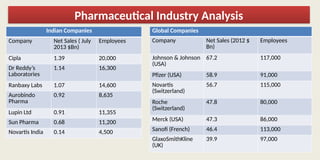

Pharmaceutical Industry Analysis

IndianCompanies

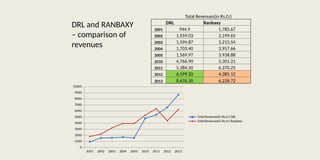

Company Net Sales ( July

2013 $Bn)

Employees

Cipla 1.39 20,000

Dr Reddy’s

Laboratories

1.14 16,300

Ranbaxy Labs 1.07 14,600

Aurobindo

Pharma

0.92 8,635

Lupin Ltd 0.91 11,355

Sun Pharma 0.68 11,200

Novartis India 0.14 4,500

Global Companies

Company Net Sales (2012 $

Bn)

Employees

Johnson & Johnson

(USA)

67.2 117,000

Pfizer (USA) 58.9 91,000

Novartis

(Switzerland)

56.7 115,000

Roche

(Switzerland)

47.8 80,000

Merck (USA) 47.3 86,000

Sanofi (French) 46.4 113,000

GlaxoSmithKline

(UK)

39.9 97,000

3.

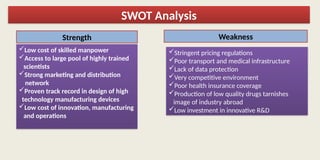

SWOT Analysis

Strength

Low costof skilled manpower

Access to large pool of highly trained

scientists

Strong marketing and distribution

network

Proven track record in design of high

technology manufacturing devices

Low cost of innovation, manufacturing

and operations

Weakness

Stringent pricing regulations

Poor transport and medical infrastructure

Lack of data protection

Very competitive environment

Poor health insurance coverage

Production of low quality drugs tarnishes

image of industry abroad

Low investment in innovative R&D

4.

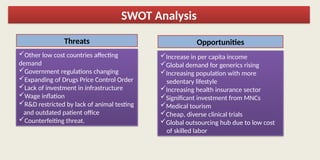

SWOT Analysis

Threats

Other lowcost countries affecting

demand

Government regulations changing

Expanding of Drugs Price Control Order

Lack of investment in infrastructure

Wage inflation

R&D restricted by lack of animal testing

and outdated patient office

Counterfeiting threat.

Opportunities

Increase in per capita income

Global demand for generics rising

Increasing population with more

sedentary lifestyle

Increasing health insurance sector

Significant investment from MNCs

Medical tourism

Cheap, diverse clinical trials

Global outsourcing hub due to low cost

of skilled labor

5.

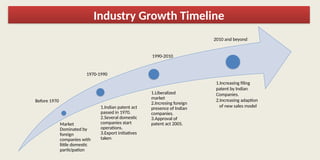

Market

Dominated by

foreign

companies with

littledomestic

participation

1.Indian patent act

passed in 1970.

2.Several domestic

companies start

operations.

3.Export initiatives

taken

1.Liberalized

market

2.Incresing foreign

presence of Indian

companies.

3.Approval of

patent act 2005.

Before 1970

1970-1990

1990-2010

1.Increasing filing

patent by Indian

Companies.

2.Increasing adaption

of new sales model

Industry Growth Timeline

2010 and beyond

6.

• Indian Pharmacompany spends 2% of their revenue on R&D.

• Expenditure on R&D is likely to increase due to introduction of product

patent.

Research & Development

• Pharmaceutical export council expects pharma exports to reach $25

billion in 2016.

Export revenue

• Multinational companies are collaborating with Indian companies to

develop new drugs.

• Phizer partnered with Aurobindo Pharma to develop generic medicine.

Joint ventures

Patents Act

Trends in Indian Pharma Industry

•Amendments to Indian patent act 1970 , to make it TRIPS compliant.

•Increased incentives to domestic firms to conduct R&D.

7.

• To promoteR&D(for future growth) as well as generic

Business(for current profits), a robust organisational model

was required.

• The organizational model should be able to differentiate bulk

activities and generics from speciality and new drug

discovery business

DRL -Challenges

8.

