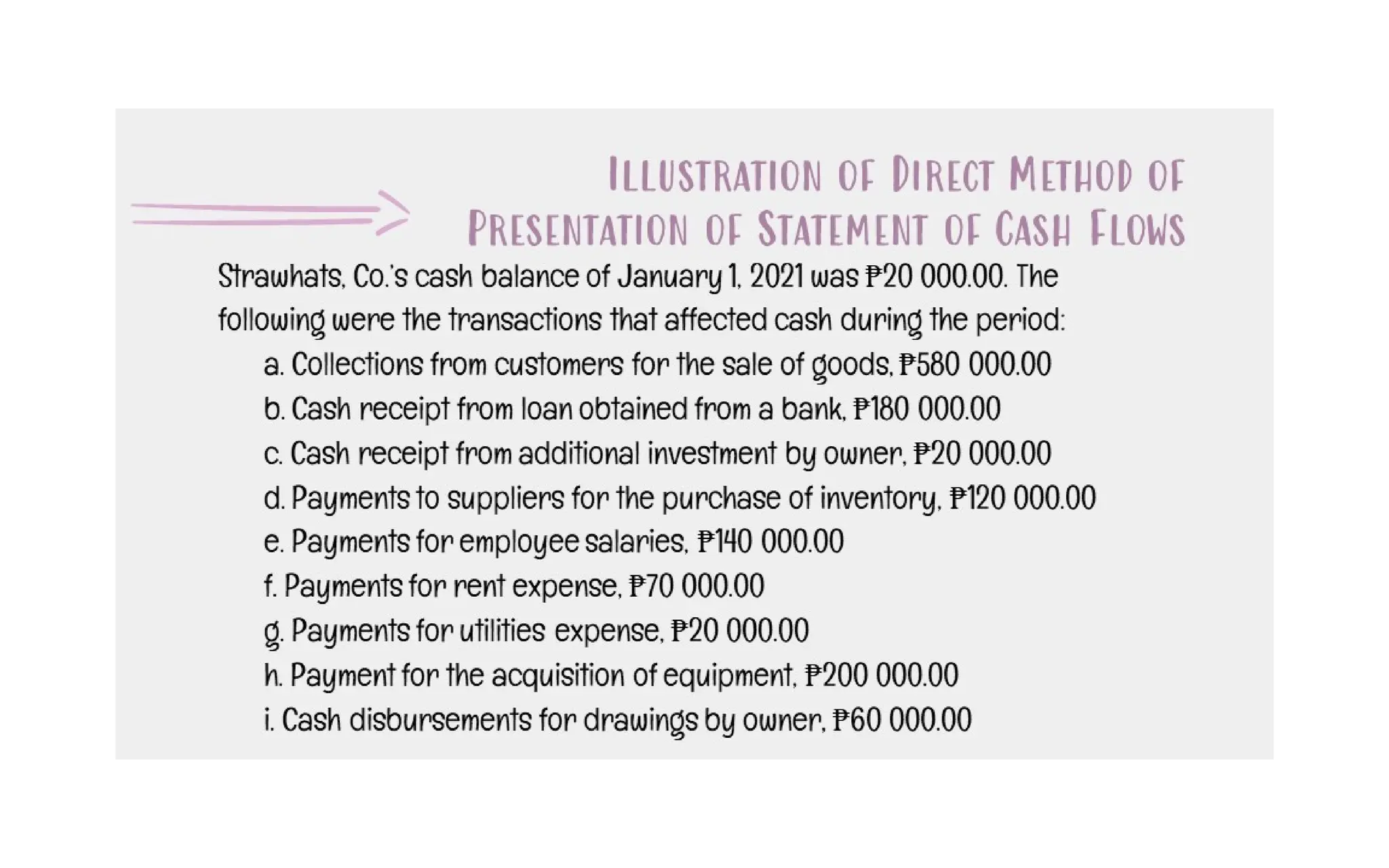

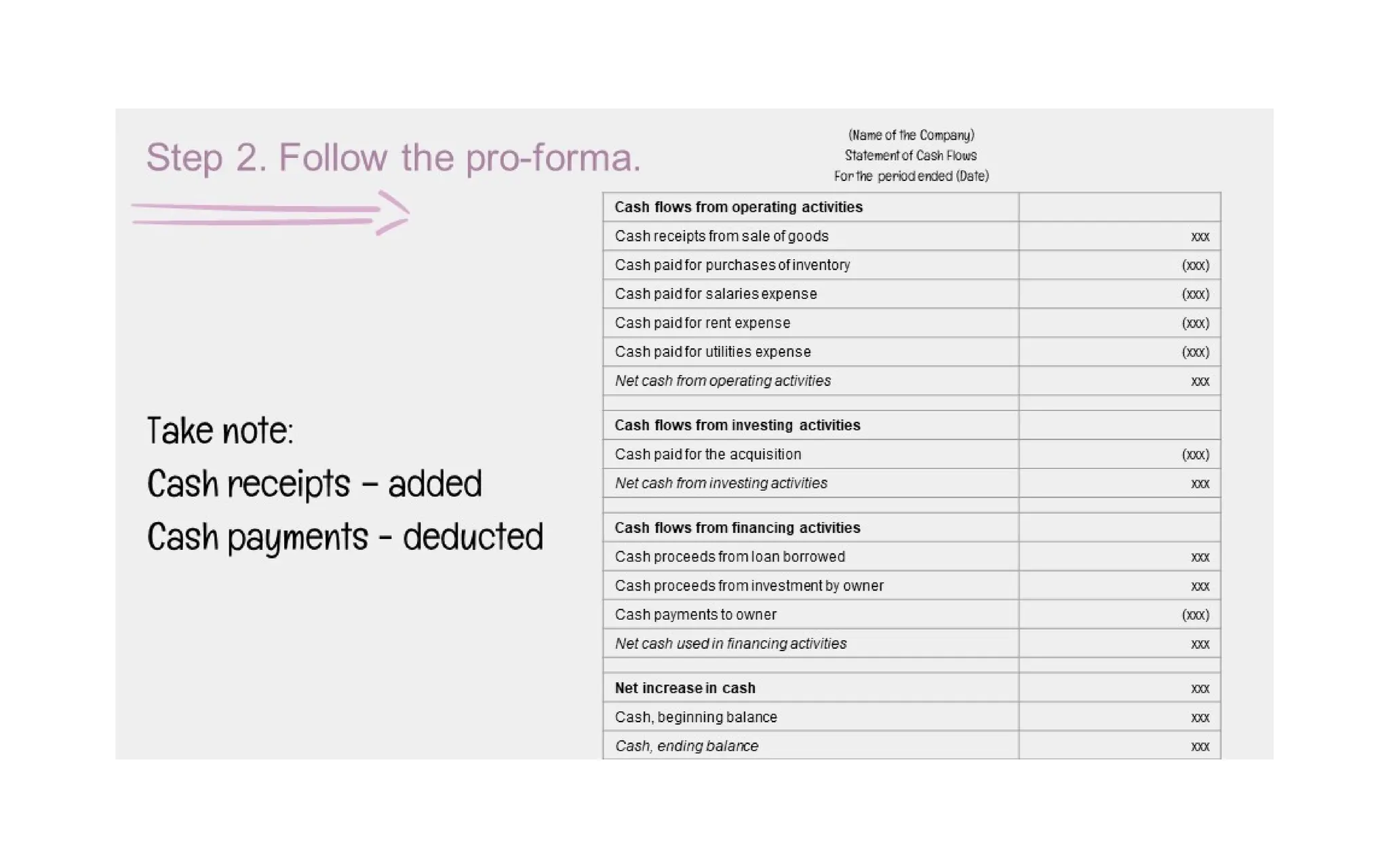

Statement of cashflow

The statement of cash flows is a financial statement that

shows the company's cash flows resulting from its

operating, investing, and financing activities during the

accounting period. It reports the company's cash receipts

and cash disbursements representing its cash inflow and

cash outflow.

54.

