OC Roadshow Hosted by Bank of America Merrill Lynch – Philadelphia

ETFC Initiation

1. RBC Capital Markets, LLC

Bulent Ozcan, CFA (Analyst)

(212) 863-4818

bulent.ozcan@rbccm.com

Sector: Brokers, Asset Managers & Exchanges

Outperform

NASDAQ: ETFC; USD 27.05

Price Target USD 35.00

Scenario Analysis*

Downside

Scenario

23.00

15%

Current

Price

27.05

Price

Target

35.00

29%

Upside

Scenario

42.00

55%

*Implied Total Returns

Key Statistics

Shares O/S (MM): 289.2

Dividend: 0.00

Market Cap (MM): 7,822

Yield: 0.0%

Avg. Daily Volume: 3,072,501

RBC Estimates

FY Dec 2014A 2015E 2016E 2017E

EPS, Rpt Diluted 1.00 1.29 1.55 2.09

P/Rpt EPS 27.2x 21.0x 17.4x 12.9x

EBITDA 665.0 766.4 880.1 1,114.7

DPS 0.00 0.00 0.28 0.48

Div Yield 0.0% 0.0% 1.0% 1.8%

BVPS Basic 18.59 20.00 21.80 23.97

P/BVPS 1.46x 1.35x 1.24x 1.13x

EPS, Rpt Diluted Q1 Q2 Q3 Q4

2014 0.33A 0.24A 0.29A 0.14A

2015 0.28E 0.30E 0.35E 0.35E

2016 0.38E 0.36E 0.40E 0.41E

EBITDA

2014 198.0A 167.0A 178.0A 122.0A

2015 173.0E 182.4E 206.0E 204.9E

2016 218.1E 208.5E 226.7E 226.7E

All values in USD unless otherwise noted.

March 26, 2015

E*TRADE Financial Corporation

Initiating at Outperform: We Expect Excess Capital

to Grow Materially

Our view: E*TRADE Financial is a special situations story with significant

upside. Having realigned its legal entities, we expect excess capital at the

parent company to grow from $310 million today to close to $2 billion over

the next two years. We expect balance sheet growth to accelerate, as we

view the $50B size limitation as a temporary constraint.

Key points:

Our detailed analysis on the firm's excess capital position leads us to

believe that parent company liquidity could increase significantly over the

next two years. Moreover, we believe that the market underestimates

earnings growth, which could exceed a CAGR of 26% over the next three

years. We think that investors stand to reap the benefits of a restructuring

story that is still in the early innings:

• Capacity to upstream dividends improved significantly: Realignment of

legal entity structure provides the firm with financial flexibility, which

could accelerate efforts to return capital to its shareholders. We expect

share buybacks of $40 million in 2015 and $200 million in 2016.

• Excess capital to grow significantly: We expect earnings growth to add

over $1 billion to excess capital. Furthermore, we expect phasing in of

Basel III and running the bank at a Tier 1 leverage ratio of 8% to add

$599 million to excess capital. In addition, we believe that FDIC expense

reductions and deferred tax assets could contribute to excess capital

over time.

• Asset sensitivity to drive earnings growth: We believe that E*TRADE

Financial continues to be meaningfully interest-rate sensitive despite

the firm's hedging program. We estimate that earnings per share could

benefit by approximately 24 cents (21% accretive relative to 2014 EPS)

for a 50 basis points increase in interest rates.

• Sweep account optimization to boost balance sheet: A reduction in the

safety buffer needed to not exceed a targeted balance sheet size limit of

$50 billion could add approximately $3 billion to assets and $60 million

to net interest income. We expect this project to be completed in 1H/15.

• Over the longer term, expect balance sheet growth to accelerate as

the management team could abandon its $50B size limit: We believe

that the opportunity cost of remaining below $50B is going to increase

with rising interest rates. We estimate earnings could be 16 cents (14

percent) higher if the company managed approximately $15B of client

assets on its own balance sheet. We expect the opportunity cost to more

than double over the next three years. Furthermore, there seems to be

bipartisan support to revisit the $50B limit above which banks qualify as

“systemically important” under the Dodd-Frank Act. We think we could

see an upward revision of this threshold.

We arrive at our above consensus $35 price target by applying a 23x P/E

multiple on earnings of $1.55 and valuing deferred tax assets separately

at $2.

Priced as of prior trading day's market close, EST (unless otherwise noted).

For Required Conflicts Disclosures, see Page 48.

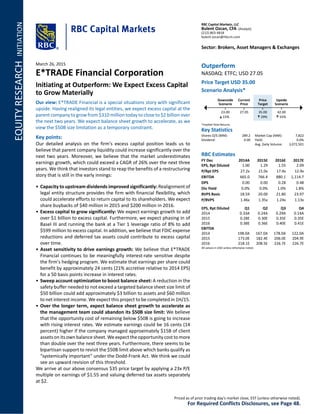

2. Target/Upside/Downside Scenarios

Exhibit 1: E*TRADE Financial Corporation

80m

60m

40m

20m

N

2012

D J F M A M J J A S O N

2013

D J F M A M J J A S O N

2014

D J F

2015

M

UPSIDE 42.00

TARGET 35.00

CURRENT 27.05

DOWNSIDE 23.00

Mar 2016

37.5

27.5

22.5

17.5

12.5

7.50

125 Weeks 02NOV12 - 25MAR15

ETFC Rel. S&P 500 COMPOSITE MA 40 weeks

Source: Bloomberg and RBC Capital Markets estimates for Upside/Downside/Target

Target price/base case

Our 12-month price target for E*TRADE is $35. We arrive at

our price target using a price-to-earnings multiple of 23.0x on

our 2016 calendar year earnings estimate of $1.55 per diluted

weighted average shares. We then discount the resulting

valuation using a cost of equity of 11.0%, before adding an

estimated value of $2 for the DTA to our valuation to arrive at

our price target.

These are our assumptions: Net interest margins of 283

basis points by the year 2016; average enterprise interest-

earning assets of $47.8 billion; daily average revenue trades of

175,776; average revenue per revenue trade of $11.00.

Upside scenario

Our valuation is $42. We arrive at our price target using a

price-to-earnings multiple of 25.0x on our 2016 calendar year

earnings estimate of $1.71. We then add $2 to our price target

for the DTA.

These are our assumptions: Net interest margins of 298

basis points by the year 2016; average enterprise interest-

earning assets of $47.8 billion; daily average revenue trades of

177,700; average revenue per revenue trade of $11.00.

Downside scenario

Our valuation is $23. We arrive at our price target using a

price-to-earnings multiple of 16.0x on our 2016 calendar year

earnings estimate of $1.39. We then add $2 to our price target

for the DTA.

These are our assumptions: Net interest margins of 268

basis points by the year 2016; average enterprise interest-

earning assets of $47.8 billion; daily average revenue trades of

173,861; average revenue per revenue trade of $11.00.

Investment summary

We think of E*TRADE Financial Corporation as a special

situations story that is still to play out. Investors stand to

reap the benefits of management's efforts to restructure the

company to unlock value.

Potential Catalysts

• Capacity to upstream dividends improved post the

realignment of legal entities and we expect excess capital

to grow significantly: Realignment of legal entity structure

could accelerate efforts to return capital to its shareholders.

We expect earnings growth to add over $1 billion to excess

capital over the next two years and phasing in of Basel III

& running the bank at a Tier 1 leverage ratio of 8% to add

another $599 million to excess capital.

