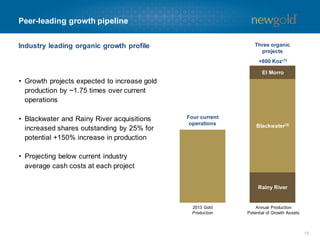

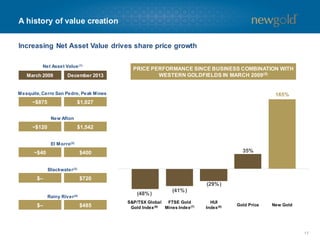

New Gold is an intermediate gold producer with a portfolio of assets in top-rated jurisdictions. It has a track record of low-cost production and is among the lowest-cost gold producers. New Gold also has an industry-leading growth pipeline through its Rainy River, Blackwater, and El Morro projects which could increase annual gold production by over 1.75 times current levels. New Gold has established a history of value creation through acquisitions and exploration success that has increased its net asset value and driven share price growth.