Biz Outlook for 2013

•

1 like•587 views

Presentation of Jay Penaflor for the WSPH organized 12th HR Learning EB

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Viewers also liked (16)

Similar to Biz Outlook for 2013

Similar to Biz Outlook for 2013 (20)

More from Sonnie Santos

More from Sonnie Santos (16)

Recently uploaded

Recently uploaded (20)

Biz Outlook for 2013

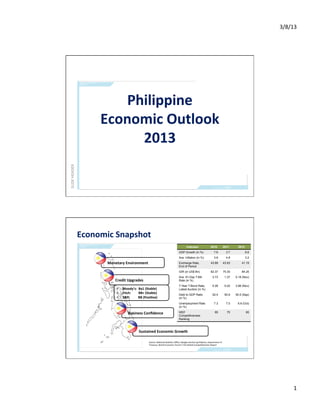

- 1. 3/8/13 Philippine Economic Outlook 2013 SLIDE HEADER Economic Snapshot Indicator 2010 2011 2012 GDP Growth (in %) 7.6 3.7 6.6 Ave. Inflation (in %) 3.8 4.8 3.2 Monetary Environment Exchange Rate, 43.89 43.93 41.19 End of Period GIR (in US$ Bn) 62.37 75.30 84.25 Ave. 91-Day T-Bill 3.73 1.37 0.18 (Nov) Credit Upgrades Rate (in %) 7-Year T-Bond Rate, 5.28 5.02 3.98 (Nov) • Moody’s: Ba1 (Stable) Latest Auction (in %) • Fitch: BB+ (Stable) Debt to GDP Ratio 52.4 50.9 50.5 (Sep) • S&P: BB (PosiIve) (in %) Unemployment Rate 7.3 7.0 6.8 (Oct) (in %) Business Confidence WEF 85 75 65 Competitiveness Ranking Sustained Economic Growth Source: Na0onal Sta0s0cs Office, Bangko Sentral ng Pilipinas, Department of Treasury, World Economic Forum’s The Global Compe00veness Report 1

- 2. 3/8/13 Success Factors in 2012 • Good governance • OFW Dollar RemiPances propelled consumer spending to higher levels • Business Process Outsourcing created the much needed jobs • Strong inflows from foreign investment funds • Contained inflaIon levels • Favorable interest rates • Sterling fiscal and monetary posiIon • Flourishing tourism industry ROP vs. Other Asian Countries 2

- 3. 3/8/13 Economic Snapshot Economic Snapshot 3

- 4. 3/8/13 Economic Snapshot Lower Self-‐Rated Poverty 4

- 5. 3/8/13 Economic Snapshot Success Factors in 2012 Philippines “New Tiger of Asia” “New Darling of Global Investors” Second most progressive stock market in the world in 2012 5

- 6. 3/8/13 Catalysts for Growth in 2013 • Good Governance • Credit RaIng Upgrade – Investment Grade • Intensified Infrastructure Spending through PPP • Stronger Business Process Outsourcing • Stronger inflows of OFW Dollar RemiPances and Foreign Direct and PorZolio Investments Catalysts for Growth in 2013 • Contained InflaIon levels and favorable Interest Rates environment • Healthier fiscal and monetary posiIon • Flourishing Tourism and Leisure Industries • ElecIon Spending • Improving Global Economy • Flourishing Capital Markets 6

- 7. 3/8/13 Rosy Philippine Economic Outlook for 2013 • Philippine Government 6-‐6.5% • First Metro Investment CorporaIon 7.5-‐8% • World Bank 6.2% • HSBC 5.9% • InternaIonal Monetary Fund 6% • ADB 6.2% Leading Economic Indicators 2013 7

- 8. 3/8/13 Thank You! SLIDE HEADER 8