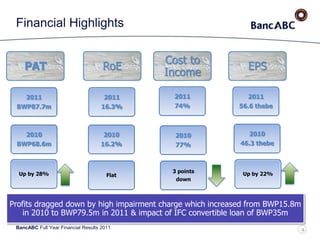

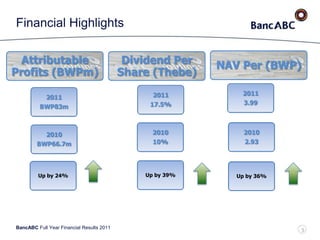

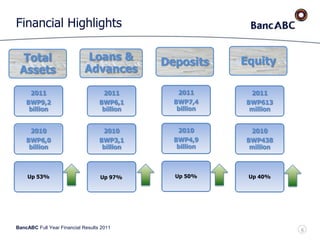

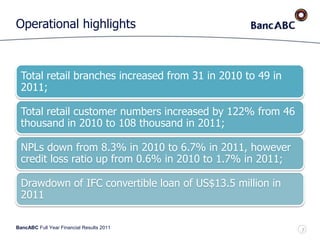

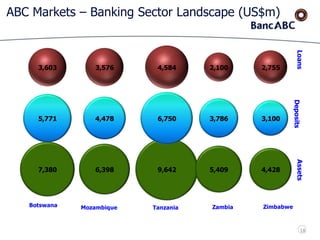

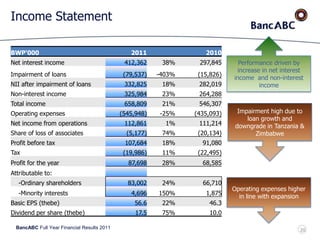

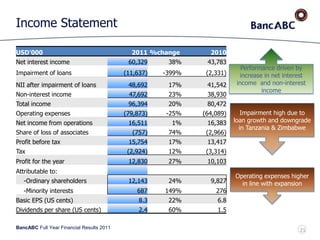

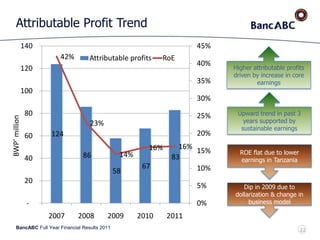

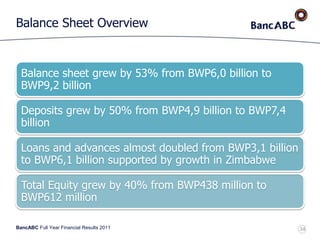

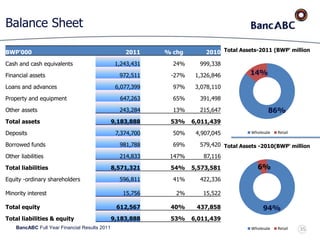

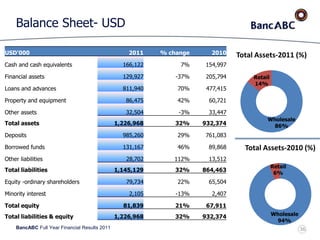

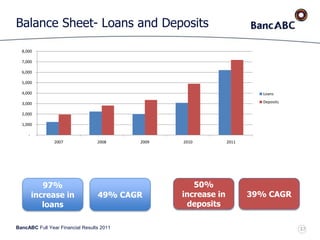

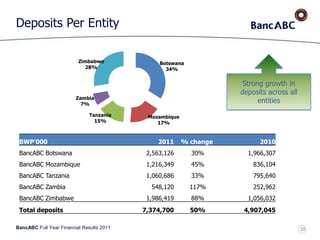

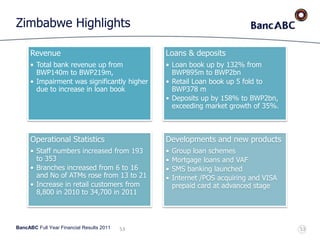

Net asset value per share and profits increased. Profits were dragged down by a high impairment charge and an IFC convertible loan. Total assets, loans and advances, and deposits all increased significantly. Non-performing loans decreased slightly but credit loss ratios increased. The bank expanded its retail operations and customer base substantially.