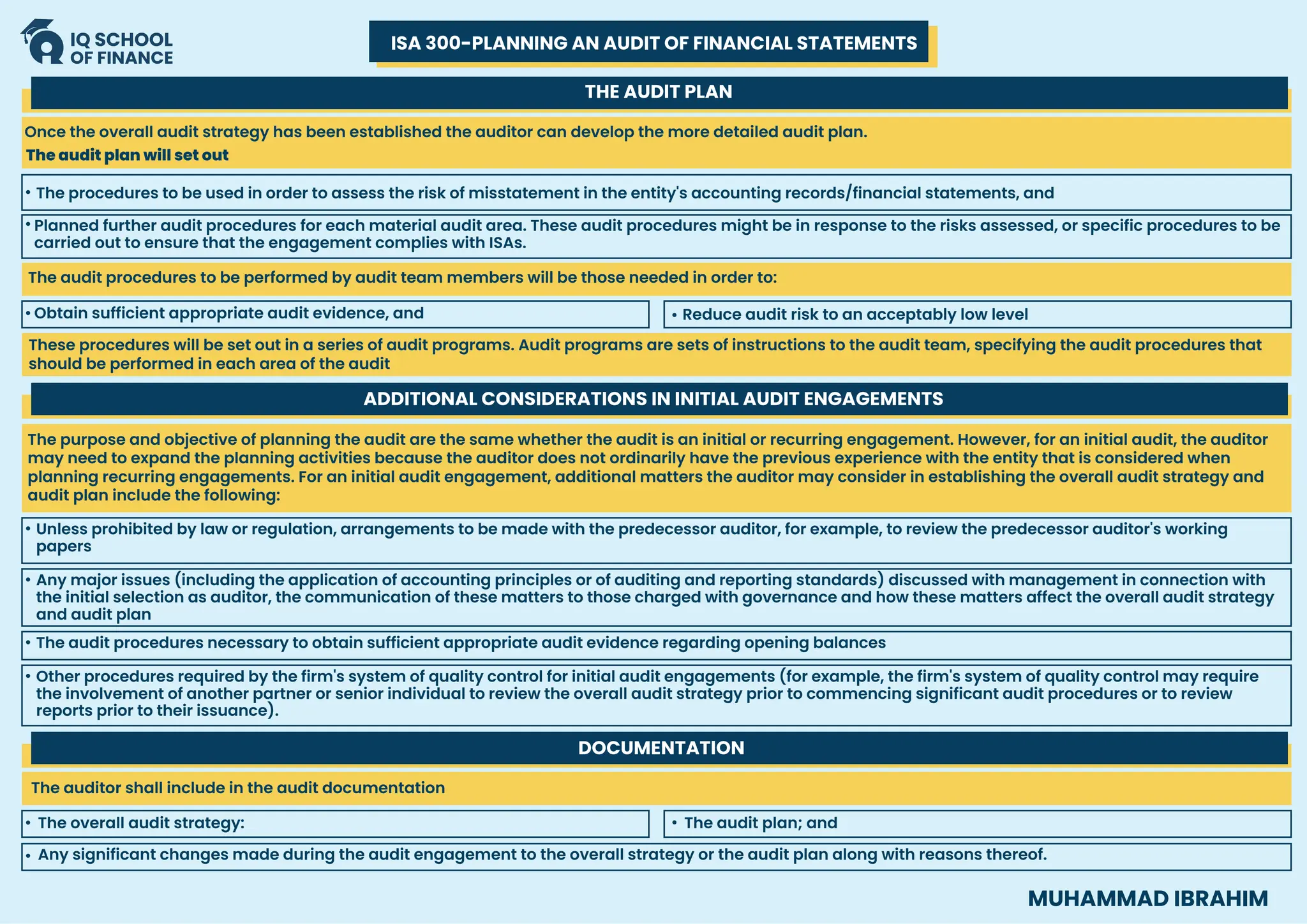

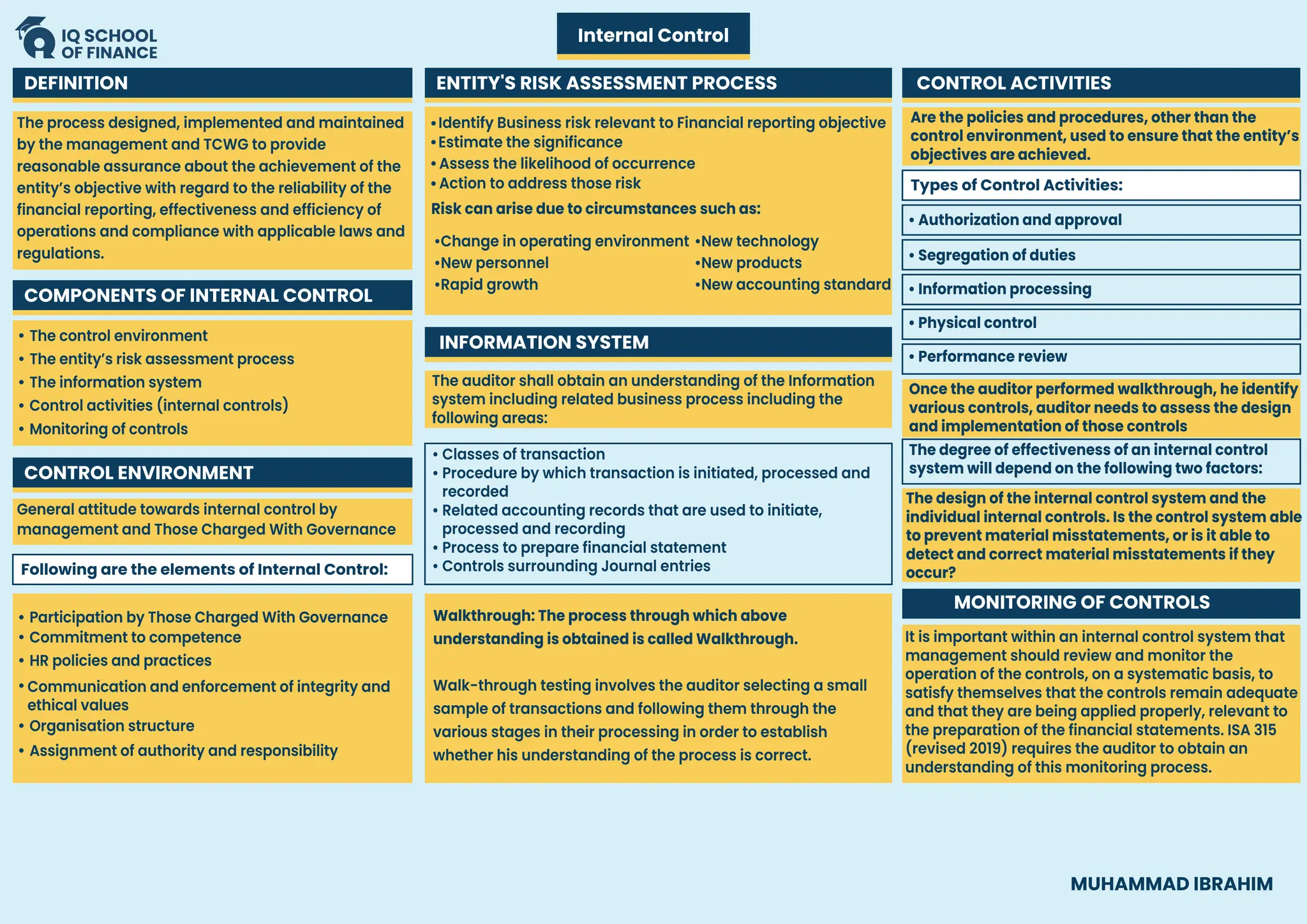

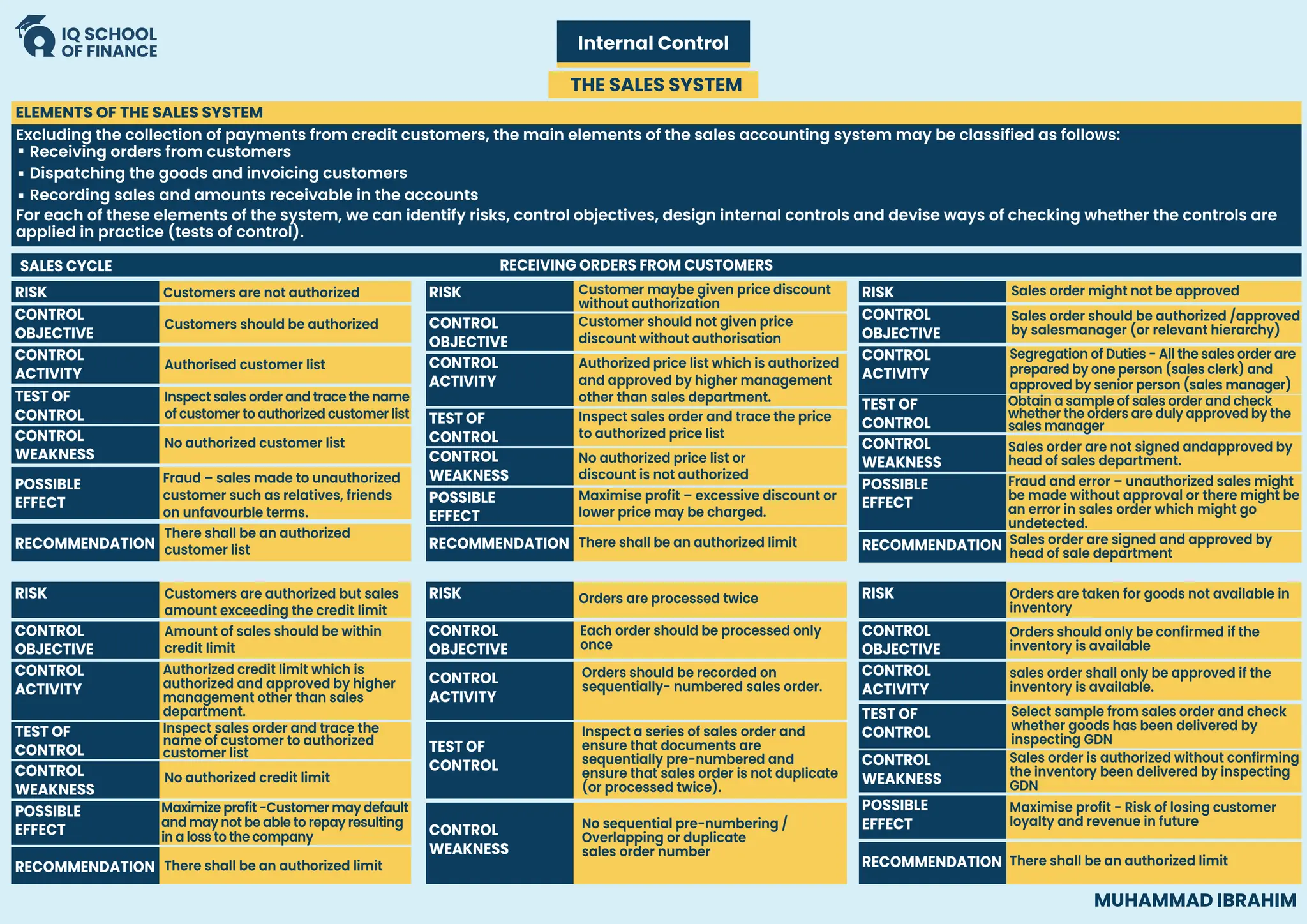

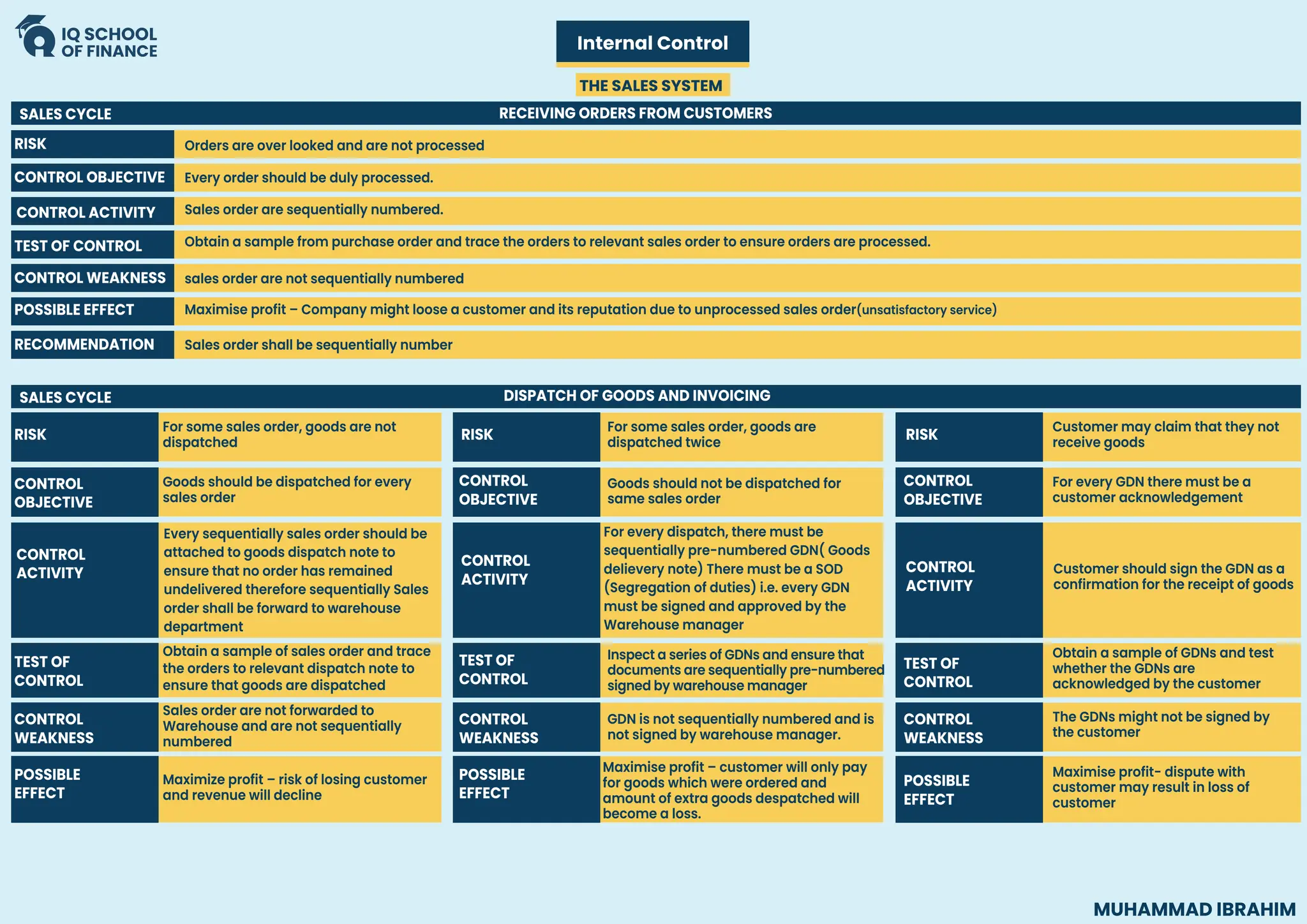

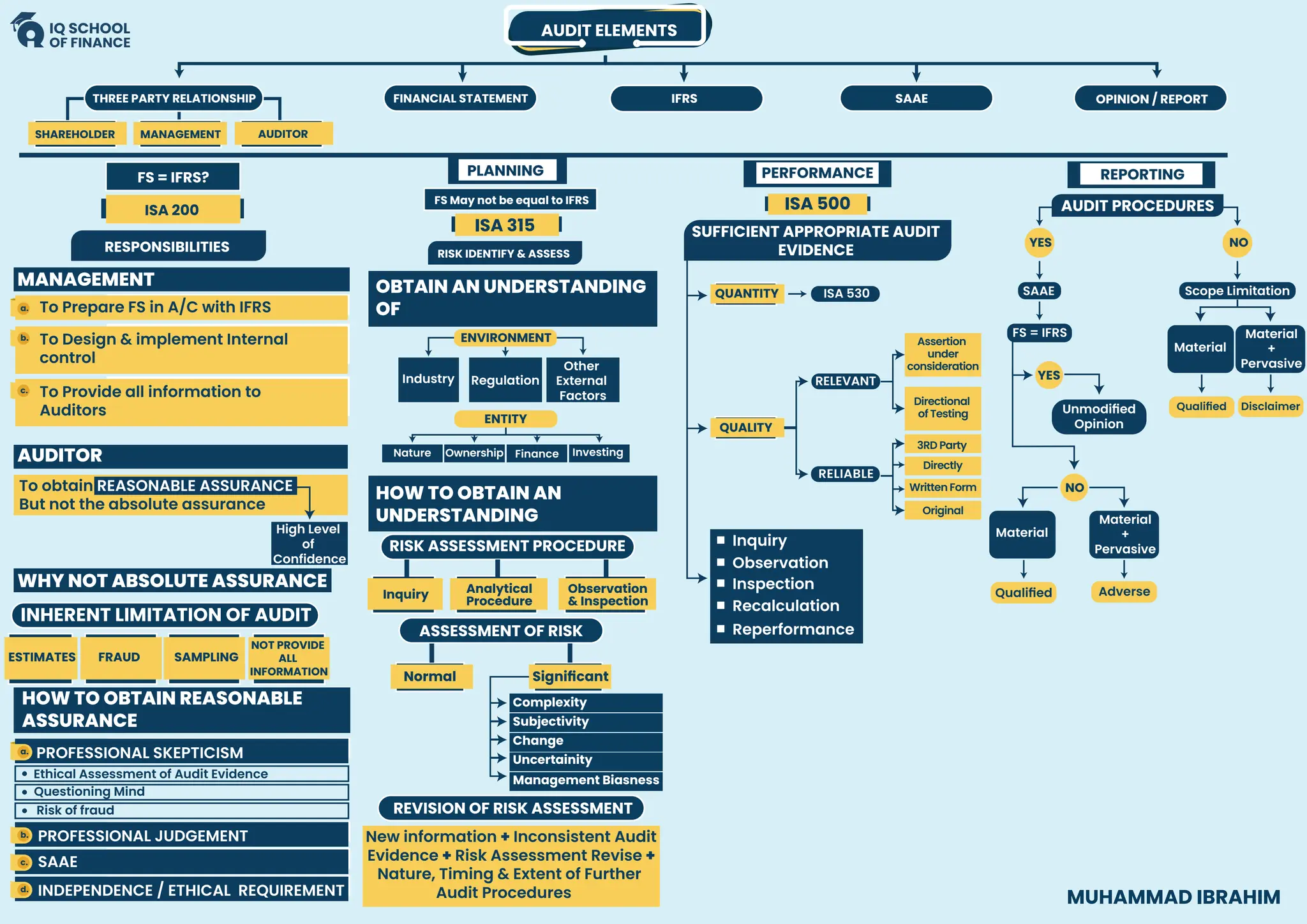

AUDIT ELEMENTS

FINANCIAL STATEMENTIFRS SAAE OPINION / REPORT

SHAREHOLDER MANAGEMENT AUDITOR

FRAUD

NOT PROVIDE

ALL

INFORMATION

SAMPLING

FS = IFRS?

ISA 200

FS May not be equal to IFRS

ISA 315

RESPONSIBILITIES RISK IDENTIFY & ASSESS

ISA 500

SUFFICIENT APPROPRIATE AUDIT

EVIDENCE

a.

a.

b.

c.

d.

b.

c.

To Prepare FS in A/C with IFRS

PROFESSIONAL SKEPTICISM

PROFESSIONAL JUDGEMENT

SAAE

INDEPENDENCE / ETHICAL REQUIREMENT

To Design & implement Internal

control

To Provide all information to

Auditors

INHERENT LIMITATION OF AUDIT

Ethical Assessment of Audit Evidence

Questioning Mind

Risk of fraud

Industry Regulation

Other

External

Factors

ENVIRONMENT

ENTITY

RISK ASSESSMENT PROCEDURE

ASSESSMENT OF RISK

Inquiry Analytical

Procedure

Observation

& Inspection

Normal

REVISION OF RISK ASSESSMENT

Significant

Complexity

Uncertainity

Subjectivity

Change

Management Biasness

QUALITY

ISA 530

RELEVANT

RELIABLE

Inquiry

Observation

Inspection

Recalculation

Reperformance

QUANTITY

AUDIT PROCEDURES

YES

YES

NO

NO

SAAE

FS = IFRS

Unmodified

Opinion

Material

Material

+

Pervasive

Adverse

Scope Limitation

PLANNING PERFORMANCE REPORTING

MUHAMMAD IBRAHIM

To obtain REASONABLE ASSURANCE

But not the absolute assurance

High Level

of

Confidence

Nature Ownership Finance Investing

New information + Inconsistent Audit

Evidence + Risk Assessment Revise +

Nature, Timing & Extent of Further

Audit Procedures

Assertion

under

consideration

Directional

of Testing

3RD Party

Directly

Written Form

Original

Qualified

Material

Material

+

Pervasive

Disclaimer

Qualified

MANAGEMENT

AUDITOR

WHY NOT ABSOLUTE ASSURANCE

HOW TO OBTAIN REASONABLE

ASSURANCE

OBTAIN AN UNDERSTANDING

OF

HOW TO OBTAIN AN

UNDERSTANDING

THREE PARTY RELATIONSHIP

ESTIMATES

2.

