Download to read offline

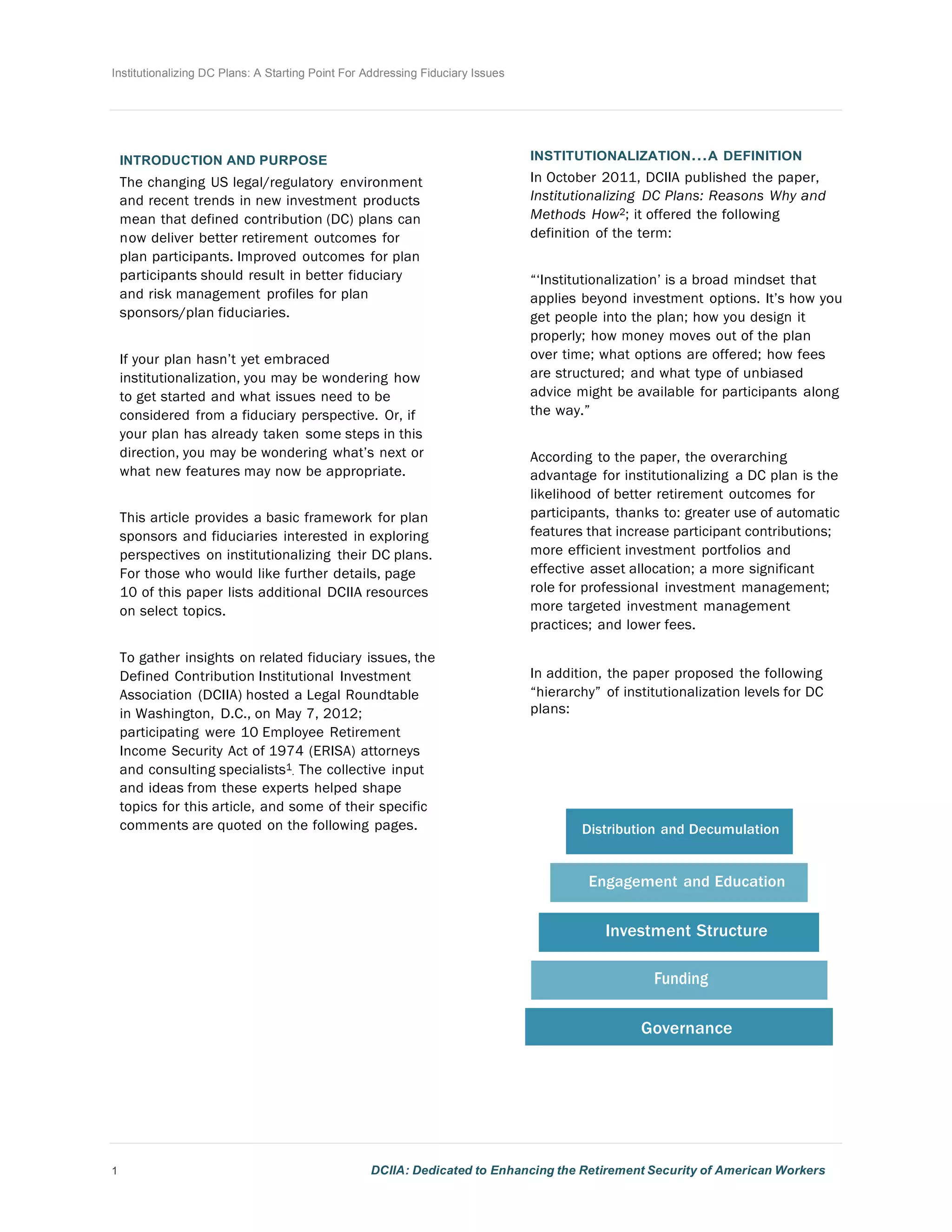

This document discusses the institutionalization of defined contribution (DC) plans, emphasizing its potential to improve retirement outcomes for participants through better fiduciary practices and efficient investment management. It outlines key areas for plan sponsors to consider when institutionalizing their plans, including governance, funding, and investment structure, along with actionable steps and fiduciary responsibilities. Resources for further guidance and insights based on expert opinions are also provided to assist in the process of implementing institutionalization.