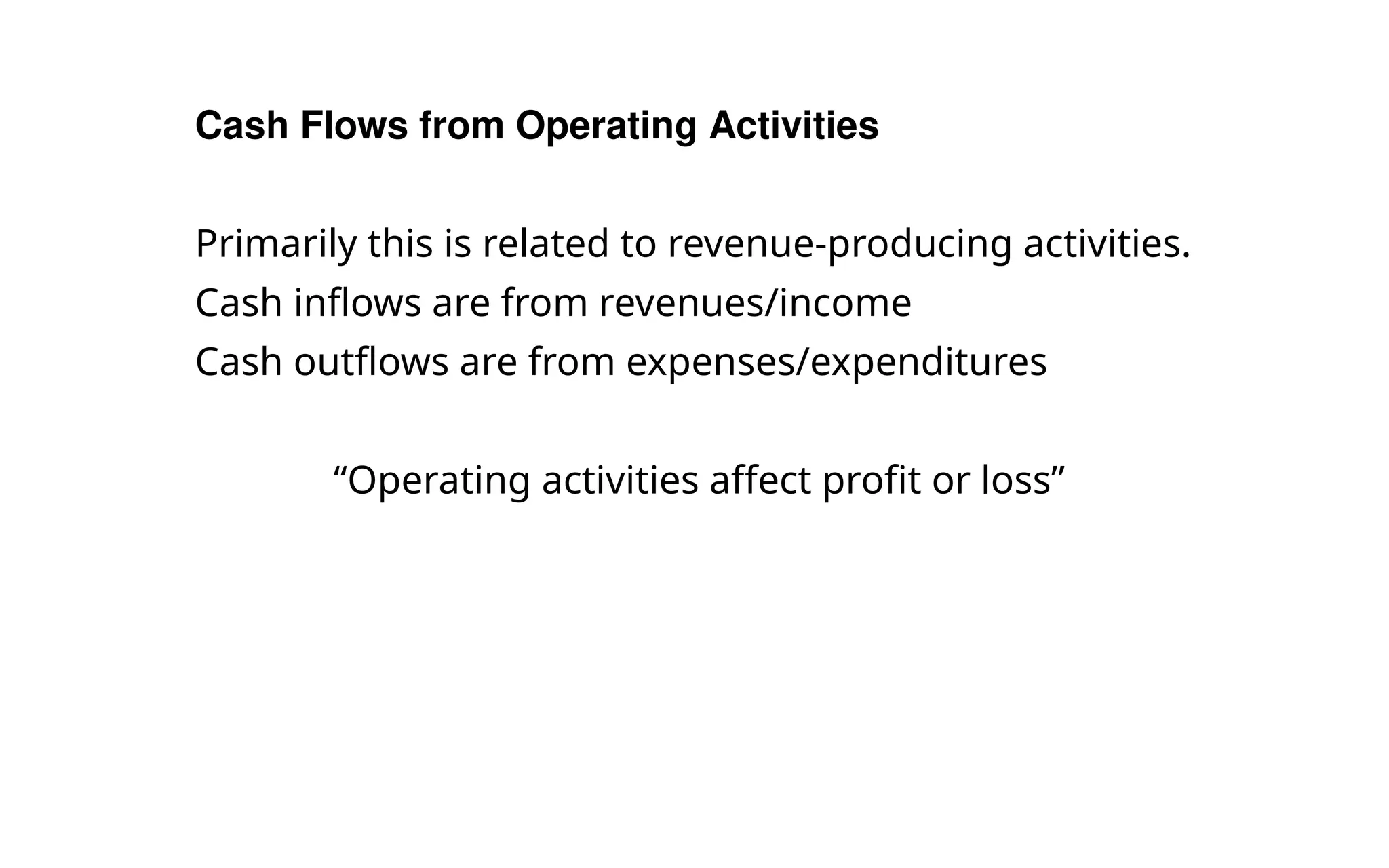

Cash Flows fromOperating Activities

Primarily this is related to revenue-producing activities.

Cash inflows are from revenues/income

Cash outflows are from expenses/expenditures

“Operating activities affect profit or loss”

55.