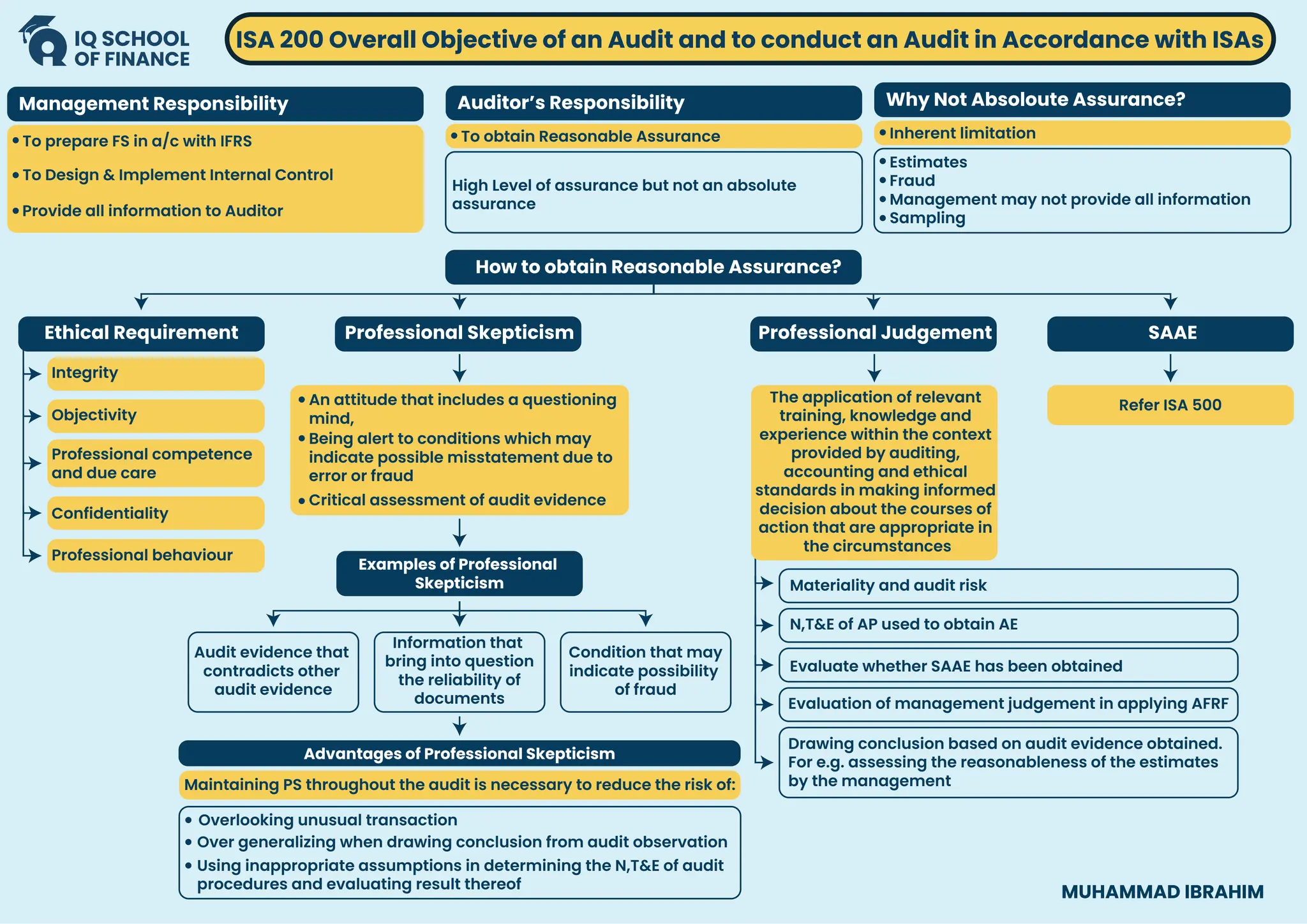

Management Responsibility Auditor’sResponsibility Why Not Absoloute Assurance?

How to obtain Reasonable Assurance?

To prepare FS in a/c with IFRS

To Design & Implement Internal Control

Provide all information to Auditor

ISA 200 Overall Objective of an Audit and to conduct an Audit in Accordance with ISAs

Ethical Requirement Professional Skepticism Professional Judgement SAAE

Examples of Professional

Skepticism

Advantages of Professional Skepticism

To obtain Reasonable Assurance

High Level of assurance but not an absolute

assurance

Estimates

Fraud

Management may not provide all information

Sampling

Inherent limitation

Integrity

Audit evidence that

contradicts other

audit evidence

Information that

bring into question

the reliability of

documents

Condition that may

indicate possibility

of fraud

Overlooking unusual transaction

Over generalizing when drawing conclusion from audit observation

Using inappropriate assumptions in determining the N,T&E of audit

procedures and evaluating result thereof

An attitude that includes a questioning

mind,

Maintaining PS throughout the audit is necessary to reduce the risk of:

Refer ISA 500

Objectivity

Professional competence

and due care

Confidentiality

Professional behaviour

N,T&E of AP used to obtain AE

Materiality and audit risk

Evaluate whether SAAE has been obtained

Evaluation of management judgement in applying AFRF

Drawing conclusion based on audit evidence obtained.

For e.g. assessing the reasonableness of the estimates

by the management

The application of relevant

training, knowledge and

experience within the context

provided by auditing,

accounting and ethical

standards in making informed

decision about the courses of

action that are appropriate in

the circumstances

Being alert to conditions which may

indicate possible misstatement due to

error or fraud

Critical assessment of audit evidence

MUHAMMAD IBRAHIM

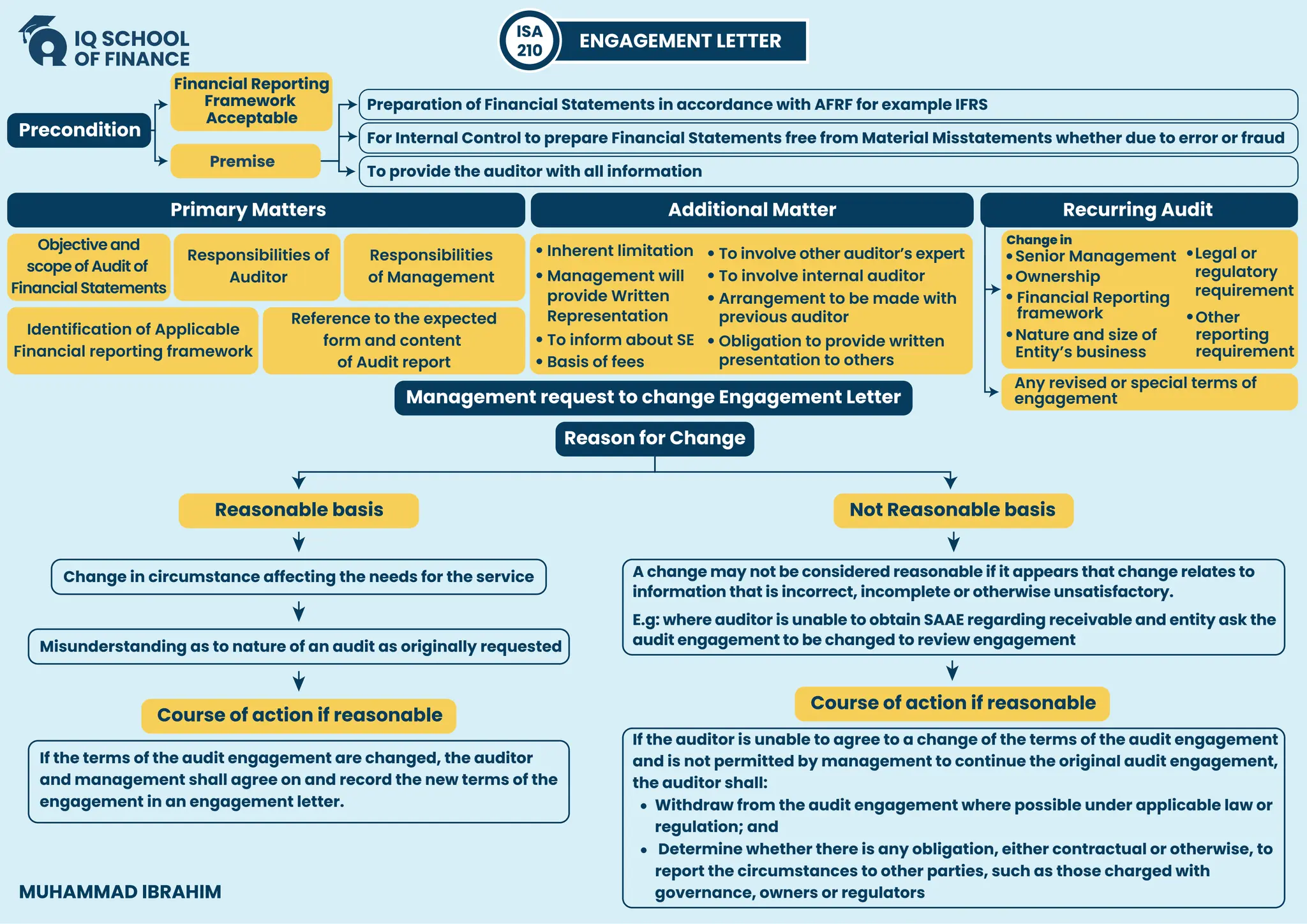

3.

ENGAGEMENT LETTER

ISA

210

Precondition

Primary Matters

Managementrequest to change Engagement Letter

Reason for Change

Change in circumstance affecting the needs for the service

Reasonable basis

Course of action if reasonable

Not Reasonable basis

Additional Matter Recurring Audit

Financial Reporting

Framework

Acceptable

Preparation of Financial Statements in accordance with AFRF for example IFRS

Inherent limitation

Objective and

scope of Audit of

Financial Statements

Responsibilities of

Auditor

Responsibilities

of Management

Reference to the expected

form and content

of Audit report

Identification of Applicable

Financial reporting framework

For Internal Control to prepare Financial Statements free from Material Misstatements whether due to error or fraud

To provide the auditor with all information

Premise

Management will

provide Written

Representation

To inform about SE

Basis of fees

To involve other auditor’s expert

Change in

Senior Management Legal or

regulatory

requirement

Other

reporting

requirement

Ownership

Financial Reporting

framework

Nature and size of

Entity’s business

Any revised or special terms of

engagement

To involve internal auditor

Arrangement to be made with

previous auditor

Obligation to provide written

presentation to others

A change may not be considered reasonable if it appears that change relates to

information that is incorrect, incomplete or otherwise unsatisfactory.

E.g: where auditor is unable to obtain SAAE regarding receivable and entity ask the

audit engagement to be changed to review engagement

Misunderstanding as to nature of an audit as originally requested

If the terms of the audit engagement are changed, the auditor

and management shall agree on and record the new terms of the

engagement in an engagement letter.

If the auditor is unable to agree to a change of the terms of the audit engagement

and is not permitted by management to continue the original audit engagement,

the auditor shall:

Withdraw from the audit engagement where possible under applicable law or

regulation; and

Determine whether there is any obligation, either contractual or otherwise, to

report the circumstances to other parties, such as those charged with

governance, owners or regulators

Course of action if reasonable

MUHAMMAD IBRAHIM

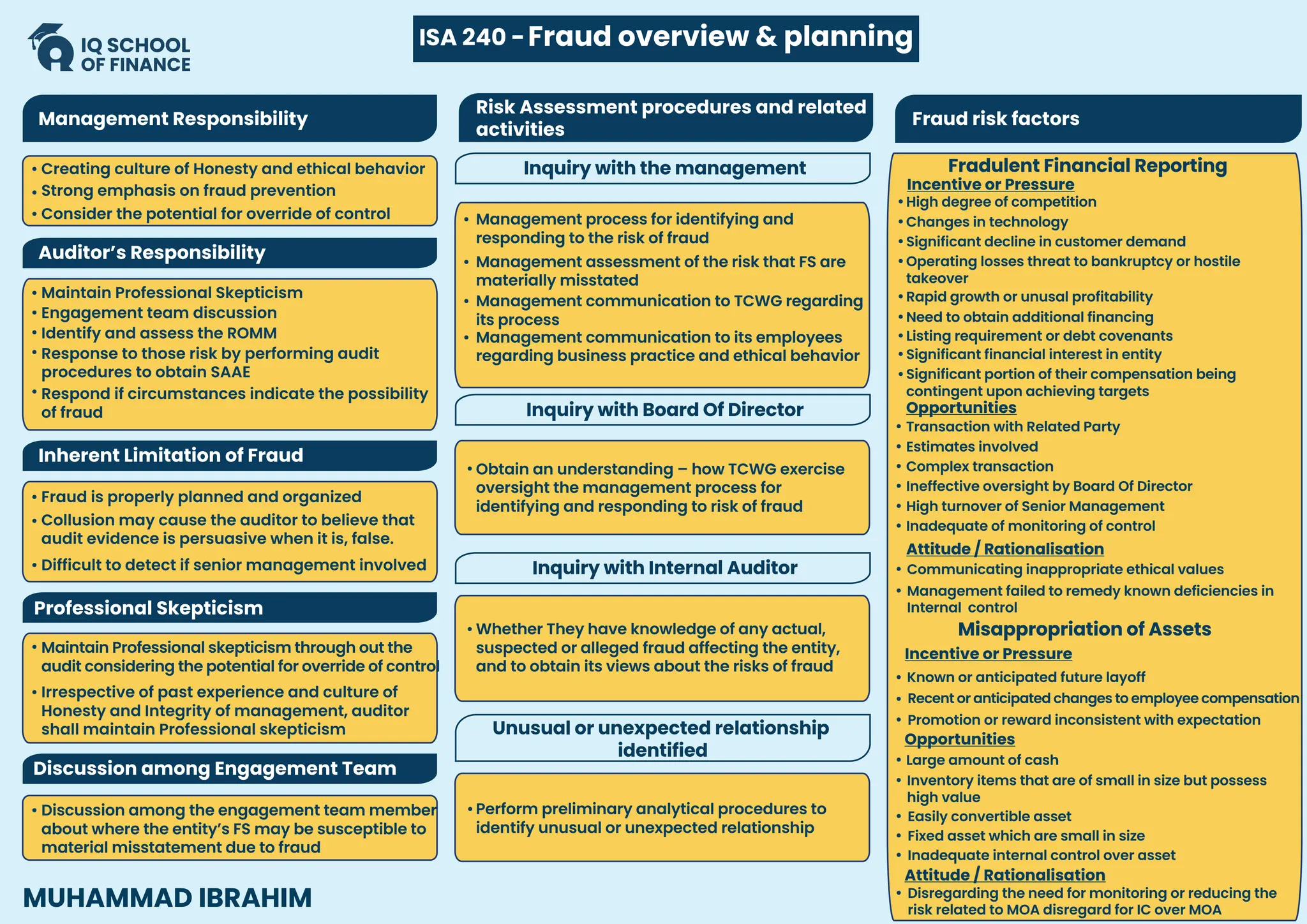

4.

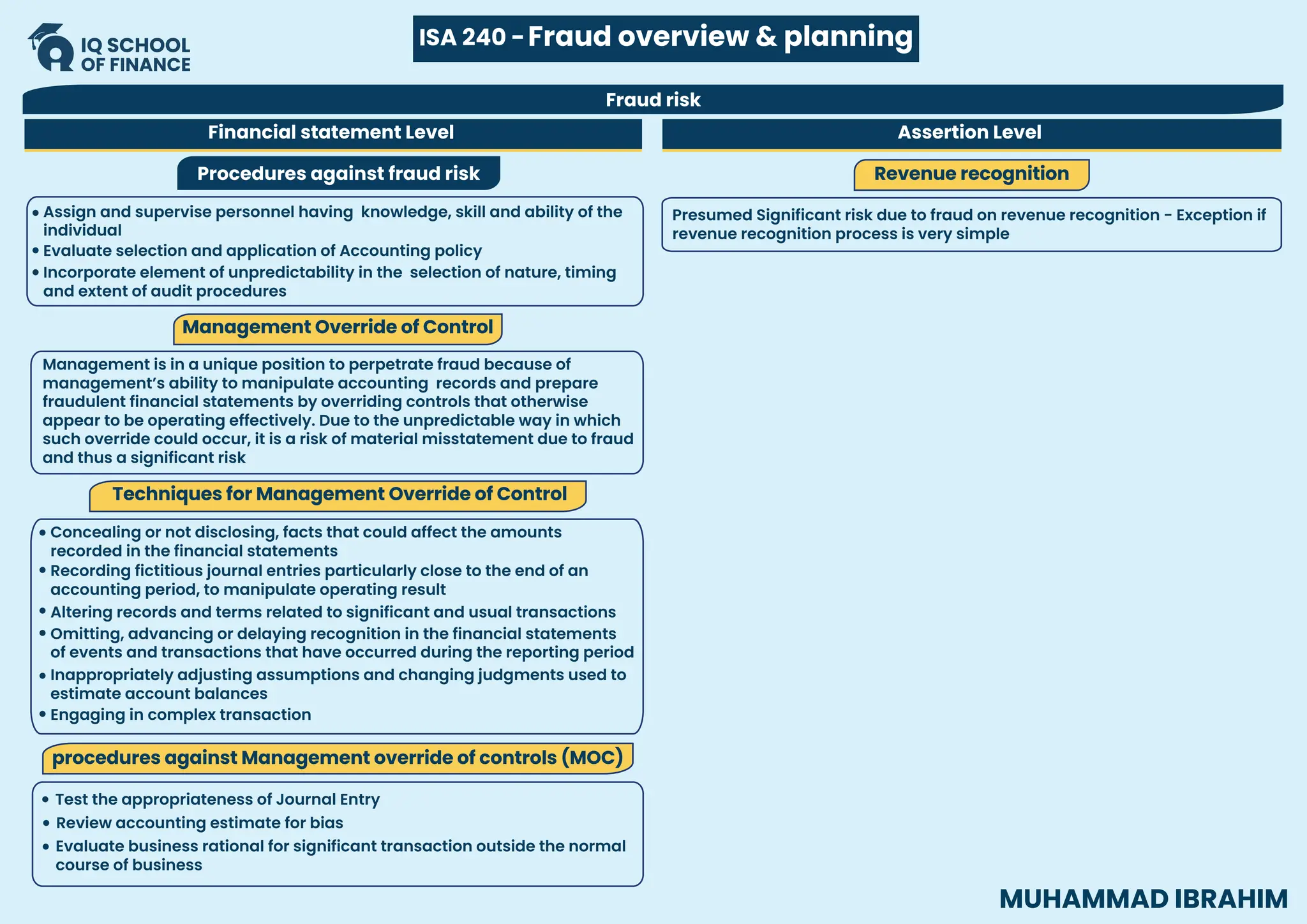

ISA 240 -Fraudoverview & planning

Management Responsibility

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Creating culture of Honesty and ethical behavior

Strong emphasis on fraud prevention

Consider the potential for override of control

Auditor’s Responsibility

Inherent Limitation of Fraud

Professional Skepticism

Discussion among Engagement Team

Maintain Professional Skepticism

Engagement team discussion

Identify and assess the ROMM

Response to those risk by performing audit

procedures to obtain SAAE

Respond if circumstances indicate the possibility

of fraud

Fraud is properly planned and organized

Collusion may cause the auditor to believe that

audit evidence is persuasive when it is, false.

Difficult to detect if senior management involved

Maintain Professional skepticism through out the

audit considering the potential for override of control

Irrespective of past experience and culture of

Honesty and Integrity of management, auditor

shall maintain Professional skepticism

Discussion among the engagement team member

about where the entity’s FS may be susceptible to

material misstatement due to fraud

•

•

•

•

•

•

•

Risk Assessment procedures and related

activities

Inquiry with Board Of Director

Inquiry with Internal Auditor

Inquiry with the management

Management process for identifying and

responding to the risk of fraud

Management assessment of the risk that FS are

materially misstated

Management communication to TCWG regarding

its process

Obtain an understanding – how TCWG exercise

oversight the management process for

identifying and responding to risk of fraud

Whether They have knowledge of any actual,

suspected or alleged fraud affecting the entity,

and to obtain its views about the risks of fraud

Unusual or unexpected relationship

identified

Perform preliminary analytical procedures to

identify unusual or unexpected relationship

Management communication to its employees

regarding business practice and ethical behavior

Fraud risk factors

•

•

•

•

•

•

Opportunities

Inadequate of monitoring of control

Transaction with Related Party

•

Estimates involved

Complex transaction

Ineffective oversight by Board Of Director

High turnover of Senior Management

Attitude / Rationalisation

Communicating inappropriate ethical values

•

• Management failed to remedy known deficiencies in

Internal control

Incentive or Pressure

Misappropriation of Assets

Recent or anticipated changes to employee compensation

Promotion or reward inconsistent with expectation

Known or anticipated future layoff

•

•

•

Opportunities

Large amount of cash

•

• Inventory items that are of small in size but possess

high value

Easily convertible asset

•

•

•

Fixed asset which are small in size

Inadequate internal control over asset

Attitude / Rationalisation

Disregarding the need for monitoring or reducing the

risk related to MOA disregard for IC over MOA

•

•

•

•

•

•

•

•

•

Fradulent Financial Reporting

High degree of competition

Changes in technology

Significant decline in customer demand

Operating losses threat to bankruptcy or hostile

takeover

Rapid growth or unusal profitability

Need to obtain additional financing

Listing requirement or debt covenants

Significant financial interest in entity

Significant portion of their compensation being

contingent upon achieving targets

Incentive or Pressure

MUHAMMAD IBRAHIM

5.

Fraud risk

ISA 240-Fraud overview & planning

MUHAMMAD IBRAHIM

Financial statement Level Assertion Level

Procedures against fraud risk

Management is in a unique position to perpetrate fraud because of

management’s ability to manipulate accounting records and prepare

fraudulent financial statements by overriding controls that otherwise

appear to be operating effectively. Due to the unpredictable way in which

such override could occur, it is a risk of material misstatement due to fraud

and thus a significant risk

Recording fictitious journal entries particularly close to the end of an

accounting period, to manipulate operating result

Concealing or not disclosing, facts that could affect the amounts

recorded in the financial statements

Altering records and terms related to significant and usual transactions

Inappropriately adjusting assumptions and changing judgments used to

estimate account balances

Engaging in complex transaction

Omitting, advancing or delaying recognition in the financial statements

of events and transactions that have occurred during the reporting period

Assign and supervise personnel having knowledge, skill and ability of the

individual

Incorporate element of unpredictability in the selection of nature, timing

and extent of audit procedures

Evaluate selection and application of Accounting policy

Test the appropriateness of Journal Entry

Evaluate business rational for significant transaction outside the normal

course of business

Review accounting estimate for bias

Management Override of Control

procedures against Management override of controls (MOC)

Techniques for Management Override of Control

Presumed Significant risk due to fraud on revenue recognition - Exception if

revenue recognition process is very simple

Revenue recognition

6.