• Asset sensitivity to drive earnings growth: We estimate

that earnings per share could benefit by approximately 24

cents (21% accretive to 2014 EPS) for a 50 basis points

increase in interest rates.

• We expect the firm to grow its balance sheet beyond

the $50 billion threshold: We estimate sweep account

optimization could boost balance sheet by approximately $3

billion in the near term. Furthermore, we would expect the

management team to abandon its $50 billion size limit as

higher interest rates add to the opportunity cost of having

third-party financial institutions manage the firm's assets.

Risks

• Drop in consumer confidence & commissions could

negatively impact commission revenues and earnings.

• Prolonged period of low interest rates could compress net

interest margins.

• Unforeseen regulatory constraints could impact valuation.

• Balance sheet growth below our expectation could lead to

an earnings miss.

• Changes in average balances, especially client margin, could

impact operating results. Revenues could fall short of our

expectation were balance sheet growth to slow significantly

or decline.

• The company has significant exposure to mortgage

loans which could result in losses due to deteriorating

performance.

• Sharp decline in securities markets & deterioration in credit

markets/housing which could lead to a sharp increase in

provisions and a decline in earnings.

• Deferred tax assets might not be realized. The firm has about

$1 billion of deferred tax assets. E*TRADE might have to

establish a valuation allowance against these reserves if it

determines that not all of these assets will be realized. This

could negatively impact earnings and valuation.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 2

3. Key questions

Our view

1. Given the recent announcement

on the upcoming realignment of its

legal entities, what are the likely

options for returning capital to

shareholders?

The firm’s January announcement that its regulators have approved plans to modify

the corporate structure is a significant positive development. This should enable the

firm to upstream dividends and excess capital of $509 million in 1Q/15.

Furthermore, it should become meaningfully less burdensome to get regulatory

approval to upstream quarterly dividends to the parent company in the future.

However, we believe that investors should not expect dividend payments in 2015.

We believe that the management team is done de-levering the balance sheet. We

view balance sheet growth, de-risking legacy assets, and share buybacks as the most

likely use of excess capital. We expect dividend payments to commence in 2016 at

the earliest. We estimate that excess capital could approach $2 billion by the end of

2016.

2. Are there any catalysts that could

drive the share price even higher

given recent performance?

We believe that the firm is in its 4

th

inning. The realignment of its legal entities has

put the firm in a position to return capital. We believe that excess capital will grow

significantly from here on. We expect earnings growth, phasing in of Basel III,

running E*TRADE Bank at a Tier 1 leverage ratio, reduction in FDIC charges, and

usage of deferred tax assets to add significantly to excess capital. We provide the

details in the note.

3. How should investors think about

asset growth as the company

approaches the $50 billion SIFI

mark?

While one could argue that growth could be limited given the company’s current

desire to limit the size of its balance sheet, we believe that the firm’s balance sheet

will exceed $50 billion in 2016. Certainly, right now, it makes sense to avoid more

stringent regulatory capital requirements and adherence to enhanced prudential

standards under the Dodd-Frank Act. However, there seems to be bipartisan

support to raise the $50 billion threshold to be considered systemically important.

Furthermore, we believe that the opportunity cost of using third-party financial

institutions to manage the firm’s assets will grow with rising interest rates. We

believe that a sweep account optimization will allow the firm to approach $50 billion

quickly. We also think that the firm will start managing the $10.5 billion of non-

money market client assets at third parties on its balance sheet with rising interest

rates. We estimate that earnings could be boosted by $0.36/share by 2017 by

managing the assets on E*TRADE’s balance sheet.

4. How asset sensitive is the firm and

should investors buy ETFC’s shares

to position themselves for rising

rates?

We estimate that a 50 basis points move in interest rates would impact earnings per

share to the tune of 24 cents (21% accretive relative to 2014 EPS). In comparison,

we would expect TD Ameritrade’s earnings to be impacted by around 12 cents to 14

cents (9% accretive based on 2014 EPS) and Charles Schwab’s earnings by about 31

cents (33% accretive based on 2014 EPS). Despite generating about 60% of its

revenues through spread-based revenues, earnings are not as interest rate sensitive

as one would expect. We believe that the company has taken a defensive posture

and hedged its interest rate exposure meaningfully. Management could decide to

reduce its hedging efforts with rising interest rates, potentially picking up

incremental earnings beyond our estimate.

5. What risks remain on the balance

sheet post the company’s efforts

to de-risk it?

While the company’s management has done a tremendous job de-risking the

company’s balance sheet, E*TRADE Financial’s balance sheet continues to remain

meaningfully more risky than that of its peers, in our view. The company maintains a

sizeable exposure to mortgage loans. Whereas we are not as concerned about the

HELOC portfolio, as the allowance for loan losses seems adequate, we have seen a

significant decline in provisions for loan losses for one- to four-family home loans.

About $1.3 billion of a total of $3.1 billion of one- to four-family home loans will

convert from interest only to amortizing loans over the coming three years. An

increase in frequency or severity of losses could lead to the need to add to reserves

as the company has been releasing provisions for loan losses.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 3

4. Table of contents

We expect excess capital at the parent company to grow significantly over next two

years ....................................................................................................................................5

Realignment of legal entity structure now puts E*TRADE Financial in a position to

return capital to its shareholders........................................................................................5

We expect E*TRADE Financial to grow excess capital meaningfully over the next

two years.............................................................................................................................7

We anticipate earnings to increase significantly with rising interest rates ........................9

Sweep account optimization could lead to accelerated balance sheet growth ...............11

We think that the firm’s $50 billion size limit is increasingly becoming a “soft target”.......14

Bringing back assets held by third-party financial institutions could boost earnings.......14

We are modeling a meaningful improvement in operating margins and cash

generation starting in 2016...............................................................................................15

Items management needs to address over the coming years .............................................20

E*TRADE’s business model is too transactional................................................................20

Balance sheet continues to be the most risky among peers ............................................23

Ban on payment for order flow practices could impact earnings.....................................25

Sharp increase in short-term interest rates could negatively impact the firm given

the duration of its balance sheet ......................................................................................26

Valuation framework .........................................................................................................27

Risks and price target impediments ...................................................................................30

Quick overview of E*TRADE Financial Corp. .......................................................................31

Products.............................................................................................................................33

Revenue break-down .........................................................................................................35

Business segments .............................................................................................................39

Products.............................................................................................................................40

Distribution ........................................................................................................................41

Competitors .......................................................................................................................42

History................................................................................................................................43

Management team.............................................................................................................44

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 4

5. We expect excess capital at the parent company to grow significantly over

next two years

Realignment of legal entity structure now puts E*TRADE

Financial in a position to return capital to its shareholders

We believe that the recent regulatory approval to realign E*TRADE Financial Corporation’s

legal entities puts the firm in a situation to buy back shares in 2015. We are estimating that

the firm could repurchase shares worth approximately $40 million in 2015 and $200 million

in 2016.

In 2009, E*TRADE Financial was required to move its introducing broker–dealer entity

(E*TRADE Securities) under E*TRADE Bank at the request of its regulators where the firm’s

clearing broker–dealer (E*TRADE Clearing) was already residing. Consequently, the company

turned both broker–dealers into a subsidiary of E*TRADE Bank as part of an attempt to

strengthen the bank’s capital. Under this structure, management had to get approval from its

regulators before it was able to “dividend-up” any excess capital to the parent company.

