This document summarizes a study on the financial performance evaluation of Punjab National Bank from 2014-2018. It provides background on the bank, including its history dating back to 1894. The study aims to examine the business performance of PNB through analyzing financial ratios and conducting regression analysis to determine the impact of deposits and advances on net profit. The methodology section outlines the secondary data sources used and tools for statistical analysis. Preliminary results are presented on key financial indicators for PNB over the period studied.

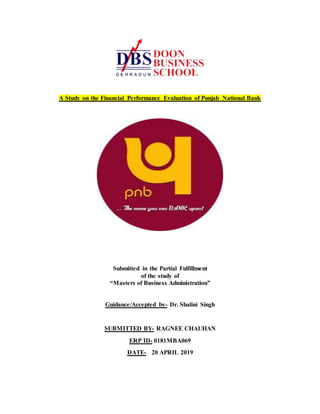

![2.3 Punjab National Bank Fraud Case, 2018

Punjab National Bank disclosed in February 2018 that it detected fraudulent transactions of up to

$1.77 billion at just one of its branches.[13]

2.4 Financial performance data-

2.5 Mergers and acquisitions

Number

Acquisition

date

Company Location Price

Ref(s

).

1 1951

Bharat Bank

Ltd.

New Delhi, India —

2 1961

Universal Bank

of India

Dalmianagar, Bi

har, India

—

3 1962

Indo-

Commercial

Bank

India —

4 1986

Hindustan

Commercial

Bank

India —

Financial performance Rupees. In millions

Mar2018 Mar2017 Mar2016 Mar2015 Mar2014 Mar2013 Mar2012 Mar2011 Mar2010 Mar2009

TotalAssets 7658301.05 7203305.48 6673904.55 6033335.96 5504199.15 4789477.34 4581923.47 3783252.40 2966327.77 2469186.17

OperatingProfitGrowth 0.00 20.02 0.00 0.00 0.00 0.00 0.00 0.00 6.50 0.00

ReportedNetProfit -125843.30 -125843.30 -125843.30 -125843.30 -125843.30 -125843.30 -125843.30 -125843.30 -125843.30 -125843.30

ROA(%) 0.00 0.19 0.00 0.53 0.65 1.01 1.17 1.31 1.44 1.39

GrossNPA 86620.05 55370.45 55818.33 25694.86 18880.06 13465.79 8719.62 4379.39 3214.41 2767.47

NetNPA 48684.29 32702.10 35422.56 15396.50 9916.99 7236.50 4454.23 2038.63 981.69 263.85](https://image.slidesharecdn.com/doonbusinessschoolpnb-200319131431/85/Doon-business-school-pnb-11-320.jpg)

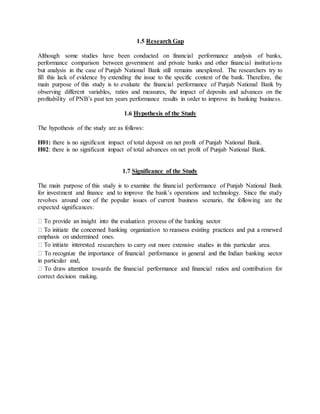

![Number

Acquisition

date

Company Location Price

Ref(s

).

5 1993

New Bank of

India

New Delhi, India —

6 2003

Nedungadi

Bank

Kozhikode, Kera

la, India

—

2.6 Listings and shareholding-

PNB's equity shares are listed on Bombay Stock Exchange and the National Stock Exchange of

India.[20][21] It is a constituent of the CNX Nifty at the NSE.

Shareholders (as on 31-Dec-2013) Shareholding

Promoter Group (Govt. of India) 58.87%

Foreign Institutional Investors (FII) 17.51%

Insurance Companies 15.46%

Individual shareholders 04.05%

Banks/Financial Institutions/Mutual Funds/UTI 03.02%

Others 01.09%

Total 100.0%

2.7 Employees-

PNB Head Office

As on 31 March 2015, the bank had 68,290 employees. As of 31 March 2013, it also had 919

employees with disabilities on the same date (1.45%). The average age of bank employees on the

same date was 46 years. The bank reported business of INR 11.65 crores per employee and net

profit of INR 8.06 lakhs per employee during the FY 2012-13. The company incurred INR 5,751

crores towards employee benefit expenses during the same financial year.](https://image.slidesharecdn.com/doonbusinessschoolpnb-200319131431/85/Doon-business-school-pnb-12-320.jpg)

![8.[77 92]effects and consequences of emphasizing sectoral recovery rate and s...](https://cdn.slidesharecdn.com/ss_thumbnails/8-77-92effectsandconsequencesofemphasizingsectoralrecoveryrateandsectoralproportioninloanportfolioonapprovingnewprojectloansofbangladeshshilpabank-111203185104-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)