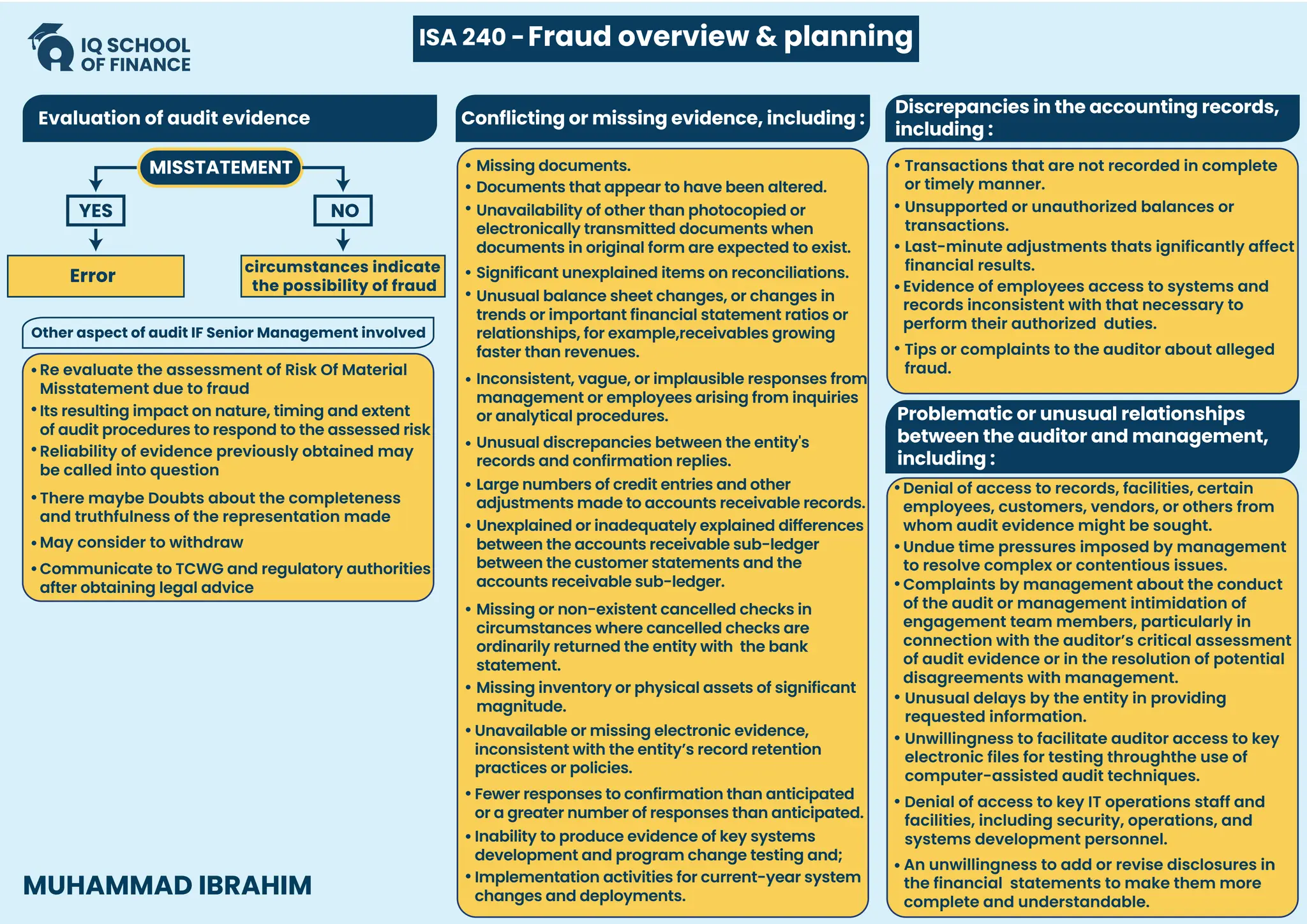

Evaluation of auditevidence

MISSTATEMENT

YES NO

Error

circumstances indicate

the possibility of fraud

Re evaluate the assessment of Risk Of Material

Misstatement due to fraud

Its resulting impact on nature, timing and extent

of audit procedures to respond to the assessed risk

Reliability of evidence previously obtained may

be called into question

There maybe Doubts about the completeness

and truthfulness of the representation made

May consider to withdraw

Communicate to TCWG and regulatory authorities

after obtaining legal advice

Conflicting or missing evidence, including :

Missing documents.

Documents that appear to have been altered.

Unavailability of other than photocopied or

electronically transmitted documents when

documents in original form are expected to exist.

Significant unexplained items on reconciliations.

Unusual balance sheet changes, or changes in

trends or important financial statement ratios or

relationships, for example,receivables growing

faster than revenues.

Inconsistent, vague, or implausible responses from

management or employees arising from inquiries

or analytical procedures.

Unusual discrepancies between the entity's

records and confirmation replies.

Large numbers of credit entries and other

adjustments made to accounts receivable records.

Unexplained or inadequately explained differences

between the accounts receivable sub-ledger

between the customer statements and the

accounts receivable sub-ledger.

Missing inventory or physical assets of significant

magnitude.

Missing or non-existent cancelled checks in

circumstances where cancelled checks are

ordinarily returned the entity with the bank

statement.

Unavailable or missing electronic evidence,

inconsistent with the entity’s record retention

practices or policies.

Fewer responses to confirmation than anticipated

or a greater number of responses than anticipated.

Inability to produce evidence of key systems

development and program change testing and;

Implementation activities for current-year system

changes and deployments.

Discrepancies in the accounting records,

including :

Transactions that are not recorded in complete

or timely manner.

Last-minute adjustments thats ignificantly affect

financial results.

Evidence of employees access to systems and

records inconsistent with that necessary to

perform their authorized duties.

Tips or complaints to the auditor about alleged

fraud.

Unsupported or unauthorized balances or

transactions.

Problematic or unusual relationships

between the auditor and management,

including :

Denial of access to records, facilities, certain

employees, customers, vendors, or others from

whom audit evidence might be sought.

Undue time pressures imposed by management

to resolve complex or contentious issues.

Complaints by management about the conduct

of the audit or management intimidation of

engagement team members, particularly in

connection with the auditor’s critical assessment

of audit evidence or in the resolution of potential

disagreements with management.

Unusual delays by the entity in providing

requested information.

Unwillingness to facilitate auditor access to key

electronic files for testing throughthe use of

computer-assisted audit techniques.

Denial of access to key IT operations staff and

facilities, including security, operations, and

systems development personnel.

An unwillingness to add or revise disclosures in

the financial statements to make them more

complete and understandable.

ISA 240 -Fraud overview & planning

MUHAMMAD IBRAHIM

7.

To obtain anunderstanding

Entity

Environment

Industry

Regulatory

Other external factors

How to obtain an understanding

Observation &

Inspection

Analytical

procedure

These are procedure that assist Auditor in identifying and

assessing the risk of material misstatement at FS level or at

assertion level.

Inquiry

Risk Assessment Procedures

Assessment Of Risk

Complexity

Subjectivity

Change

Uncertainty

Management Bias

ISA 315: AUDIT RISK

Revision Of Risk Assessment

The auditor’s assessment of the risks of material

misstatement at the assertion level may change during

the course of the audit as additional audit evidence is

obtained. The auditor shall revise the assessment and

modify the further planned audit procedures accordingly.

Significant risk are

those risk that

requires special

audit consideration

Internal Control

Risk Factors

FS Level Assertion Level

MUHAMMAD IBRAHIM

Property Plant &

Equipment

Inventory

Revenue

Receivable

A/C Pay

Bank Loan

Security Deposit

Payable

Existance

Completeness

Rights & Obligations

Valuation

What is Audit risk?

Financial statements

may not be equal to

IFRS

IAS 02 Lower of cost

or NRV

IAS 36 PPE Impaired

IAS 36 P&M Impaired

Normal Risk Significant Risk

Operation

Ownership governance structure

Types of investment including

special purpose entities

The way that the entity is

structured & how it is financed

8.

In the eventof becoming aware of information

during the audit that would have caused the

auditor to have determined a different amount

(or amounts) initially

Change in circumstances

Changes in auditors understanding of entity and

operations

New Information

If lower materiality as compared to initially

determined the auditor shall determine whether it

is necessary to revise performance materiality, and

whether the nature, timing and extent of the

further audit procedures remain appropriate

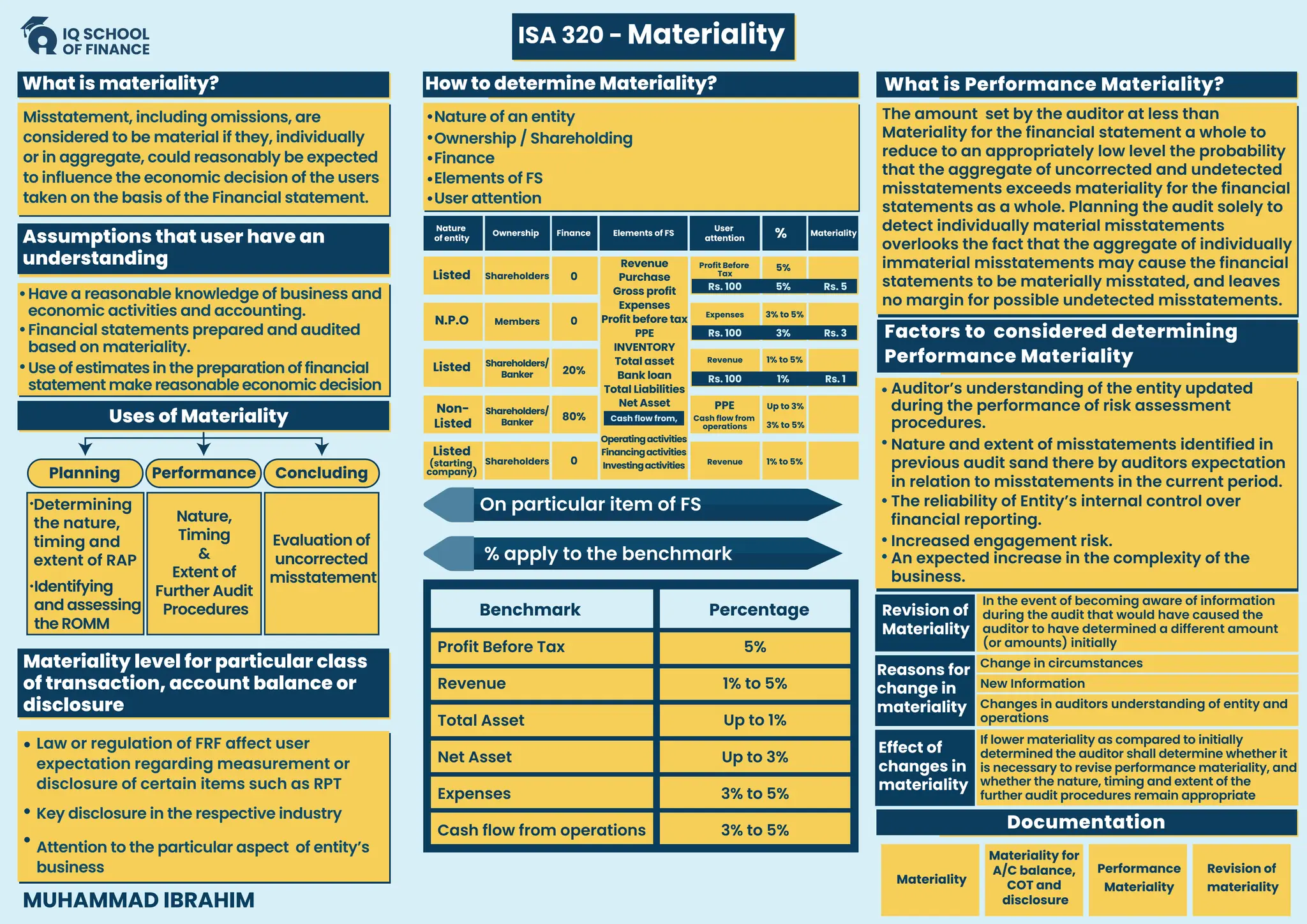

Misstatement, including omissions, are

considered to be material if they, individually

or in aggregate, could reasonably be expected

to influence the economic decision of the users

taken on the basis of the Financial statement.

What is materiality?

Assumptions that user have an

understanding

Uses of Materiality

Concluding

Planning Performance

Nature,

Timing

&

Extent of

Further Audit

Procedures

Evaluation of

uncorrected

misstatement

Factors to considered determining

Performance Materiality

Revision of

Materiality

Reasons for

change in

materiality

Effect of

changes in

materiality

On particular item of FS

% apply to the benchmark

Benchmark Percentage

Profit Before Tax

Revenue

Total Asset

Net Asset

Expenses

Cash flow from operations

5%

1% to 5%

Up to 1%

Up to 3%

3% to 5%

3% to 5%

How to determine Materiality?

Nature

of entity

Ownership Finance Elements of FS

User

attention

Materiality

%

Listed 0

Profit Before

Tax

5%

Shareholders

0

Members

N.P.O

Expenses 3% to 5%

20%

Shareholders/

Banker

Listed

Revenue 1% to 5%

80%

Shareholders/

Banker

Non-

Listed

Cash flow from

operations

Up to 3%

3% to 5%

PPE

0

Shareholders

Listed

(starting

company)

Revenue 1% to 5%

Revenue

Purchase

Gross profit

Expenses

Profit before tax

PPE

INVENTORY

Total asset

Bank loan

Total Liabilities

Net Asset

Cash flow from,

Operatingactivities

Financingactivities

Investingactivities

Rs. 100 5% Rs. 5

Rs. 100 3% Rs. 3

Rs. 100 1% Rs. 1

Determining

the nature,

timing and

extent of RAP

Identifying

and assessing

the ROMM

Materiality level for particular class

of transaction, account balance or

disclosure

Law or regulation of FRF affect user

expectation regarding measurement or

disclosure of certain items such as RPT

Key disclosure in the respective industry

Attention to the particular aspect of entity’s

business

What is Performance Materiality?

The amount set by the auditor at less than

Materiality for the financial statement a whole to

reduce to an appropriately low level the probability

that the aggregate of uncorrected and undetected

misstatements exceeds materiality for the financial

statements as a whole. Planning the audit solely to

detect individually material misstatements

overlooks the fact that the aggregate of individually

immaterial misstatements may cause the financial

statements to be materially misstated, and leaves

no margin for possible undetected misstatements.

Auditor’s understanding of the entity updated

during the performance of risk assessment

procedures.

Nature and extent of misstatements identified in

previous audit sand there by auditors expectation

in relation to misstatements in the current period.

The reliability of Entity’s internal control over

financial reporting.

Increased engagement risk.

An expected increase in the complexity of the

business.

Documentation

Materiality for

A/C balance,

COT and

disclosure

Materiality

Performance

Materiality

Revision of

materiality

ISA 320 - Materiality

MUHAMMAD IBRAHIM

Have a reasonable knowledge of business and

economic activities and accounting.

Nature of an entity

Ownership / Shareholding

Finance

Elements of FS

User attention

Financial statements prepared and audited

based on materiality.

Use of estimates in the preparation of financial

statement make reasonable economic decision

9.

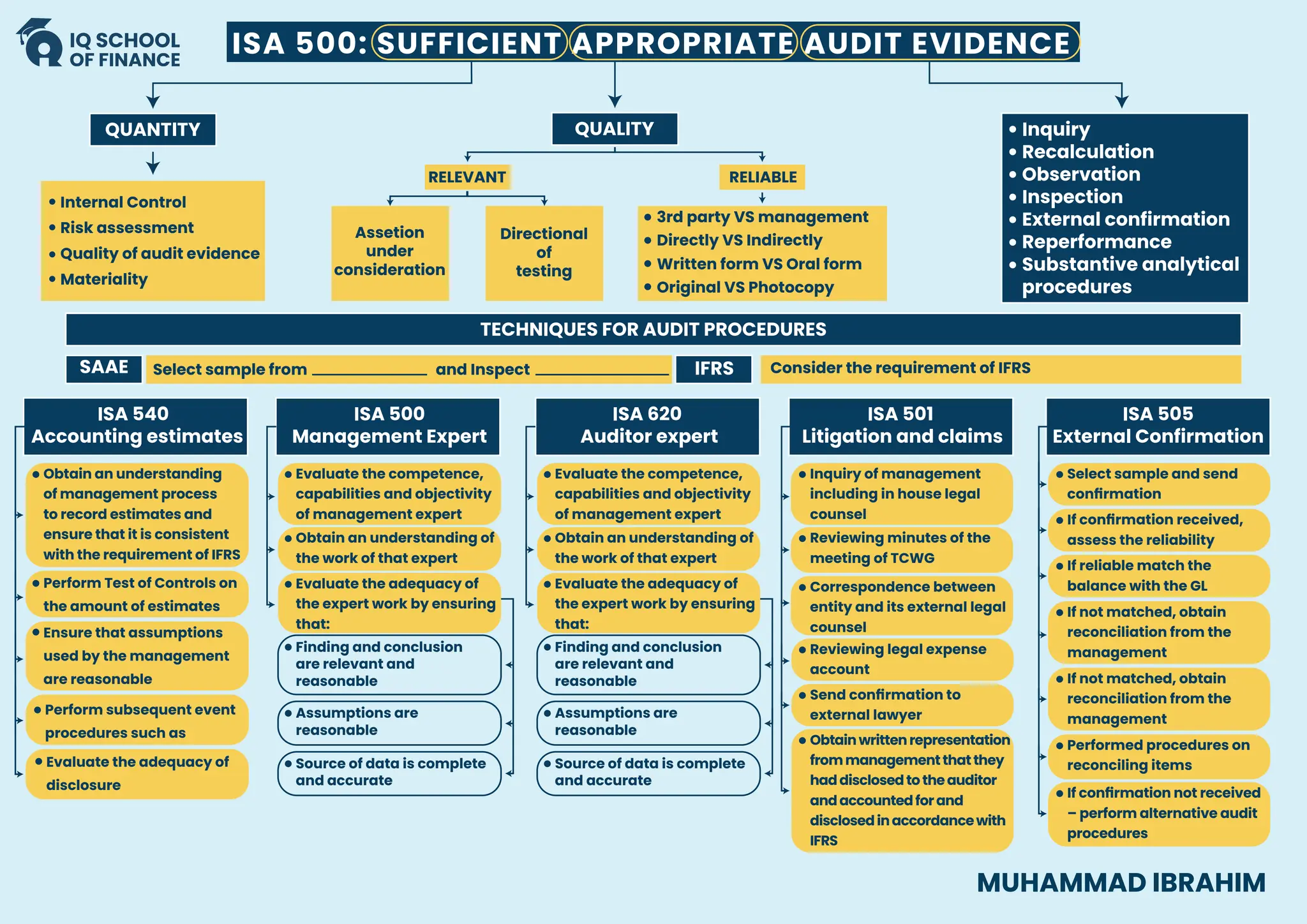

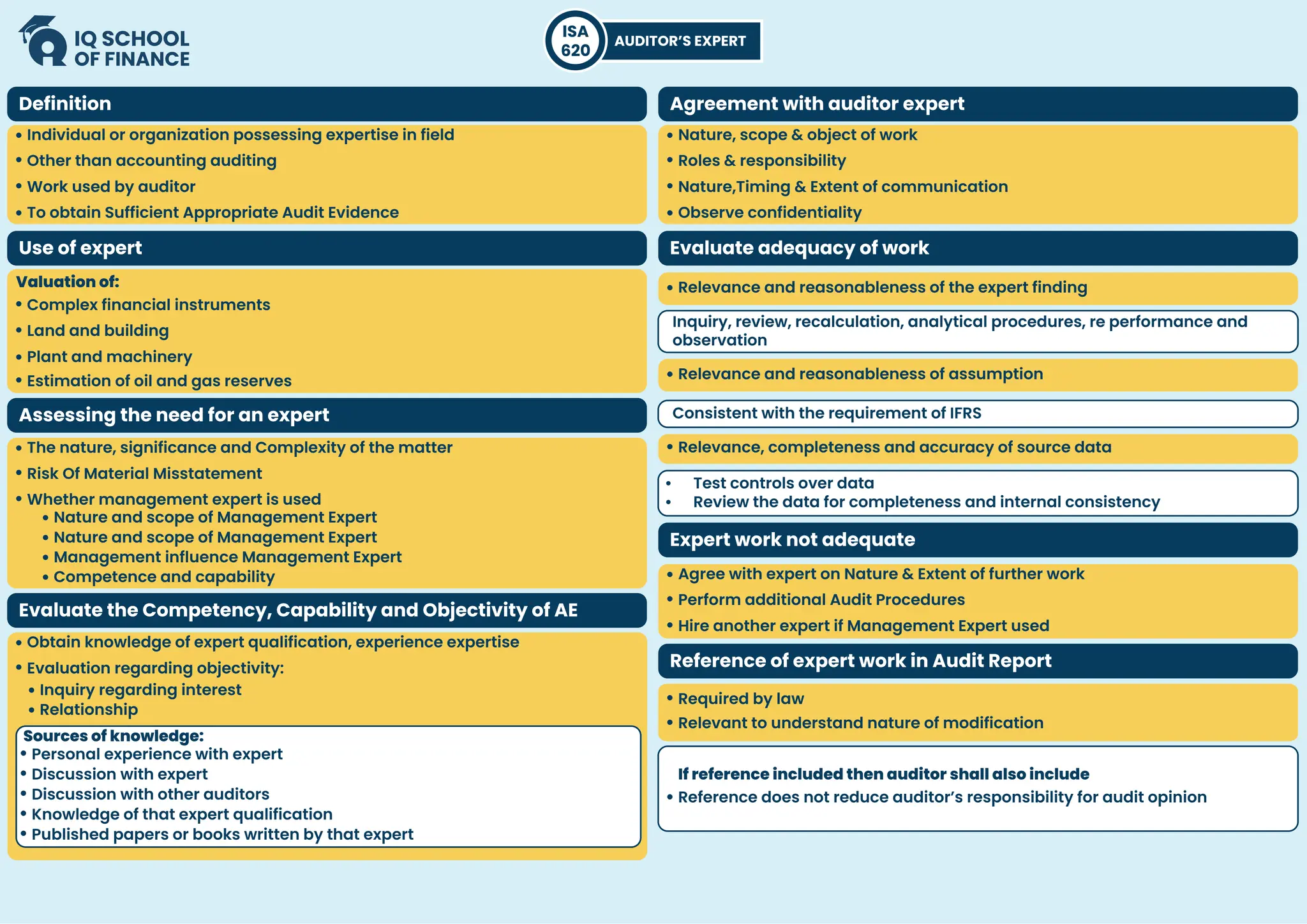

ISA 500: SUFFICIENTAPPROPRIATE AUDIT EVIDENCE

QUANTITY

SAAE IFRS

ISA 540

Accounting estimates

ISA 500

Management Expert

ISA 620

Auditor expert

ISA 501

Litigation and claims

ISA 505

External Confirmation

Internal Control

Risk assessment

Select sample from and Inspect

Quality of audit evidence

Materiality

QUALITY

TECHNIQUES FOR AUDIT PROCEDURES

Inquiry

Recalculation

Observation

Inspection

External confirmation

Reperformance

Substantive analytical

procedures

RELEVANT

Assetion

under

consideration

Directional

of

testing

RELIABLE

Original VS Photocopy

3rd party VS management

Directly VS Indirectly

Written form VS Oral form

Consider the requirement of IFRS

Obtain an understanding

of management process

to record estimates and

ensure that it is consistent

with the requirement of IFRS

Perform Test of Controls on

the amount of estimates

Ensure that assumptions

used by the management

are reasonable

Perform subsequent event

procedures such as

Evaluate the adequacy of

disclosure

Evaluate the competence,

capabilities and objectivity

of management expert

Obtain an understanding of

the work of that expert

Evaluate the adequacy of

the expert work by ensuring

that:

Finding and conclusion

are relevant and

reasonable

Assumptions are

reasonable

Source of data is complete

and accurate

Evaluate the competence,

capabilities and objectivity

of management expert

Inquiry of management

including in house legal

counsel

Select sample and send

confirmation

If confirmation received,

assess the reliability

If reliable match the

balance with the GL

If not matched, obtain

reconciliation from the

management

If not matched, obtain

reconciliation from the

management

Performed procedures on

reconciling items

If confirmation not received

– perform alternative audit

procedures

Reviewing minutes of the

meeting of TCWG

Correspondence between

entity and its external legal

counsel

Reviewing legal expense

account

Send confirmation to

external lawyer

Obtainwrittenrepresentation

frommanagementthatthey

haddisclosedtotheauditor

andaccountedforand

disclosedinaccordancewith

IFRS

Obtain an understanding of

the work of that expert

Evaluate the adequacy of

the expert work by ensuring

that:

Finding and conclusion

are relevant and

reasonable

Assumptions are

reasonable

Source of data is complete

and accurate

MUHAMMAD IBRAHIM

10.

