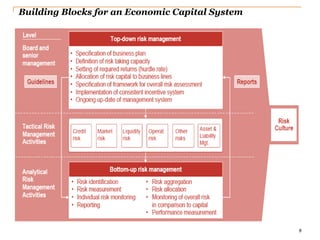

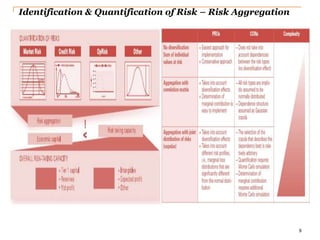

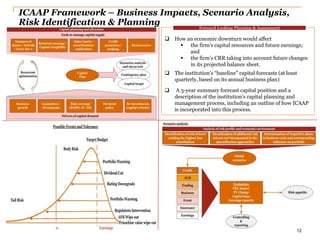

This document discusses frameworks and solutions for risk and capital management. It addresses establishing an enterprise risk management framework, optimizing capital allocation by linking risk to capital, and maximizing risk-adjusted returns. It emphasizes the importance of building these frameworks on a strong data and analytics foundation with continuous measurement and optimization. It also discusses identifying and quantifying total risk, allocating economic capital, and scenario analysis as part of an internal capital adequacy assessment process.