The document summarizes the analysis of a credit card default dataset to predict customer default status. A logistic regression model was created using income, balance, and student status as predictors. The model had good performance with an AUC of 0.9503, correctly classifying 86.24% of customers and reducing the default rate from 3.36% to 0.32% using a probability threshold of 0.03197311. Balance was the most significant predictor of default. The model provides a useful tool for credit card companies to identify high-risk customers.

![7

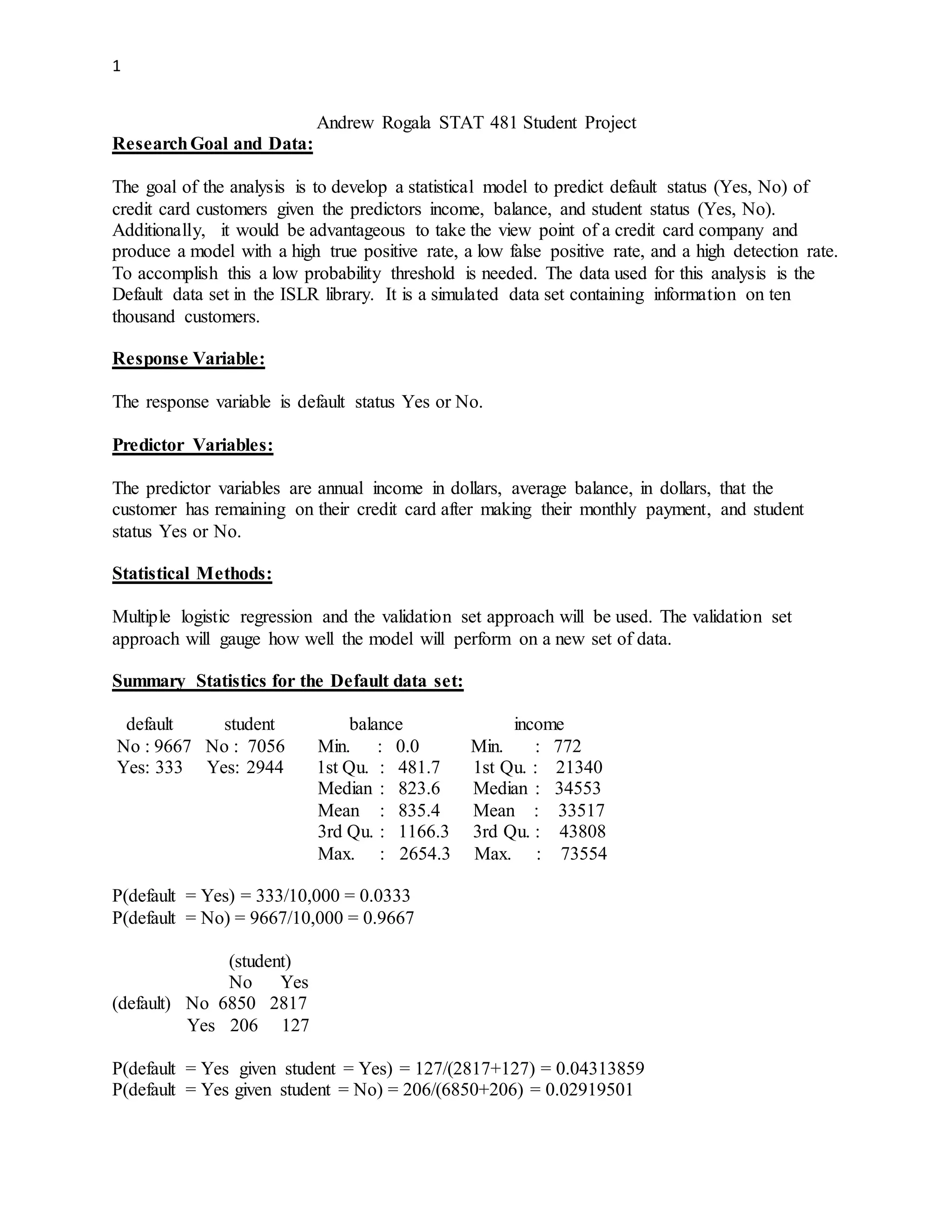

R Code and R OutPut:

>library(pROC)

>library(ROCR)

>library(mgcv)

>library(caret)

>library(e1071)

>library(ISLR)

> attach(Default)

> fix(Default)

> dim(Default)

[1] 10000 4

> ?Default

> summary(Default)

default student balance income

No :9667 No :7056 Min. : 0.0 Min. : 772

Yes: 333 Yes:2944 1st Qu.: 481.7 1st Qu.:21340

Median : 823.6 Median :34553

Mean : 835.4 Mean :33517

3rd Qu.:1166.3 3rd Qu.:43808

Max. :2654.3 Max. :73554

> #P(Default = Yes)

