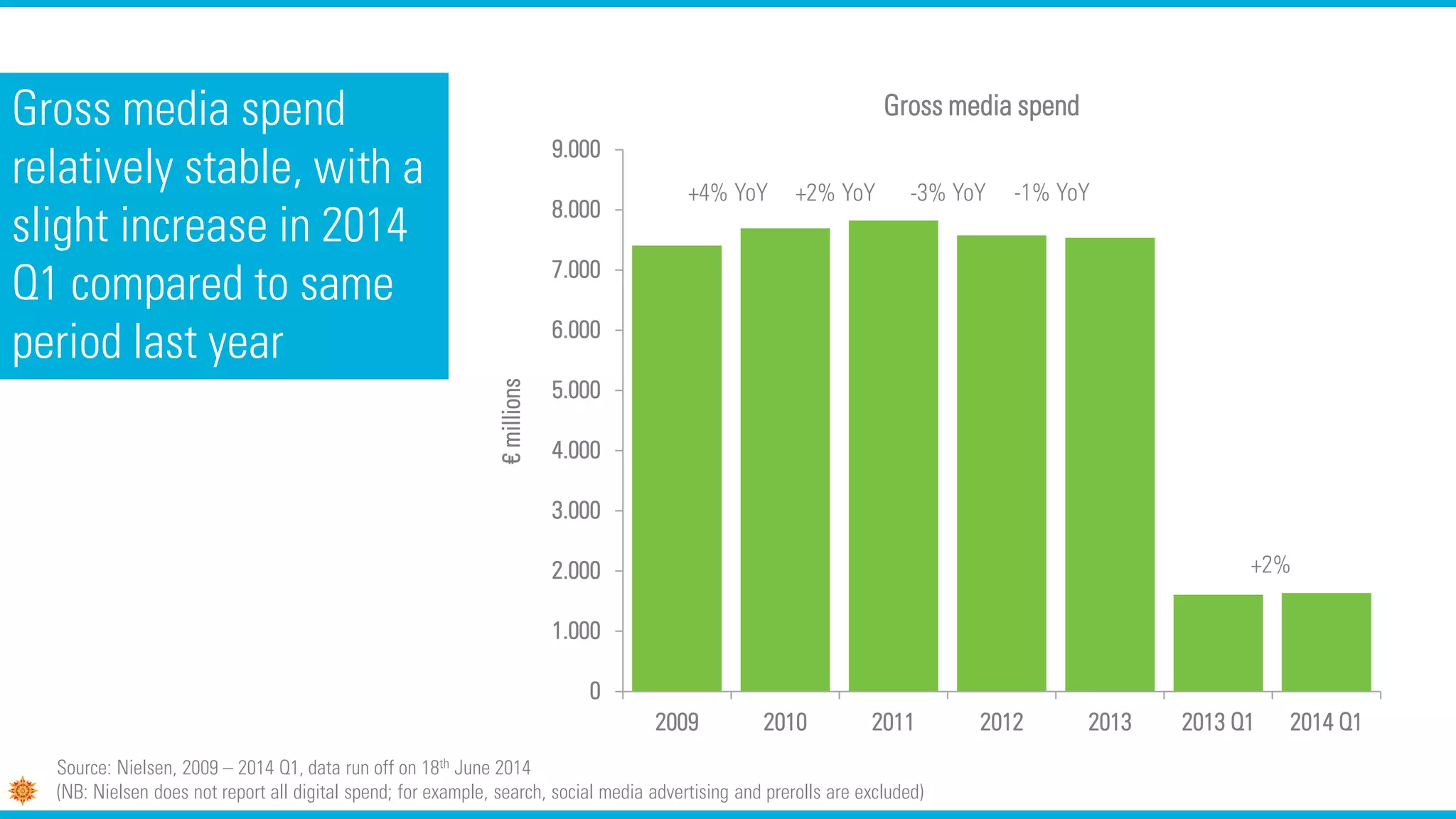

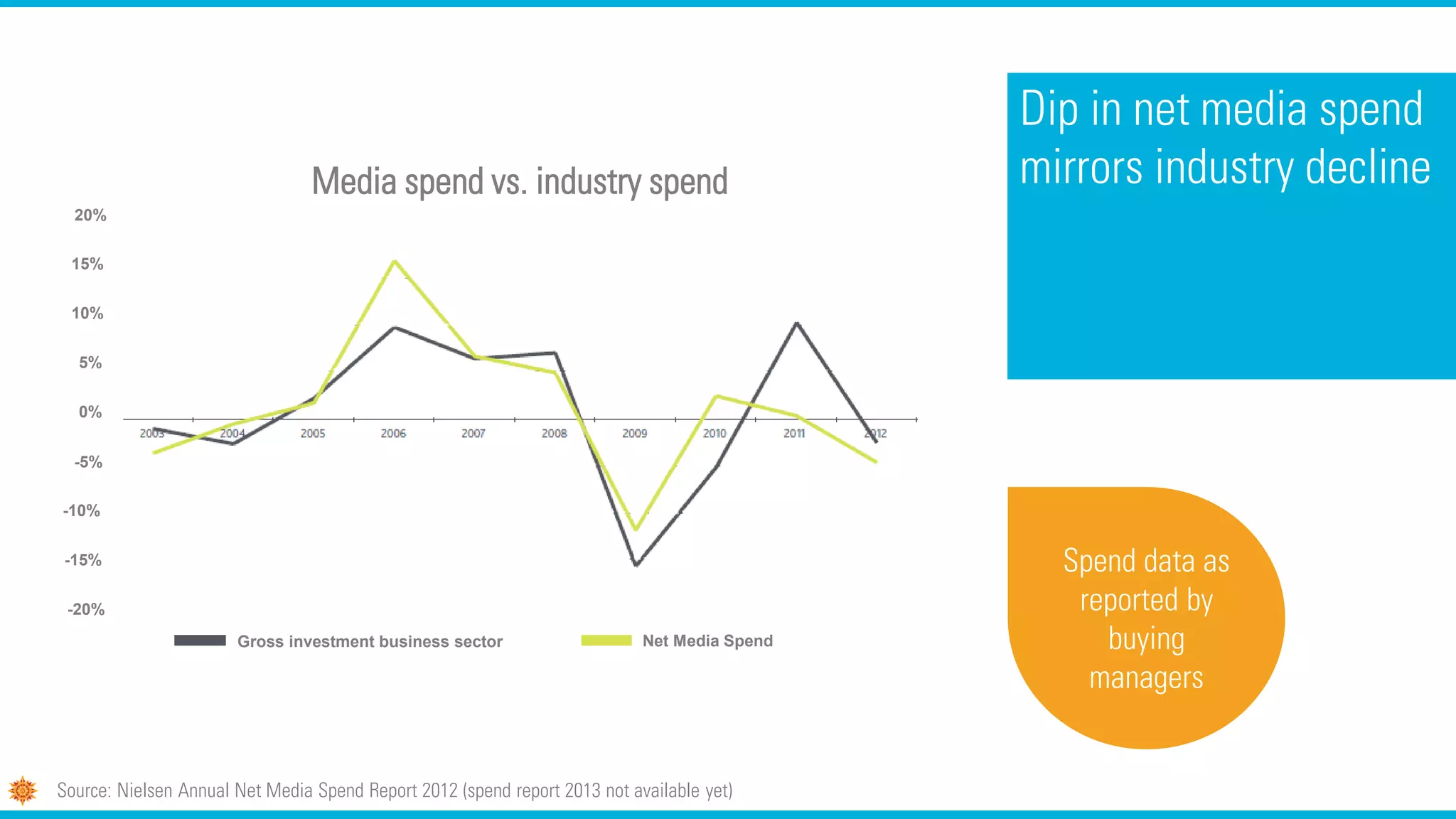

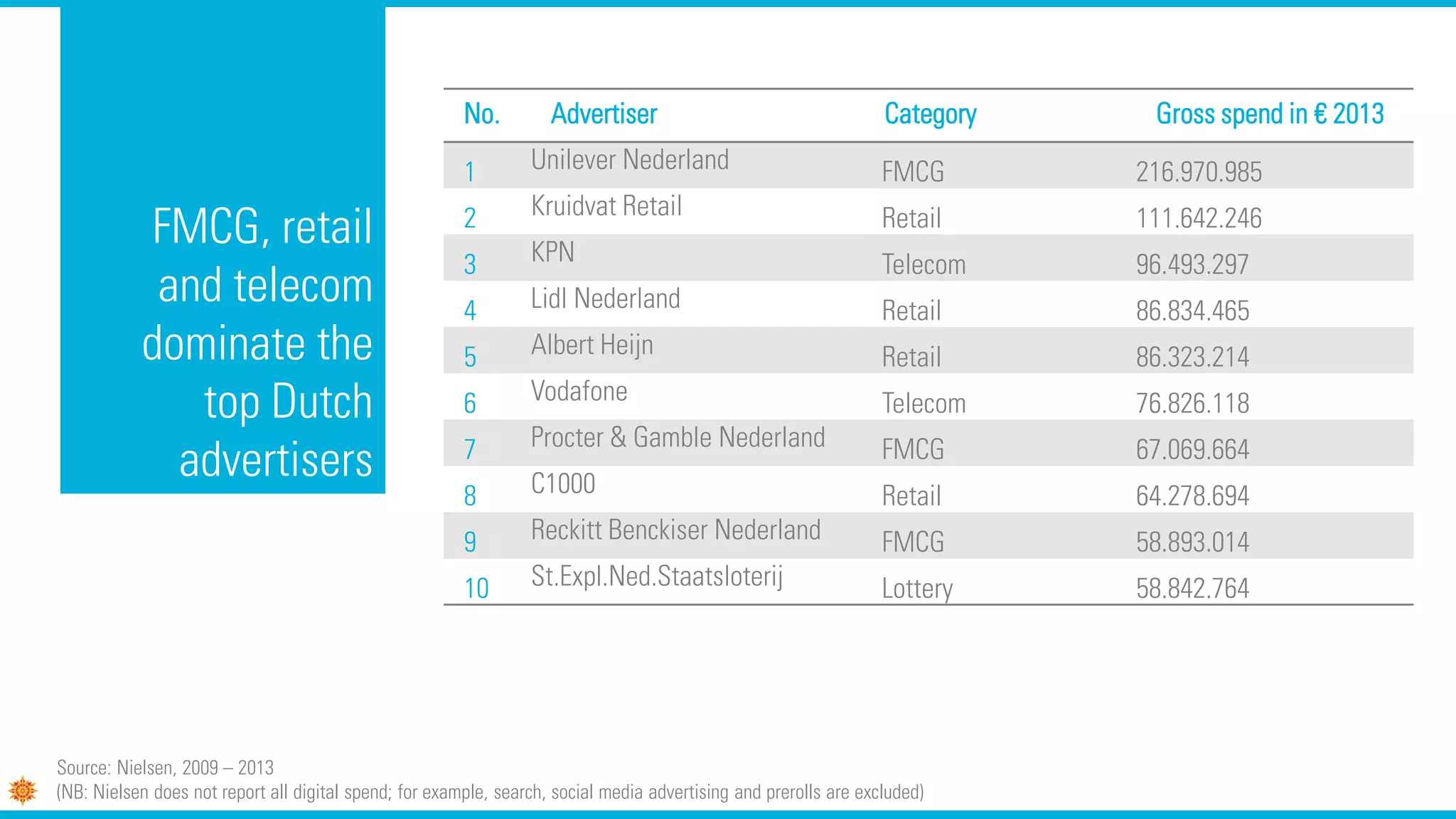

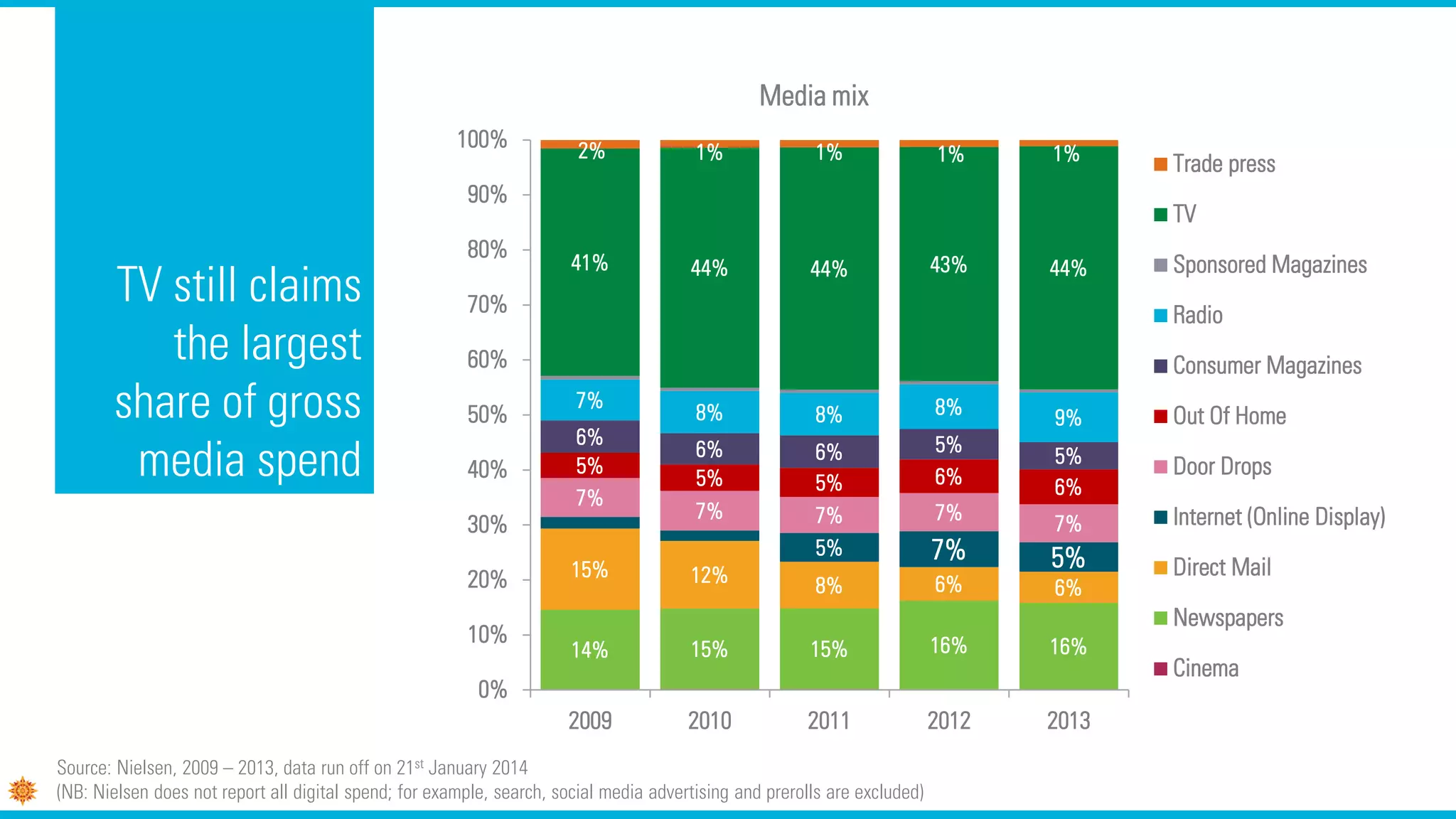