More recently, the firm proposed a new “simplified” structure to its regulators in order to

create a direct source of capital to the parent. Furthermore, E*TRADE Financial requested

permission to operate its bank at a Tier 1 leverage ratio of 9%. This was a 50 basis points

reduction from its previous target.

The recent regulatory permission to realign its corporate structure and operate the bank at a

lower tier 1 leverage ratio has significant positive implications. Access to excess capital

generated by the broker–dealers has been simplified. The income and capital generated by

the broker–dealers is now housed directly below the parent company. Previously, the

earnings generated by the firm’s broker–dealers were generated within the bank and thus

subject to bank regulatory approvals before any capital could be moved to the parent

company.

The company provided some context on what these changes imply during its 4Q/14 earnings

call. Under the previous structure, E*TRADE Financial was able to pay quarterly dividends of

$75 million in 2014, or $300 million for the entire year. Under the new structure, the firm

would have been able to dividend-up $225 million of earnings from the bank in 2014. In

addition, the broker–dealers would have generated excess capital of about $200 million, for

a total of $425 million for 2014. The chart below shows this:

Exhibit 2: E*TRADE Financial should be able to dividend-up significantly more capital post regulatory approval & realignment

Current structure

2014

E*TRADE Bank

E*TRADE Financial

E*TRADE Securities E*TRADE Clearing

$300M dividends

Proposed new structure

2014 pro forma for realignment

E*TRADE Financial

E*TRADE Bank E*TRADE Securities E*TRADE Clearing

$225M dividends $200M dividends

Source: Company reports; RBC Capital Markets

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 5

6. The company indicated that it will dividend-up $434 million to the parent company in 1Q/15.

Furthermore, the company will also ask to dividend-up $75 million from the bank in 1Q/15.

Beginning in 2Q/15, it will request the full amount of the previous quarter’s earnings

generated by the bank as dividends.

The company has also provided a timeline for the realignment. E*TRADE Securities is

expected to be moved closer to the parent in early February, while E*TRADE Clearing will be

moved in late 2015. This proposed realignment of legal entities should improve the

company’s liquidity and cash position considerably. The exhibit below shows this.

Exhibit 3: Parent liquidity will be over $500 million post the realignment of entities and

reduction in debt ($M)

$233

$310

$560

$434

$75

( $432 )

$250

$-

$100

$200

$300

$400

$500

$600

$700

$800

4Q/14

Corporate

cash

Legal entity

realignment

Planned Q1

dividend from

bank

Debt

reduction and

refinance

4Q/14 Pro-

forma

corporate cash

Revolver 4Q/14 Pro-

forma parent

liquidity

Source: Company filings; RBC Capital Markets

What are E*TRADE Financial’s options now that it is in a strong position to have access to

excess capital at the parent company? We do not expect the firm to pay dividends in 2015,

nor to pay down more debt. It has now achieved its long-term goal of having $1 billion of

debt outstanding. We believe that the incremental benefits of reducing debt would be small

from here on as the debt burden is manageable. The firm’s stated target is to hold a

minimum of twice the annual debt service. Applying a weighted average cost of debt of 5.0%,

we arrive at a minimum cash balance of $100 million.

Clearly, E*TRADE Financial will enjoy some financial flexibility following the realignment of its

legal entities and the reduction in debt burden. We believe that there are three likely options

to deploy excess capital, namely buying back shares, reducing wholesale financing needs,

and growing the firm’s balance sheet. The company’s capital plan could include a

combination of all of the above. After all, we do not believe that the current shareholder

base invested in E*TRADE is expecting dividend payments. Thus, we would not expect

current shareholders to be disappointed should E*TRADE choose a different mode of

creating shareholder value.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 6

7. We expect E*TRADE Financial to grow excess capital

meaningfully over the next two years

We believe that excess capital could reach $2 billion, as the company reduces its bank’s

targeted Tier 1 leverage ratio to 8 percent and phases in Basel III. In addition, FDIC

expenses could potentially decline due to management’s efforts to reduce debt and de-risk

the loan portfolio.

A) We anticipate earnings growth to add approximately $1.2 billion to excess

capital at the parent company over the next two years

Assuming that we are correct with our $550 million of excess capital generation figure for

2015, excess capital could stand at $810 million by the end of this year. Assuming that net

income grows another 18% in 2016, excess capital could stand at $1.4 billion should

E*TRADE Financial’s management decide not to return capital to its shareholders over the

next two years. This scenario assumes that the firm will incur $50 million of interest expense

on its debt each year and that it will not deploy excess capital for share buybacks or pay

dividends.

Exhibit 4: Excess capital could grow to $1.4 billion by 2016 ($ in million)

$310

$810

$1,410

$1,660

$550

$50

$650

$50

$250

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

4Q/14 Pro-

forma

corporate

cash

2015

Excess

capital

generated

2015 int.

expense

4Q/15 pro-

forma

excess

capital

2016

Excess

capital

generated

2016 int.

expense

4Q/16 pro-

forma

excess

capital

Revolver Pro-forma

parent

liquidity

Source: Company filings; RBC Capital Markets

However, there are additional factors beyond earnings growth that could add to excess

capital.

B) We believe that phasing-in Basel III and reducing the bank’s targeted Tier 1

leverage ratio could add another $432 million to $599 million to excess capital

over time

The table below shows E*TRADE Bank’s pro-forma Tier 1 leverage ratio assuming that the

broker–dealers had been moved from below the bank at the end of the December quarter.

The ratio also reflects a dividend payment of $75 million to the parent company, which is

scheduled for 1Q/15. Thus, the resulting pro-forma leverage ratio of 9% would be in line with

the firm’s current target of running the bank at a Tier 1 leverage ratio of 9%. Were we to

include the deferred tax assets that are currently not being accounted for in Tier 1 capital,

we would estimate the Tier 1 leverage ratio to be 9.8% under Basel III. This provides the firm

with incremental excess capital. Moreover, we would expect excess capital to increase

further, as E*TRADE Financial approaches its target of operating at a Tier 1 leverage ratio of

8% by 2016. The table below shows our calculation.

Excess capital could grow

to $1.4 billion over the next

two years

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 7

8. Exhibit 5: We think phasing in Basel III and reducing the firm’s Tier 1 leverage ratio target to 8% could add about $599 million to

excess capital

($ in million)

E*TRADE

Bank

E*TRADE

Securities

E*TRADE

Clearing

Pro-forma

Bank

Pro-forma

for 1Q/15

div.

Basel III DTA

adjustment

Pro-forma

Bank

Tier 1 capital $4,548 ($625) ($883) $3,040 $2,965 +$300 $3,265

Tier 1 assets $42,876 ($743) ($9,031) $33,102 $33,027 +$300 $33,327

Tier 1 leverage ratio 10.6% 84.1% 9.8% 9.2% 9.0% 9.8%

Excess capital at targeted:

Tier 1 leverage ratio 8.5% $158 $432

Tier 1 leverage ratio 8.0% $323 $599

Source: Company filings; RBC Capital Markets estimates

The management team indicated that it would like to run the bank at a targeted Tier 1

leverage ratio of 8% over the next two years. Thus, we would expect this to add about $323

million to excess capital, which could be streamed-up to the parent company with the

approval of the bank’s regulator. Furthermore, we would expect the addition of deferred tax

assets in the definition of Tier 1 capital under Basel III to add another $300 million to excess

capital. Thus, at a Tier 1 leverage ratio of 8%, the bank’s excess capital would grow to $599

million without the firm having to grow its balance sheet. Consequently, with the approval of

OCC, we would expect the parent company’s liquidity position to grow by an incremental

$599 million excluding the impact of earnings. Combining this with our earnings growth

estimate, we would expect excess capital to grow to approximately $2.0 billion.

