This document summarizes tax issues from 2009, including:

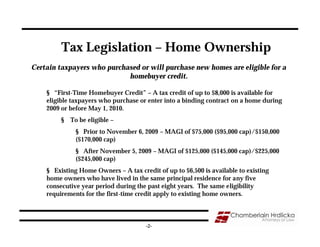

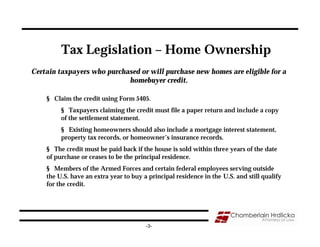

1) Homebuyer tax credits for those who purchased homes in 2009 or 2010, claiming the credit using Form 5405.

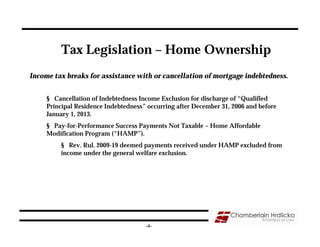

2) Income tax breaks for mortgage assistance/cancellation from 2007-2012 and exclusions for HAMP payments.

3) A sales tax deduction for vehicles purchased in 2009 and exclusions for "Cash for Clunkers" vouchers.

4) Various energy, education, and payroll tax credits, along with IRA and retirement contribution limits.