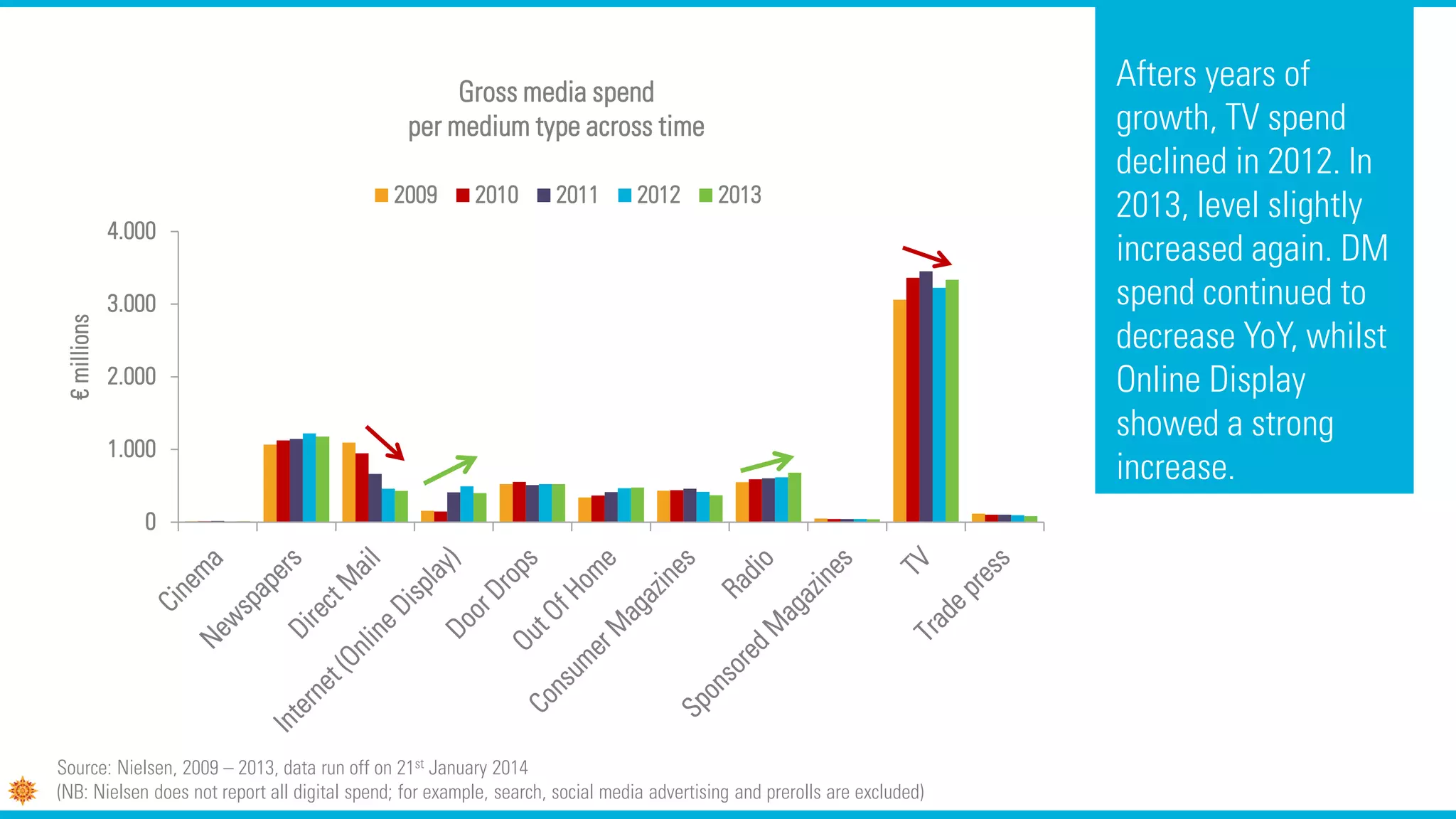

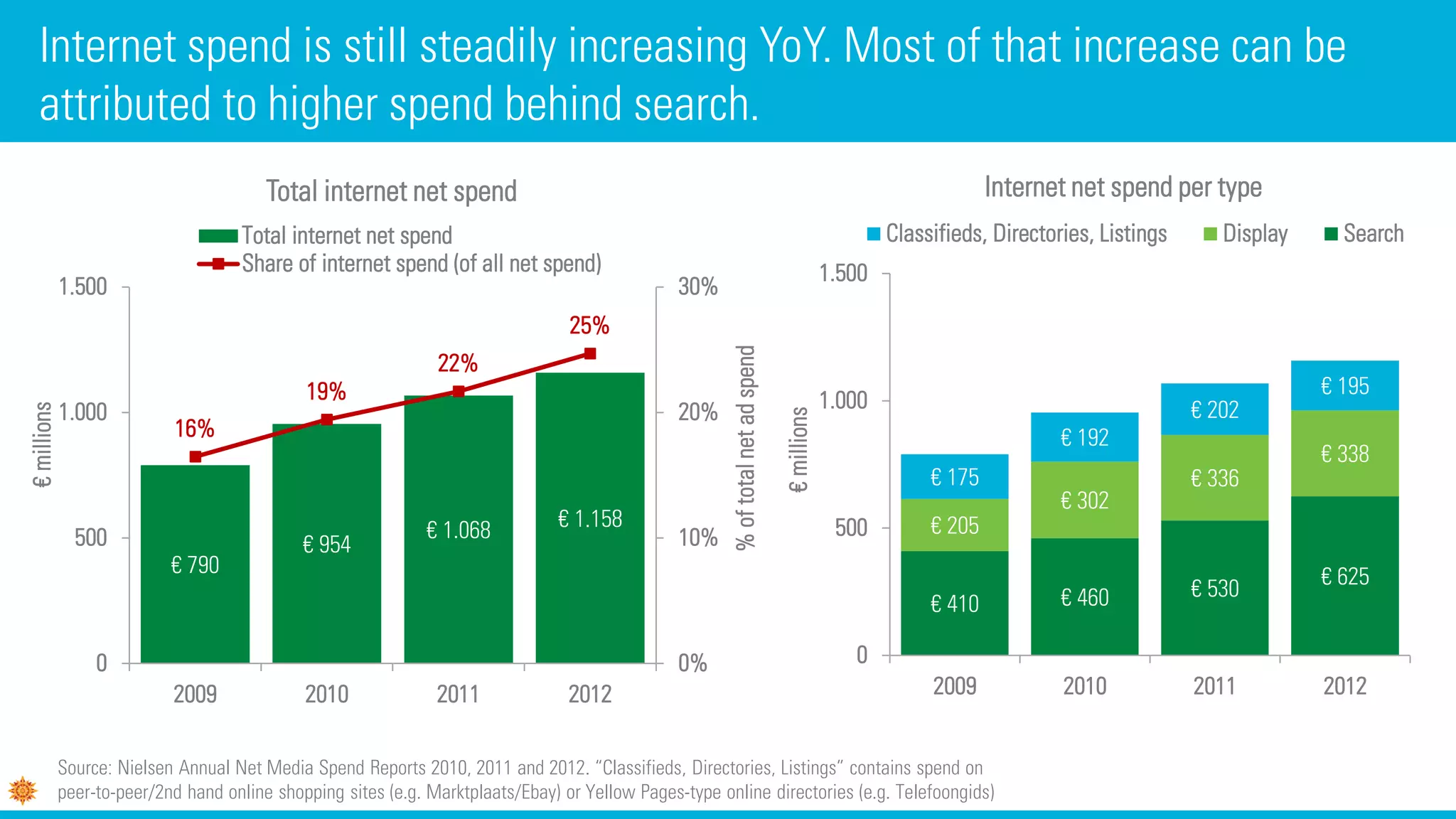

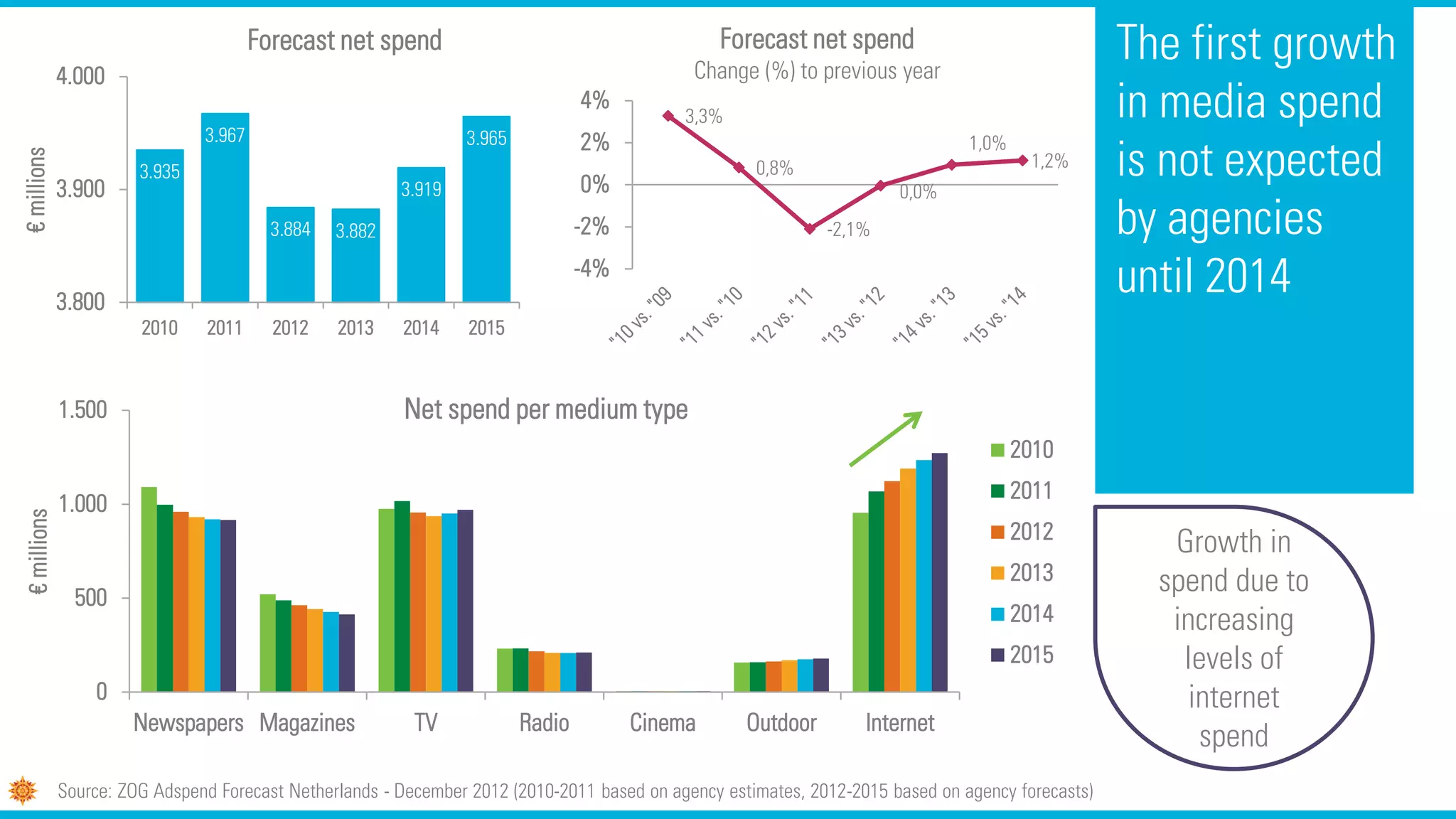

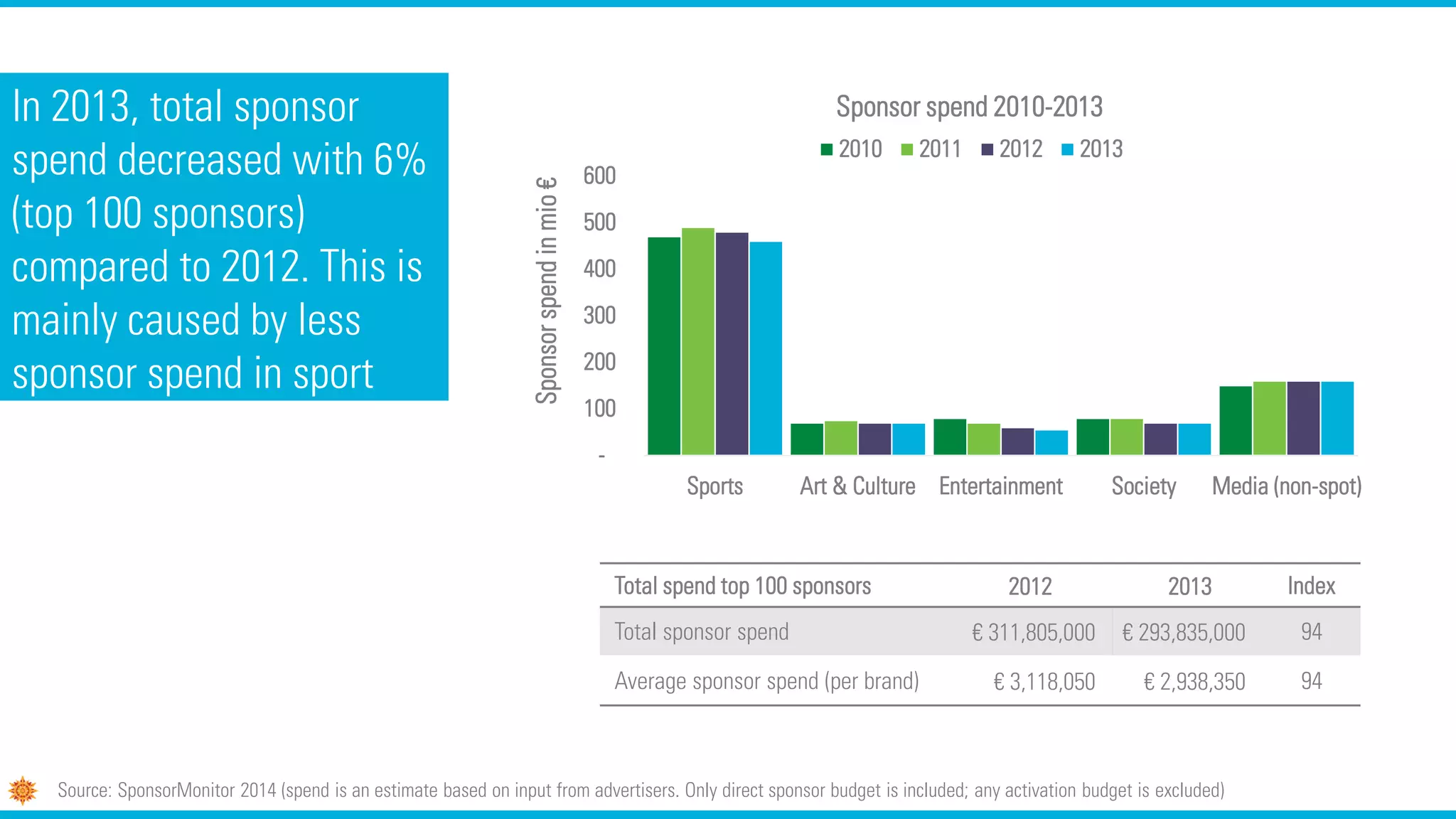

