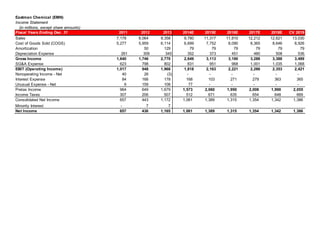

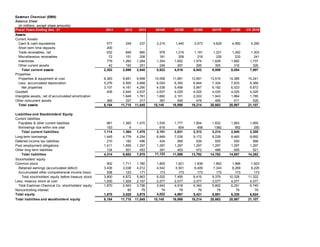

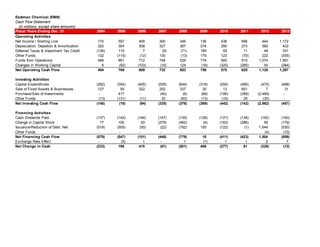

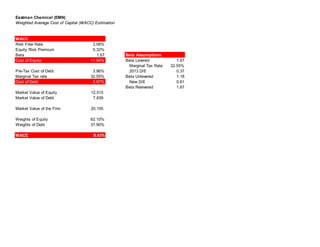

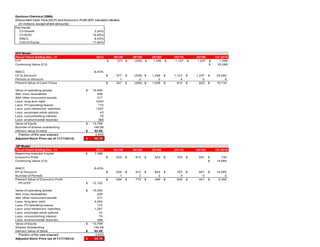

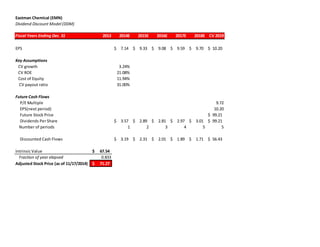

Eastman Chemical Company (EMN) is a global specialty chemicals company that produces advanced materials, chemicals, and fibers found in everyday products. EMN has 45 manufacturing sites in 16 countries and equity interests in joint ventures worldwide. It began as a chemicals supplier to Eastman Kodak in 1920 and became publicly traded in 1993. EMN focuses on shifting its sales towards specialty chemicals for stability as commodity products experience more volatility. Recent acquisitions have expanded EMN's product portfolio and capacity in high-growth markets. EMN is well positioned to acquire Taminco to boost its personal care, coatings, and oil and gas businesses.

![Quarterly_Nov2017_Commodity [Compatibility Mode].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/quarterlynov2017commoditycompatibilitymode-241203221638-fa9bf0f9-thumbnail.jpg?width=640&height=640&fit=bounds)