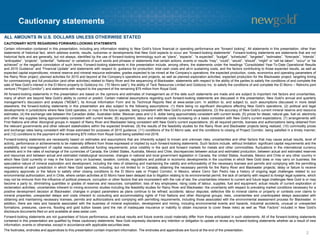

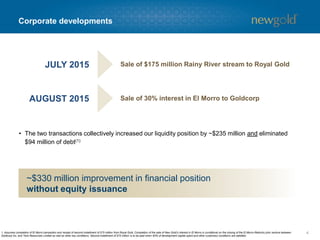

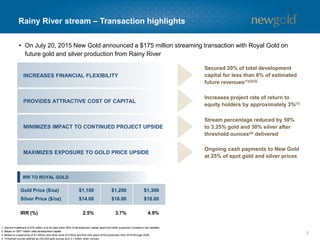

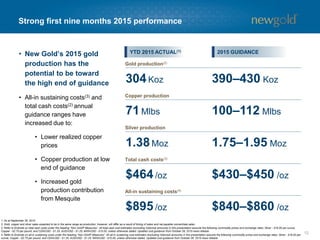

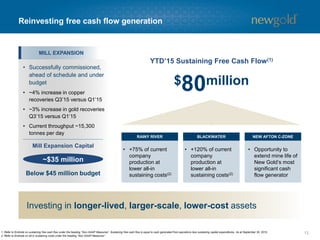

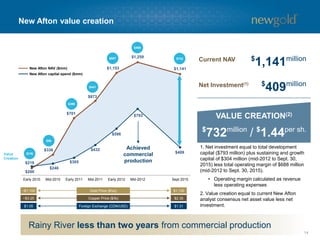

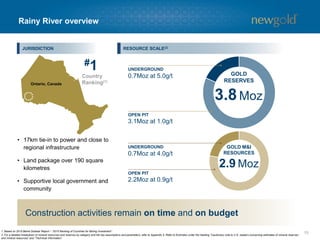

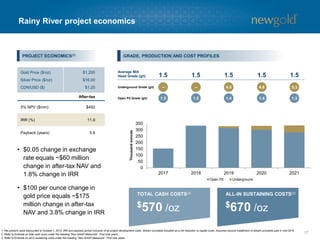

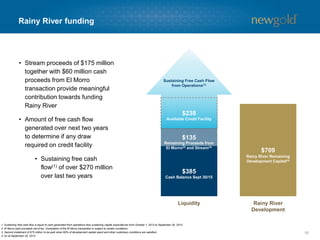

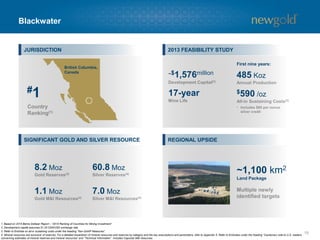

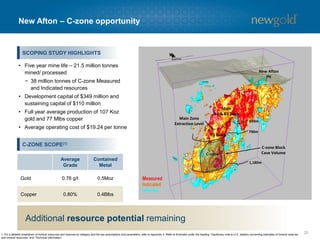

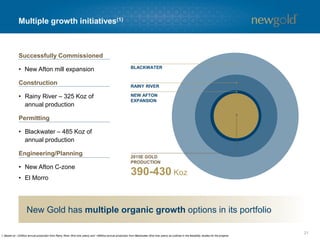

The document is a corporate presentation from New Gold that outlines its investment thesis. It discusses New Gold's portfolio of assets in top-rated jurisdictions, its invested and experienced team, and its track record of being among the lowest-cost gold producers. It also highlights New Gold's peer-leading growth pipeline, which is expected to deliver around 8% production growth in 2015. The presentation notes that New Gold has a history of value creation and that its share price has outperformed industry indexes since 2009.