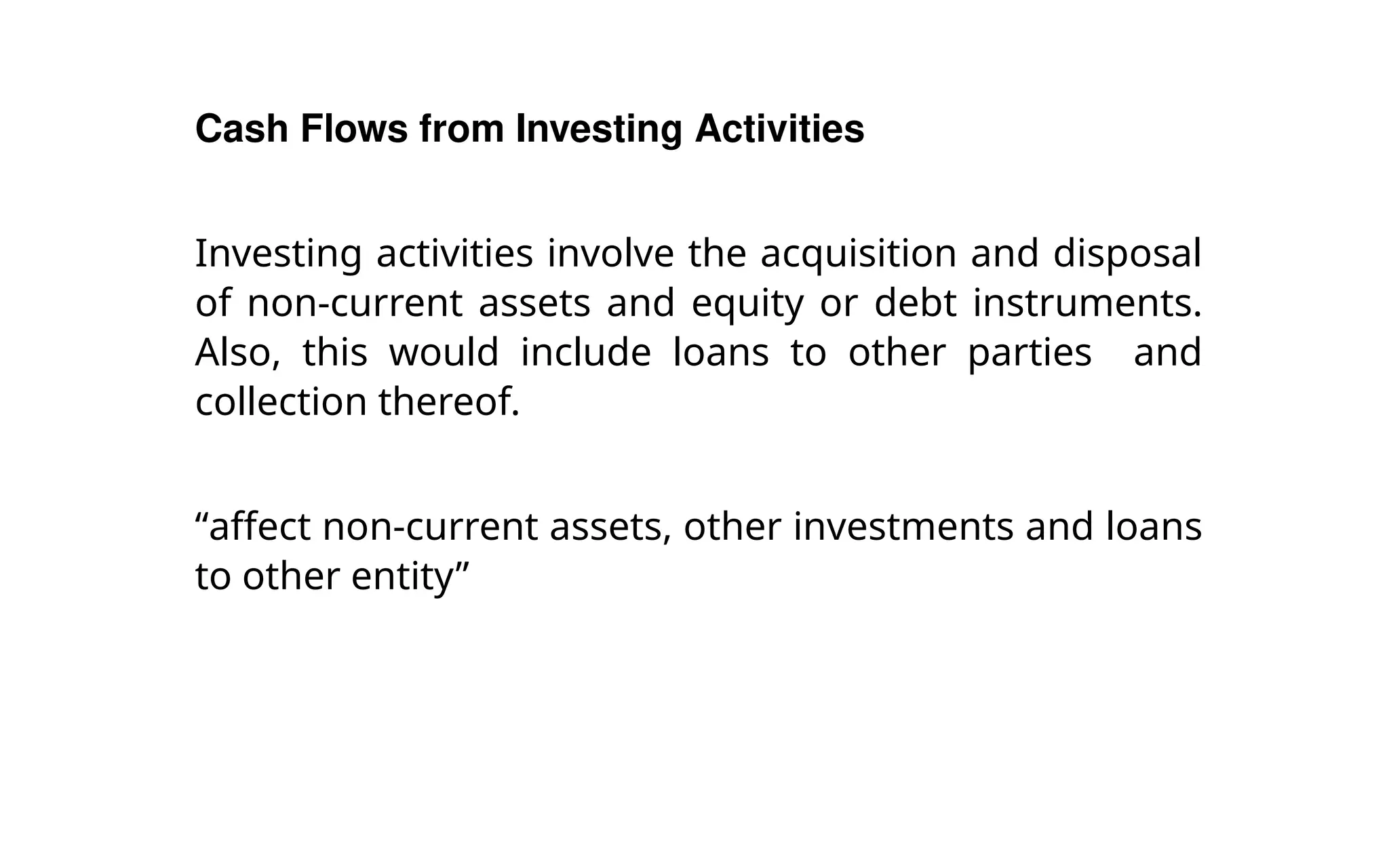

Cash Flows fromInvesting Activities

Investing activities involve the acquisition and disposal

of non-current assets and equity or debt instruments.

Also, this would include loans to other parties and

collection thereof.