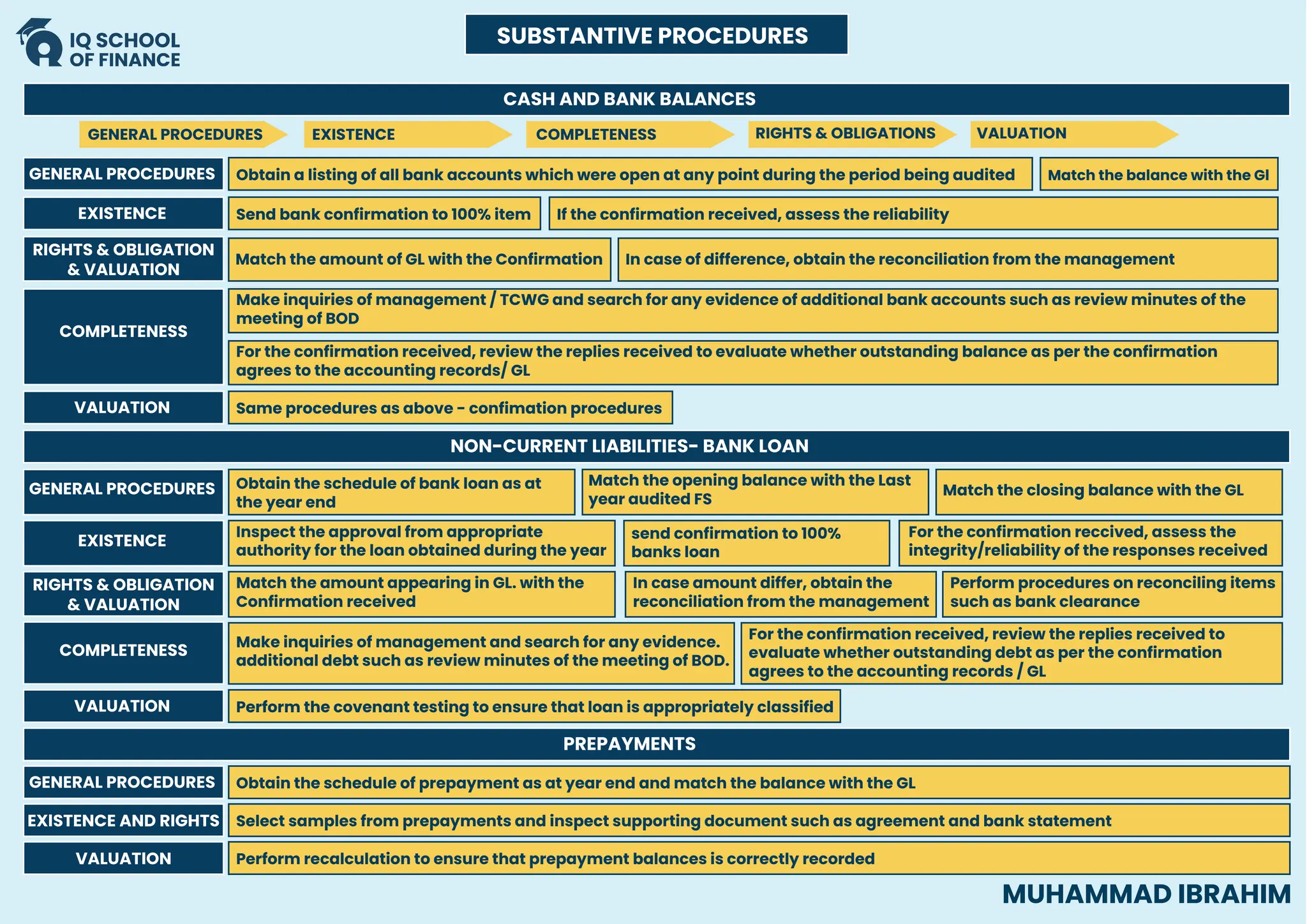

CASH AND BANKBALANCES

NON-CURRENT LIABILITIES- BANK LOAN

PREPAYMENTS

GENERAL PROCEDURES EXISTENCE COMPLETENESS RIGHTS & OBLIGATIONS VALUATION

GENERAL PROCEDURES

GENERAL PROCEDURES

EXISTENCE

RIGHTS & OBLIGATION

& VALUATION

RIGHTS & OBLIGATION

& VALUATION

COMPLETENESS

COMPLETENESS

Obtain a listing of all bank accounts which were open at any point during the period being audited

GENERAL PROCEDURES Obtain the schedule of prepayment as at year end and match the balance with the GL

EXISTENCE AND RIGHTS Select samples from prepayments and inspect supporting document such as agreement and bank statement

Perform recalculation to ensure that prepayment balances is correctly recorded

Obtain the schedule of bank loan as at

the year end

Match the opening balance with the Last

year audited FS

Match the closing balance with the GL

Send bank confirmation to 100% item

EXISTENCE

Inspect the approval from appropriate

authority for the loan obtained during the year

Match the amount appearing in GL. with the

Confirmation received

Make inquiries of management and search for any evidence.

additional debt such as review minutes of the meeting of BOD.

For the confirmation received, review the replies received to

evaluate whether outstanding debt as per the confirmation

agrees to the accounting records / GL

In case amount differ, obtain the

reconciliation from the management

Perform procedures on reconciling items

such as bank clearance

send confirmation to 100%

banks loan

For the confirmation reccived, assess the

integrity/reliability of the responses received

VALUATION Same procedures as above - confimation procedures

VALUATION Perform the covenant testing to ensure that loan is appropriately classified

Make inquiries of management / TCWG and search for any evidence of additional bank accounts such as review minutes of the

meeting of BOD

For the confirmation received, review the replies received to evaluate whether outstanding balance as per the confirmation

agrees to the accounting records/ GL

Match the amount of GL with the Confirmation In case of difference, obtain the reconciliation from the management

If the confirmation received, assess the reliability

Match the balance with the Gl

VALUATION

SUBSTANTIVE PROCEDURES

MUHAMMAD IBRAHIM

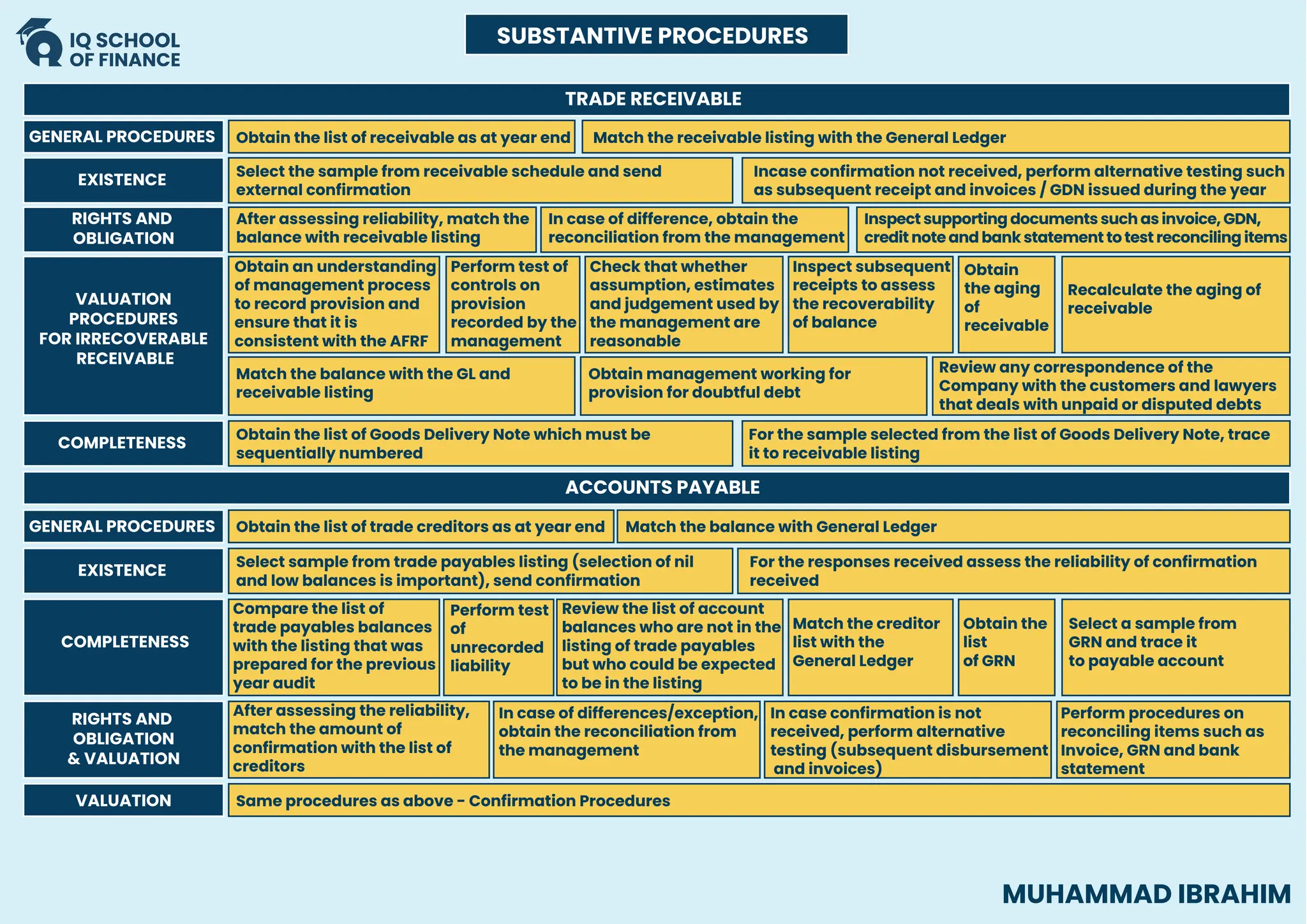

11.

EXISTENCE

Select the samplefrom receivable schedule and send

external confirmation

EXISTENCE

Select sample from trade payables listing (selection of nil

and low balances is important), send confirmation

For the responses received assess the reliability of confirmation

received

COMPLETENESS

Obtain the list of Goods Delivery Note which must be

sequentially numbered

Incase confirmation not received, perform alternative testing such

as subsequent receipt and invoices / GDN issued during the year

Same procedures as above - Confirmation Procedures

VALUATION

TRADE RECEIVABLE

ACCOUNTS PAYABLE

GENERAL PROCEDURES Obtain the list of receivable as at year end

GENERAL PROCEDURES

Match the receivable listing with the General Ledger

RIGHTS AND

OBLIGATION

VALUATION

PROCEDURES

FOR IRRECOVERABLE

RECEIVABLE

After assessing reliability, match the

balance with receivable listing

RIGHTS AND

OBLIGATION

& VALUATION

Obtain an understanding

of management process

to record provision and

ensure that it is

consistent with the AFRF

Obtain management working for

provision for doubtful debt

Review any correspondence of the

Company with the customers and lawyers

that deals with unpaid or disputed debts

Match the balance with the GL and

receivable listing

Perform test of

controls on

provision

recorded by the

management

Check that whether

assumption, estimates

and judgement used by

the management are

reasonable

Inspect subsequent

receipts to assess

the recoverability

of balance

Obtain

the aging

of

receivable

Recalculate the aging of

receivable

COMPLETENESS

In case of difference, obtain the

reconciliation from the management

Inspect supporting documents such as invoice, GDN,

credit note and bank statement to test reconciling items

For the sample selected from the list of Goods Delivery Note, trace

it to receivable listing

Obtain the list of trade creditors as at year end Match the balance with General Ledger

Match the creditor

list with the

General Ledger

Obtain the

list

of GRN

Select a sample from

GRN and trace it

to payable account

Review the list of account

balances who are not in the

listing of trade payables

but who could be expected

to be in the listing

Compare the list of

trade payables balances

with the listing that was

prepared for the previous

year audit

Perform test

of

unrecorded

liability

After assessing the reliability,

match the amount of

confirmation with the list of

creditors

In case of differences/exception,

obtain the reconciliation from

the management

Perform procedures on

reconciling items such as

Invoice, GRN and bank

statement

In case confirmation is not

received, perform alternative

testing (subsequent disbursement

and invoices)

SUBSTANTIVE PROCEDURES

MUHAMMAD IBRAHIM

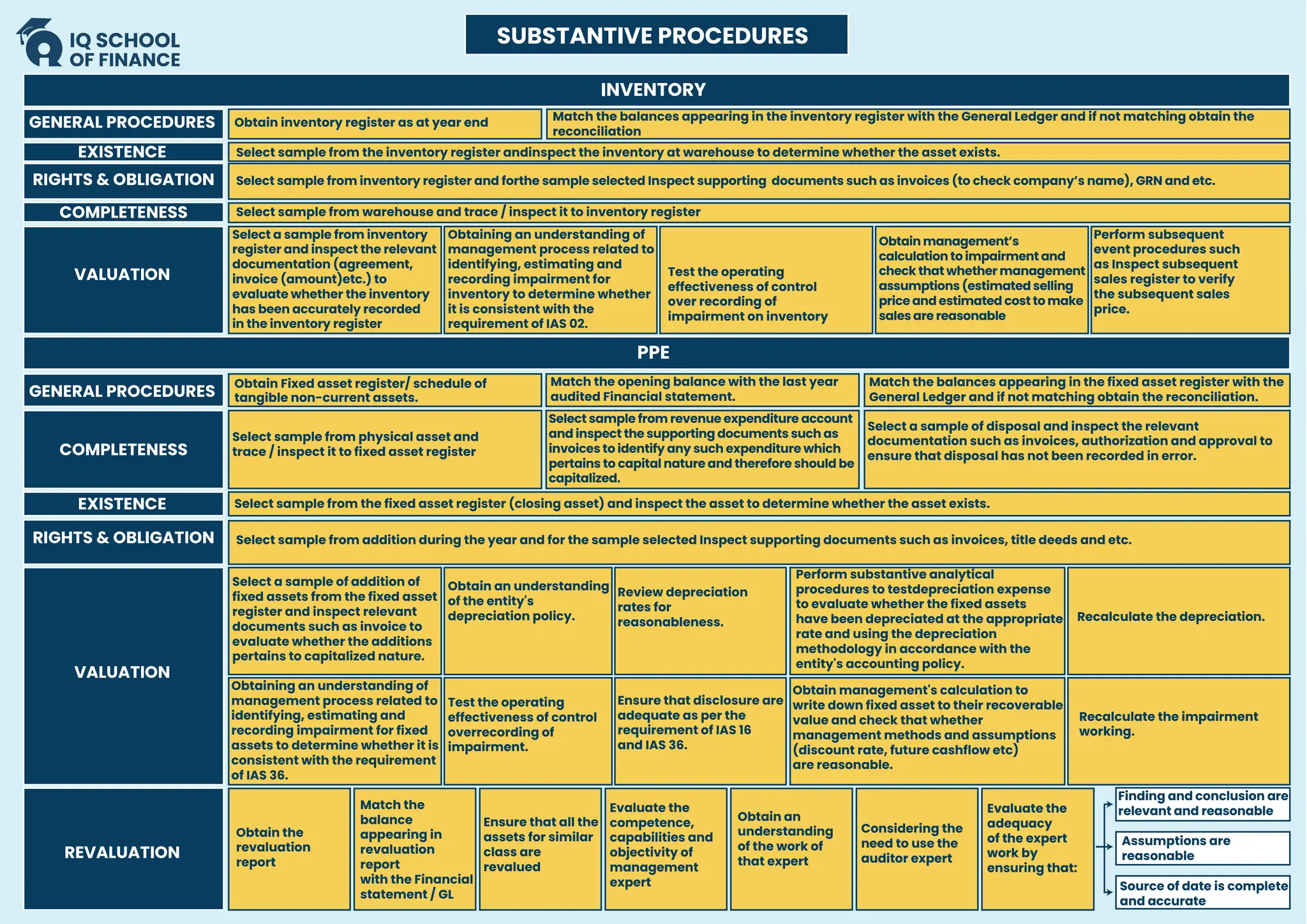

12.

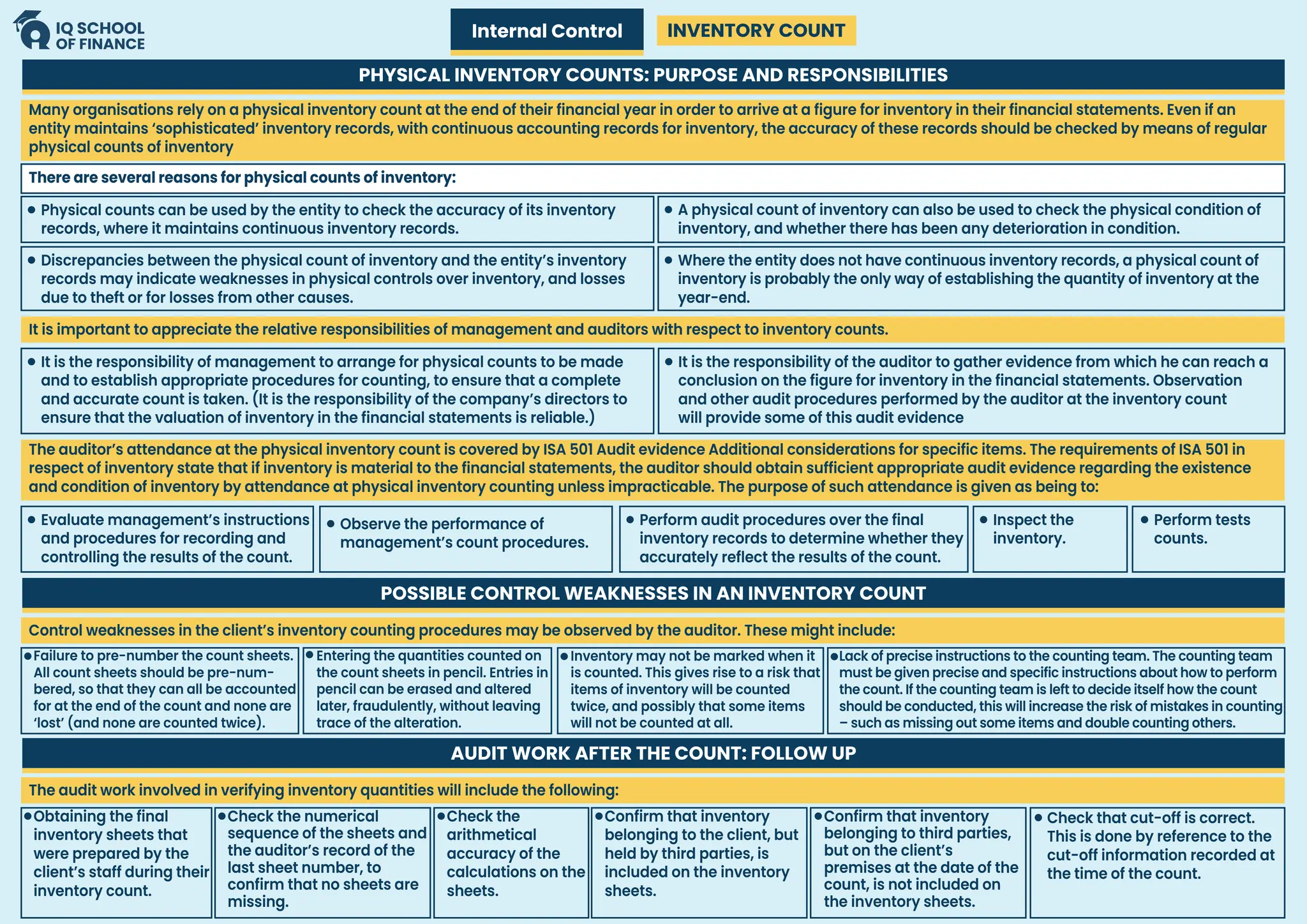

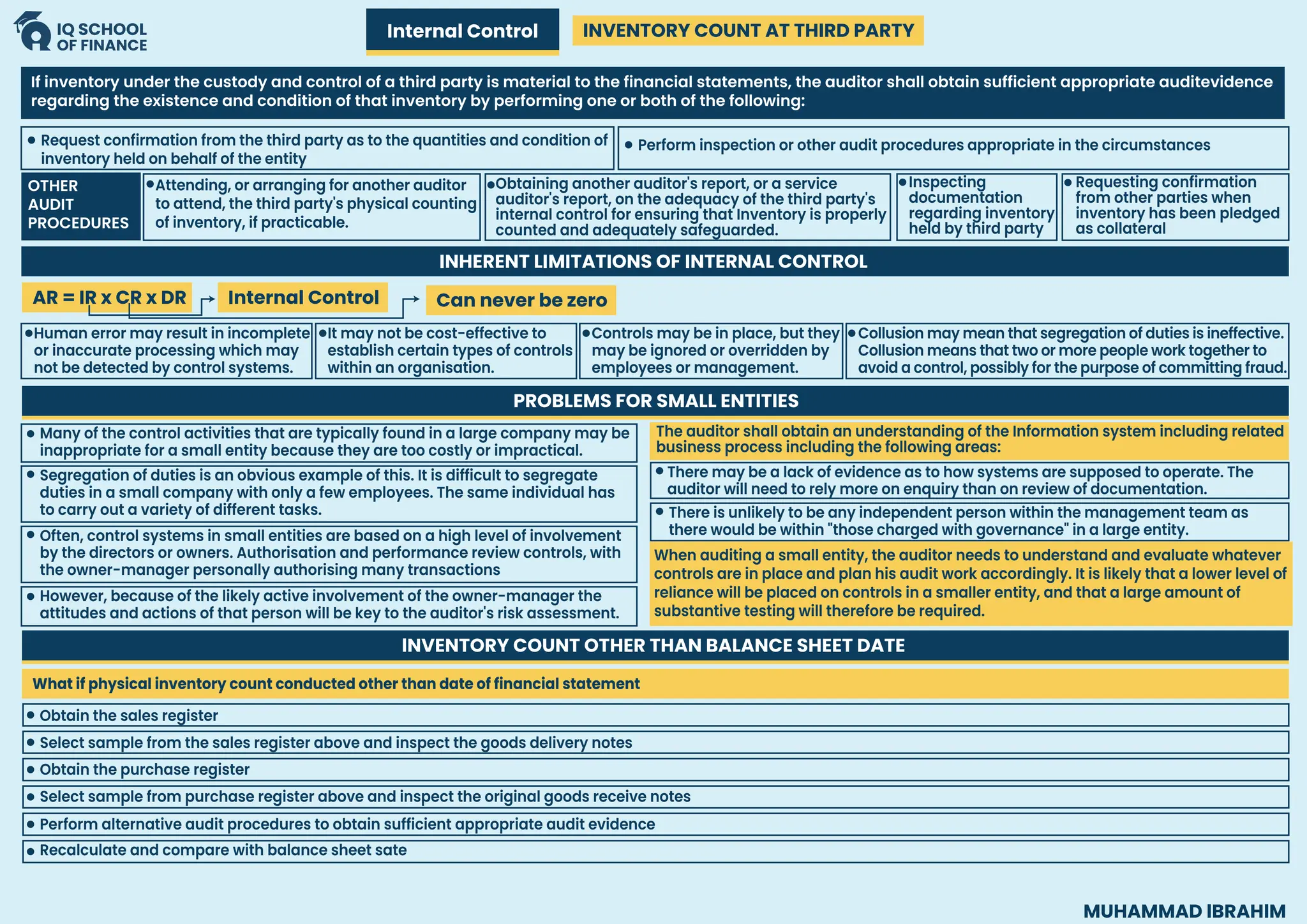

EXISTENCE

RIGHTS & OBLIGATION

COMPLETENESS

VALUATION

Selectsample from the inventory register andinspect the inventory at warehouse to determine whether the asset exists.

