Download to read offline

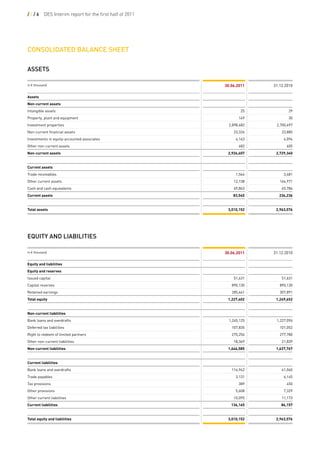

This interim report provides key financial information for Deutsche EuroShop for the first half of 2011: - Revenue increased 29% to €91.1 million compared to the first half of 2010, due to acquisitions of new shopping centers. - Funds from operations rose 13% to €0.77 per share, an absolute increase of 27% compared to the same period last year. - Consolidated profit increased 24% to €32.3 million and earnings per share rose to €0.63. - Deutsche EuroShop acquired additional interests in existing shopping centers and one new shopping center, expanding its portfolio.

![How to Write Emails People WANT to Respond to [Sales Template]](https://cdn.slidesharecdn.com/ss_thumbnails/how-to-write-emails-people-want-to-respond-to-131203110213-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)