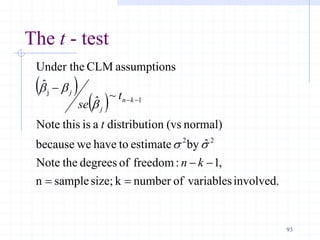

This document provides an introduction to econometrics. It defines econometrics as the integration of economic theory, statistics, and mathematics to empirically analyze economic phenomena. The chapter discusses the need, objectives, and goals of econometrics, including describing economic reality, testing hypotheses, and forecasting. It also compares economic models to econometric models, and outlines the methodology and desirable properties of econometric models. Finally, it discusses different types of data used in econometric analysis, including time series, cross-sectional, and pooled data.

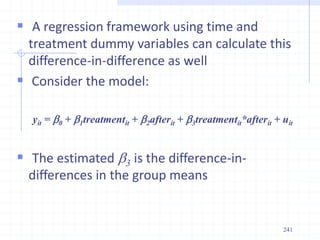

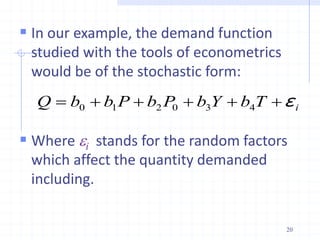

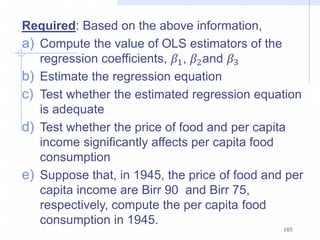

![2.3. The ordinary least squares (OLS) method of

estimation

In the regression model Yi = a + bXi+ i , the values of

the parameters α and β are not known. When they

are estimated from a sample of size n, we obtain the

sample regression line given by:

where α and β are estimated by and respectively,

and is the estimated value of Y.

The dominating and powerful estimation method of

the parameters (or regression coefficients) α and β is

the method of least squares. The deviations between

the observed and estimated values of Y are called the

residuals, . [Note 1: Proof]

,...n

,

,i

X

β

α

Y i

i 2

1

ˆ

ˆ

ˆ

α

ˆ β

ˆ

Y

ˆ

ε

ˆ 47](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-47-320.jpg)

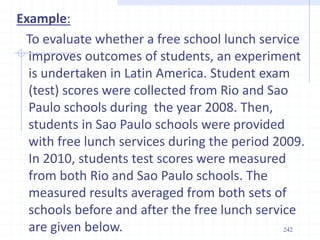

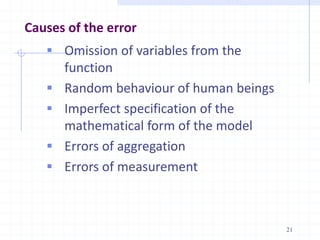

![Proofing the Assumptions

E(𝜀𝑖) = 0

Var(𝜀𝑖) = E(𝜀𝑖 - E(𝜀𝑖))2 , but E(𝜀𝑖) = 0;

= E(𝜀𝑖 -0)2 = E(𝜀𝑖)2 = 𝜎2

Ui~ N(0, 𝜎2) --- from equation 1 and 2

Cov(𝑈𝑖, 𝑈𝑗) = E[(𝑈𝑖 –E(𝑈𝑖)][𝑈𝑗 – E(𝑈𝑗)]; since the E(𝑈𝑖) & E(𝑈𝑗)=0,

= E[(𝑈𝑖 – 0)(𝑈𝑗 – 0)]= E[(𝑈𝑖)(𝑈𝑗)] = E(𝑈𝑖) E(𝑈𝑗) = 0

Cov(𝑋𝑖, 𝑈𝑖) = 0; E(𝑋𝑖–E(𝑋𝑖))(𝑈𝑖– E(𝑈𝑖), but the E(𝑈𝑖) = 0; then E(𝑋𝑖– E(𝑥𝑖))(𝑈𝑖)

= E(𝑋𝑖𝑈𝑖 – 𝑈𝑖E(𝑥𝑖) = 𝑋𝑖E(𝑈𝑖) – 𝑥𝑖E(𝑈𝑖) = 𝑋𝑖(o) – xi(0) = 0

83](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-83-320.jpg)

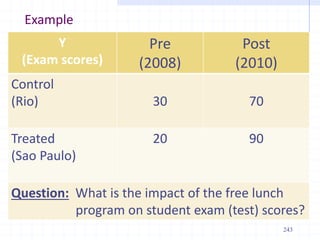

![Consider the following equation:

Yi= b1 + b2X2i + b3X3i + . . . bkXki + i ,

For (k = 3), Yi= b1 + b2X2i + b3X3i + i

3.3. Estimation of parameters and SEs

2

3

2

2

3

2

2

3

2

3

2

3

2

2

)

(

[

]

][

[

]

][

[

]

)

(

][

[

ˆ

i

i

i

i

i

i

i

i

i

i

i

x

x

x

x

x

x

y

x

x

y

x

β

2

3

2

2

3

2

2

3

2

2

2

2

3

3

)

(

[

]

][

[

]

][

[

]

][

[

ˆ

i

i

i

i

i

i

i

i

i

i

i

x

x

x

x

x

x

y

x

x

y

x

β

85](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-85-320.jpg)

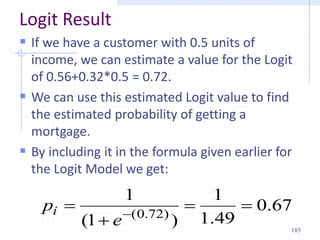

![Computing p-values and t tests with

statistical packages

Most computer packages will compute the

p-value for you, assuming a two-sided test

If you really want a one-sided alternative,

just divide the two-sided p-value by 2

Stata provides the t statistic, p-value, and

95% confidence interval for H0: bj = 0 for

you, in columns labeled “t”, “P > |t|” and

“[95% Conf. Interval]”, respectively

108](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-108-320.jpg)

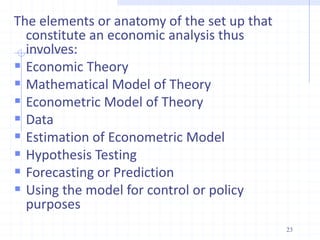

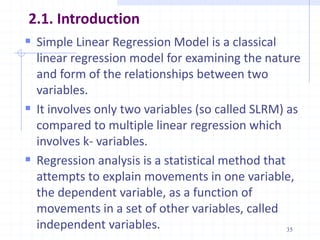

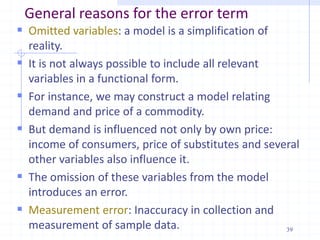

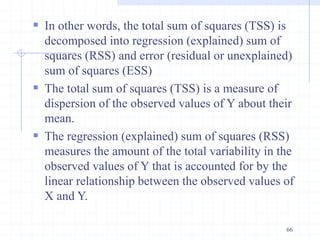

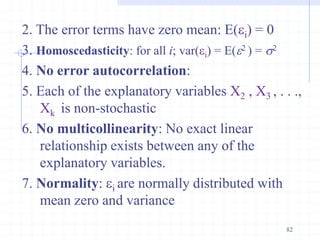

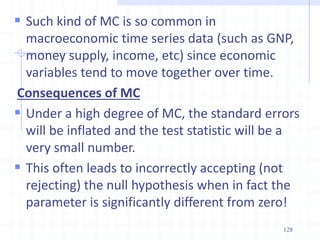

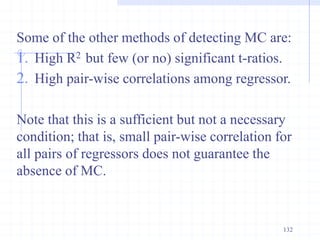

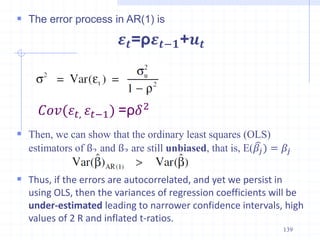

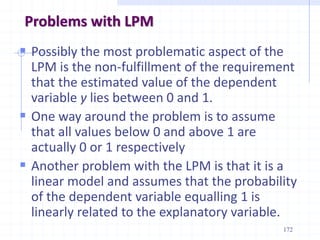

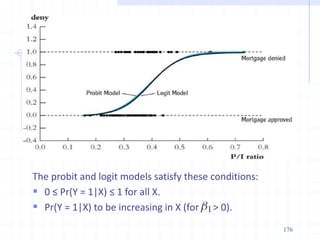

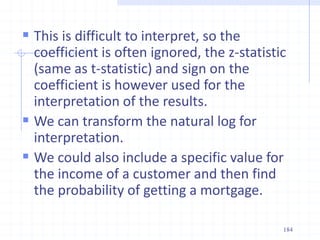

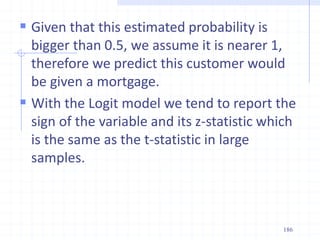

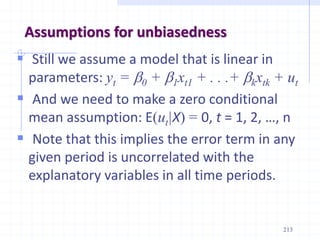

![109

Given multiple regression stata output for income as dependent

variable and temperature, altitude, cities, wage, education,

ownership, and location as explanatory variables and _cons is a

constant term. Based on this, answer the questions that follow.

