Downloaded 29 times

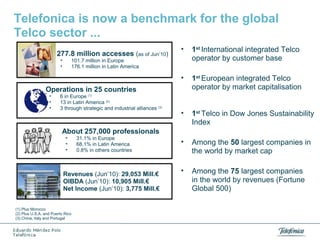

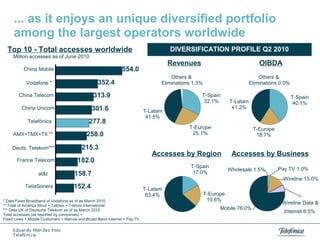

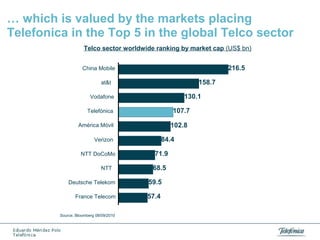

This document discusses how mobile cloud computing affects asset ownership. It begins by providing an overview of Telefonica, noting that it is a benchmark operator with over 277 million customers across 25 countries. It then discusses how Telefonica has a unique diversified portfolio among large operators, with revenues and OIBDA coming from Spain, Europe, and Latin America. Finally, it notes that Telefonica is among the top 5 global telecom companies by market capitalization, valued by markets for its diversification.