EXISTENCE

Select sample from warehouse and trace / inspect it to inventory register

Select sample from inventory register and forthe sample selected Inspect supporting documents such as invoices (to check company’s name), GRN and etc.

RIGHTS & OBLIGATION

INVENTORY

PPE

GENERAL PROCEDURES Obtain inventory register as at year end

GENERAL PROCEDURES

Obtain Fixed asset register/ schedule of

tangible non-current assets.

Match the balances appearing in the inventory register with the General Ledger and if not matching obtain the

reconciliation

Select a sample from inventory

register and inspect the relevant

documentation (agreement,

invoice (amount)etc.) to

evaluate whether the inventory

has been accurately recorded

in the inventory register

Obtaining an understanding of

management process related to

identifying, estimating and

recording impairment for

inventory to determine whether

it is consistent with the

requirement of IAS 02.

Test the operating

effectiveness of control

over recording of

impairment on inventory

Obtain management’s

calculation to impairment and

check that whether management

assumptions (estimated selling

price and estimated cost to make

sales are reasonable

Perform subsequent

event procedures such

as Inspect subsequent

sales register to verify

the subsequent sales

price.

VALUATION

REVALUATION

Match the balances appearing in the fixed asset register with the

General Ledger and if not matching obtain the reconciliation.

Match the opening balance with the last year

audited Financial statement.

Select sample from physical asset and

trace / inspect it to fixed asset register

Select sample from revenue expenditure account

and inspect the supporting documents such as

invoices to identify any such expenditure which

pertains to capital nature and therefore should be

capitalized.

COMPLETENESS

Select a sample of disposal and inspect the relevant

documentation such as invoices, authorization and approval to

ensure that disposal has not been recorded in error.

Select sample from the fixed asset register (closing asset) and inspect the asset to determine whether the asset exists.

Select sample from addition during the year and for the sample selected Inspect supporting documents such as invoices, title deeds and etc.

Select a sample of addition of

fixed assets from the fixed asset

register and inspect relevant

documents such as invoice to

evaluate whether the additions

pertains to capitalized nature.

Perform substantive analytical

procedures to testdepreciation expense

to evaluate whether the fixed assets

have been depreciated at the appropriate

rate and using the depreciation

methodology in accordance with the

entity's accounting policy.

Obtain an understanding

of the entity's

depreciation policy.

Review depreciation

rates for

reasonableness. Recalculate the depreciation.

Obtaining an understanding of

management process related to

identifying, estimating and

recording impairment for fixed

assets to determine whether it is

consistent with the requirement

of IAS 36.

Obtain management's calculation to

write down fixed asset to their recoverable

value and check that whether

management methods and assumptions

(discount rate, future cashflow etc)

are reasonable.

Test the operating

effectiveness of control

overrecording of

impairment.

Recalculate the impairment

working.

Ensure that disclosure are

adequate as per the

requirement of IAS 16

and IAS 36.

Match the

balance

appearing in

revaluation

report

with the Financial

statement / GL

Ensure that all the

assets for similar

class are

revalued

Evaluate the

competence,

capabilities and

objectivity of

management

expert

Evaluate the

adequacy

of the expert

work by

ensuring that:

Obtain an

understanding

of the work of

that expert

Considering the

need to use the

auditor expert

Obtain the

revaluation

report

Finding and conclusion are

relevant and reasonable

Assumptions are

reasonable

Source of date is complete

and accurate

SUBSTANTIVE PROCEDURES

13.

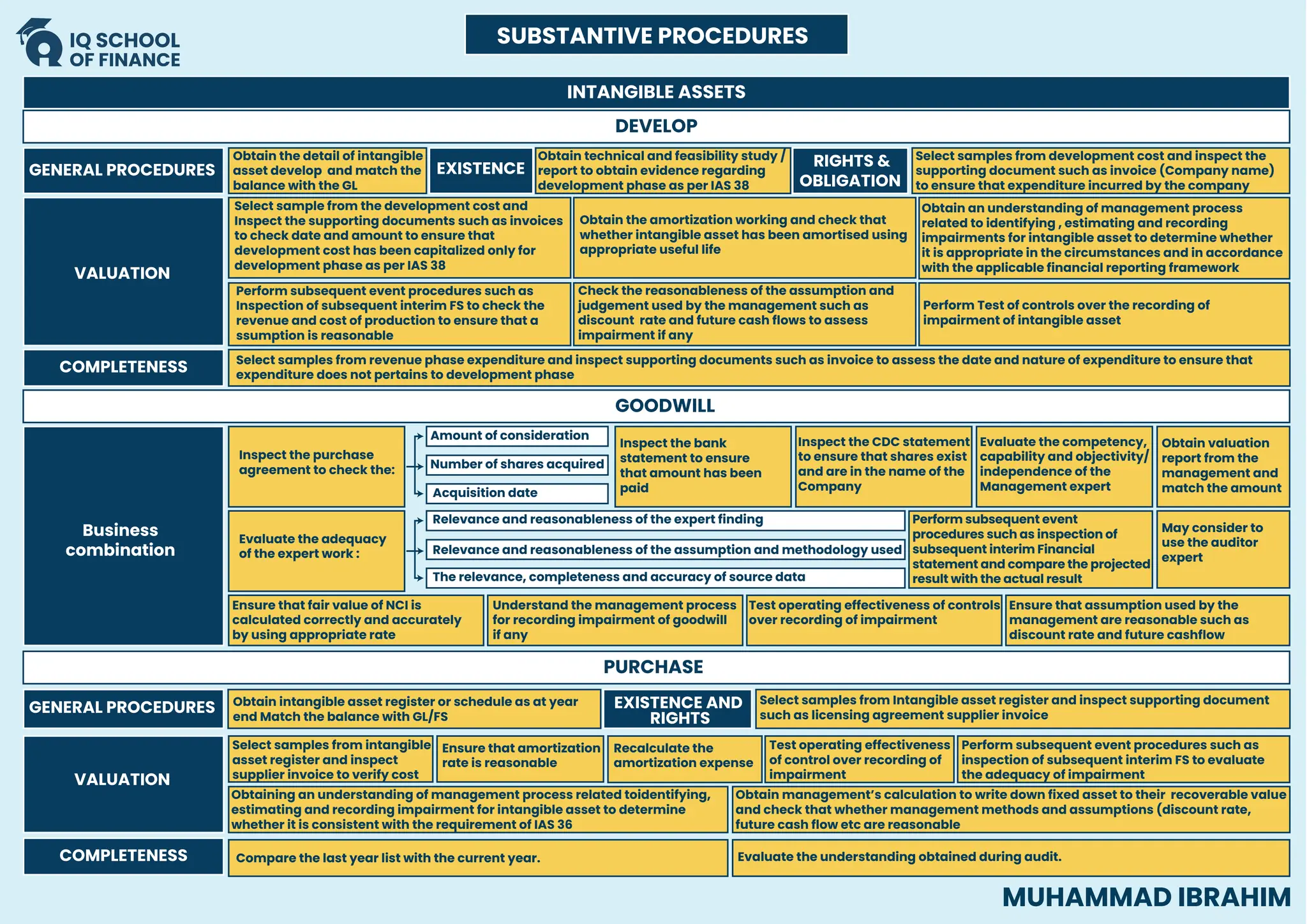

INTANGIBLE ASSETS

DEVELOP

GOODWILL

PURCHASE

GENERAL PROCEDURES

COMPLETENESS

VALUATION

Obtainthe detail of intangible

asset develop and match the

balance with the GL

GENERAL PROCEDURES

Obtain technical and feasibility study /

report to obtain evidence regarding

development phase as per IAS 38

EXISTENCE RIGHTS &

OBLIGATION

Select samples from development cost and inspect the

supporting document such as invoice (Company name)

to ensure that expenditure incurred by the company

Select sample from the development cost and

Inspect the supporting documents such as invoices

to check date and amount to ensure that

development cost has been capitalized only for

development phase as per IAS 38

Obtain the amortization working and check that

whether intangible asset has been amortised using

appropriate useful life

Select samples from revenue phase expenditure and inspect supporting documents such as invoice to assess the date and nature of expenditure to ensure that

expenditure does not pertains to development phase

COMPLETENESS

Obtain an understanding of management process

related to identifying , estimating and recording

impairments for intangible asset to determine whether

it is appropriate in the circumstances and in accordance

with the applicable financial reporting framework

Perform Test of controls over the recording of

impairment of intangible asset

Check the reasonableness of the assumption and

judgement used by the management such as

discount rate and future cash flows to assess

impairment if any

Perform subsequent event procedures such as

Inspection of subsequent interim FS to check the

revenue and cost of production to ensure that a

ssumption is reasonable

VALUATION

Business

combination

Inspect the purchase

agreement to check the:

Amount of consideration

Number of shares acquired

Acquisition date

Inspect the bank

statement to ensure

that amount has been

paid

Inspect the CDC statement

to ensure that shares exist

and are in the name of the

Company

Obtain valuation

report from the

management and

match the amount

Evaluate the competency,

capability and objectivity/

independence of the

Management expert

Evaluate the adequacy

of the expert work :

Relevance and reasonableness of the expert finding

Relevance and reasonableness of the assumption and methodology used

The relevance, completeness and accuracy of source data

May consider to

use the auditor

expert

Understand the management process

for recording impairment of goodwill

if any

Test operating effectiveness of controls

over recording of impairment

Ensure that assumption used by the

management are reasonable such as

discount rate and future cashflow

Ensure that fair value of NCI is

calculated correctly and accurately

by using appropriate rate

Obtain intangible asset register or schedule as at year

end Match the balance with GL/FS

Select samples from Intangible asset register and inspect supporting document

such as licensing agreement supplier invoice

EXISTENCE AND

RIGHTS

Obtain management’s calculation to write down fixed asset to their recoverable value

and check that whether management methods and assumptions (discount rate,

future cash flow etc are reasonable

Obtaining an understanding of management process related toidentifying,

estimating and recording impairment for intangible asset to determine

whether it is consistent with the requirement of IAS 36

Select samples from intangible

asset register and inspect

supplier invoice to verify cost

Recalculate the

amortization expense

Ensure that amortization

rate is reasonable

Test operating effectiveness

of control over recording of

impairment

Perform subsequent event procedures such as

inspection of subsequent interim FS to evaluate

the adequacy of impairment

Evaluate the understanding obtained during audit.

Compare the last year list with the current year.

SUBSTANTIVE PROCEDURES

Perform subsequent event

procedures such as inspection of

subsequent interim Financial

statement and compare the projected

result with the actual result

MUHAMMAD IBRAHIM

14.

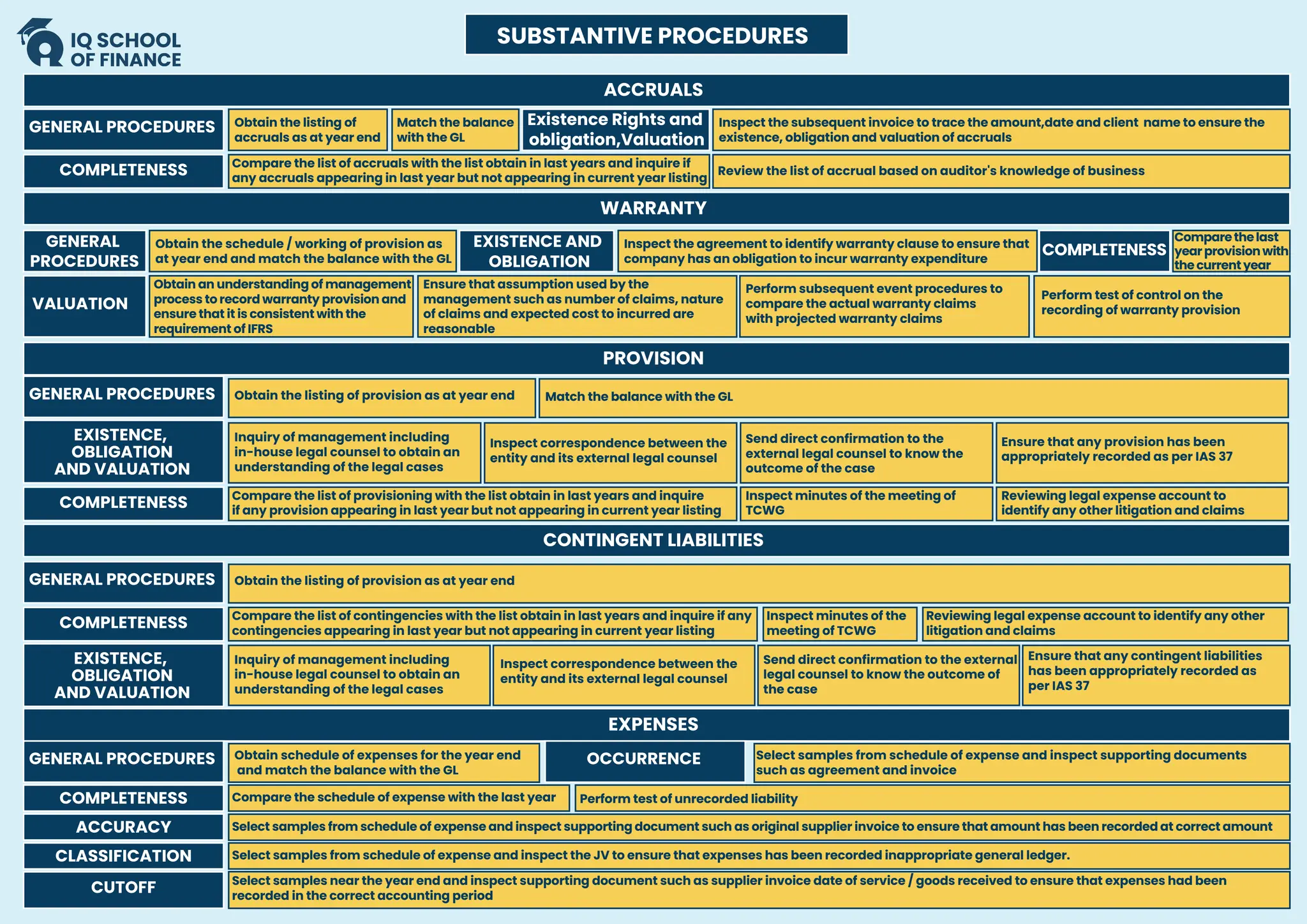

ACCRUALS

PROVISION

CONTINGENT LIABILITIES

EXPENSES

WARRANTY

GENERAL PROCEDURES

GENERALPROCEDURES

EXISTENCE,

OBLIGATION

AND VALUATION

EXISTENCE,

OBLIGATION

AND VALUATION

Obtain the listing of

accruals as at year end

GENERAL

PROCEDURES

Obtain the schedule / working of provision as

at year end and match the balance with the GL

Obtain the listing of provision as at year end

GENERAL PROCEDURES Obtain the listing of provision as at year end

GENERAL PROCEDURES Obtain schedule of expenses for the year end

and match the balance with the GL

OCCURRENCE Select samples from schedule of expense and inspect supporting documents

such as agreement and invoice

Inquiry of management including

in-house legal counsel to obtain an

understanding of the legal cases

Inquiry of management including

in-house legal counsel to obtain an

understanding of the legal cases

Inspect correspondence between the

entity and its external legal counsel

Send direct confirmation to the external

legal counsel to know the outcome of

the case

Ensure that any contingent liabilities

has been appropriately recorded as

per IAS 37

Inspect correspondence between the

entity and its external legal counsel

Send direct confirmation to the

external legal counsel to know the

outcome of the case

Ensure that any provision has been

appropriately recorded as per IAS 37

Match the balance with the GL

Inspect the agreement to identify warranty clause to ensure that

company has an obligation to incur warranty expenditure

Inspect the subsequent invoice to trace the amount,date and client name to ensure the

existence, obligation and valuation of accruals

Match the balance

with the GL

Existence Rights and

obligation,Valuation

EXISTENCE AND

OBLIGATION

COMPLETENESS Compare the list of accruals with the list obtain in last years and inquire if

any accruals appearing in last year but not appearing in current year listing

COMPLETENESS Compare the list of contingencies with the list obtain in last years and inquire if any

contingencies appearing in last year but not appearing in current year listing

Inspect minutes of the

meeting of TCWG

Reviewing legal expense account to identify any other

litigation and claims

COMPLETENESS Compare the list of provisioning with the list obtain in last years and inquire

if any provision appearing in last year but not appearing in current year listing

COMPLETENESS

ACCURACY

CLASSIFICATION

CUTOFF

Compare the schedule of expense with the last year

Select samples from schedule of expense and inspect supporting document such as original supplier invoice to ensure that amount has been recorded at correct amount

Select samples from schedule of expense and inspect the JV to ensure that expenses has been recorded inappropriate general ledger.

Select samples near the year end and inspect supporting document such as supplier invoice date of service / goods received to ensure that expenses had been

recorded in the correct accounting period

Perform test of unrecorded liability

Inspect minutes of the meeting of

TCWG

Reviewing legal expense account to

identify any other litigation and claims

COMPLETENESS

Comparethelast

yearprovisionwith

thecurrentyear

Review the list of accrual based on auditor's knowledge of business

VALUATION

Ensure that assumption used by the

management such as number of claims, nature

of claims and expected cost to incurred are

reasonable

Perform subsequent event procedures to

compare the actual warranty claims

with projected warranty claims

Perform test of control on the

recording of warranty provision

Obtain an understanding of management

process to record warranty provision and

ensure that it is consistent with the

requirement of IFRS

SUBSTANTIVE PROCEDURES

15.

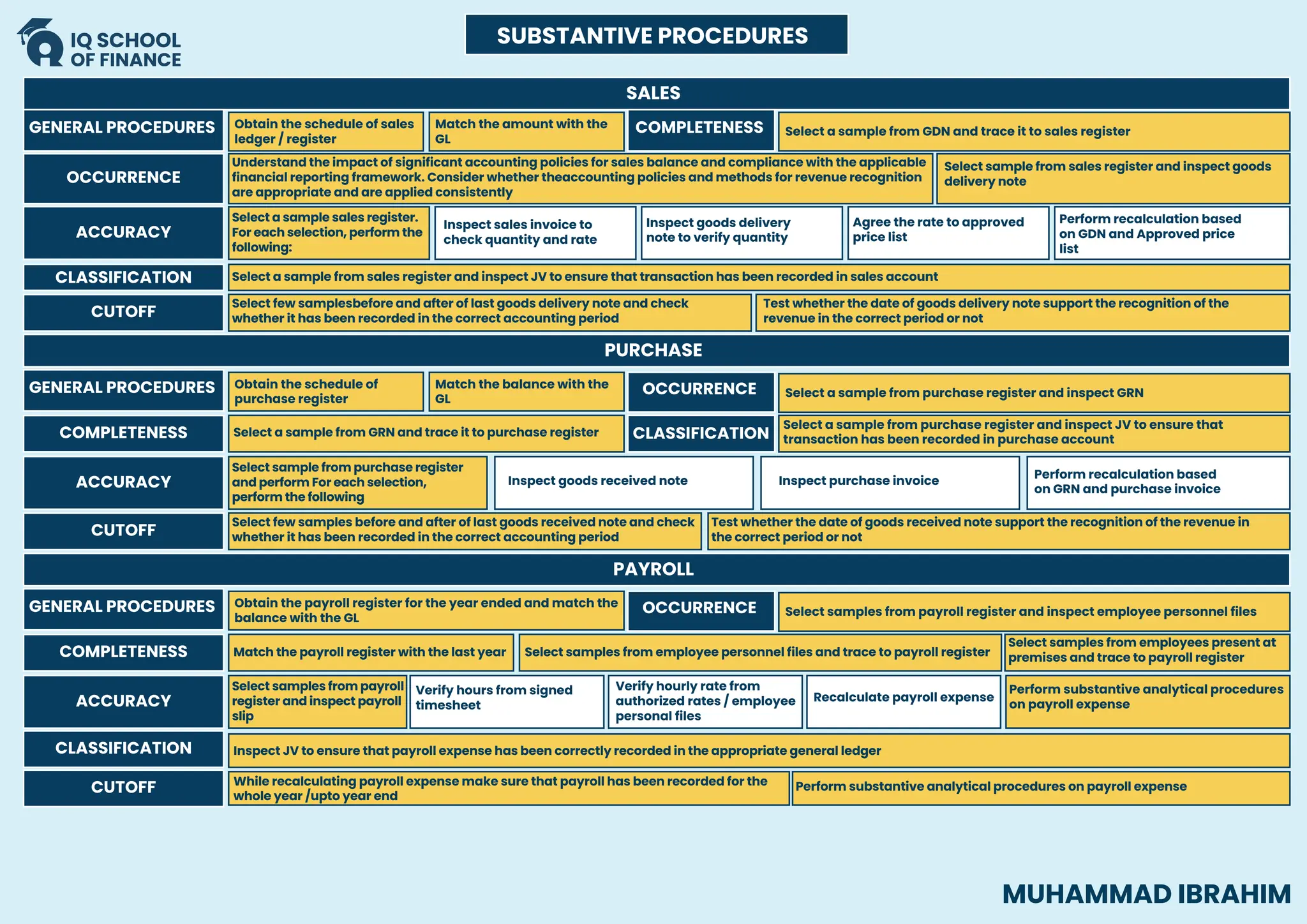

SALES

PURCHASE

GENERAL PROCEDURES Obtainthe schedule of sales

ledger / register

Match the amount with the

GL

GENERAL PROCEDURES Obtain the schedule of

purchase register

Match the balance with the

GL

COMPLETENESS Select a sample from GDN and trace it to sales register

OCCURRENCE

CLASSIFICATION

Select a sample from purchase register and inspect GRN

Select a sample from purchase register and inspect JV to ensure that

transaction has been recorded in purchase account

OCCURRENCE

ACCURACY

ACCURACY

CLASSIFICATION

CUTOFF

Understand the impact of significant accounting policies for sales balance and compliance with the applicable

financial reporting framework. Consider whether theaccounting policies and methods for revenue recognition

are appropriate and are applied consistently

Select sample from sales register and inspect goods

delivery note

Select a sample sales register.