> 333/10000

[1] 0.0333

> #P(Default = No)

> 9667/10000

[1] 0.9667

> #Some Conditional Probabilities

> table(Default$default,Default$student)

No Yes

No 6850 2817

Yes 206 127

> #P(default = Yes given student = Yes)

> 127/(2817+127)

[1] 0.04313859

> #P(default = Yes given student = No)

> 206/(6850+206)

[1] 0.02919501

>#Box Plots

> par(mfrow=c(1,2))

> plot(default, balance, xlab="Default", ylab="Credit Card Balance", col="red")

> plot(default, income, xlab="Default", ylab="Income", col="green")

> par(mfrow=c(1,2))](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-7-320.jpg)

![8

> plot(student,balance,xlab="Student Status",ylab="Credit Card Balance", col="red")

> plot(student,income,xlab="Student Status",ylab="Income", col="green")

> #Training and HoldOut Sets

> set.seed(23)

> ReSampleData = Default[sample(nrow(Default)),]

> Data.Set.Splits = cut(seq(1,nrow(ReSampleData)),breaks=2,labels=FALSE)

> tIndexes = which(Data.Set.Splits!=1,arr.ind=TRUE)

> Training.Set = ReSampleData[tIndexes, ]

> fix(Training.Set)

> HoldOut.Set = ReSampleData[-tIndexes,]

> fix(HoldOut.Set)

> #fit the 1st logistic regression on training data

> default.glm.training = glm(default~income + balance,

family=binomial(link="logit"),data=Training.Set)

> summary(default.glm.training)

Call:

glm(formula = default ~ income + balance, family = binomial(link = "logit"),

data = Training.Set)

Deviance Residuals:

Min 1Q Median 3Q Max

-2.4201 -0.1489 -0.0604 -0.0231 3.6961

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -1.127e+01 6.000e-01 -18.778 <2e-16 ***

income 1.788e-05 7.088e-06 2.522 0.0117 *

balance 5.538e-03 3.162e-04 17.516 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1450.21 on 4999 degrees of freedom

Residual deviance: 797.18 on 4997 degrees of freedom

AIC: 803.18

Number of Fisher Scoring iterations: 8

> #predicts probabilities for holdout set values using the training set model

> HoldOut.Set$predict.default.glm.hold=predict(default.glm.training,

type="response",newdata=data.frame(HoldOut.Set))

> fix(HoldOut.Set)](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-8-320.jpg)

![9

> # Plot the ROC curve

> perf.AUC.glm =

performance(prediction(HoldOut.Set$predict.default.glm.hold,HoldOut.Set$default),"tpr","fpr")

> par(mfrow=c(1,1))

> plot(perf.AUC.glm,col="blue",lwd=3,main="ROC Curve 1st model")

> # Estimate of AUC ROC

> ROC.glm.hold=roc(HoldOut.Set$default,HoldOut.Set$predict.default.glm.hold

,percent=FALSE,plot=FALSE,ci=TRUE)

> AUC.glm.hold=ROC.glm.hold$auc

> AUC.glm.hold.lb=ROC.glm.hold$ci[1]

> AUC.glm.hold.ub=ROC.glm.hold$ci[3]

> AUC.glm.hold

Area under the curve: 0.9493

> AUC.glm.hold.lb

[1] 0.935706

> AUC.glm.hold.ub

[1] 0.9629286

> #Probability Threshold

> thresh.glm.hold.youden=coords(ROC.glm.hold, x="best", input="threshold",

best.method="youden")

> thresh.glm.hold=thresh.glm.hold.youden[1]

> specif.glm.hold=thresh.glm.hold.youden[2]

> sensit.glm.hold=thresh.glm.hold.youden[3]

> thresh.glm.hold

threshold

0.03540053

> specif.glm.hold

specificity

0.8667219

> sensit.glm.hold

sensitivity

0.8988095

> #Confusion Matrix and Statistics

> glm.pred.hold=rep("No",nrow(HoldOut.Set))

> glm.pred.hold[HoldOut.Set$predict.default.glm.hold>thresh.glm.hold]="Yes"

> xtab.glm.hold=table(glm.pred.hold,HoldOut.Set$default)

> xtab.glm.hold

glm.pred.hold No Yes

No 4188 17

Yes 644 151

> confusionMatrix(xtab.glm.hold,positive="Yes")

Confusion Matrix and Statistics

glm.pred.hold No Yes

No 4188 17

Yes 644 151](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-9-320.jpg)