C) Reduction in FDIC charges could add further to excess capital

The company is clearly in a better position to utilize its excess capital after its regulators gave

the management team their seal of approval to move the broker–dealers closer to the

parent company. Having de-levered the balance sheet further in March and with continued

de-risking of its loan portfolio, one could expect Federal Deposit Insurance Corporation

(FDIC) insurance expenses to decline. The firm provided its own internal model during a

recent presentation. Management assumed that it could reduce FDIC charges from about 19

basis points today to around 11 basis points over time. The lower FDIC premium would

translate into savings of about $35 million on a pre-tax basis ($22 million after tax). This

would equate to 7 cents per diluted share based on 2014 assets and a 38% tax rate.

Overall, the company seems to be in a solid capital position. We believe that the Fed could

have a more favorable view of the company post management’s strong execution on its

capital plan. We believe that implementation of Basel III could provide management with

additional capital buffer. We show this below. On a consolidated basis, we estimate that Tier

1 leverage ratio would have increased by 90 basis points under Basel III had the company

removed 75% of its trust preferred securities from and added about $718 million of deferred

tax assets to the definition of Tier 1 capital.

E*TRADE could add 7 cents

to earnings and $22m to

excess capital were the

firm to be successful in

reducing FDIC expenses

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 8

9. Exhibit 6: Tier 1 leverage ratio would have been 8.9% phasing out 75% of trust preferred

securities

Consolidated

($ in million) Reported TRUPs DTA Pro-Forma

Tier 1 capital $3,463 ($325) $651 $3,789

Tier 1 assets $42,845 ($325) $651 $42,520

Tier 1 leverage ratio 8.1% 8.9%

TRUPs 75% phased out

Source: RBC Capital Markets estimates

Were the company to phase out 100% of the trust preferred securities right away, Tier 1

leverage ratio would increase by 60 basis points. However, the company is required to phase

out 75% of the trust preferred securities in 2015 and the remaining 25% in 2016. Thus, we

would expect the firm to generate additional capital, which would add to the above

estimates.

Exhibit 7: Tier 1 leverage ratio would have been 8.7% phasing out 100% of trust preferred

securities

Consolidated

($ in million) Reported TRUPs DTA Pro-Forma

Tier 1 capital $3,463 ($433) $651 $3,681

Tier 1 assets $42,845 ($433) $651 $42,412

Tier 1 leverage ratio 8.1% 8.7%

TRUPs 100% phased out

Source: RBC Capital Markets estimates

Our key point is this: E*TRADE Financial seems well capitalized. The management team will

have to think hard about how to unlock value over the coming quarters and years. Options

include paying dividends, buying back shares, growing the balance sheet, or running off

legacy assets at an accelerated rate. We believe that any of these options could be a catalyst

for E*TRADE’s shares. We would rank addressing legacy issues and buybacks a top priority.

While we have demonstrated that excess capital at the parent company will increase

meaningfully, we also need to address why we believe that E*TRADE Financial could

generate earnings growth in excess of consensus figures. We show this below.

We anticipate earnings to increase significantly with rising

interest rates

E*TRADE Financial’s earnings could increase by about 24 cents (or 21% based on 2014

earnings) for a 50 basis point move in interest rates.

While not as asset sensitive as Charles Schwab, E*TRADE Financial is nonetheless

meaningfully asset sensitive. We estimate that a 50 basis points increase in interest rates

could add about $0.24 to earnings. This would be 21% accretive to normalized earnings of

$1.12 per share, which the company reported in 2014. As a comparison, we estimate that

Charles Schwab’s 2014 earnings per share would have been 33% higher, and TD Ameritrade’s

2014 earnings about 9% higher had we had higher interest rates.

This should not come as a surprise as the largest component of the firm’s net revenues is

spread-based revenues. The exhibit below provides a revenue bridge for 2014.

We estimate a pro-forma

Tier 1 leverage ratio of 9%

post implementation of

Basel III guidelines

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 9

10. Exhibit 8: Spread-based revenues comprised 60% of total net revenues in 2014 ($M)

$456

$1,814

$1,088

$186

$84

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Commission

revenues

Spread revenues Fee revenues Other Total net revenue

Source: Company filings; RBC Capital Markets

Given the firm’s large dependency on interest-earning assets in order to generate revenues,

one would expect E*TRADE Financial to be the most interest rate sensitive among its peers.

However, this does not seem to be the case. One reason for this could be that the company

has hedged its interest rate sensitivity. Over time, management could decide to roll off these

hedges as interest rates start rising.

While E*TRADE Financial does not provide its own sensitivity to interest rates, we believe

that we were able to come up with a workable approach. We have arrived at our conclusion

using the company’s financial model as presented during a competitor’s conference earlier

this year. E*TRADE Financial provided an estimate of the impact of lower interest rates on its

revenues. The company pointed out that revenues would have been higher to the tune of

$182 million based on its 2014 balance sheet had net interest spreads been 300 basis points.

This is what the company would expect net interest margins to be in a normalized rate

environment.

As a reference, net interest margins were 255 basis points in 2014. Thus, the company’s

model would imply that a 45 basis points rise in net interest margins would impact net

revenues by the aforementioned $182 million. Consequently, it appears that each basis point

increase in net interest margin would result in a $4 million boost to net interest revenues.

We then tried to figure out what by how much net interest margins would expand for a 50

basis point move in interest rates. Looking at historical data, we estimated that funding costs

would increase by about 12 basis points should interest-earning yields improve by 50 basis

points. Consequently, we would expect an increase in interest rates of 50 basis points to

impact net interest margins by 38 basis points.

A 38 basis points expansion in net interest margins would result in incremental net interest

income revenue of $153 million. The next point is up for debate. We assumed an incremental

margin of 75% on these earnings, similar to our approach for its peers. We then arrived at

the EPS impact by using a 38% tax rate and 294 million of diluted shares.

The exhibit below provides a sensitivity table showing the impact on EPS using various

assumptions for interest rate movements and pre-tax margins.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 10

11. Exhibit 9: We estimate that a 50 bps move in interest rates would impact EPS by about 24 cents

40 43 45 48 50 53 55

40.0% $0.10 $0.11 $0.12 $0.12 $0.13 $0.14 $0.14

42.5% $0.11 $0.12 $0.12 $0.13 $0.14 $0.14 $0.15

45.0% $0.12 $0.12 $0.13 $0.14 $0.15 $0.15 $0.16

47.5% $0.12 $0.13 $0.14 $0.15 $0.15 $0.16 $0.17

50.0% $0.13 $0.14 $0.15 $0.15 $0.16 $0.17 $0.18

52.5% $0.14 $0.14 $0.15 $0.16 $0.17 $0.18 $0.19

55.0% $0.14 $0.15 $0.16 $0.17 $0.18 $0.19 $0.20

57.5% $0.15 $0.16 $0.17 $0.18 $0.19 $0.20 $0.20

60.0% $0.16 $0.17 $0.17 $0.18 $0.19 $0.20 $0.21

62.5% $0.16 $0.17 $0.18 $0.19 $0.20 $0.21 $0.22

65.0% $0.17 $0.18 $0.19 $0.20 $0.21 $0.22 $0.23

67.5% $0.17 $0.19 $0.20 $0.21 $0.22 $0.23 $0.24

70.0% $0.18 $0.19 $0.20 $0.22 $0.23 $0.24 $0.25

72.5% $0.19 $0.20 $0.21 $0.22 $0.23 $0.25 $0.26

75.0% $0.19 $0.21 $0.22 $0.23 $0.24 $0.26 $0.27

77.5% $0.20 $0.21 $0.23 $0.24 $0.25 $0.26 $0.28

Move in interest rates (bps)

Assumedincrementalmargins

Source: RBC Capital Markets estimates

Thus, we would expect a move of 50 basis points in interest rates to impact earnings by

about 24 cents (21% of normalized 2014 EPS). As a comparison, we estimated an impact of

31 cents on EPS for Charles Schwab (or 33% of 2014 EPS) and about 12 cents to 14 cents at

TD Ameritrade (9% of 2014 EPS using midpoint).