For each selection, perform the

following:

Select sample from purchase register

and perform For each selection,

perform the following

Inspect sales invoice to

check quantity and rate

Inspect goods received note Inspect purchase invoice

Perform recalculation based

on GRN and purchase invoice

Inspect goods delivery

note to verify quantity

Agree the rate to approved

price list

Perform recalculation based

on GDN and Approved price

list

Select a sample from sales register and inspect JV to ensure that transaction has been recorded in sales account

Select few samplesbefore and after of last goods delivery note and check

whether it has been recorded in the correct accounting period

CUTOFF

Select few samples before and after of last goods received note and check

whether it has been recorded in the correct accounting period

Test whether the date of goods received note support the recognition of the revenue in

the correct period or not

COMPLETENESS Select a sample from GRN and trace it to purchase register

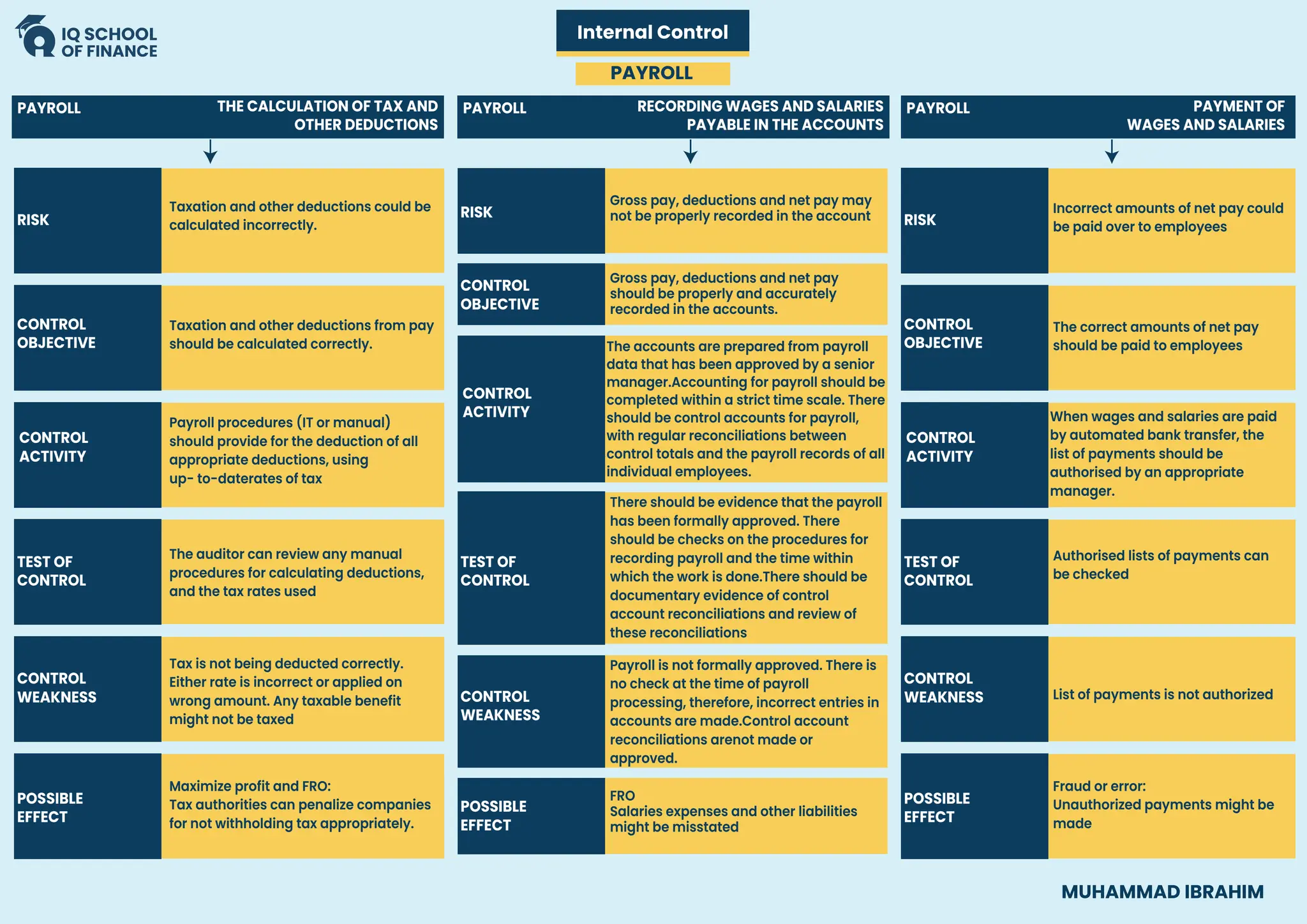

PAYROLL

GENERAL PROCEDURES Obtain the payroll register for the year ended and match the

balance with the GL

OCCURRENCE Select samples from payroll register and inspect employee personnel files

ACCURACY

Select samples from payroll

register and inspect payroll

slip

Perform substantive analytical procedures

on payroll expense

Verify hours from signed

timesheet

Verify hourly rate from

authorized rates / employee

personal files

Recalculate payroll expense

CUTOFF

Inspect JV to ensure that payroll expense has been correctly recorded in the appropriate general ledger

While recalculating payroll expense make sure that payroll has been recorded for the

whole year /upto year end

Perform substantive analytical procedures on payroll expense

COMPLETENESS Match the payroll register with the last year Select samples from employee personnel files and trace to payroll register

Test whether the date of goods delivery note support the recognition of the

revenue in the correct period or not

Select samples from employees present at

premises and trace to payroll register

CLASSIFICATION

SUBSTANTIVE PROCEDURES

MUHAMMAD IBRAHIM

16.

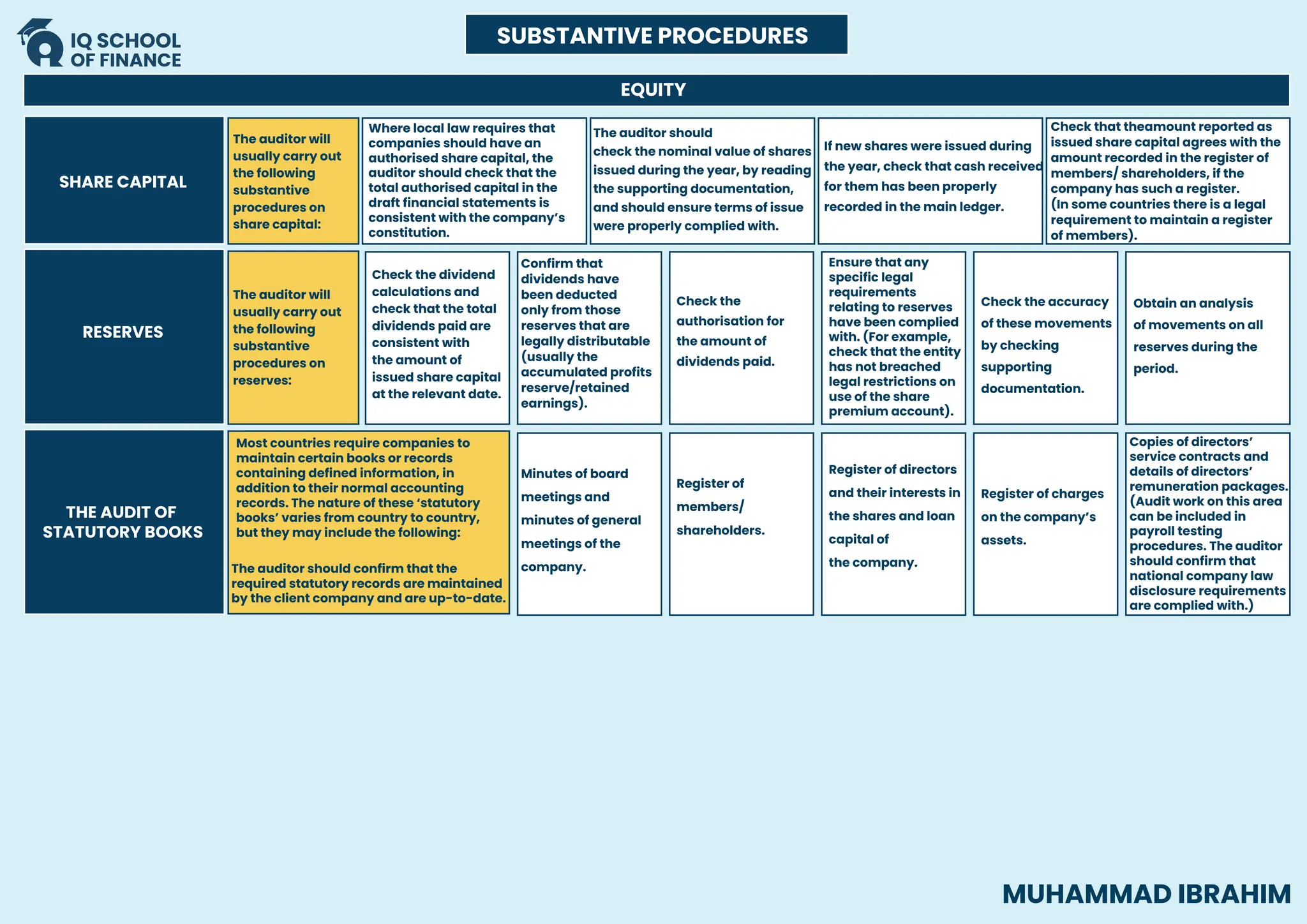

EQUITY

SHARE CAPITAL

The auditorwill

usually carry out

the following

substantive

procedures on

share capital:

Where local law requires that

companies should have an

authorised share capital, the

auditor should check that the

total authorised capital in the

draft financial statements is

consistent with the company’s

constitution.

The auditor should

check the nominal value of shares

issued during the year, by reading

the supporting documentation,

and should ensure terms of issue

were properly complied with.

If new shares were issued during

the year, check that cash received

for them has been properly

recorded in the main ledger.

Check that theamount reported as

issued share capital agrees with the

amount recorded in the register of

members/ shareholders, if the

company has such a register.

(In some countries there is a legal

requirement to maintain a register

of members).

RESERVES

THE AUDIT OF

STATUTORY BOOKS

The auditor will

usually carry out

the following

substantive

procedures on

reserves:

Most countries require companies to

maintain certain books or records

containing defined information, in

addition to their normal accounting

records. The nature of these ‘statutory

books’ varies from country to country,

but they may include the following:

The auditor should confirm that the

required statutory records are maintained

by the client company and are up-to-date.

Check the dividend

calculations and

check that the total

dividends paid are

consistent with

the amount of

issued share capital

at the relevant date.

Confirm that

dividends have

been deducted

only from those

reserves that are

legally distributable

(usually the

accumulated profits

reserve/retained

earnings).

Check the

authorisation for

the amount of

dividends paid.

Ensure that any

specific legal

requirements

relating to reserves

have been complied

with. (For example,

check that the entity

has not breached

legal restrictions on

use of the share

premium account).

Check the accuracy

of these movements

by checking

supporting

documentation.

Obtain an analysis

of movements on all

reserves during the

period.

Minutes of board

meetings and

minutes of general

meetings of the

company.

Register of

members/

shareholders.

Register of directors

and their interests in

the shares and loan

capital of

the company.

Register of charges

on the company’s

assets.

Copies of directors’

service contracts and

details of directors’

remuneration packages.

(Audit work on this area

can be included in

payroll testing

procedures. The auditor

should confirm that

national company law

disclosure requirements

are complied with.)

SUBSTANTIVE PROCEDURES

MUHAMMAD IBRAHIM

17.

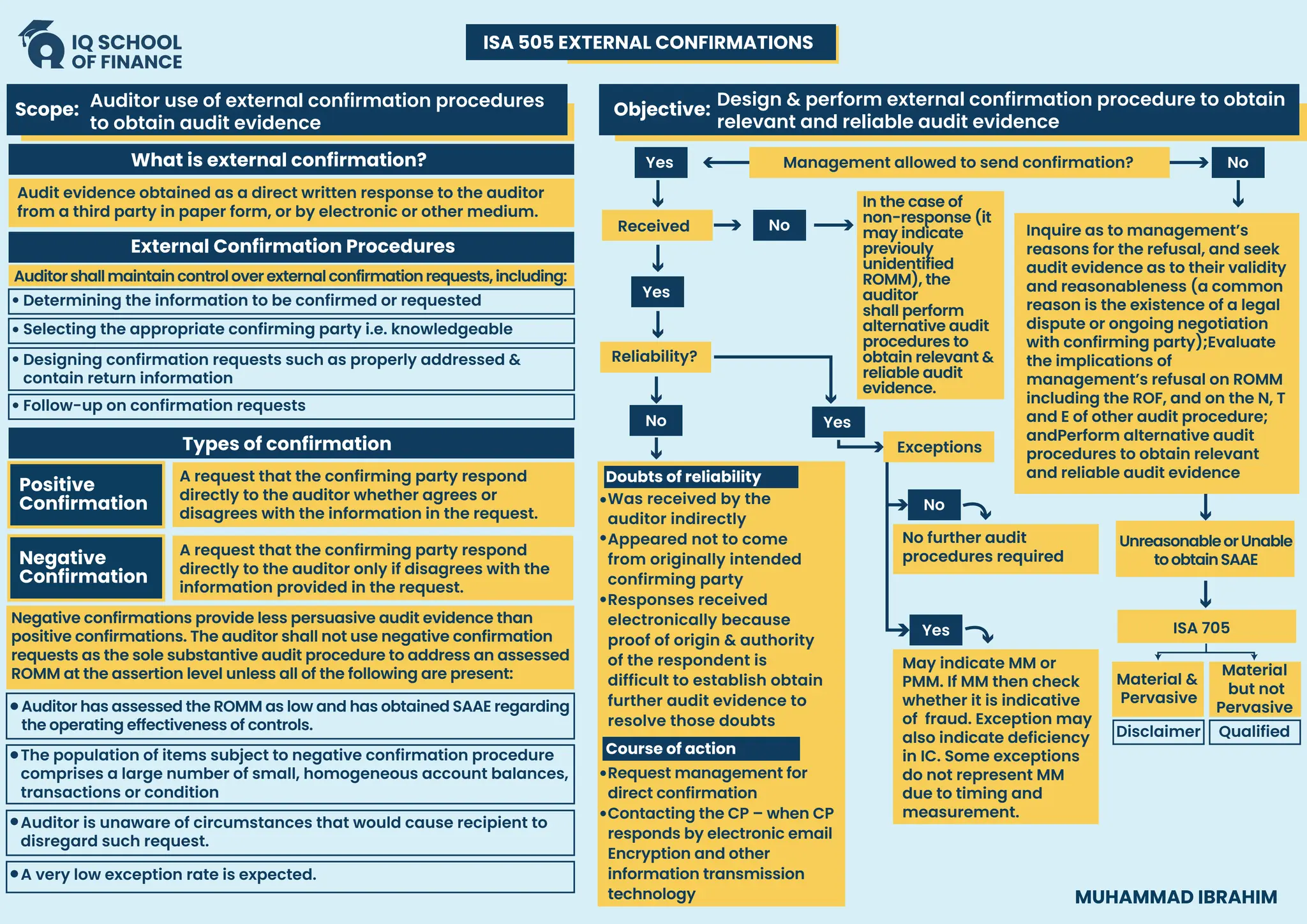

ISA 505 EXTERNALCONFIRMATIONS

MUHAMMAD IBRAHIM

What is external confirmation?

External Confirmation Procedures

Types of confirmation

Auditor use of external confirmation procedures

to obtain audit evidence

Scope: Objective:

Audit evidence obtained as a direct written response to the auditor

from a third party in paper form, or by electronic or other medium.

Positive

Confirmation

Negative

Confirmation

Auditorshallmaintaincontroloverexternalconfirmationrequests,including:

Determining the information to be confirmed or requested

Selecting the appropriate confirming party i.e. knowledgeable

Designing confirmation requests such as properly addressed &

contain return information

Follow-up on confirmation requests

A request that the confirming party respond

directly to the auditor whether agrees or

disagrees with the information in the request.

A request that the confirming party respond

directly to the auditor only if disagrees with the

information provided in the request.

Negative confirmations provide less persuasive audit evidence than

positive confirmations. The auditor shall not use negative confirmation

requests as the sole substantive audit procedure to address an assessed

ROMM at the assertion level unless all of the following are present:

Design & perform external confirmation procedure to obtain

relevant and reliable audit evidence

Yes

Yes

No

No

Yes

Received

Reliability?

No

No Inquire as to management’s

reasons for the refusal, and seek

audit evidence as to their validity

and reasonableness (a common

reason is the existence of a legal

dispute or ongoing negotiation

with confirming party);Evaluate

the implications of

management’s refusal on ROMM

including the ROF, and on the N, T

and E of other audit procedure;

andPerform alternative audit

procedures to obtain relevant

and reliable audit evidence

Was received by the

auditor indirectly

Appeared not to come

from originally intended

confirming party

Responses received

electronically because

proof of origin & authority

of the respondent is

difficult to establish obtain

further audit evidence to

resolve those doubts

Request management for

direct confirmation

Contacting the CP – when CP

responds by electronic email

Encryption and other

information transmission

technology

In the case of

non-response (it

may indicate

previouly

unidentified

ROMM), the

auditor

shall perform

alternative audit

procedures to

obtain relevant &

reliable audit

evidence.

Exceptions

Doubts of reliability

Course of action

No further audit

procedures required

Yes

May indicate MM or

PMM. If MM then check

whether it is indicative

of fraud. Exception may

also indicate deficiency

in IC. Some exceptions

do not represent MM

due to timing and

measurement.

UnreasonableorUnable

toobtainSAAE

ISA 705

Material &

Pervasive

Material

but not

Pervasive

Management allowed to send confirmation?

Auditor has assessed the ROMM as low and has obtained SAAE regarding

the operating effectiveness of controls.

The population of items subject to negative confirmation procedure

comprises a large number of small, homogeneous account balances,

transactions or condition

Auditor is unaware of circumstances that would cause recipient to

disregard such request.

A very low exception rate is expected.

Disclaimer Qualified

18.

