Download as PDF, PPTX

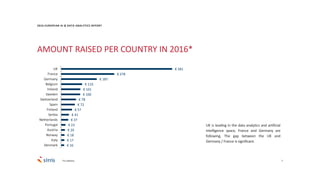

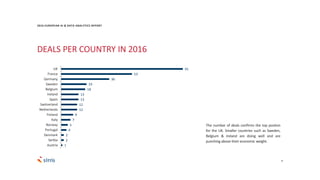

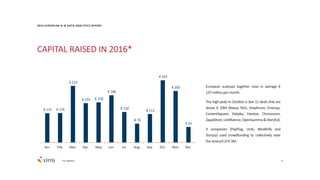

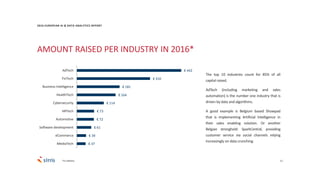

The 2016 European Artificial Intelligence and Data Analytics Scaleups Report provides an overview of funding trends and the performance of AI and data analytics startups across 22 European countries. It highlights that the UK leads in both funding and number of deals, while most AI scaleups are B2B oriented with a significant preference for content-driven business models. Key findings show that no European AI scaleups went public in 2016, and there is a marked gender disparity, with only 6% of founders or CEOs being female.