As mentioned earlier, we believe that the company has taken a defensive posture and

hedged its interest rate exposure meaningfully, which contributes to the current asset

sensitivity. This would make sense as its regulators need to be comfortable about the firm’s

risk profile in order to allow it to move up its broker–dealers, which have been a “source of

strength” post the financial crisis. Furthermore, the firm’s balance sheet has a three-year

duration. This compares to about two years for TD Ameritrade and Charles Schwab. This

longer duration would impact the company more than its peers if interest rates increased

sharply. Thus, hedging the company from sudden moves in interest rates is the prudent thing

to do as net interest margins could decline were funding costs to re-price faster than the

yield on the firm’s investment portfolio.

However, there is the possibility that the firm’s interest rate sensitivity could increase above

our expectation as the firm’s capital position strengthens and management decides not to

roll over all hedges. We view this as an optionality.

Sweep account optimization could lead to accelerated balance

sheet growth

Assuming that E*TRADE Financial holds an incremental $3 billion of assets on its balance

sheet and earns a 200 basis point spread, we would expect net operating income to

increase by about $60 million (or 5 cents per share).

Currently, E*TRADE Financial’s management team has set itself a limit of keeping the firm’s

balance sheet below $50 billion. The goal is to avoid additional regulatory burdens. E*TRADE

Financial’s balance sheet is currently at $45.5 billion. Considering that it needs to hold a

buffer to avoid crossing the $50 billion mark, we think that balance sheet growth would have

to be decelerated significantly once the firm gets to the $48 billion range. We believe that

We expect EPS to be

impacted by about 24 cents

based on a 50 basis points

movement in interest rates

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 11

12. the firm would have to maintain a buffer in order not to exceed the $50 billion target. Our

call is that there will not be a need for a large buffer once the firm has optimized its sweep

account processes over the coming months. We think that management will provide its

treasury function with additional flexibility and allow it to nightly move its clients’ assets

quickly to and from third-party financial institutions. This will add to balance sheet growth

and earnings.

Today, E*TRADE Financial is forced to route client cash to third-party financial institutions if

assets on its balance sheet approach a certain level. Whereas cash can be swept overnight to

third-party financial institutions, it can take E*TRADE Financial several months before it gains

access to this capital given the current structure. It is difficult to maximize profits under

today’s structure as the firm needs to maintain a sufficient buffer for unforeseen growth in

the balance sheet.

Consider this: While adding clients could lead to growth, there are other reasons beyond

client growth that could result in a larger balance sheet. For instance, the balance sheet

could grow as consumer engagement declines. Here is why: If customers reduced their

market engagement, buying fewer shares, and keeping their assets in cash and cash

equivalents, then the balance sheet grows. This poses a real risk to the company’s target of

limiting the size of its balance sheet. This is not a hypothetical, but real risk. The firm

disclosed for its fiscal year 2014 that net buying activity was $7.7 billion. Management

estimates normalized levels to be in the $2 billion to $3 billion range. Thus, the balance sheet

could grow by $4 billion to $5 billion if clients decided to reduce their equity market

exposure.

The exhibit below shows assets held by these third parties, i.e., outside of E*TRADE Financial.

These include money market funds and sweep deposit accounts at unaffiliated financial

institutions. Were these assets included on the company’s balance sheet, it would be safe to

assume that E*TRADE Financial would have to comply with additional regulatory burdens,

given that its own balance sheet is about $45.5 billion—excluding $15 billion of assets held

by third parties.

Exhibit 10: Assets held by unaffiliated financial institutions have grown to over $15 billion

$-

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Source: Company filings; RBC Capital Markets

While there still will be a need to sweep money to third parties in the near term, we believe

that E*TRADE Financial should be able to approach the $50 billion limit once it has optimized

its sweep account procedures without the risk of exceeding this size limit.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 12

13. The impact of increasing its balance sheet on revenues should not be ignored. Assuming that

E*TRADE Financial could hold an incremental $3 billion of assets on its balance sheet and

earn spread of 200 basis points, we would expect net operating interest income to increase

by about $60 million. Assuming a 40% margin and a 38% tax rate, we estimate earnings could

increase by 5 cents per share by optimizing sweep account procedures. The exhibit below

provides a sensitivity analysis.

Exhibit 11: Adding $3 billion to interest-earning assets could increase EPS by 5 cents

25% 30% 35% 40% 45% 50%

150 $0.02 $0.03 $0.03 $0.04 $0.04 $0.05

175 $0.03 $0.03 $0.04 $0.04 $0.05 $0.06

200 $0.03 $0.04 $0.04 $0.05 $0.06 $0.06

225 $0.04 $0.04 $0.05 $0.06 $0.06 $0.07

250 $0.04 $0.05 $0.06 $0.06 $0.07 $0.08

275 $0.04 $0.05 $0.06 $0.07 $0.08 $0.09

300 $0.05 $0.06 $0.07 $0.08 $0.09 $0.09

325 $0.05 $0.06 $0.07 $0.08 $0.09 $0.10

Pre-tax margins

Interestspreads(bps)

Source: RBC Capital Markets estimates

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 13

14. We think that the firm’s $50 billion size limit is increasingly becoming a “soft

target”

Bringing back assets held by third-party financial institutions

could boost earnings

Management’s current limit on the balance sheet size is not sustainable over time, as we

expect the opportunity cost to increase with rising interest rates. Furthermore, there seems

to be growing support to reconsider the $50 billion bright line test to be considered

systemically important. We estimate that earnings could increase by 16 cents were the

company to move assets held by third-party financial institutions on its balance sheet

today.

We think that the $50 billion threshold to be considered a systemically important financial

institution could potentially change. There seems to be growing bipartisan support to

reconsider this bright line $50 billion assets test. The threshold for triggering systemic risk

worthy of enhanced prudential standards could be lifted to a higher number such as $100

billion or $200 billion. This could be combined with qualitative assessments of risk. The

Bipartisan Policy Center, a non-profit organization focused on promoting bipartisan

solutions, has endorsed a hybrid approach that would raise the threshold to $250 billion. It

would also establish more of a “dashed line” versus the brightline-test that would give

regulators discretion to add firms based on risk factors other than size and exclude business

deemed less systemically imporantant. Former Rep. Barney Frank, D-Mass., a key author of

the financial reform law, also testified before the House banking panel in July that lawmakers

should revisit the $50 billion threshold. Several other regulators, including Federal Reserve

Gov. Daniel Tarullo and Comptroller of the Curry Thomas Curry, have made similar

statements.

Here we provide a sensitivity analysis around incremental earnings potential.