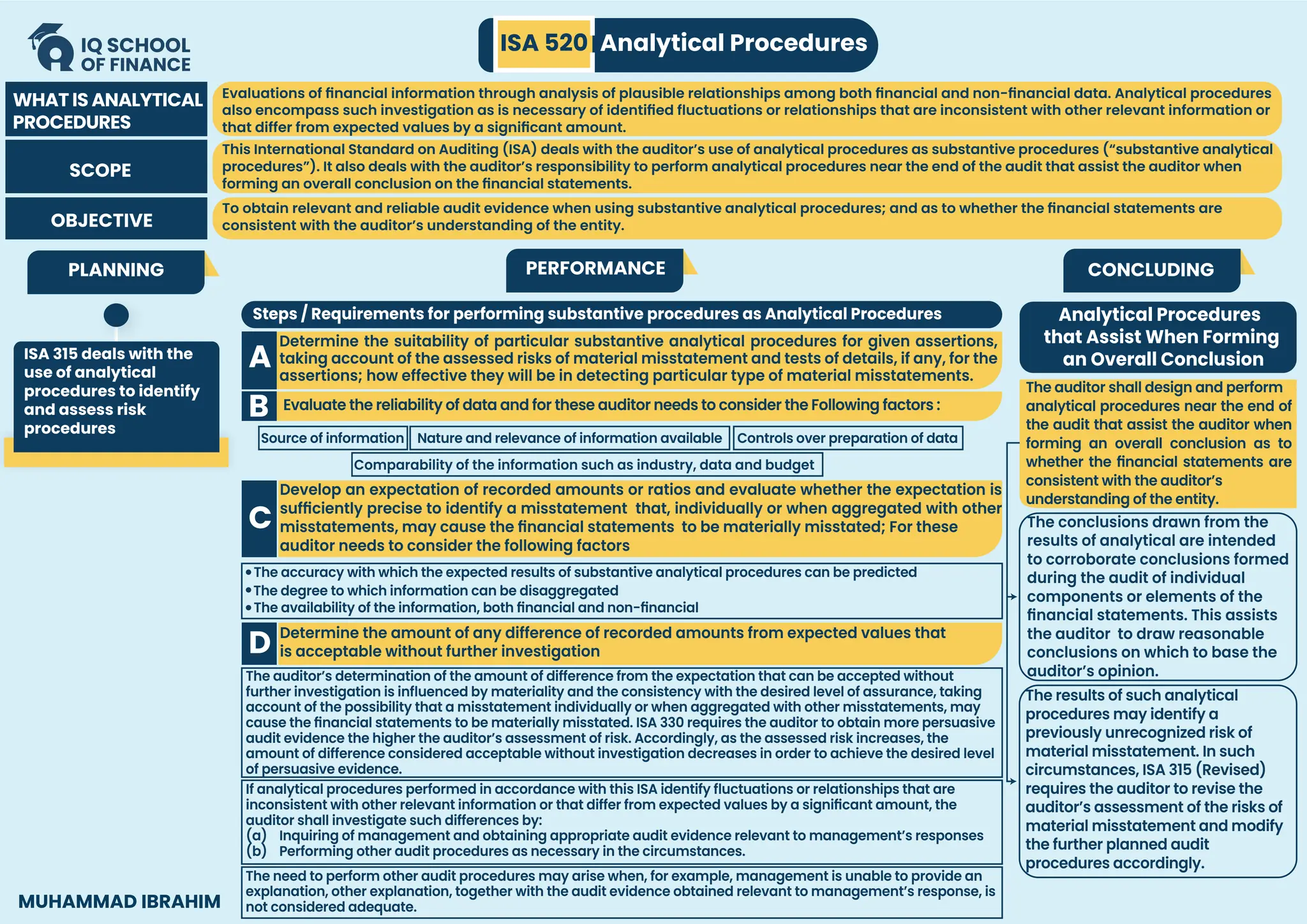

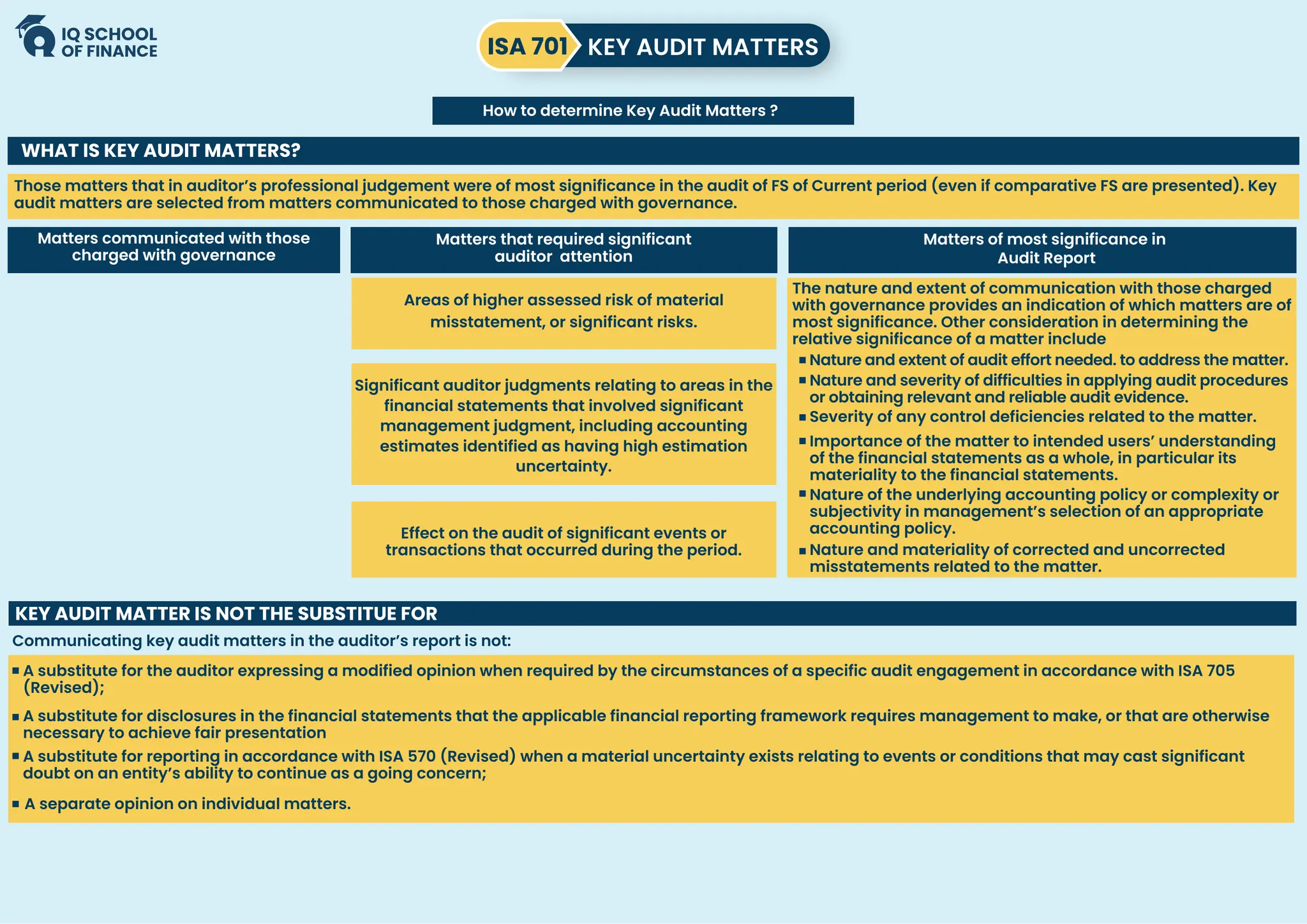

ISA 520 AnalyticalProcedures

Evaluations of financial information through analysis of plausible relationships among both financial and non-financial data. Analytical procedures

also encompass such investigation as is necessary of identified fluctuations or relationships that are inconsistent with other relevant information or

that differ from expected values by a significant amount.

This International Standard on Auditing (ISA) deals with the auditor’s use of analytical procedures as substantive procedures (“substantive analytical

procedures”). It also deals with the auditor’s responsibility to perform analytical procedures near the end of the audit that assist the auditor when

forming an overall conclusion on the financial statements.

To obtain relevant and reliable audit evidence when using substantive analytical procedures; and as to whether the financial statements are

consistent with the auditor’s understanding of the entity.

WHAT IS ANALYTICAL

PROCEDURES

SCOPE

OBJECTIVE

PLANNING

ISA 315 deals with the

use of analytical

procedures to identify

and assess risk

procedures

PERFORMANCE CONCLUDING

Steps / Requirements for performing substantive procedures as Analytical Procedures

Determine the suitability of particular substantive analytical procedures for given assertions,

taking account of the assessed risks of material misstatement and tests of details, if any, for the

assertions; how effective they will be in detecting particular type of material misstatements.

A

B Evaluate the reliability of data and for these auditor needs to consider the Following factors :

C

Source of information

Comparability of the information such as industry, data and budget

Nature and relevance of information available Controls over preparation of data

Develop an expectation of recorded amounts or ratios and evaluate whether the expectation is

sufficiently precise to identify a misstatement that, individually or when aggregated with other

misstatements, may cause the financial statements to be materially misstated; For these

auditor needs to consider the following factors

D

The conclusions drawn from the

results of analytical are intended

to corroborate conclusions formed

during the audit of individual

components or elements of the

financial statements. This assists

the auditor to draw reasonable

conclusions on which to base the

auditor’s opinion.

The results of such analytical

procedures may identify a

previously unrecognized risk of

material misstatement. In such

circumstances, ISA 315 (Revised)

requires the auditor to revise the

auditor’s assessment of the risks of

material misstatement and modify

the further planned audit

procedures accordingly.

Analytical Procedures

that Assist When Forming

an Overall Conclusion

The auditor shall design and perform

analytical procedures near the end of

the audit that assist the auditor when

forming an overall conclusion as to

whether the financial statements are

consistent with the auditor’s

understanding of the entity.

The accuracy with which the expected results of substantive analytical procedures can be predicted

The degree to which information can be disaggregated

The availability of the information, both financial and non-financial

Determine the amount of any difference of recorded amounts from expected values that

is acceptable without further investigation

The auditor’s determination of the amount of difference from the expectation that can be accepted without

further investigation is influenced by materiality and the consistency with the desired level of assurance, taking

account of the possibility that a misstatement individually or when aggregated with other misstatements, may

cause the financial statements to be materially misstated. ISA 330 requires the auditor to obtain more persuasive

audit evidence the higher the auditor’s assessment of risk. Accordingly, as the assessed risk increases, the

amount of difference considered acceptable without investigation decreases in order to achieve the desired level

of persuasive evidence.

If analytical procedures performed in accordance with this ISA identify fluctuations or relationships that are

inconsistent with other relevant information or that differ from expected values by a significant amount, the

auditor shall investigate such differences by:

(a) Inquiring of management and obtaining appropriate audit evidence relevant to management’s responses

(b) Performing other audit procedures as necessary in the circumstances.

The need to perform other audit procedures may arise when, for example, management is unable to provide an

explanation, other explanation, together with the audit evidence obtained relevant to management’s response, is

not considered adequate.

MUHAMMAD IBRAHIM

19.

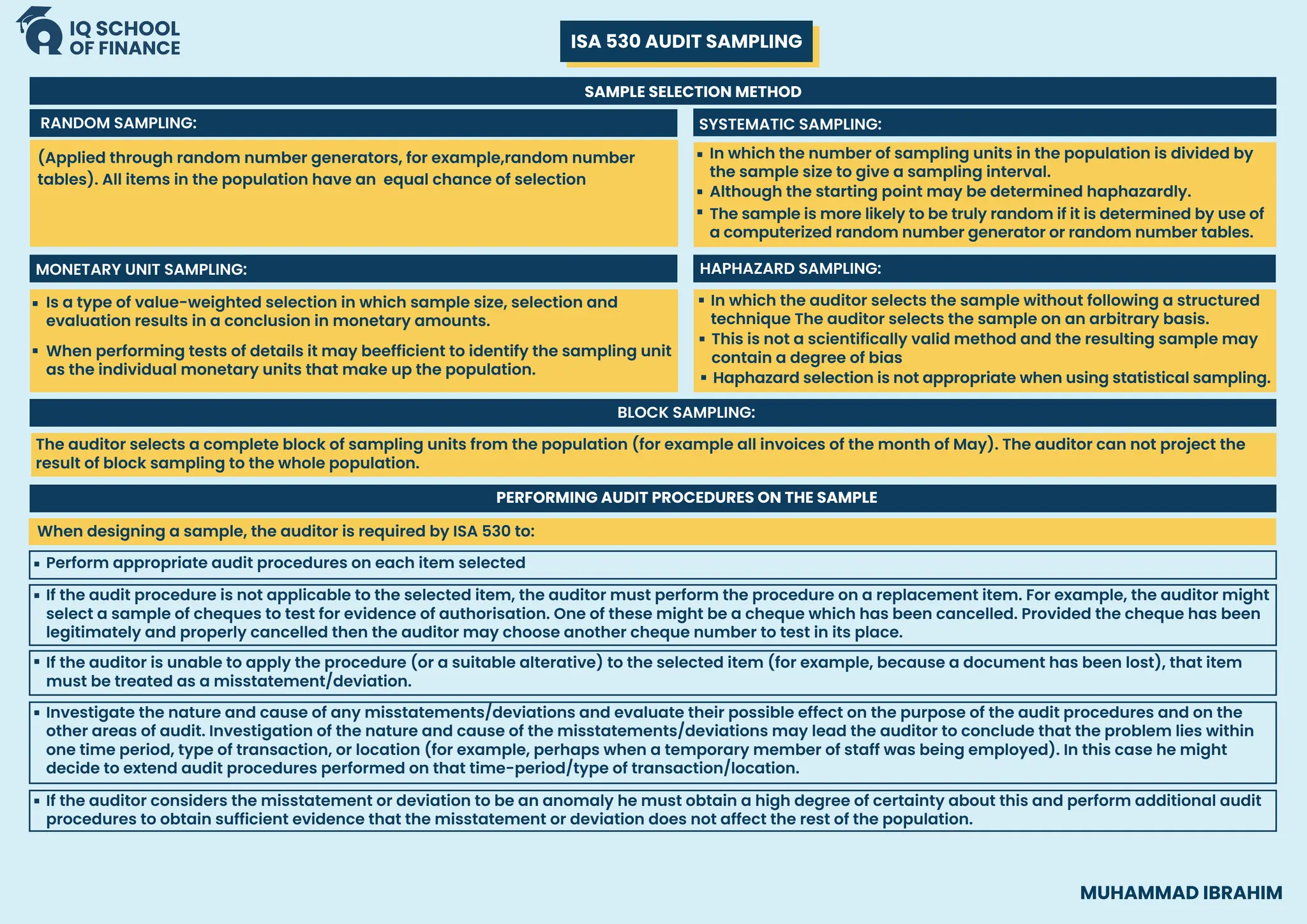

ISA 530 AUDITSAMPLING

DESIGN OF SAMPLES

DEFINITIONS

MUHAMMAD IBRAHIM

Audit sampling (sampling)

The application of auditprocedures to less than 100% of items within

apopulation of audit relevance such that allsamplingunits haveachance of

selectioninorder to provide the auditor witha reasonable basis on which to

draw conclusions about the entire population.

POPULATION

The entire set of data from which a sample is selected and about which the

auditor wishes to draw conclusions.

SAMPLING RISK

The risk that the auditor’s conclusion based on a sample may be different

from the conclusion if the entire population were subjected to the same

audit procedure.

SAMPLE SIZE - TOD ( TEST OF DETAILS)

FACTOR

EFFECT ON

SAMPLE SIZE

Increase

Increase

Decrease

Decrease

An increase in the amount of misstatement the auditor expects

to find in the population

SAMPLE SIZE - TOD

The auditor shall determine a sample size sufficient to reduce sampling risk to

an acceptably low level. The level of sampling risk that the auditor is willing to

accept affects the sample size required. The lower the risk the auditor is willing

to accept, the greater the sample size will need to be.

An increase in the auditor’s

assessment of the risk of material misstatement

An increase in the use of other substantive

procedures directed at the same assertion

An increase in tolerable misstatement

FACTOR

EFFECT ON

SAMPLE SIZE

Increase

Increase

Increase

Negligible

effect

Decrease

An increase in the auditor’s desired level of assurance that the

tolerable rate of deviation is not exceeded by the actual rate of

deviation in the population

An increase in the number of sampling units in the population

SAMPLE SIZE - TOC

An increase in the extent to which the auditor’s risk assessment

takes into account relevant controls

An increase in the tolerable rate of deviation

An increase in the expected rate of deviation of the population

to be tested

It deals with the auditor’s use of statistical and non-statistical sampling when designing and selecting the audit sample, performing TOC and TOD, and

evaluating the results from the sample.

Auditor’s responsibility to design and perform audit procedures to obtain SAAE to be able to draw reasonable conclusions on which to base the auditor’s opinion

To provide a reasonable basis for the auditor to draw conclusions about the population from which the sample is selected.

SCOPE

OBJECTIVE

1. CHARACTERISTICS OF THE POPULATION

5. STATISTICAL & NON-STATISTICAL SAMPLING

7. DEFINE MISSTATEMENT

2. DEFINE AUDIT PROCEDURES

3. SAMPLE SIZE 4. SAMPLE SELECTION METHOD

6. STRATIFICATION

8. PROJECTION OF MISSTATEMENT

Audit efficiency may be improved if the auditor stratifies a population by

dividing it into discrete sub-populations which have an identifying

characteristics.

STRATIFICATION

The objective of stratification is to reduce the variability of items within each

stratum and therefore allow sample size to be reduced without increasing

sampling risk.

20.

ISA 530 AUDITSAMPLING

MUHAMMAD IBRAHIM

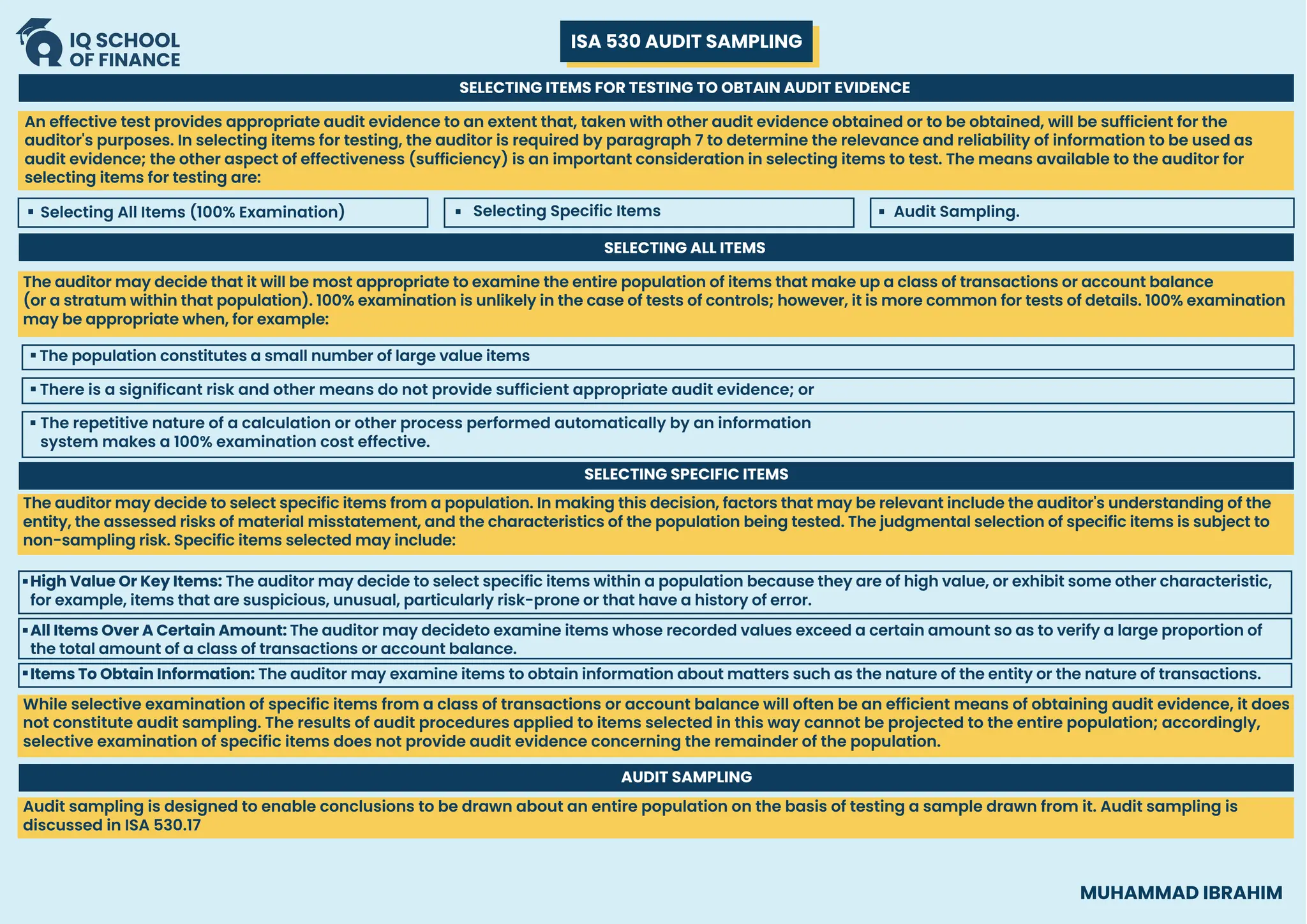

SELECTING ITEMS FOR TESTING TO OBTAIN AUDIT EVIDENCE

Selecting All Items (100% Examination) Selecting Specific Items Audit Sampling.

An effective test provides appropriate audit evidence to an extent that, taken with other audit evidence obtained or to be obtained, will be sufficient for the

auditor's purposes. In selecting items for testing, the auditor is required by paragraph 7 to determine the relevance and reliability of information to be used as

audit evidence; the other aspect of effectiveness (sufficiency) is an important consideration in selecting items to test. The means available to the auditor for

selecting items for testing are:

SELECTING ALL ITEMS

The auditor may decide that it will be most appropriate to examine the entire population of items that make up a class of transactions or account balance

(or a stratum within that population). 100% examination is unlikely in the case of tests of controls; however, it is more common for tests of details. 100% examination

may be appropriate when, for example:

The population constitutes a small number of large value items

There is a significant risk and other means do not provide sufficient appropriate audit evidence; or

The repetitive nature of a calculation or other process performed automatically by an information

system makes a 100% examination cost effective.

The auditor may decide to select specific items from a population. In making this decision, factors that may be relevant include the auditor's understanding of the

entity, the assessed risks of material misstatement, and the characteristics of the population being tested. The judgmental selection of specific items is subject to

non-sampling risk. Specific items selected may include:

While selective examination of specific items from a class of transactions or account balance will often be an efficient means of obtaining audit evidence, it does

not constitute audit sampling. The results of audit procedures applied to items selected in this way cannot be projected to the entire population; accordingly,

selective examination of specific items does not provide audit evidence concerning the remainder of the population.

Audit sampling is designed to enable conclusions to be drawn about an entire population on the basis of testing a sample drawn from it. Audit sampling is

discussed in ISA 530.17

SELECTING SPECIFIC ITEMS

High Value Or Key Items: The auditor may decide to select specific items within a population because they are of high value, or exhibit some other characteristic,

for example, items that are suspicious, unusual, particularly risk-prone or that have a history of error.

All Items Over A Certain Amount: The auditor may decideto examine items whose recorded values exceed a certain amount so as to verify a large proportion of

the total amount of a class of transactions or account balance.

Items To Obtain Information: The auditor may examine items to obtain information about matters such as the nature of the entity or the nature of transactions.

AUDIT SAMPLING

21.

ISA 530 AUDITSAMPLING

MUHAMMAD IBRAHIM

SAMPLE SELECTION METHOD

(Applied through random number generators, for example,random number

tables). All items in the population have an equal chance of selection

RANDOM SAMPLING:

MONETARY UNIT SAMPLING:

Is a type of value-weighted selection in which sample size, selection and

evaluation results in a conclusion in monetary amounts.

When performing tests of details it may beefficient to identify the sampling unit

as the individual monetary units that make up the population.

The auditor selects a complete block of sampling units from the population (for example all invoices of the month of May). The auditor can not project the

result of block sampling to the whole population.

When designing a sample, the auditor is required by ISA 530 to:

Perform appropriate audit procedures on each item selected

BLOCK SAMPLING:

This is not a scientifically valid method and the resulting sample may

contain a degree of bias

Haphazard selection is not appropriate when using statistical sampling.

SYSTEMATIC SAMPLING:

In which the number of sampling units in the population is divided by

the sample size to give a sampling interval.

The sample is more likely to be truly random if it is determined by use of

a computerized random number generator or random number tables.

Although the starting point may be determined haphazardly.

If the audit procedure is not applicable to the selected item, the auditor must perform the procedure on a replacement item. For example, the auditor might

select a sample of cheques to test for evidence of authorisation. One of these might be a cheque which has been cancelled. Provided the cheque has been

legitimately and properly cancelled then the auditor may choose another cheque number to test in its place.

Investigate the nature and cause of any misstatements/deviations and evaluate their possible effect on the purpose of the audit procedures and on the

other areas of audit. Investigation of the nature and cause of the misstatements/deviations may lead the auditor to conclude that the problem lies within

one time period, type of transaction, or location (for example, perhaps when a temporary member of staff was being employed). In this case he might

decide to extend audit procedures performed on that time-period/type of transaction/location.

If the auditor considers the misstatement or deviation to be an anomaly he must obtain a high degree of certainty about this and perform additional audit

procedures to obtain sufficient evidence that the misstatement or deviation does not affect the rest of the population.

If the auditor is unable to apply the procedure (or a suitable alterative) to the selected item (for example, because a document has been lost), that item

must be treated as a misstatement/deviation.

PERFORMING AUDIT PROCEDURES ON THE SAMPLE

HAPHAZARD SAMPLING:

In which the auditor selects the sample without following a structured

technique The auditor selects the sample on an arbitrary basis.

22.