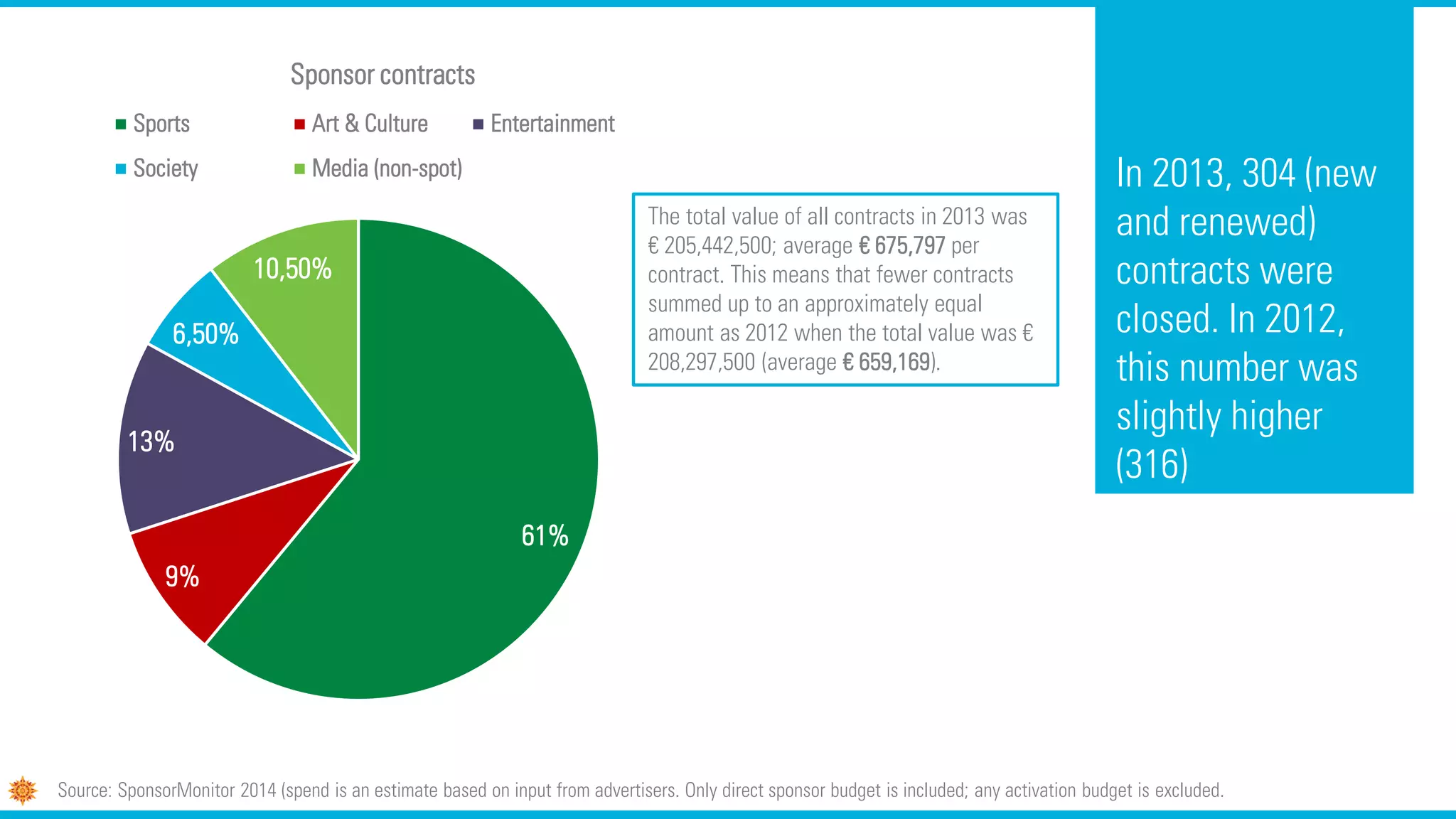

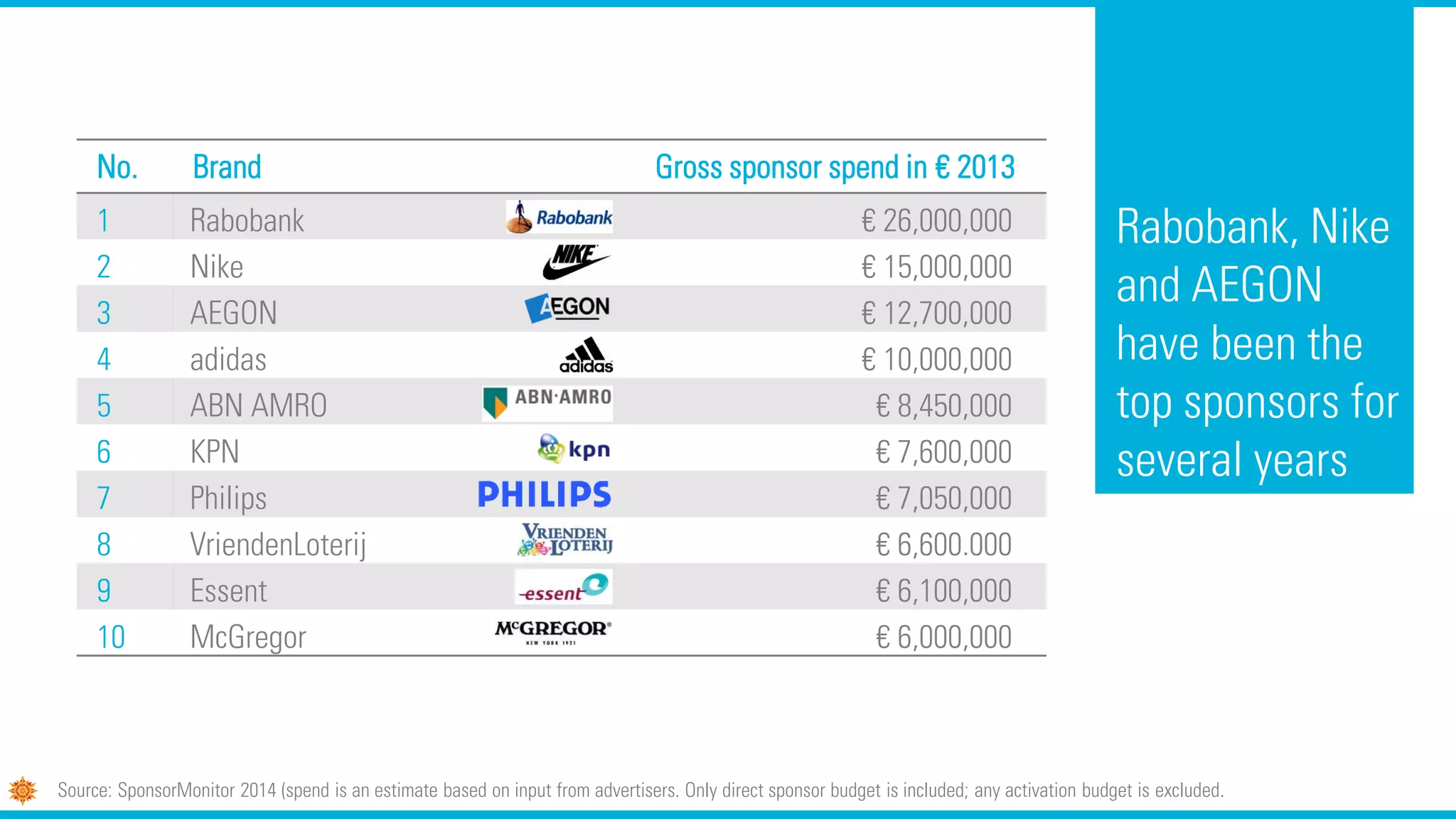

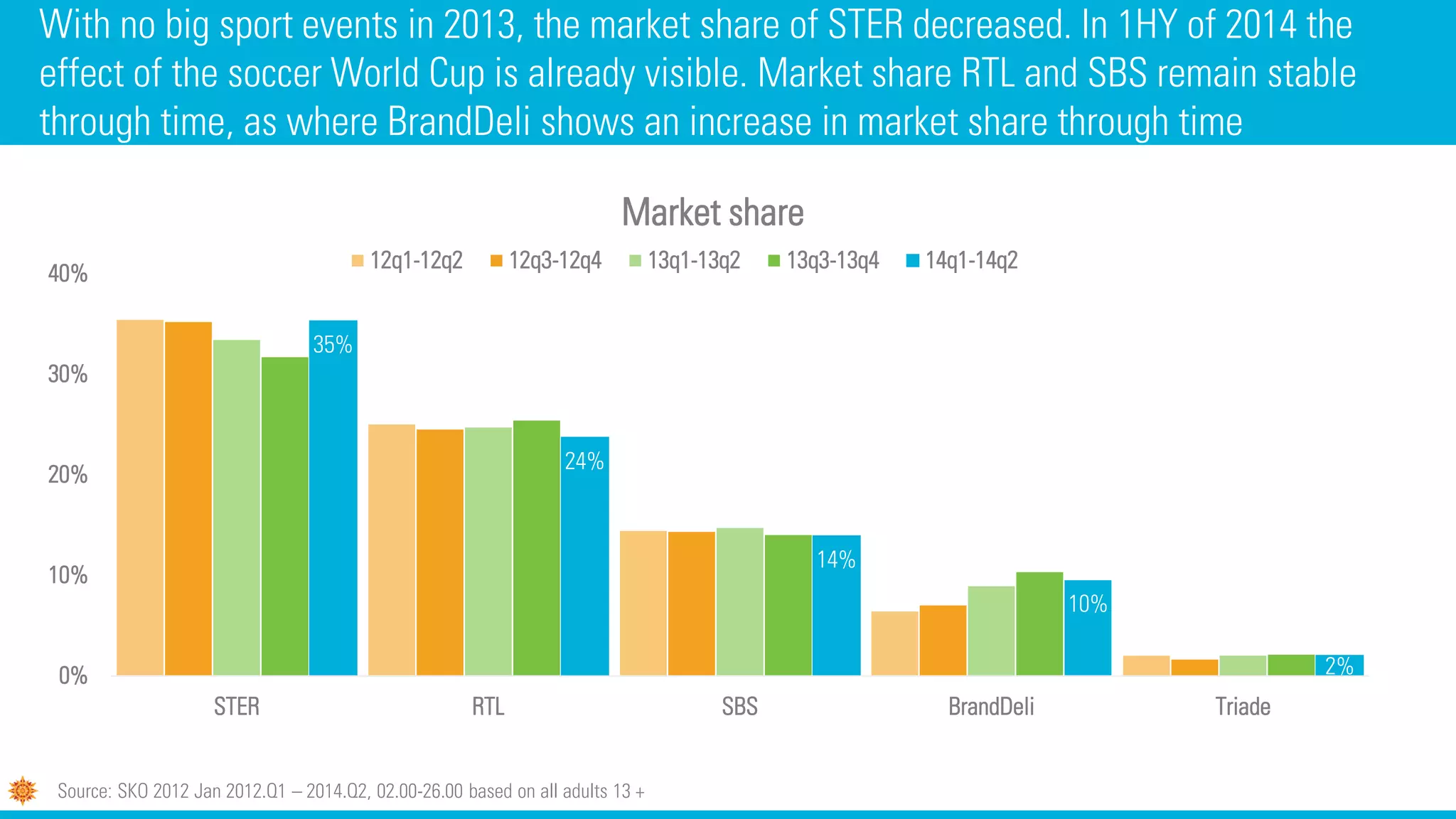

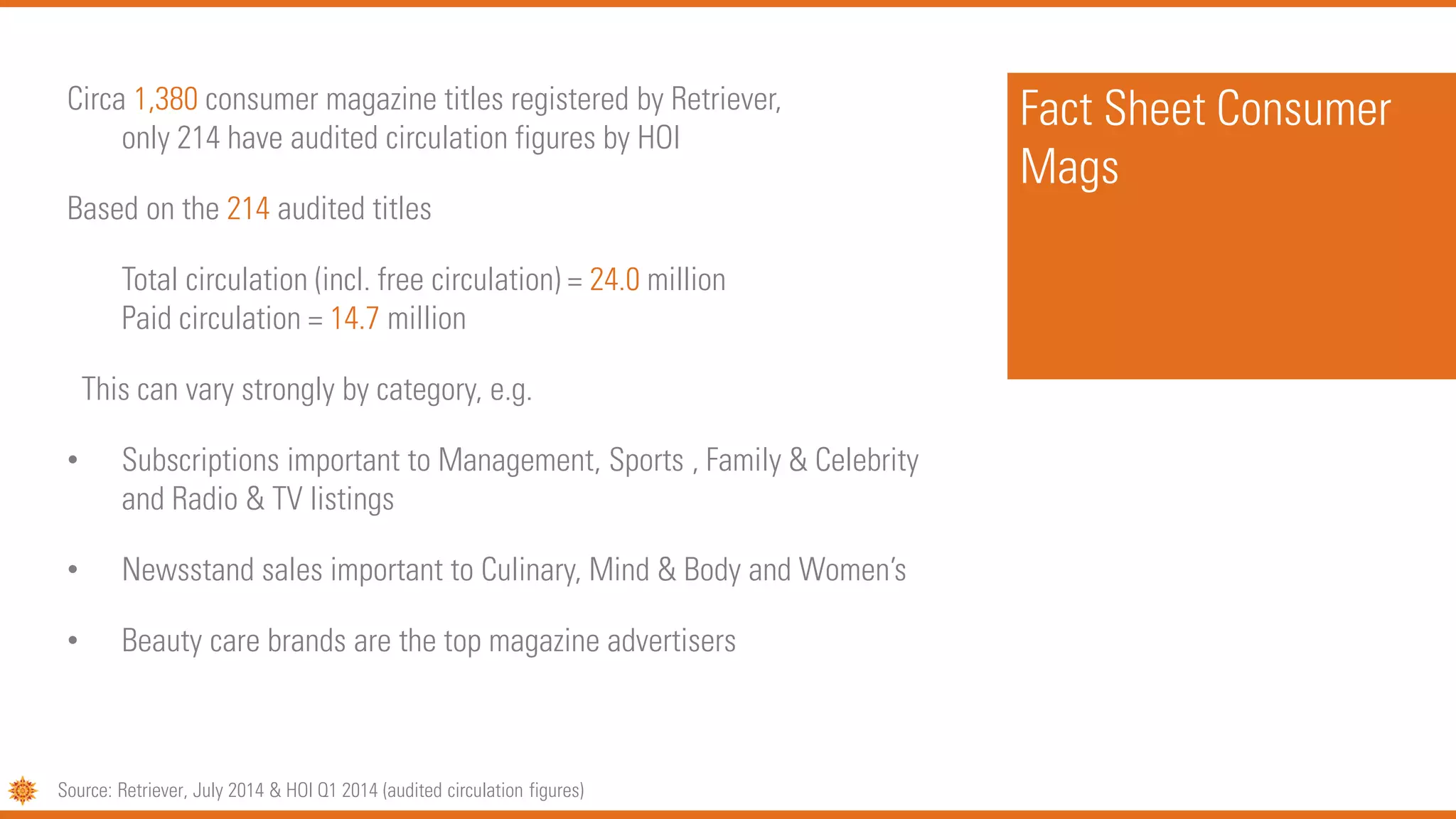