Bringing back assets held by third-party financial institutions could boost earnings

It should not come as a surprise that E*TRADE Financial’s decision to sweep client assets to

third-party financial institutions costs the firm a significant amount of earnings. The firm

reported earnings of only $14 million in 2014 on assets held by these third-party institutions.

We estimate that the average assets routed off the balance sheet were approximately $14.5

billion, resulting in a meager 10 basis points yield on these assets. As a comparison, E*TRADE

Finanical’s net interest margins were 255 basis points in 2014. Thus, the decision to have

third parties manage clients’ assets costs the firm $236 million in incremental revenues.

Assuming that one-third of the assets are in money market funds earning 10 basis points and

a 254 basis points net interest margin on the remaining assets, plus a 25% pre-tax margin, a

38% tax rate, and 294.1 million shares outstanding, earnings per diluted share could have

been 13 cents higher than the $1.00 reported for 2014 were the company not forced to

route cash to unaffiliated financial institutions. We should note that the above calculation

does not assume that assets are being brought back today, but is intended to provide a

“what if” analysis. Certainly, new investment rates would be around 200 basis points today.

At 200 basis points and 40% of incremental pre-tax margins, EPS would have been 16 cents

higher. The table below provides various scenarios.

We estimate that

managing client assets on

its balance sheet would

have been 12% accretive to

2014 earnings

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 14

15. Exhibit 12: At an incremental margin of 40% and 200 bps of net interest margin, EPS could

have been 16 cents higher

20% 25% 30% 35% 40% 45% 50%

100 $0.04 $0.05 $0.06 $0.07 $0.08 $0.09 $0.10

125 $0.05 $0.06 $0.07 $0.09 $0.10 $0.11 $0.12

150 $0.06 $0.07 $0.09 $0.10 $0.12 $0.13 $0.15

175 $0.07 $0.09 $0.11 $0.12 $0.14 $0.16 $0.18

200 $0.08 $0.10 $0.12 $0.14 $0.16 $0.18 $0.20

225 $0.09 $0.11 $0.14 $0.16 $0.18 $0.21 $0.23

250 $0.10 $0.13 $0.15 $0.18 $0.20 $0.23 $0.26

275 $0.11 $0.14 $0.17 $0.20 $0.23 $0.25 $0.28

300 $0.12 $0.15 $0.19 $0.22 $0.25 $0.28 $0.31

325 $0.13 $0.17 $0.20 $0.23 $0.27 $0.30 $0.34

Pre-tax margins

Interestspreads(bps)

Source: RBC Capital Markets estimates

There is more. Assets held by third parties have grown at a compound average growth rate

of 46% over the past four years. This growth rate has declined to 12.3% year over year in

2014. Assuming that assets continue to grow at 12.3% over the next three years, those could

reach $22 billion by 2017. Were we correct with our pre-tax margin projection of 40% by

2017 and assuming net interest spread assumption of 275 basis points (or 24 basis points

below our overall portfolio yield projection for 2017) , earnings per share would be lifted by

36 cents by managing these client assets on the E*TRADE Financial’s balance sheet instead.

To us, this pickup in earnings seems compelling and we believe that management will have

to ponder whether the opportunity cost incurred justifies trying to avoid incremental

regulatory scrutiny.

We do believe that the firm has the compliance and regulatory systems already in place to

operate a much larger balance sheet. After all, regulators needed to be comfortable with the

existing enterprise risk management at E*TRADE Financial before allowing the firm to realign

its legal entities. It is just a question of time until the benefits of a larger balance sheet

exceed the incremental cost associated with having to comply with modified liquidity

coverage ratio requirements. We believe that management could make a decision relatively

quickly once interest rates start rising.

We are modeling a meaningful improvement in operating

margins and cash generation starting in 2016

We believe that there are encouraging signs that management will grow its balance sheet

beyond $50 billion, resulting in operating leverage and margin expansion.

We have already seen a significant improvement in operating margins and cash generation

since Mr. Paul T. Idzik was appointed CEO on January 17, 2013, joining E*TRADE Financial

after having worked as Group Chief Executive of DTZ Holdings PLC in London and having

served 10 years at Barclays PLC.

While one could argue that all discount brokers have benefited from improving margins, we

would point out that margin expansion was not simply a case of the “tide lifting all the

boats”. In fact, E*TRADE Financial’s management team has been working hard on its

turnaround story. The exhibit below shows the improvement in the firm’s opreating margins

and cash generation capacity. We use the EBITDA to net revenues ratio as a proxy for cash

generation.

Having gone through a

number of changes at the

top level, we believe that

the current E*TRADE

management team has the

needed qualities to

position the firm for

growth over time

Were the company to

deploy $14.5 billion of

client assets at a 200 basis

points yield today, we

would expect EPS to

increase by 16 cents

assuming 40% incremental

margins on these earnings

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 15

16. Our call is that we are not done yet and could see continued improvement over the next

three years.

Exhibit 13: Operating margins have been expanding significantly since 2013

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2010 2011 2012 2013 2014 2015E 2016E 2017E

AMTD SCHW ETFC

Source: Company filings; RBC Capital Markets estimates

In fact, we belive that E*TRADE Finanical could add 7.9 percentage points to its pre-tax

operating margin from 2014 to 2017. This, in turn, would improve the company’s ability to

generate excess capital. The exhibit below depicts the EBITDA to revenue ratio over time.

Exhibit 14: E*TRADE Financial has improved its EBITDA/revenue ratios meaningfully

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 2015E 2016E 2017E

AMTD SCHW ETFC

Source: Company filings; RBC Capital Markets estimates

We believe that there are encouraging signs that management will grow its balance sheet,

resulting in operating leverage. Management has done a remarkable job de-risking its loan

EBITDA to total net

revenues has improved

significantly at E*TRADE

since 2012

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 16

17. portfolio and de-levering the balance sheet. This in turn, has resulted in fewer clients leaving

E*TRADE Financial. In fact, client attrition has declined significantly over time. This positions

the firm for growth. The next two sub-sections provide specifics on what the management

team has done to make E*TRADE Financial a better fiduciary of its clients’ capital.

Management de-risked its loan portfolio

The company has been continuously reducing the risk embedded in the loan portfolio. The

firm had about $6.4 billion of gross loan receivables as of 4Q/14. This was comprised of $3.1

billion in one- to four-family home loans, $2.8 billion of home equity loans, and $461 million

of consumer and other loans. This compares to a loan portfolio of $2.7 billion of consumer

loans, $16.9 billion of one- to four-family home loans, and $12.4 billion of home equity loans

as of 3Q/07. In addition, there were about $17 billion of securities on its balance sheet

including MBS securities, bonds, and asset-backed securities that management had to

address.

The exhibit below shows the progress the company has made. The chart depicts delinquent

loans as a percentage of total gross loans. Clearly, the trend has been improving since 2010.

Exhibit 15: Delinquent loans as % of gross loans have been declining since 2010

0%

2%

4%

6%

8%

10%

12%

14%

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

Source: Company filings; RBC Capital Markets

A slow but steady ecomomic recovery in combination with better risk management has

helped the firm improve the performance of its loan portfolio. In order to test how well

management had anticipated expected losses, and more importantly, reserved for it, we

aggregated the charge-offs for four quarters and compared the result to the beginning

allowance for loan losses at the start of the four-quarter period (Exhibit 16). While

management had to set up large provisions for loan losses in 2009, it seems that it had built

enough cushion to absorb losses starting in 2013. In fact, E*TRADE Financial started releasing

some provisions it had set up for its one- to four-family home loan portfolio over the past

eight quarters.