ISA 530 AUDITSAMPLING

MUHAMMAD IBRAHIM

SAMPLE SELECTION METHOD

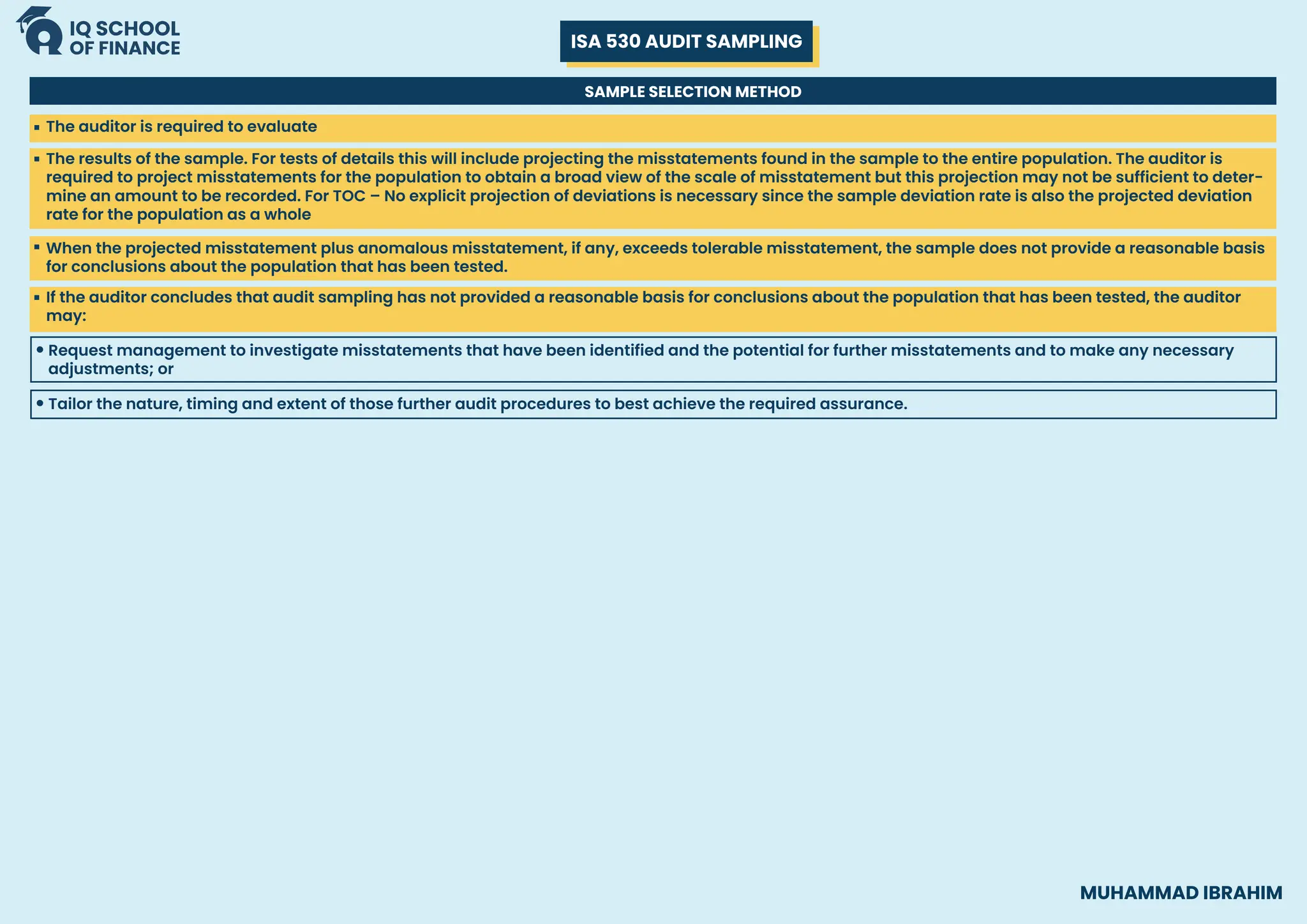

The auditor is required to evaluate

The results of the sample. For tests of details this will include projecting the misstatements found in the sample to the entire population. The auditor is

required to project misstatements for the population to obtain a broad view of the scale of misstatement but this projection may not be sufficient to deter-

mine an amount to be recorded. For TOC – No explicit projection of deviations is necessary since the sample deviation rate is also the projected deviation

rate for the population as a whole

If the auditor concludes that audit sampling has not provided a reasonable basis for conclusions about the population that has been tested, the auditor

may:

Request management to investigate misstatements that have been identified and the potential for further misstatements and to make any necessary

adjustments; or

When the projected misstatement plus anomalous misstatement, if any, exceeds tolerable misstatement, the sample does not provide a reasonable basis

for conclusions about the population that has been tested.

Tailor the nature, timing and extent of those further audit procedures to best achieve the required assurance.

23.

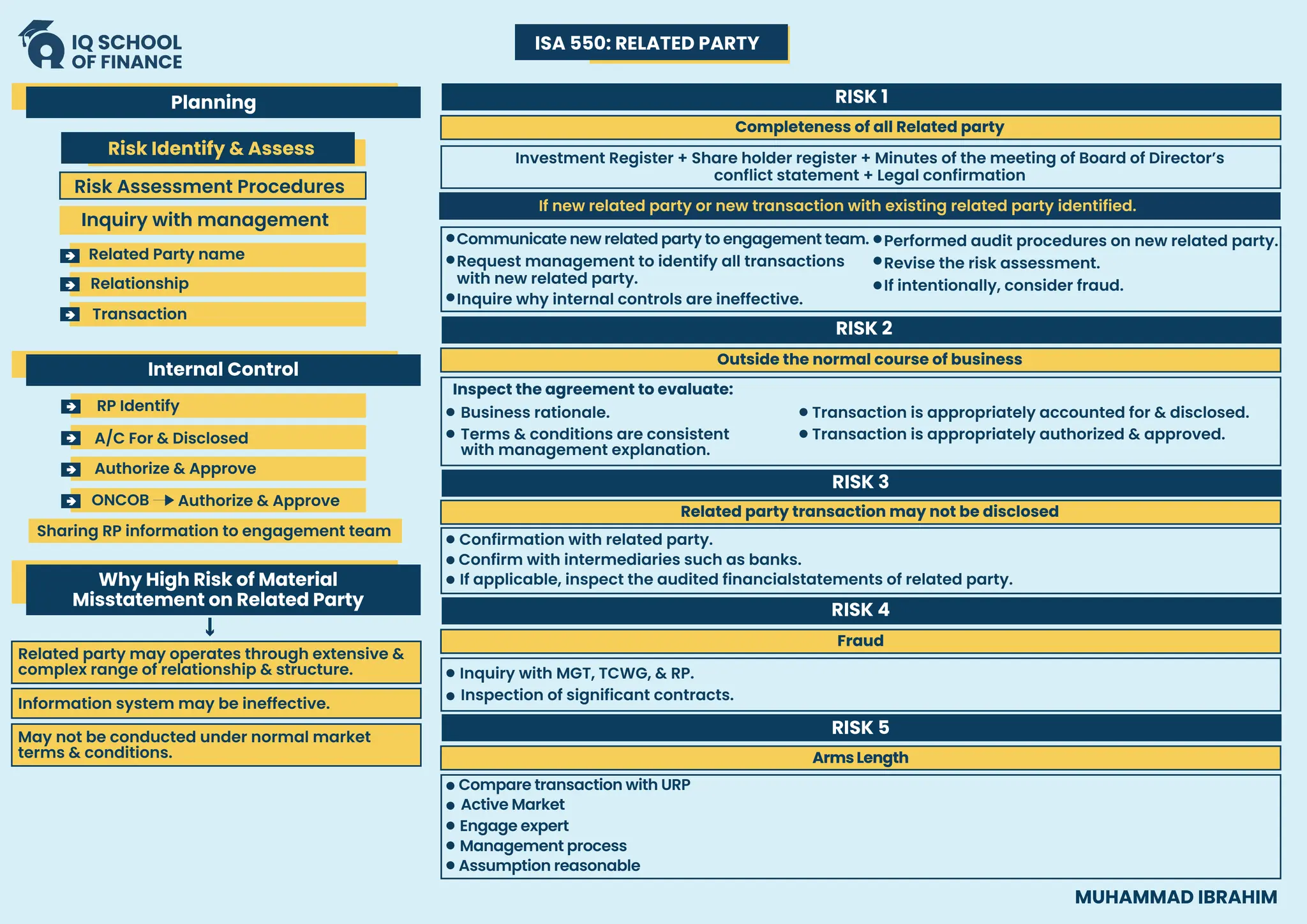

ISA 550: RELATEDPARTY

Planning

Risk Identify & Assess

Risk Assessment Procedures

Inquiry with management

Internal Control

Why High Risk of Material

Misstatement on Related Party

Related party may operates through extensive &

complex range of relationship & structure.

Information system may be ineffective.

May not be conducted under normal market

terms & conditions.

Completeness of all Related party

Outside the normal course of business

Related party transaction may not be disclosed

Investment Register + Share holder register + Minutes of the meeting of Board of Director’s

conflict statement + Legal confirmation

If new related party or new transaction with existing related party identified.

Communicate new related party to engagement team.

Request management to identify all transactions

with new related party.

Inquire why internal controls are ineffective.

Performed audit procedures on new related party.

Revise the risk assessment.

If intentionally, consider fraud.

Inspect the agreement to evaluate:

Business rationale.

RISK 1

RISK 2

Terms & conditions are consistent

with management explanation.

Transaction is appropriately accounted for & disclosed.

Transaction is appropriately authorized & approved.

RISK 3

RISK 4

Confirmation with related party.

Confirm with intermediaries such as banks.

If applicable, inspect the audited financialstatements of related party.

Related Party name

Relationship

Transaction

RP Identify

A/C For & Disclosed

Authorize & Approve

Authorize & Approve

ONCOB

Sharing RP information to engagement team

Fraud

Inquiry with MGT, TCWG, & RP.

Inspection of significant contracts.

RISK 5

Arms Length

Compare transaction with URP

Active Market

Engage expert

Management process

Assumption reasonable

MUHAMMAD IBRAHIM

24.

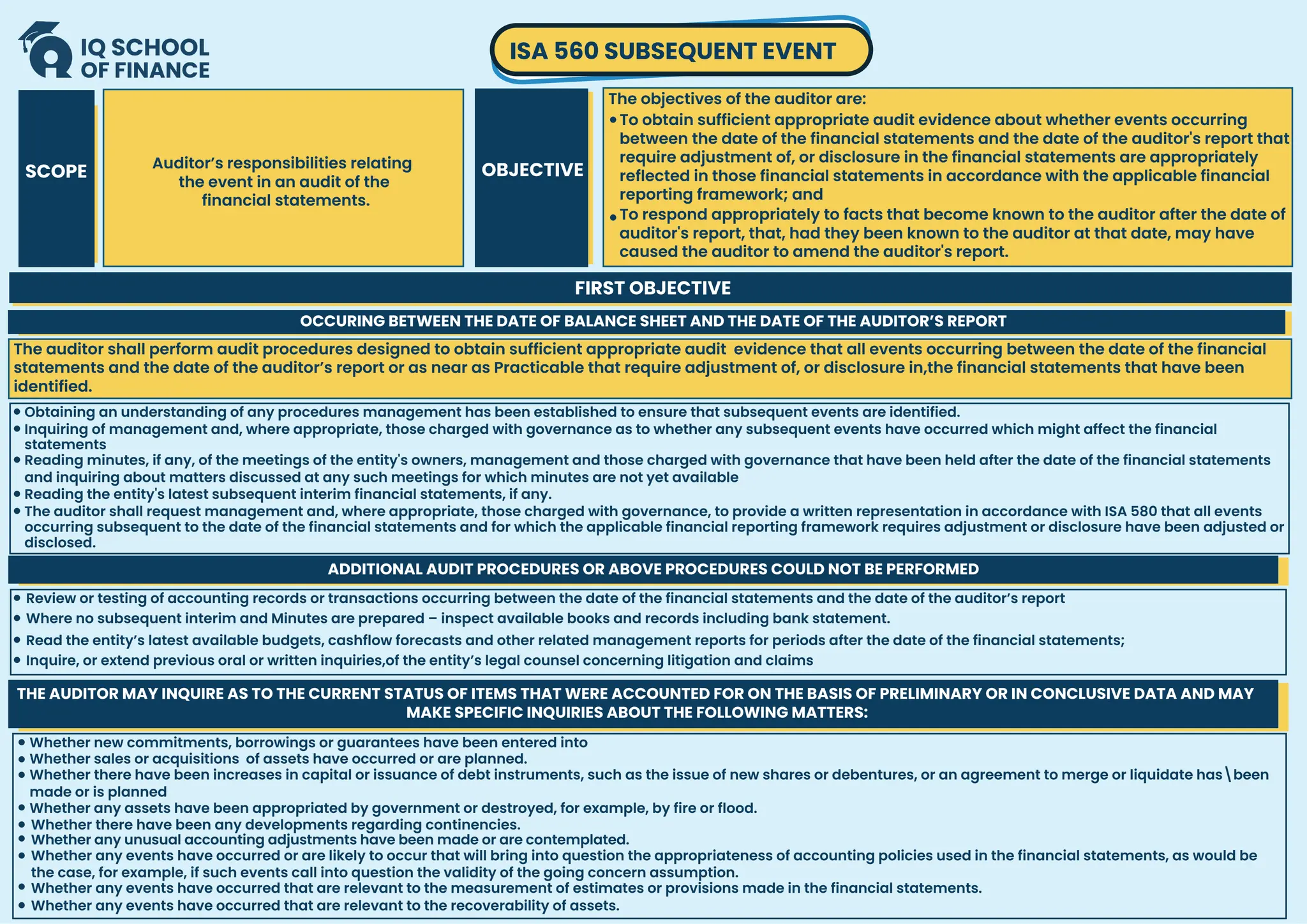

SCOPE Auditor’s responsibilitiesrelating

the event in an audit of the

financial statements.

OBJECTIVE

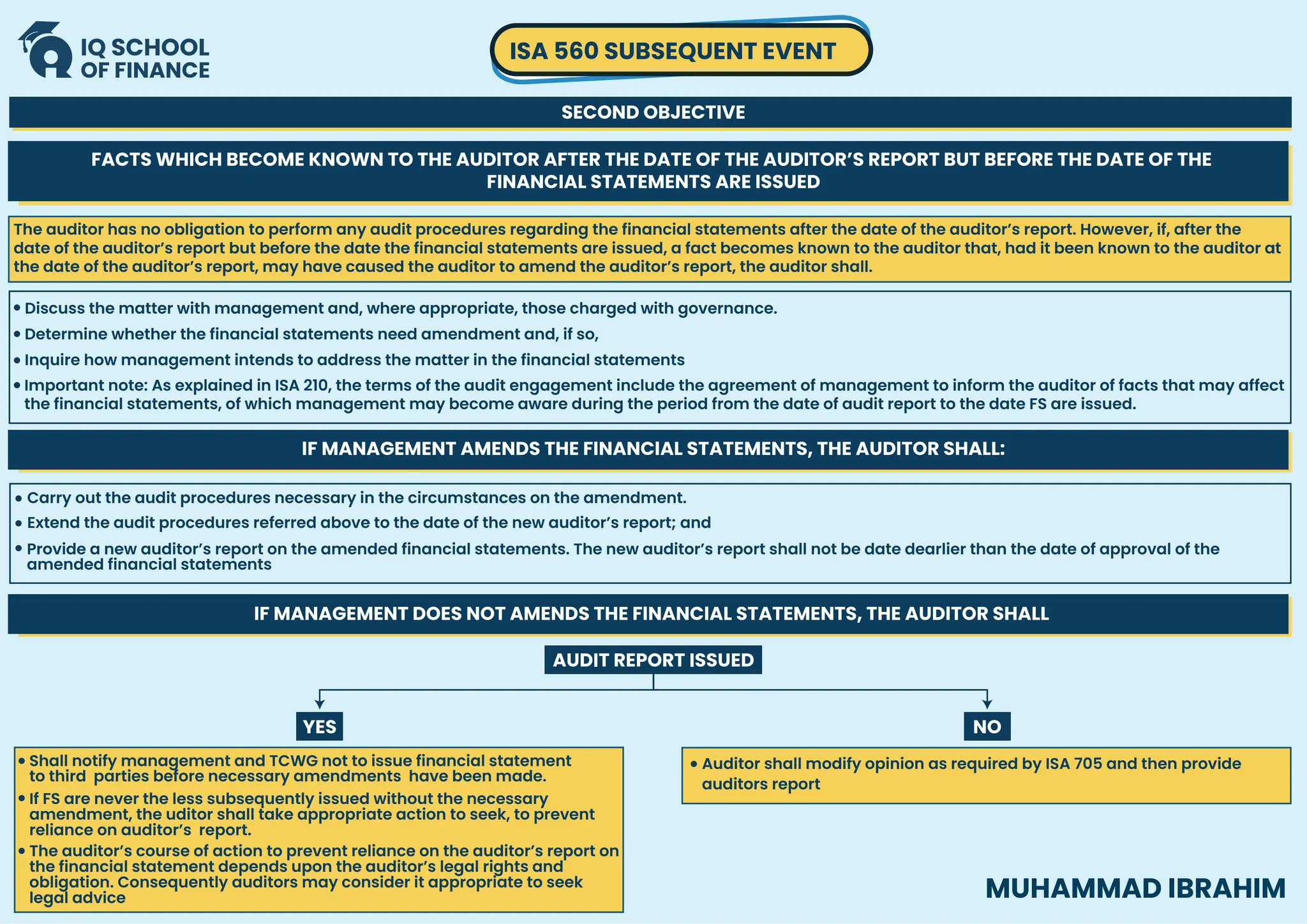

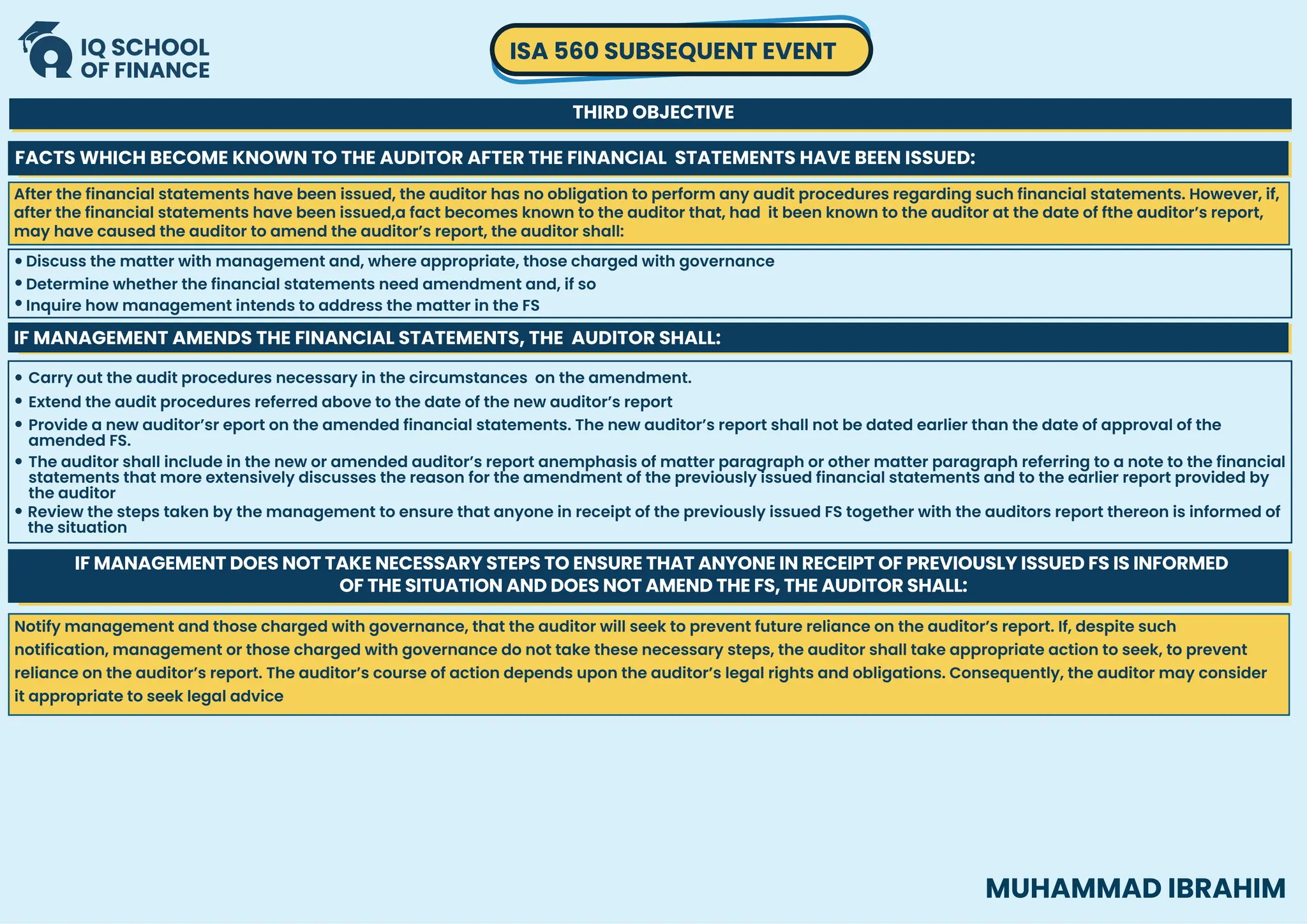

ISA 560 SUBSEQUENT EVENT

To obtain sufficient appropriate audit evidence about whether events occurring

between the date of the financial statements and the date of the auditor's report that

require adjustment of, or disclosure in the financial statements are appropriately

reflected in those financial statements in accordance with the applicable financial

reporting framework; and

To respond appropriately to facts that become known to the auditor after the date of

auditor's report, that, had they been known to the auditor at that date, may have

caused the auditor to amend the auditor's report.

The objectives of the auditor are:

FIRST OBJECTIVE

OCCURING BETWEEN THE DATE OF BALANCE SHEET AND THE DATE OF THE AUDITOR’S REPORT

The auditor shall perform audit procedures designed to obtain sufficient appropriate audit evidence that all events occurring between the date of the financial

statements and the date of the auditor’s report or as near as Practicable that require adjustment of, or disclosure in,the financial statements that have been

identified.

Obtaining an understanding of any procedures management has been established to ensure that subsequent events are identified.

Review or testing of accounting records or transactions occurring between the date of the financial statements and the date of the auditor’s report

Where no subsequent interim and Minutes are prepared – inspect available books and records including bank statement.

Read the entity’s latest available budgets, cashflow forecasts and other related management reports for periods after the date of the financial statements;

Inquire, or extend previous oral or written inquiries,of the entity’s legal counsel concerning litigation and claims

Inquiring of management and, where appropriate, those charged with governance as to whether any subsequent events have occurred which might affect the financial