Download to read offline

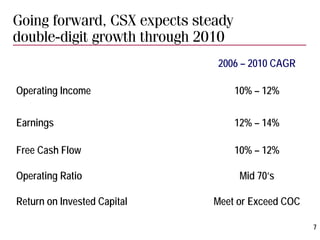

CSX Corporation presented at the BB&T Transportation Conference on February 15, 2006. CSX discussed its strategies of profitable growth and margin expansion through revenue impact, operational discipline, and performance culture. CSX also reviewed its financial and operational performance over the past years, and its expectations for continued double-digit growth through 2010. CSX outlined various capacity expansion projects along key corridors to support further growth in demand.