E*TRADE’s loan portfolio of

$32 billion in 2007, has

been reduced to its current

size and risk of about $6.4

billion of gross loans

outstanding

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 17

18. Exhibit 16: Provisions for loan losses have stabilized starting in 2014

0%

50%

100%

150%

200%

250%

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

One-to-four-family Home equity Consumer and other

Source: Company filings; RBC Capital Markets

Consequently, the firm has regained the trust of clients such that client attrition has declined

to historical levels.

Client attrition rate has declined significantly

The company’s efforts to strengthen its capital position and reduce the risk of its investment

portfolio is yielding results, positioning the firm to grow client accounts and its balance

sheet. It is undeniable that management has been able to restore confidence after the

events of 2007. The exhibit below shows the decline in the attrition rate for the period from

2008 to 2014. Clearly, the trend has been positive.

Exhibit 17: Fewer clients are leaving E*TRADE today than in the past

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2008 2009 2010 2011 2012 2013 2014

Source: Company filings; RBC Capital Markets

The attrition rate, which the company defines as closed accounts as a percentage of previous

quarter’s total brokerage accounts, has declined from 16.9% in 2008 to 8.7% as of 2014.

Consequently, the firm was able to grow the total number of accounts starting in 2011.

Client attrition has declined

from 16.9% in 2008 to 8.7%

as of 2014

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 18

19. Exhibit 18: Total account growth commenced in 2011

3,900,000

4,000,000

4,100,000

4,200,000

4,300,000

4,400,000

4,500,000

4,600,000

4,700,000

4,800,000

4,900,000

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

Source: Company filings; RBC Capital Markets

This bodes well for revenue growth as we expect the firm to continue to add to its client

base—as long as the number of gross new brokerage accounts exceeds closures. This seems

to be the case since 2011.

Exhibit 19: E*TRADE Financial added 155,981 net new client accounts in 2014

28,439

(213,903)

69,162

163,063

133,713

155,981

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

0

50,000

100,000

150,000

200,000

2009 2010 2011 2012 2013 2014

Source: Company filings; RBC Capital Markets

Net new brokerage accounts were the main contributors to total net new accounts in 2014,

with net new stock plans and net new banking accounts contributing marginally to growth. In

fact, net new brokerage accounts of 146,000 in 2014 was the highest addition in over a

decade at E*TRADE Financial. It seems that management has been able to restore confidence

among retail clients, as it is able to retain more existing clients while adding new accounts.

The improvement we have seen in fixing the business and being able to add to the client

base gives us confidence that E*TRADE Financial will be able to grow its assets. We would

argue that balance sheet growth could accelerate once the management team determines

that the limit on its balance sheet size of $50 billion is too costly to maintain. We expect the

opportunity cost to do so to increase with higher interest rates.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 19

20. Items management needs to address over the coming years

E*TRADE’s business model is too transactional

We believe that the firm might not able to participate in certain growth opportunities

including growth in independent RIAs as management has been too focused on fixing

legacy issues.

While E*TRADE Financial has done a great job restructuring its balance sheet and

repositioning the firm for growth, we are concerned that the business model has not

changed much. Rather, the management team has focused on unwinding the errors made by

the previous management teams and refocusing on its core franchise—which has been

providing the best trading platform for its retail client. The exhibit below shows the firm’s

product offerings versus peers.

Exhibit 20: ETFC’s product offering is limited versus peers

ETFC AMTD SCHW

Brokerage

Full range of investment products

Third-party research

In-house research

Mutual funds

Proprietary funds

Third-party funds

Exchange Traded Funds

Proprietary funds

Third-party funds

Advice - In-House

Investment advice

Tailored portfolio construction

Portfolio management

Separately managed accounts

Financial consultants 300 ~700 1,200

RIA relationships ~5,000 7,000

Number of branches 30 105 300+

Corporate services

Retirement plans (401k)

Equity compensation plans

Banking services

Full service bank

Trust services

Custody services

Administrative trustee services

Average retail client assets -estimate $65,000 $100,000 $250,000

Average age of retail client Mid 40s Mid 40s Mid 50s

Source: Company reports; RBC Capital Markets

E*TRADE’s competitors

have taken advantage of

regulatory limitations on

its growth and

management’s decision to

refocus on its core

franchise

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 20

21. Still, there have simply been too many fires to fight, which in our view, might have put the

firm at a competitive disadvantage versus its peers. The firm has not been able to expand its

product offering to the same degree as its competitors. The management team did the best

it could given the opportunity set. One can assume that its regulators would not have been

approachable had the management team been discussing paths to aggressively grow its

business. The firm missed opportunities to grow and keep up with its evolving competitors

while it was fully engaged with its regulators.

The exhibit below shows the average organic growth rate for client assets, growth in average

fee based investment assets, and growth in interest-earning assets. While E*TRADE Financial

was able to add to its client assets, we estimate that the average organic growth rate to be

the lowest with 4.6%. This compares with 5.1% for Charles Schwab, and 10.5% for TD

Ameritrade. As for interest rate sensitive assets, there has been a decline in average interest-

earning assets since 2009. The firm’s peers grew their assets at a compounded annual

growth rate of 16% to 17% since 2009.

Exhibit 21: ETFC’s five-year compound annual growth rate versus peers (2009 to 2014)

5%

11%

5%

24%

20%

n/m

16% 17%

-2%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

SCHW AMTD ETFC

Client assets organic growth Avg. fee based investment balances Avg. Interest rate sensitive assets

Source: Company filings; RBC Capital Markets

Looking at the data over a three-year period, we come to a similar conclusion. The average

organic growth rate for client assets is 4.2%, which is lower than over the five-year period. As

for interest rate sensitive assets, the firm has slowed down running off its balance sheet.

However, growth remained negative to the tune of 1.4% over the past three years.

E*TRADE seems to have fallen behind while its peers have evolved. A good example would

be TD Ameritrade. The firm’s effort to build out its RIA network and capitalize on the

“breakaway advisor” trend is paying dividends, in our view. While still lagging Charles

Schwab, we have seen a tremendous effort and some success in closing the gap. Charles

Schwab, on the other hand, has now evolved to a full-service brokerage firm.

Our point is this: E*TRADE Financial’s business model is too transactional. Certainly, the firm

has grown its corporate services business. At the end of 2009, there were about 1 million

stock plan accounts. This number increased to approximately 1.3 million by the end of 2014.

However, there has been a slowdown in growth, as evidenced by net new accounts added.

The exhibit below shows this. The decline could be due to mergers or an attempt to focus on

more profitable segments of the market. However, a decline of over 50 percent is material

and difficult to ignore.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 21

22. Exhibit 22: Net new stock plan account growth has been declining since 2012

7,083

22,711 21,890

77,180

71,979

28,407

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2009 2010 2011 2012 2013 2014

Source: Company filings; RBC Capital Markets

Given a lack of growth, it should not come as a surprise that the company’s revenue mix is

not as diversified as that of its peers. Spread-based revenues are the major contributor to

net revenues. Unlike its competitors, the firm has not grown its fee-based revenue stream.

Based on the competitive landscape as of today, we believe that—absent of any

acquisition—it will be difficult for the firm to catch up to its competitors if it attempted to

transition to an asset gathering business model. Thus, we would expect the firm to continue

to rely heavily on its balance sheet and commission revenues to grow the top line.

