European Commission economic forecasts

•

0 likes•13 views

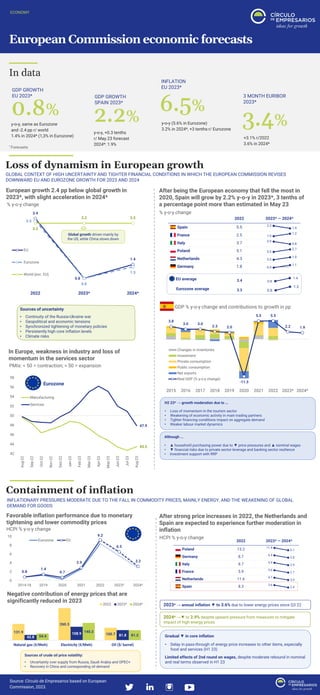

The document summarizes European Commission economic forecasts for the EU and Eurozone economies in 2023 and 2024. It finds that: 1) Growth in the EU and Eurozone will slow to 0.8% in 2023 before a slight acceleration to 1.4% in 2024, as high inflation and tighter financial conditions weigh on demand. 2) Inflation in the EU is forecast to decline to 6.5% in 2023 from its 2022 peak, and further decrease to 3.2% in 2024, assuming commodity prices and imported inflation continue to moderate. 3) Risks to the outlook include the ongoing war in Ukraine, geopolitical tensions, high core inflation persistence

Recommended

Recommended

More Related Content

Similar to European Commission economic forecasts

Similar to European Commission economic forecasts (20)

More from Círculo de Empresarios

More from Círculo de Empresarios (20)

Recently uploaded

Recently uploaded (20)

European Commission economic forecasts

- 1. 131.9 260.3 100.7 42.8 108.9 81.8 54.4 140.2 81.2 Natural gas (€/Mwh) Electricity (€/Mwh) Oil ($/ barrel) 2022 2023* 2024* 0.8 1.4 0.7 2.9 9.2 6.5 3.2 0 2 4 6 8 10 2014-18 2019 2020 2021 2022 2023* 2024* Eurozone EU European Commission economic forecasts ECONOMY In data Loss of dynamism in European growth Source: Círculo de Empresarios based on European Commission, 2023. * Forecasts GDP GROWTH SPAIN 2023* 2.2% y-o-y, +0.3 tenths r/ May.23 forecast 2024*: 1.9% 3 MONTH EURIBOR 2023* 3.4% +3.1% r/2022 3.6% in 2024* GLOBAL CONTEXT OF HIGH UNCERTAINTY AND TIGHTER FINANCIAL CONDITIONS IN WHICH THE EUROPEAN COMMISSION REVISES DOWNWARD EU AND EUROZONE GROWTH FOR 2023 AND 2024 Containment of inflation INFLATIONARY PRESSURES MODERATE DUE TO THE FALL IN COMMODITY PRICES, MAINLY ENERGY, AND THE WEAKENING OF GLOBAL DEMAND FOR GOODS Sources of uncertainty • Continuity of the Russia-Ukraine war • Geopolitical and economic tensions • Synchronized tightening of monetary policies • Persistently high core inflation levels • Climate risks GDP GROWTH EU 2023* 0.8% y-o-y, same as Eurozone and -2.4 pp r/ world 1.4% in 2024* (1,3% in Eurozone) INFLATION EU 2023* 6.5% y-o-y (5.6% in Eurozone) 3.2% in 2024*, +3 tenths r/ Eurozone In Europe, weakness in industry and loss of momentum in the services sector PMIs: < 50 = contraction; > 50 = expansion 3.4 0.8 1.4 3.3 0.8 1.3 3.2 3.2 3.2 2022 2023* 2024* EU Eurozone World (exc. EU) European growth 2.4 pp below global growth in 2023*, with slight acceleration in 2024* % y-o-y change EU average 3.4 0.8 1.4 Eurozone average 3.3 0.8 1.3 After being the European economy that fell the most in 2020, Spain will grow by 2.2% y-o-y in 2023*, 3 tenths of a percentage point more than estimated in May 23 % y-o-y change Global growth driven mainly by the US, while China slows down 43.5 47.9 42 44 46 48 50 52 54 56 58 Aug-22 Sep-22 Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 Mar-23 Apr-23 May-23 Jun-23 Jul-23 Aug-23 Manufacturing Services Eurozone H2 23* → growth moderation due to … • Loss of momentum in the tourism sector • Weakening of economic activity in main trading partners • Tighter financing conditions impact on aggregate demand • Weaker labour market dynamics 2023* → annual inflation ▼ to 3.6% due to lower energy prices since Q3 22 Gradual ▼ in core inflation • Delay in pass-through of energy price increases to other items, especially food and services (H1 23) Limited effects of 2nd round on wages, despite moderate rebound in nominal and real terms observed in H1 23 3.8 3.0 3.0 2.3 2.0 -11.3 5.5 5.5 2.2 1.9 2015 2016 2017 2018 2019 2020 2021 2022 2023* 2024* Changes in inventories Investment Private consumption Public consumption Net exports Real GDP (% y-o-y change) GDP % y-o-y change and contributions to growth in pp Although ... • ▲ household purchasing power due to ▼ price pressures and ▲ nominal wages • ▼ financial risks due to private sector leverage and banking sector resilience • Investment support with RRP Negative contribution of energy prices that are significantly reduced in 2023 Sources of crude oil price volatility: • Uncertainty over supply from Russia, Saudi Arabia and OPEC+ • Recovery in China and corresponding oil demand Favorable inflation performance due to monetary tightening and lower commodity prices HCPI % y-o-y change After strong price increases in 2022, the Netherlands and Spain are expected to experience further moderation in inflation HCPI % y-o-y change 2024* →▼ to 2.9% despite upward pressure from measures to mitigate impact of high energy prices