“affect non-current assets, other investments and loans

to other entity”

56.

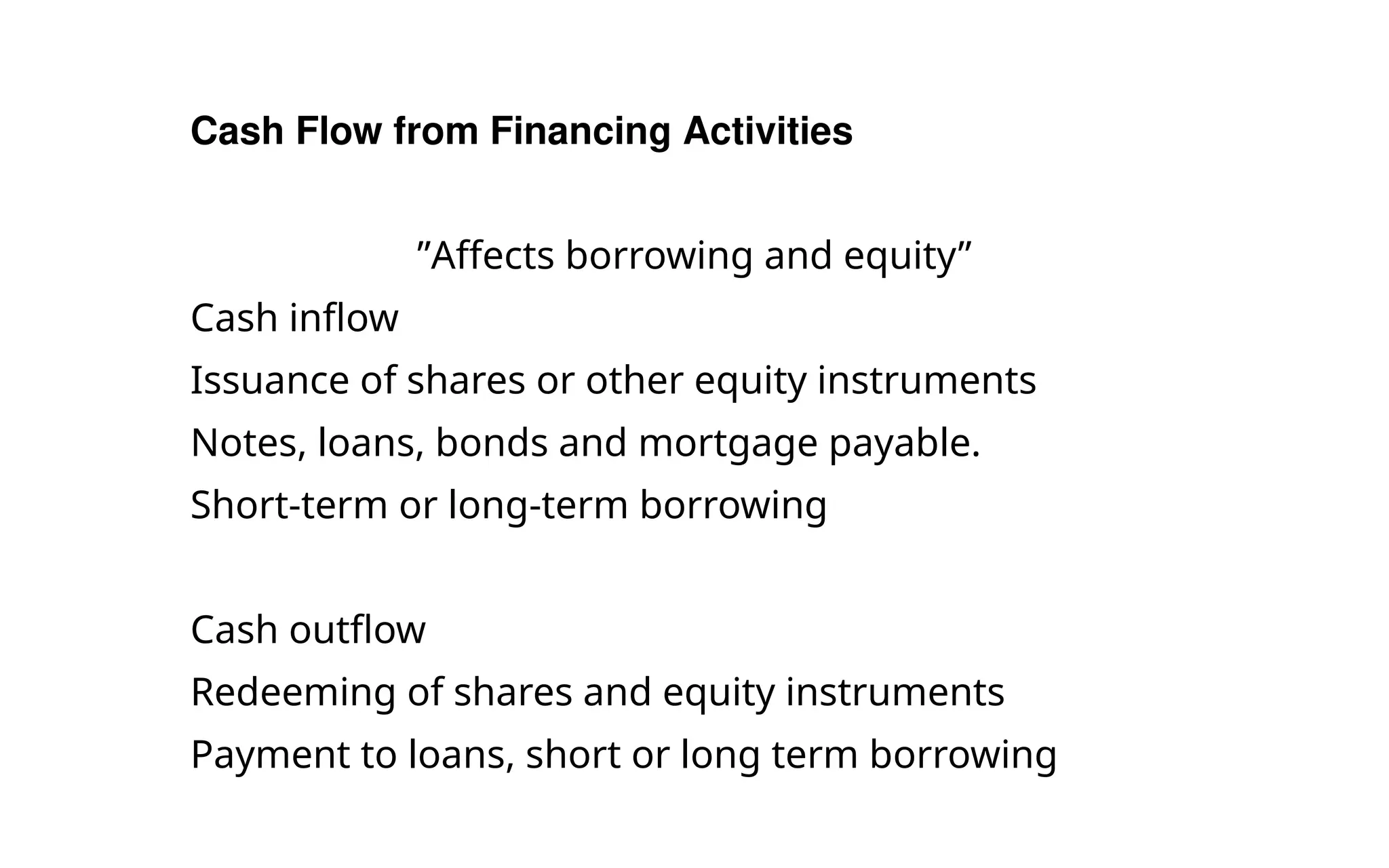

Cash Flow fromFinancing Activities

”Affects borrowing and equity”

Cash inflow

Issuance of shares or other equity instruments

Notes, loans, bonds and mortgage payable.