Exhibit 23: Spread-based revenues contribute about 60% to net revenues (2014)

15%

43%

25%

38%

19% 60%

42%

36%

10%

6% 2% 5%

0%

20%

40%

60%

80%

100%

120%

SCHW AMTD ETFC

Commission revenues Spread revenues Fee revenues Other

Source: Company filings; RBC Capital Markets

Revenues will be significantly impacted by the company’s ability to grow its interest-earning

assets. While we believe that the firm will be able to grow its balance sheet, a lack of growth

in interest-earning assets could lead to earnings growth below our expectation.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 22

23. Balance sheet continues to be the most risky among peers

While HELOC provisions seem adequate, investors need to be cognizant of the fact that

there are about $3.2 billion of loans that will convert from interest only to amortizing

loans, and that provisions for 1- to 4-family home loans have declined to $27 million. We

would expect an increase in loan loss provisions over the coming years.

While E*TRADE Financial has done a tremendous job in reducing its risk exposure, there is

still significantly more risk associated with investing in the company’s shares versus that of its

peers.

Consider this: The loan portfolio was at $32 billion at its height. Today, this portfolio has

been reduced to about $6.4 billion, and the quality of its loans has improved. Provisions for

loan losses of $36 million in 2014 were down 75% relative to 2013.

However, the company has still not turned the corner in our view. As the company pointed

out, it believes that provision for loan losses will remain in the $10–$30 million range per

quarter in 2015 and 2016. It expects the provisions to be at the lower end of that range in

2015, and at the higher end of the range of 2016. So, what is happening?

There are about $3.1 billion of one- to four-family home loans and $2.8 billion of home

equity loans on E*TRADE Financial’s balance sheet. About 42% of the one- to four-family

home loans are going to convert from interest only to amortizing loans, while this ratio will

be 68% for home equity line of credit loans (HELOC). The exhibit below shows the timing and

amount of loan balances that are going to convert.

Exhibit 24: A total of $3.2 billion of loans will convert from interest only to amortizing loans

over the next three years ($ in billion)

$0.8

$0.1 $0.1

$0.5

$0.7

$0.2

$0.1

$0.6

$1.0

$0.3

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

2013 and priod 2014 2015 2016 2017

1-4 family I/O to amortizing conversions HELOC I/O to amortizing conversions

Source: Company filings; RBC Capital Markets

What is going to happen is that borrowers will move from paying a minimum monthly

payment to paying based on a loan amortization schedule, which should increase the

amount paid by the borrowers. Certainly, some of the borrowers have already started paying

principal voluntarily. The company reported that 15% of the one- to four-family home

borrowers paid back at least $2,500 in principal during 2014, while 6% reduced their

principal amount by at least $10,000. These are positive developments. However, the

average loan size is $496,000. As for the HELOC portfolio, 38% of borrowers have returned at

Management expects

provisions for loan losses

to be in the $10 million to

$30 million per quarter

range.

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 23

24. least $500 of the principal while 17% have returned at least $2,500. Again, the average loan

amount of $73,000 is meaningful.

It is difficult to forecast potential loan losses over the next three years. Our point is that

investors should consider this risk. It appears that E*TRADE Financial has been strengthening

its allowance for loan losses for HELOC loans, but has been reducing it for one- to four-family

home loans. The exhibit below shows this.

Exhibit 25: Company expects increasing losses on HELOC loans, but lower losses on the one-

to four-family home loan portfolio (allowance for loan losses as % of outstanding balances)

0%

2%

4%

6%

8%

10%

12%

14%

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

One-to-four-family Home equity

Source: Company filings; RBC Capital Markets

There are many variables that could lead to better or worse than expected loan losses. We

believe that the severity and frequency of the losses will be determined by the borrowers’

financial situation, which is a function of the economy.

Certainly, the trend has been good. The exhibit below shows delinquent loans as a

percentage of gross loans receivable. We have seen a decline in total delinquent loans,

especially for one- to four-family home loans.

Exhibit 26: Delinquent loans as percentage of gross loans receivable have been declining

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

One-to-four-family Home equity

Source: Company filings; RBC Capital Markets

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 24

25. Nonetheless, it is difficult to determine whether current reserves will be enough to absorb

future losses. While the firm seems to be adequately reserved for losses on HELOC loans, we

have seen reserve releases from allowances for losses on one- to four-family home loans.

The exhibit below shows the current allowance as a percentage of the balances that are

expected to convert over the next three years.

Exhibit 27: It would take losses of 2.1 percent of the upcoming one- to four-family home loan

conversion balances to wipe out the current allowance

2.1%

19.3%

0%

5%

10%

15%

20%

25%

One-to-four-family Home equity

Source: Company filings; RBC Capital Markets

Ban on payment for order flow practices could impact earnings

While we do not expect a ban on payment for order flow practices, we estimate that an

adverse outcome could impact EPS to the tune of 13 cents.

In order to attract trades, exchanges pay brokers for routing a trade through them. This is

called “payment for order flow”. According to current SEC rules, all that the brokers have to

do now is disclose whether they receive payment for order flows and provide details of this

arrangement.

The Securities and Exchange Commission is currently reviewing whether brokers act in their

clients’ best interest when they “sell the orders” to a trading firm or an exchange for a fee.

While we think that there is a low probability of this changing, the SEC could decide to

eliminate this practice. The UK Financial Conduct Authority has already changed its policies in

2014 and prohibits brokers from taking payments for orders routed to other firms. Their view

is that there is a “clear conflict” of interest caused by these payments.

So far, it does not seem likely that the SEC will follow suite. Mary Jo White, The SEC’s

Chairwoman, said in her market structure reform speech that fees and payments for orders

create a conflict of interest if these payments are not passed through to customers.

However, she did not call for an end of such practices. There is a very high likelihood that the

outcome of the SEC’s inquiry into this topic could simply be better disclosures instead of

banning this practice.

However, if this practice was banned, we believe E*TRADE and TD Ameritrade would be

impacted the most. We estimate that the firm generated about $90 million in order routing

revenues in 2014. This figure compares to about $100 million at Schwab and $300 million at

While “Payment for Order

Flow” is being reviewed by

the SEC, we do not

anticipate an elimination of

these fees, but rather

expect additional

disclosures around fees

E*TRADE Financial Corporation

Brokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; bulent.ozcan@rbccm.com 25

26. TD Ameritrade. While the absolute dollar revenue generated is the lowest among peers, the

impact on EPS in percentage term appears to be the highest. This is how we arrived at our

conclusion:

The firm did not disclose the percentage of its order routing revenues from equity

transactions. We estimate this to be around 70%. As a note, the SEC is not reviewing

transactions in other types of securities. Assuming 70% of the $90 million is from equity

trades, a 100% margin on these revenues, and a 38% tax rate, we estimate that earnings per

share could be impacted to the tune of $0.13. This compares to an estimated impact of $0.17

per share at TD Ameritrade and less than a nickel at Schwab. This calculation is based on an

average share count of 294.1 million diluted shares. To put this figure into perspective, the

firm’s earnings were $1.00 per diluted share in 2014. The exhibit below shows our

calculation.

Exhibit 28: We estimate the impact from a ban on payment for order flow practices to impact

EPS by about 13 cents

($ in million) FY 2014

Order routing revenue $89.0

Assumed equity transactions 70%

Revenues at risk $62.3

Assumed margin 100%

Impact on pre-tax earnings 62.3

Tax rate 38%

Impact on earnings $38.6

Sharecount 294.1

EPS Impact $0.13

Source: RBC Capital Markets estimates