Downloaded 10 times

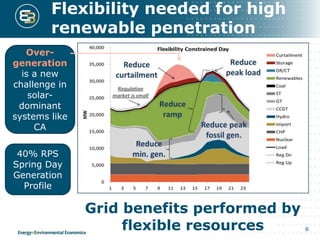

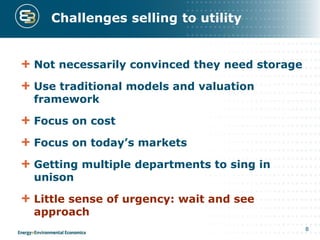

1. Utilities currently evaluate energy storage based on its net market value within traditional utility planning models and valuation frameworks that focus on costs and today's markets. However, better matching of storage technologies to grid services could unlock more value for ratepayers. 2. High renewable penetration will require increased grid flexibility that can be provided by flexible resources like energy storage. Future cost reductions and operational experience with storage will help reduce costs and make storage more competitive for renewable integration. 3. There is uncertainty around the optimal amount of energy storage investment given uncertainty in future cost reductions for storage technologies. A range of cost scenarios can help identify the timing and least-cost strategies for procuring energy storage.