Short-term or long-term borrowing

Cash outflow

Redeeming of shares and equity instruments

Payment to loans, short or long term borrowing

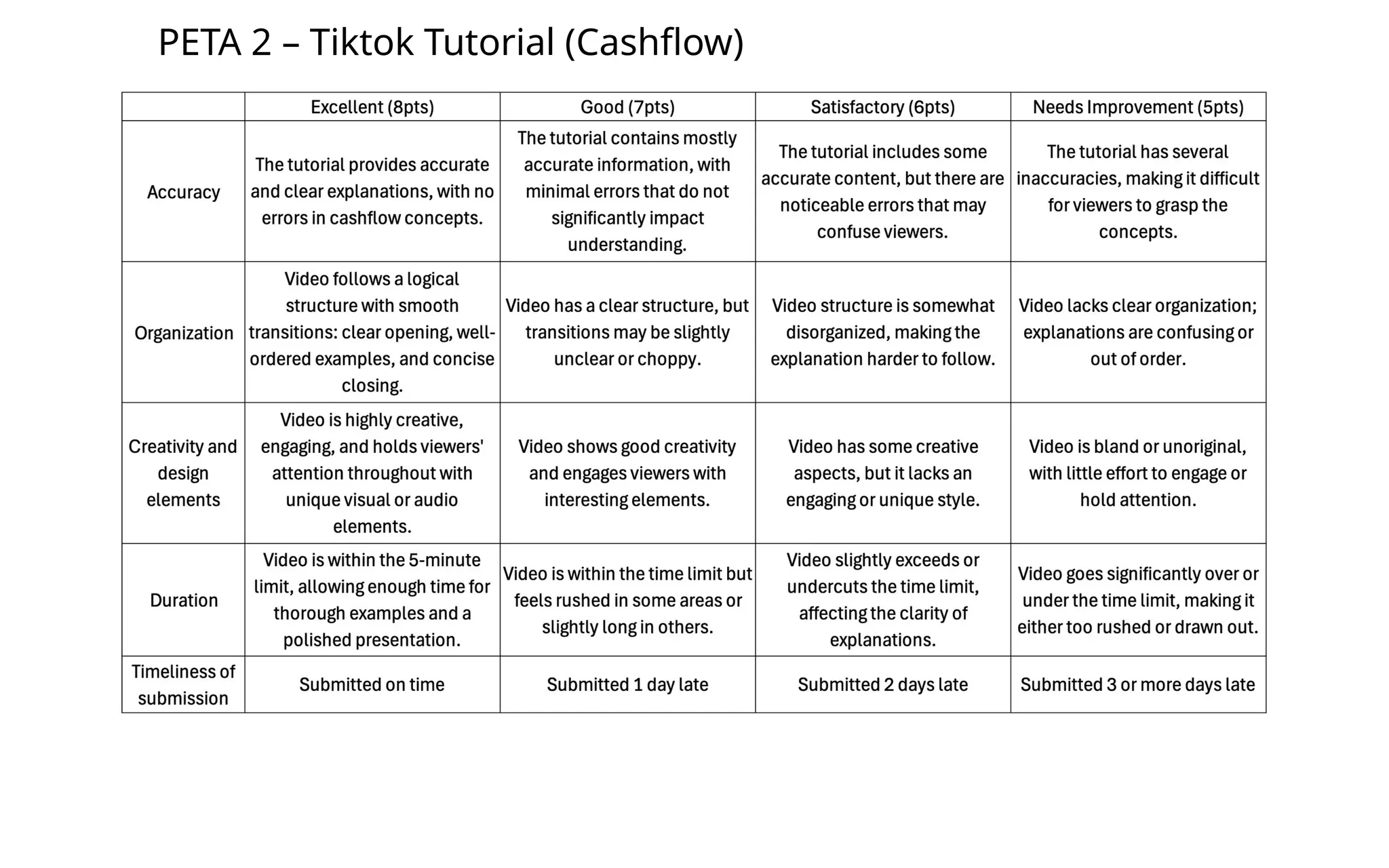

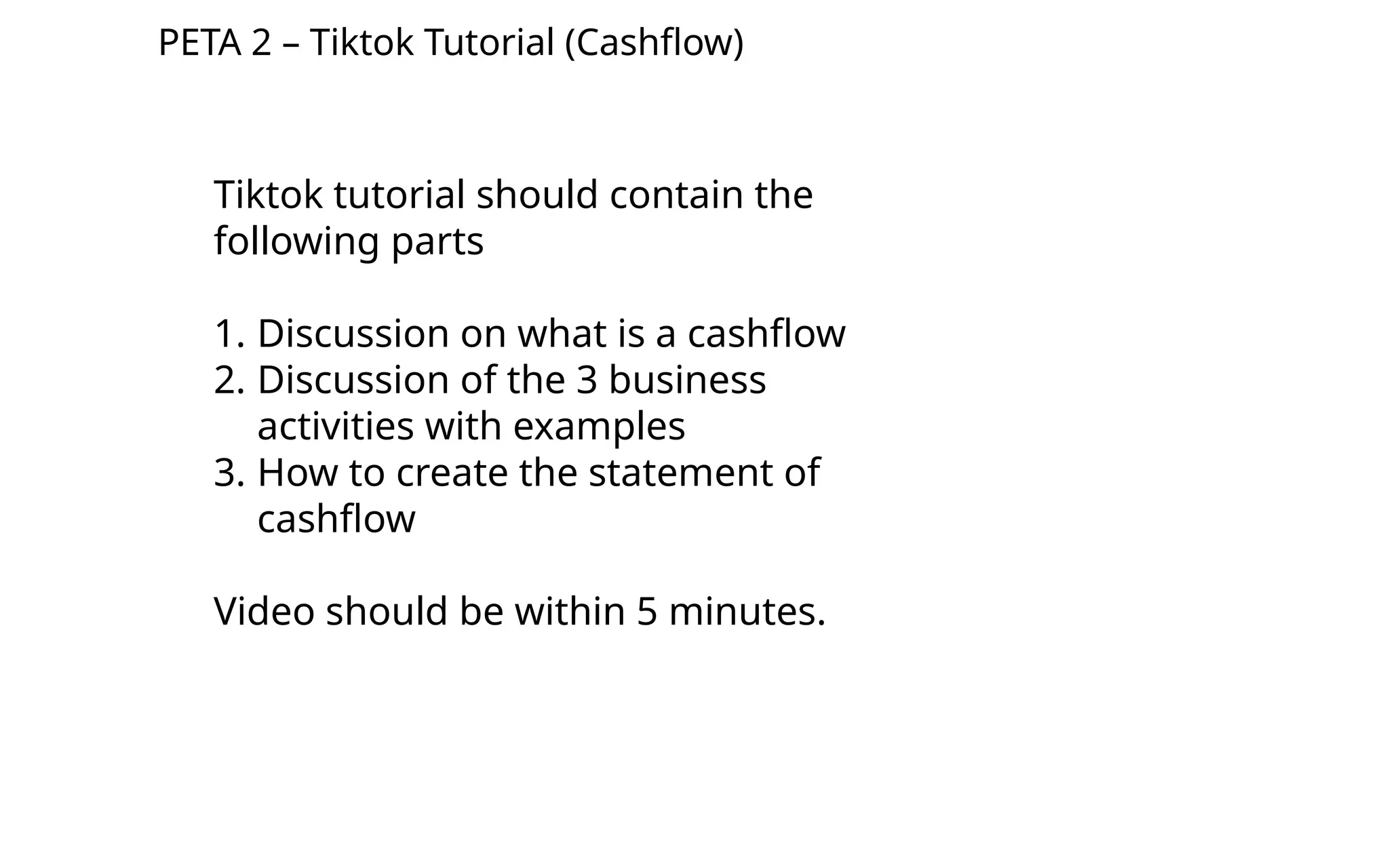

PETA 2 –Tiktok Tutorial (Cashflow)

Tiktok tutorial should contain the

following parts

1. Discussion on what is a cashflow

2. Discussion of the 3 business

activities with examples

3. How to create the statement of

cashflow

Video should be within 5 minutes.

