Download as PDF, PPTX

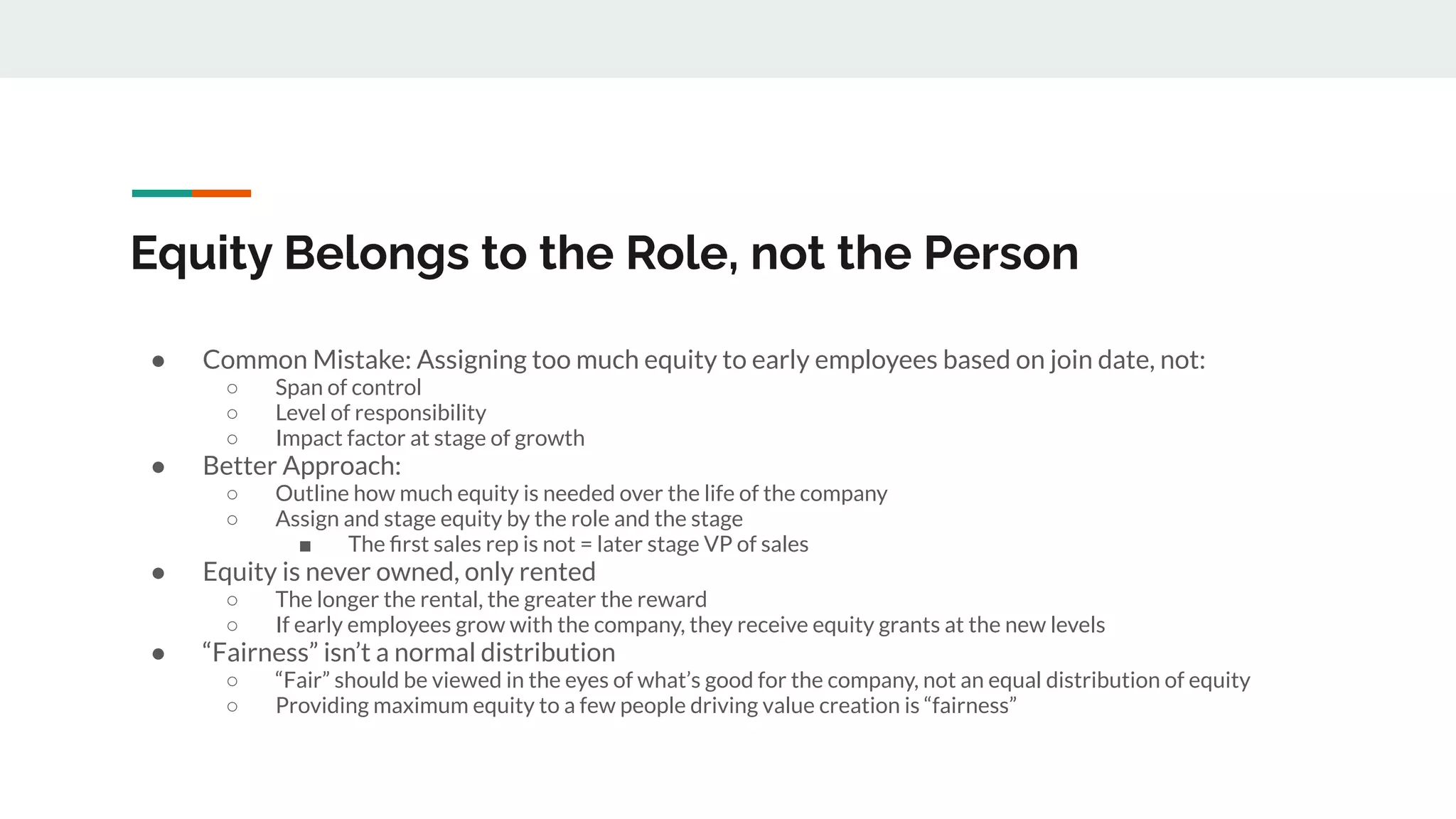

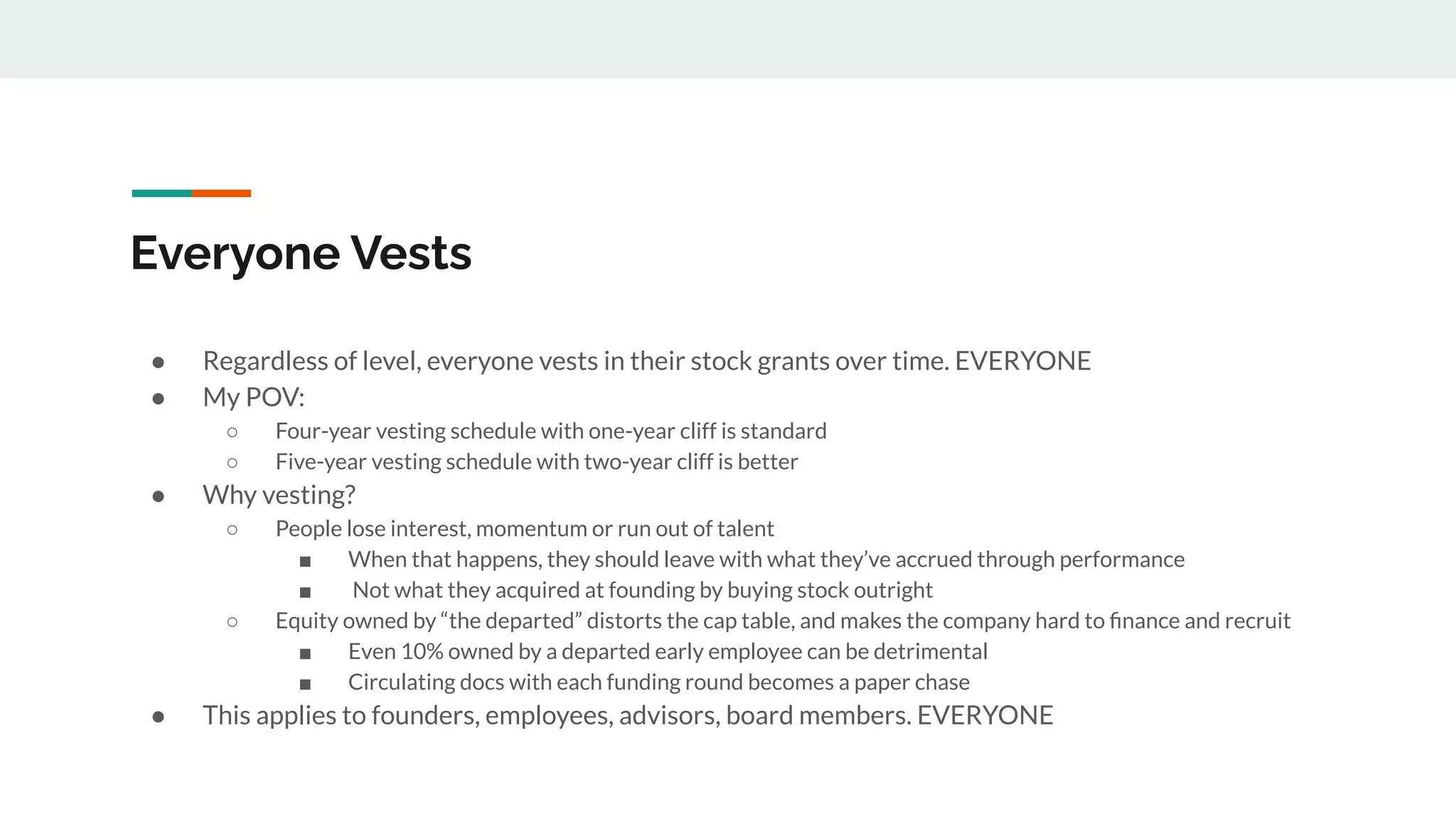

Timothy Jones provides advice on dividing startup equity based on his experience as a founding CEO, early employee, university spinout, VC, and limited partner who has viewed over 1000 deals. He recommends that equity belongs to the role not the person, everyone should vest over time, it generally takes seven long years to know if a startup will succeed or fail, and the Pareto principle suggests founders and early employees will typically end up with 20% ownership while investors own 80% after multiple funding rounds. He also stresses the importance of leaving room in the stock pool to recruit future hires and maintaining tax efficiency.