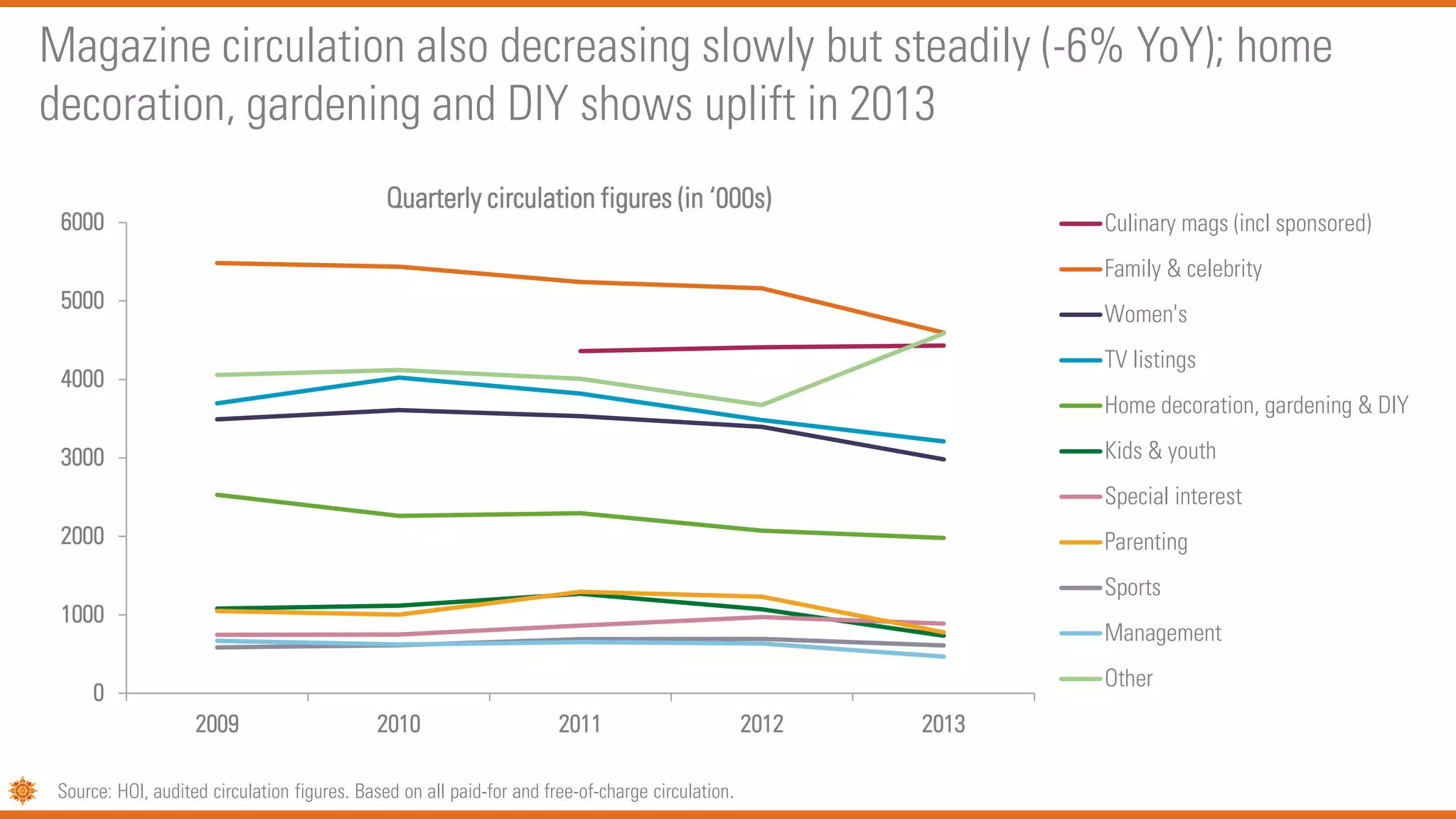

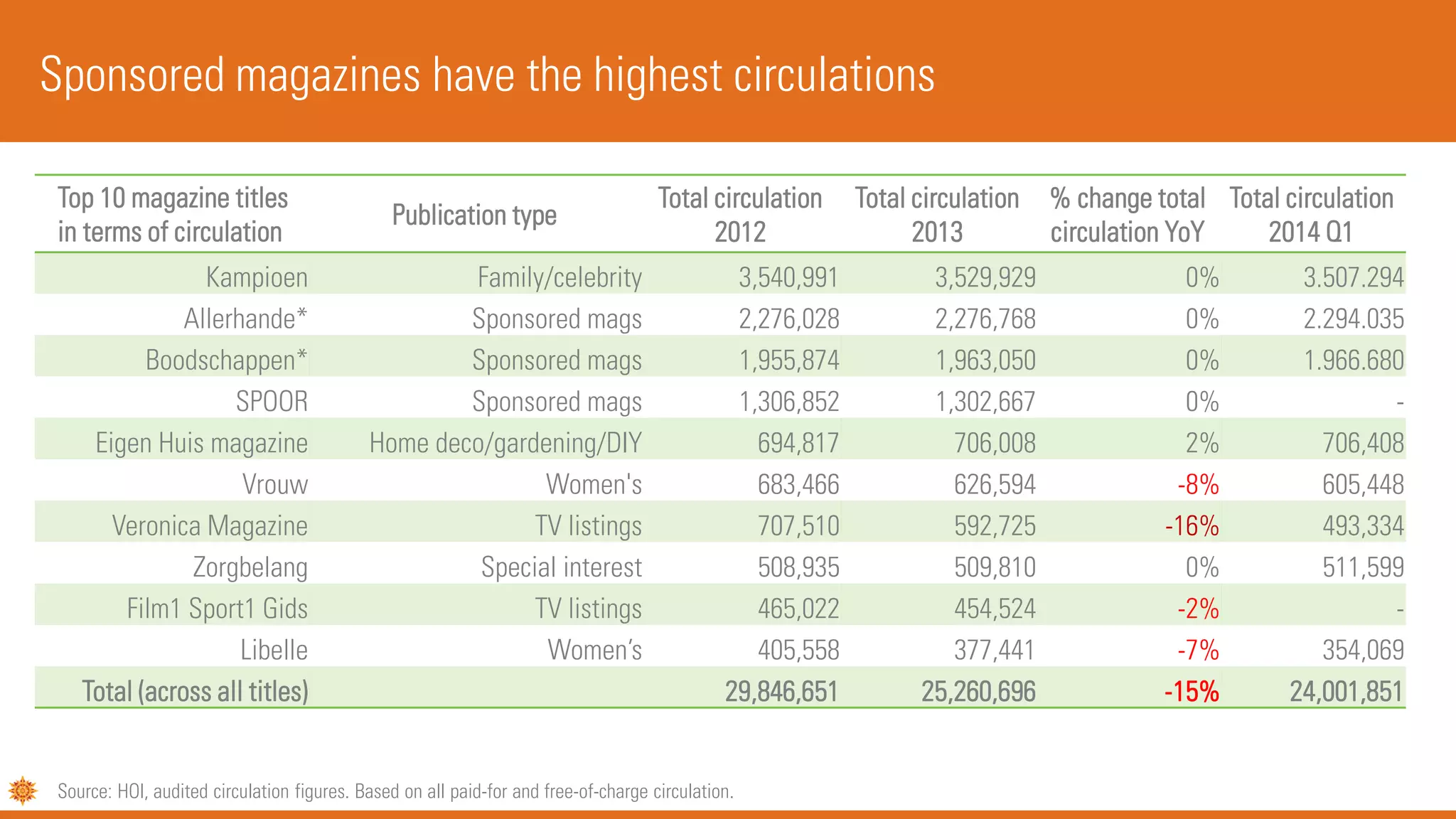

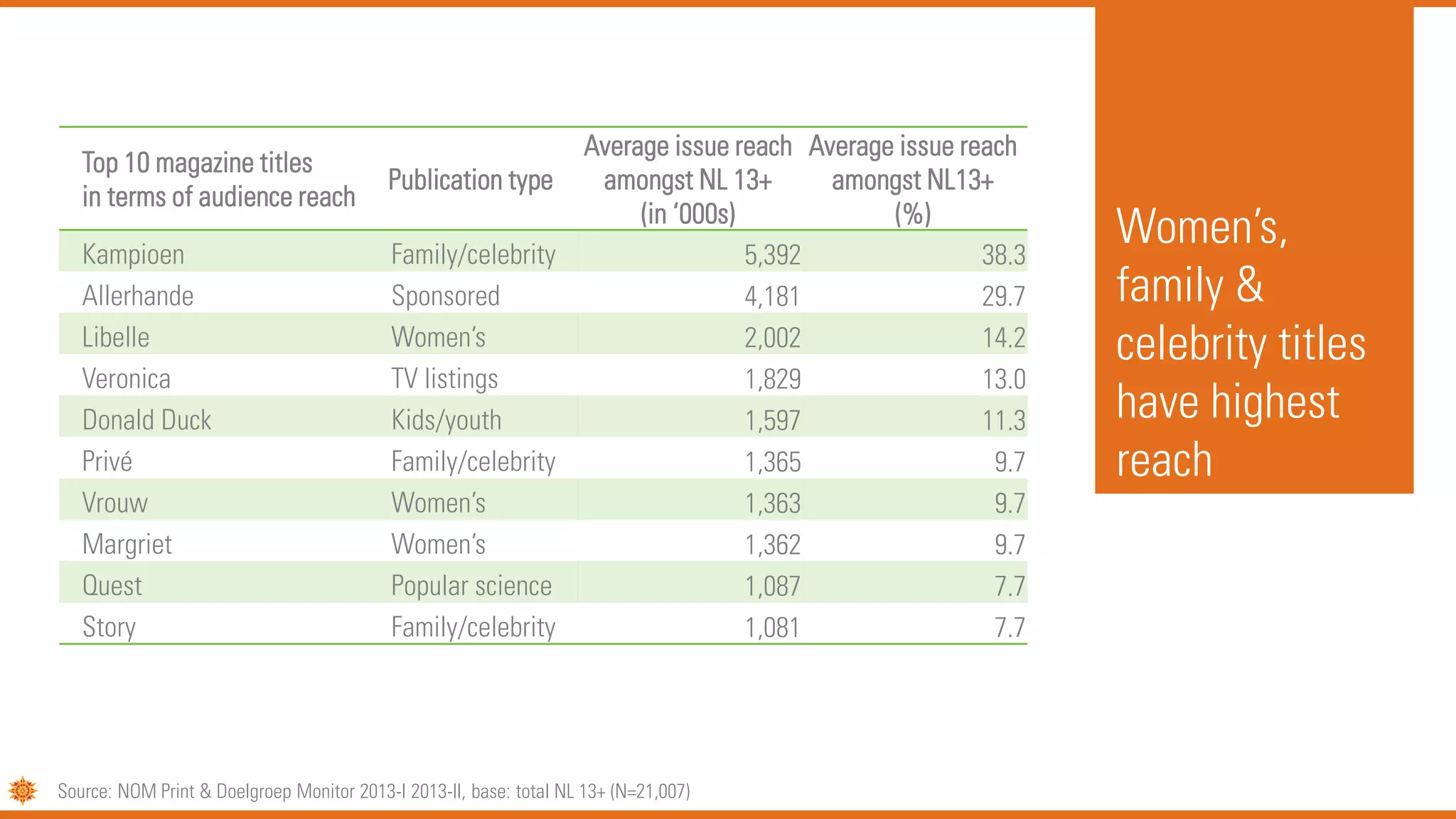

The document provides an overview of media trends in the Netherlands. Key points include: - Television still claims the largest share of gross media spend, though its share is declining as digital spend rises. Internet display spending is growing rapidly year-over-year. - Top advertisers are FMCG, retail, and telecom companies. Retail brands dominate the list of top individual brands spending on advertising. - Total sponsor spending decreased 6% in 2013, mainly due to less spending on sports sponsorships. The majority of sponsor contracts are for sports properties. - Digital trends like social, local and mobile are increasingly important across media. Consumers are engaging more with digital and multi-screen behaviors.