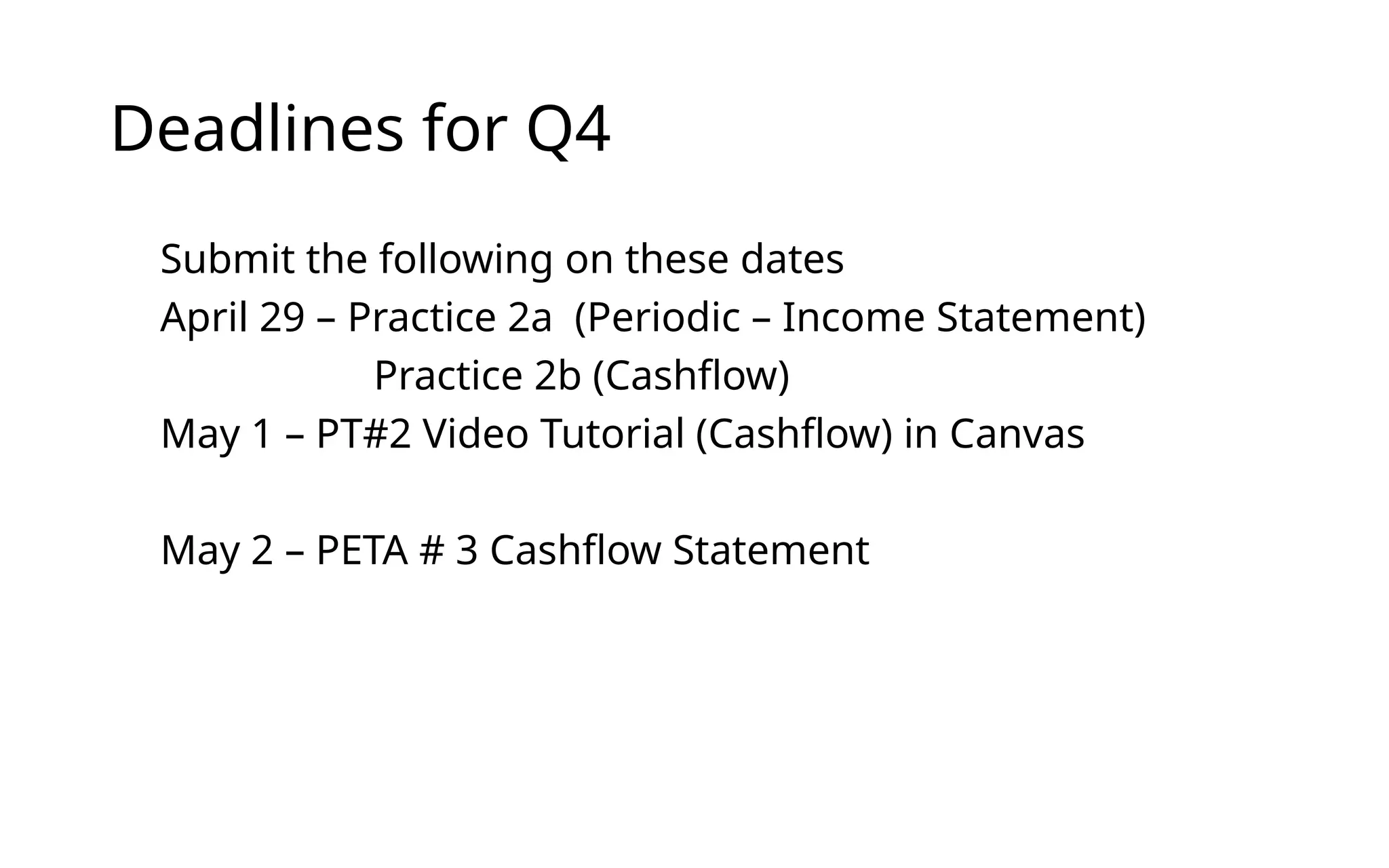

Deadlines for Q4

Submitthe following on these dates

April 29 – Practice 2a (Periodic – Income Statement)

Practice 2b (Cashflow)

May 1 – PT#2 Video Tutorial (Cashflow) in Canvas

May 2 – PETA # 3 Cashflow Statement

69.

