Downloaded 10 times

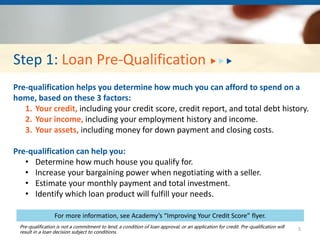

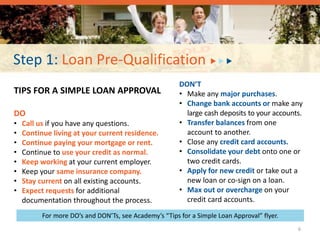

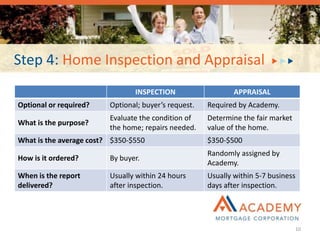

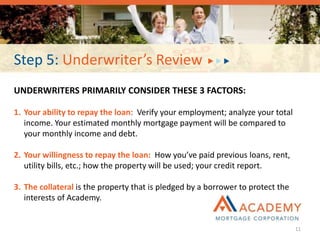

Academy Mortgage provides a 10-step guide for first-time homebuyers to purchase a home. The steps include: 1) pre-qualification to determine affordability; 2) home search with a real estate agent; 3) formal loan application and product selection; 4) home inspection and appraisal; 5) underwriter review; 6) final loan approval; 7) closing where documents are signed; 8) funding by the lender; 9) close of escrow; and 10) confirmation of recording. Academy is dedicated to helping first-time buyers achieve sustainable homeownership through the entire process.