The following table is generated using the command..

regress income temperature altitude cities wage education

ownership location

_cons .388519 .2026306 1.92 0.058 -.0126417 .7896797

location -.0334028 .009427 -3.54 0.001 -.0520661 -.0147395

ownership .1559908 .0977688 1.60 0.113 -.0375684 .34955

education .0430756 .0125391 3.44 0.001 .0182511 .0679001

wage .1425848 .0795389 1.79 0.076 -.0148835 .300053

cities -.4307053 .0685673 -6.28 0.000 -.5664523 -.2949584

altitude .002892 .0815342 0.04 0.972 -.1585266 .1643105

temperature .0498639 .0681623 0.73 0.466 -.0850814 .1848092

income Coef. Std. Err. t P>|t| [95% Conf. Interval]](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-109-320.jpg)

![ Consider parametric estimation under MLR

Thus, b2 is indeterminate. It can also be shown that b3 is also

indeterminate. Therefore, in the presence of perfect MC, the

regression coefficients can not be estimated.

0

0

25

25

5

5

ˆ

)

5

(

)

5

(

5

5

ˆ

)

(

[

]

][

[

]

][

[

]

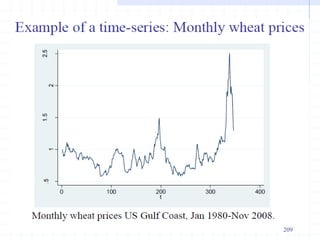

)

(

[

]

[

ˆ

2

2

3

2

3

2

3

2

3

3

2

3

3

2

2

3

3

2

3

2

3

3

3

3

2

3

3

2

2

3

2

2

3

2

2

3

2

3

2

3

2

2

x

x

x

x

y

x

x

y

x

x

x

x

x

x

x

y

x

x

y

x

x

x

x

x

x

x

y

x

x

y

x

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

b

b

b

124](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-124-320.jpg)

![ The measured dependent variable of a decision maker are

assumed to be correlated with the latent variable through the

following threshold criterion

Example: A working mother can establish just as warm and

secure of a relationship with her child as a mother who does

not work. [1=Strongly disagree; 2=Disagree; 3=Agree and

4=Strongly agree].

195](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-195-320.jpg)

![226

Types of the process

(a). Moving average (MA) process

This process only assumes a relation between

periods t and t-1 via the white noise residuals et.

A moving average process of order one [MA(1)]

can be characterized as one where

Yt = et + a1et-1, t = 1, 2,

with et being an iid sequence with mean 0 and

variance s2

This is a stationary, weakly dependent sequence as

variables 1 period apart are correlated, but 2

periods apart they are not](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-226-320.jpg)

![227

Autoregressive (AR) process

An autoregressive process of order one

[AR(1)] can be characterized as one where

Yt = yt-1 + et , t = 1, 2,…

with et being an iid sequence with mean 0

and variance se

2

For this process to be weakly dependent, it

must be the case that |r| < 1

An autoregressive process of order one

[AR(p)]

Yt = 1 yt-1 + 2 yt-2 +… p yp-1 + et](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-227-320.jpg)

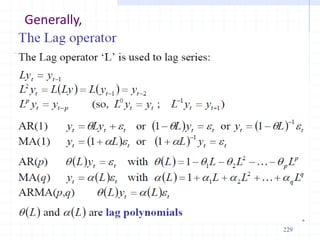

![ Similarly, a moving average (MA) of order (q)]

can be given as

Yt = et + a1et-1 + a2et-2 + … + aqet-q

A combined an AR(p) and MA(q) process can

be combined to an ARMA(p,q) process:

Yt = 1 yt-1 + 2 yt-2 + et + a1et-1 + a2et-2 … + aqet-q

Using the lag operator:

LYt=Yt-1

L2Yt =L(L)Yt=L(Yt-1 )=Yt-2

LpYt =Yt-p

228](https://image.slidesharecdn.com/econometricschaptersall-240402122151-85f21854/85/Econometrics1-2-3-4-5-6-7-8_ChaptersALL-pdf-228-320.jpg)