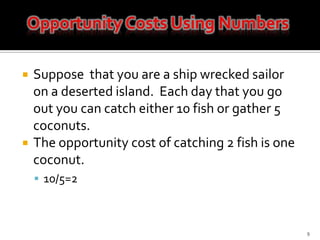

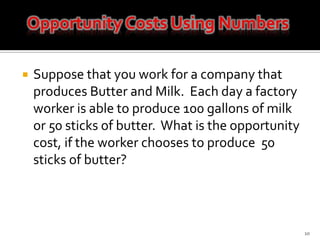

This document discusses direct costs, opportunity costs, and total costs. It defines direct costs as the out-of-pocket expenses to obtain a product, and opportunity costs as the value of the next best alternative forgone by choosing one option over others. Opportunity cost is calculated by comparing alternative production options and quantities. The document provides examples of calculating opportunity costs for activities like catching fish, producing butter and milk, and investing money. It states that total costs equal the direct costs plus the opportunity costs.