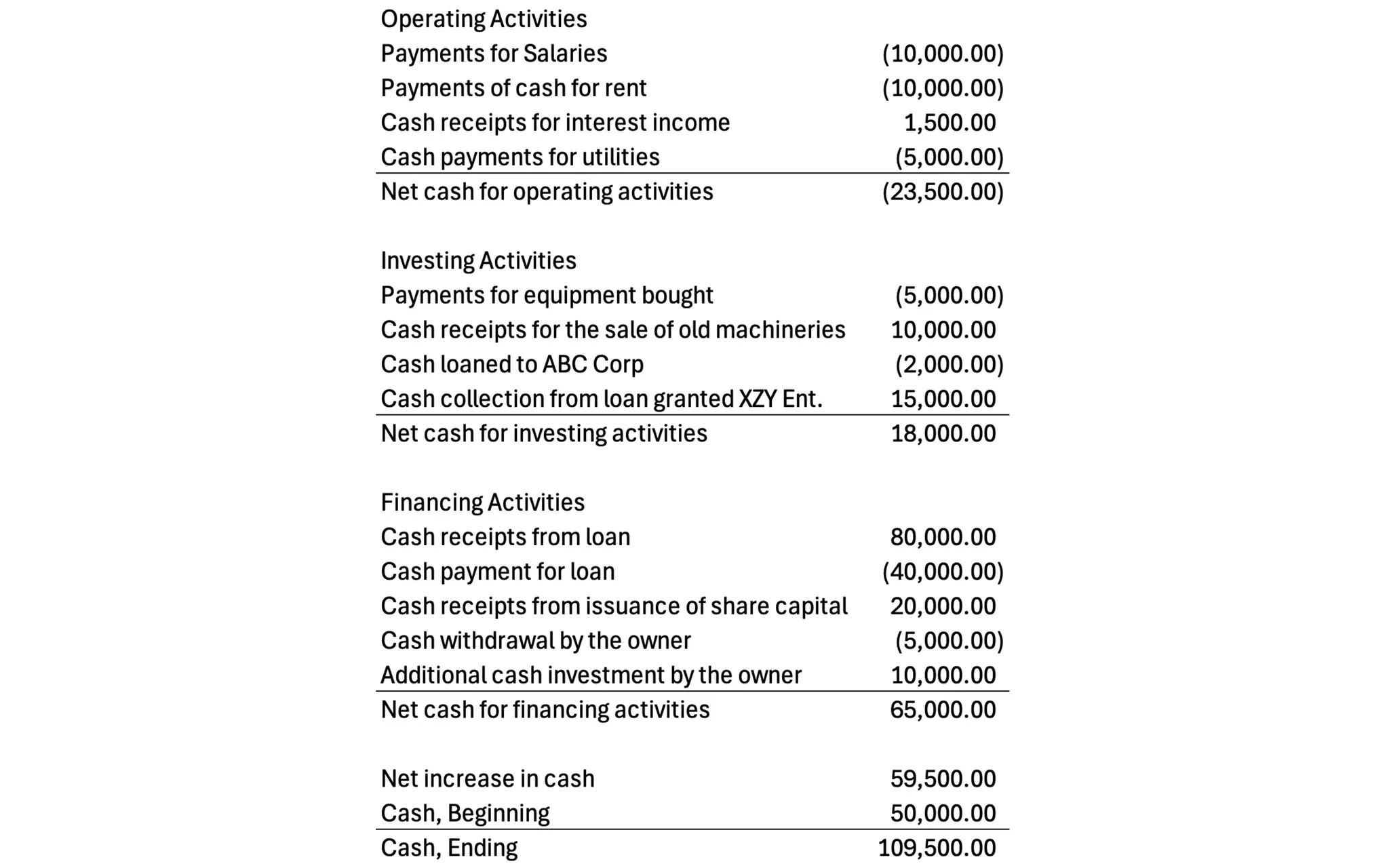

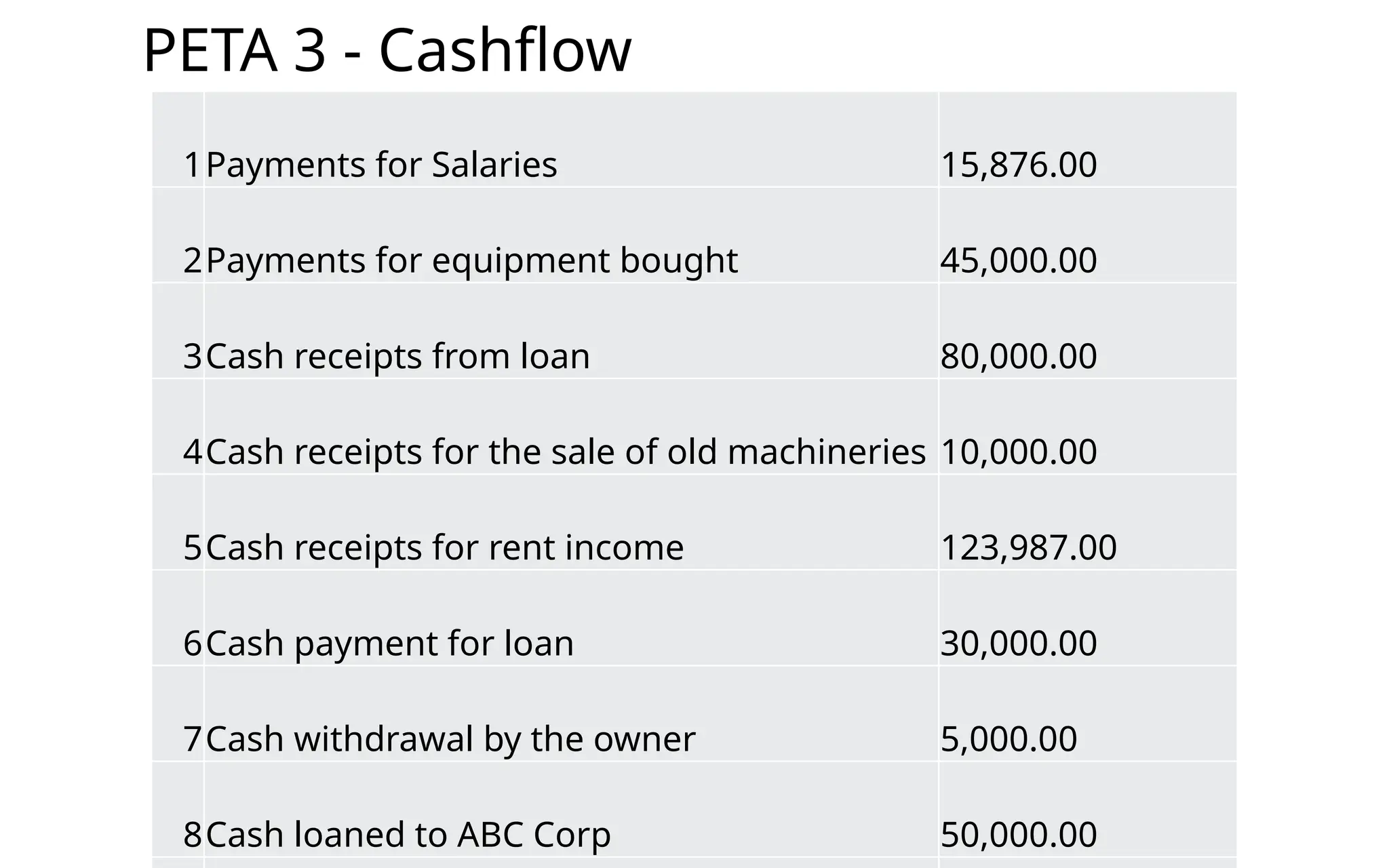

PETA 3 -Cashflow

1Payments for Salaries 15,876.00

2Payments for equipment bought 45,000.00

3Cash receipts from loan 80,000.00

4Cash receipts for the sale of old machineries 10,000.00

5Cash receipts for rent income 123,987.00

6Cash payment for loan 30,000.00

7Cash withdrawal by the owner 5,000.00

8Cash loaned to ABC Corp 50,000.00