![10

Accuracy : 0.8678

95% CI : (0.8581, 0.8771)

No Information Rate : 0.9664

P-Value [Acc > NIR] : 1

Kappa : 0.2733

Mcnemar's Test P-Value : <2e-16

Sensitivity : 0.8988

Specificity : 0.8667

Pos Pred Value : 0.1899

Neg Pred Value : 0.9960

Prevalence : 0.0336

Detection Rate : 0.0302

Detection Prevalence : 0.1590

Balanced Accuracy : 0.8828

'Positive' Class : Yes

> #fit the 2nd logistic regression on training data

> default.glm.training2 = glm(default~balance+income+student,

family=binomial(link="logit"),data=Training.Set)

> summary(default.glm.training2)

Call:

glm(formula = default ~ balance + income + student, family = binomial(link = "logit"),

data = Training.Set)

Deviance Residuals:

Min 1Q Median 3Q Max

-2.4127 -0.1455 -0.0595 -0.0226 3.7186

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -1.064e+01 6.846e-01 -15.536 <2e-16 ***

balance 5.615e-03 3.213e-04 17.476 <2e-16 ***

income 1.296e-06 1.161e-05 0.112 0.9112

studentYes -5.947e-01 3.292e-01 -1.807 0.0708 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1450.21 on 4999 degrees of freedom

Residual deviance: 793.95 on 4996 degrees of freedom](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-10-320.jpg)

![11

AIC: 801.95

Number of Fisher Scoring iterations: 8

> #predicts probabilities for holdout set values using the training set model

> HoldOut.Set$predict.default.glm.hold2=predict(default.glm.training2,

type="response",newdata=data.frame(HoldOut.Set))

> fix(HoldOut.Set)

> # Plot the ROC curve

> perf.AUC.glm2 =

performance(prediction(HoldOut.Set$predict.default.glm.hold2,HoldOut.Set$default),"tpr","fpr"

)

> par(mfrow=c(1,1))

> plot(perf.AUC.glm2,col="blue",lwd=3,main="ROC Curve 2nd model")

> #Estimate of AUC ROC

> ROC.glm.hold2=roc(HoldOut.Set$default,HoldOut.Set$predict.default.glm.hold2

,percent=FALSE,plot=FALSE,ci=TRUE)

> AUC.glm.hold2=ROC.glm.hold2$auc

> AUC.glm.hold2.lb=ROC.glm.hold2$ci[1]

> AUC.glm.hold2.ub=ROC.glm.hold2$ci[3]

> AUC.glm.hold2

Area under the curve: 0.9503

> AUC.glm.hold2.lb

[1] 0.9369902

> AUC.glm.hold2.ub

[1] 0.9635711

> #Probability Threshold

> thresh.glm.hold2.youden=coords(ROC.glm.hold2, x="best", input="threshold",

best.method="youden")

> thresh.glm.hold2=thresh.glm.hold2.youden[1]

> specif.glm.hold2=thresh.glm.hold2.youden[2]

> sensit.glm.hold2=thresh.glm.hold2.youden[3]

> thresh.glm.hold2

threshold

0.03197311

> specif.glm.hold2

specificity

0.8609272

> sensit.glm.hold2

sensitivity

0.9047619

> #Confusion Matrix and Statistics

> glm.pred.hold2=rep("No",nrow(HoldOut.Set))

> glm.pred.hold2[HoldOut.Set$predict.default.glm.hold2>thresh.glm.hold2]="Yes"

> xtab.glm.hold2=table(glm.pred.hold2,HoldOut.Set$default)](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-11-320.jpg)

![12

> xtab.glm.hold2

glm.pred.hold2 No Yes

No 4160 16

Yes 672 152

> confusionMatrix(xtab.glm.hold2,positive="Yes")

Confusion Matrix and Statistics

glm.pred.hold2 No Yes

No 4160 16

Yes 672 152

Accuracy : 0.8624

95% CI : (0.8525, 0.8718)

No Information Rate : 0.9664

P-Value [Acc > NIR] : 1

Kappa : 0.2654

Mcnemar's Test P-Value : <2e-16

Sensitivity : 0.9048

Specificity : 0.8609

Pos Pred Value : 0.1845

Neg Pred Value : 0.9962

Prevalence : 0.0336

Detection Rate : 0.0304

Detection Prevalence : 0.1648

Balanced Accuracy : 0.8828

'Positive' Class : Yes](https://image.slidesharecdn.com/adf6a9a5-51a9-43d0-b2cc-0611aa3369ae-150604170710-lva1-app6891/85/CreditCardDefaultModel-12-320.jpg)