• Vertical

• Horizontal

•Integrated

DIFFERENTIATION

• Centralization

• Decentralization

DECISION MAKING

• Tall

• Flat

• Minimum Chain of Command

HIERARCHY

• Functional

• Multidivisional

• Geographic

• Matrix

STRUCTURE

• Direct Contact, Liason Role, Team ,

INTEGRATING MECHANISM

KEY METRICS FOR ORGANIZATIONAL STRUCTURE

10.

• Incorporated in1961, as a family-owned business

• Chairman – Dr.Tsutomu Une ; CEO & Managing Director – Arun Sawhney

• Ranbaxy was facing many issues such as

– poor financial position,

– no major R&D breakthroughs,

– increasing price wars

– stiff competition in the generics market.

• In order to maintain its growth and market position, Ranbaxy needed an influx of fresh funds

• Daiichi Sankyo wanted to manufacture low cost generics because of Japan government’s new policy

• In June 2008, Daiichi Sankyo acquired over 51% stake in Ranbaxy Laboratories Ltd at Rs. 737 per share.

• Malvinder Singh sold out his stake of 34.8% to Daiichi Sankyo .

• The new entity is a significant milestone in the Ranbaxy’s mission of becoming a research-based international

pharmaceutical company.

RANBAXY LABORATORIES

11.

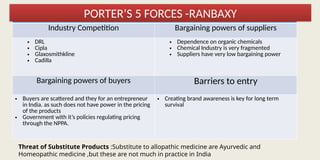

PORTER’S FIVE FORCES

IndustryCompetition Bargaining powers of suppliers

• DRL

• Cipla

• Glaxosmithkline

• Cadilla

• Dependence on organic chemicals

• Chemical Industry is very fragmented

• Suppliers have very low bargaining power

Bargaining powers of buyers Barriers to entry

• Buyers are scattered and they for an entrepreneur

in India. as such does not have power in the pricing

of the products

• Government with it’s policies regulating pricing

through the NPPA.

• Creating brand awareness is key for long term

survival

Threat of Substitute Products :Substitute to allopathic medicine are Ayurvedic and

Homeopathic medicine ,but these are not much in practice in India

PORTER’S 5 FORCES -RANBAXY

12.

• Ranbaxy’s competencyof low cost manufacturing and Daiichi Sankyo’s

competency of innovation will provide the new entity with a

sustainable, long- term competitive advantage.

• Synergies across value chain to achieve maximum stakeholder value at

every stage- with new model it is now among top 20 global pharma

companies

• Ranbaxy is among largest generics companies in India and Daiichi Sankyo is

among largest innovator companies in Japan

• Major Goals of the Global Hybrid Business model adopted in 2008:

– To achieve sustainable growth by ‘complementary business combination’

– To enhance reach in emerging countries

– To accelerate innovative drug creation by optimizing value chain efficiency

13.

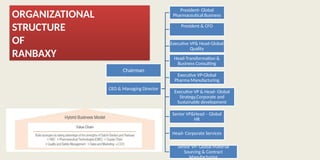

Chairman

CEO & ManagingDirector

President- Global

Pharmaceutical Business

President & CFO

Executive VP& Head-Global

Quality

Executive VP-Global

Pharma Manufacturing

Head-Transformation &

Business Consulting

Executive VP & Head- Global

Strategy,Corporate and

Sustainable development

Senior VP&Head – Global

HR

Head- Corporate Services

Senior VP- Global Material

Sourcing & Contract

Manufacturing

ORGANIZATIONAL

STRUCTURE

OF

RANBAXY

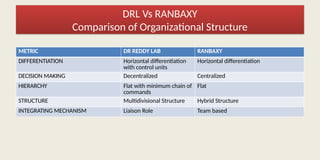

METRIC DR REDDYLAB RANBAXY

DIFFERENTIATION Horizontal differentiation

with control units

Horizontal differentiation

DECISION MAKING Decentralized Centralized

HIERARCHY Flat with minimum chain of

commands

Flat

STRUCTURE Multidivisional Structure Hybrid Structure

INTEGRATING MECHANISM Liaison Role Team based

DRL Vs RANBAXY

Comparison of Organizational Structure

16.

• Having acentralized decision making system with a robust

MIS system on the lines of reporting system of Merrill Lynch

• Centralization of R & D at corporate level to provide a more

directed corporate strategy as done in case of HP

• Adoption of Matrix structure within the remaining units

• Combining CCS with emerging business for better integrating

mechanism

RECOMMENDATIONS