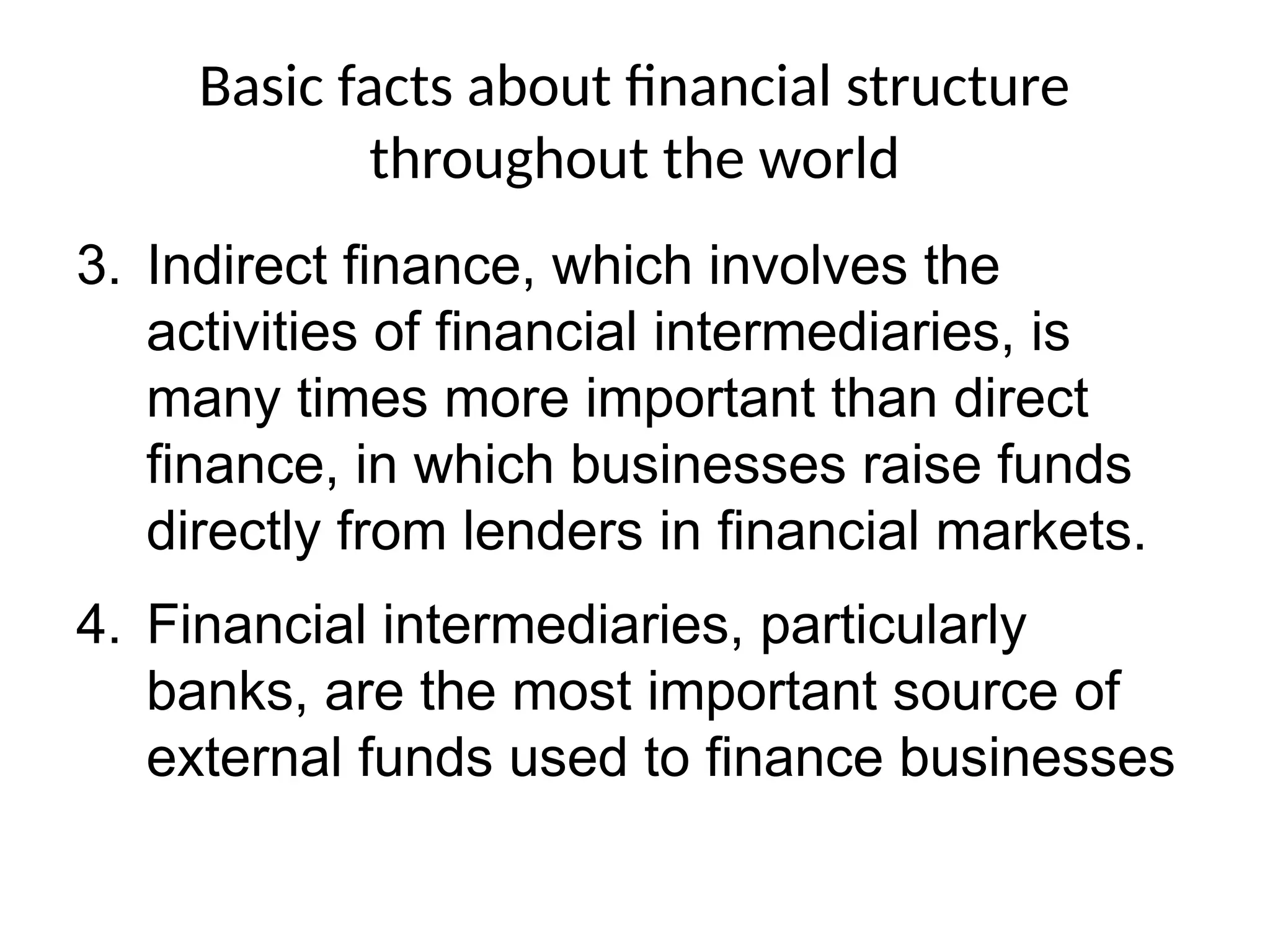

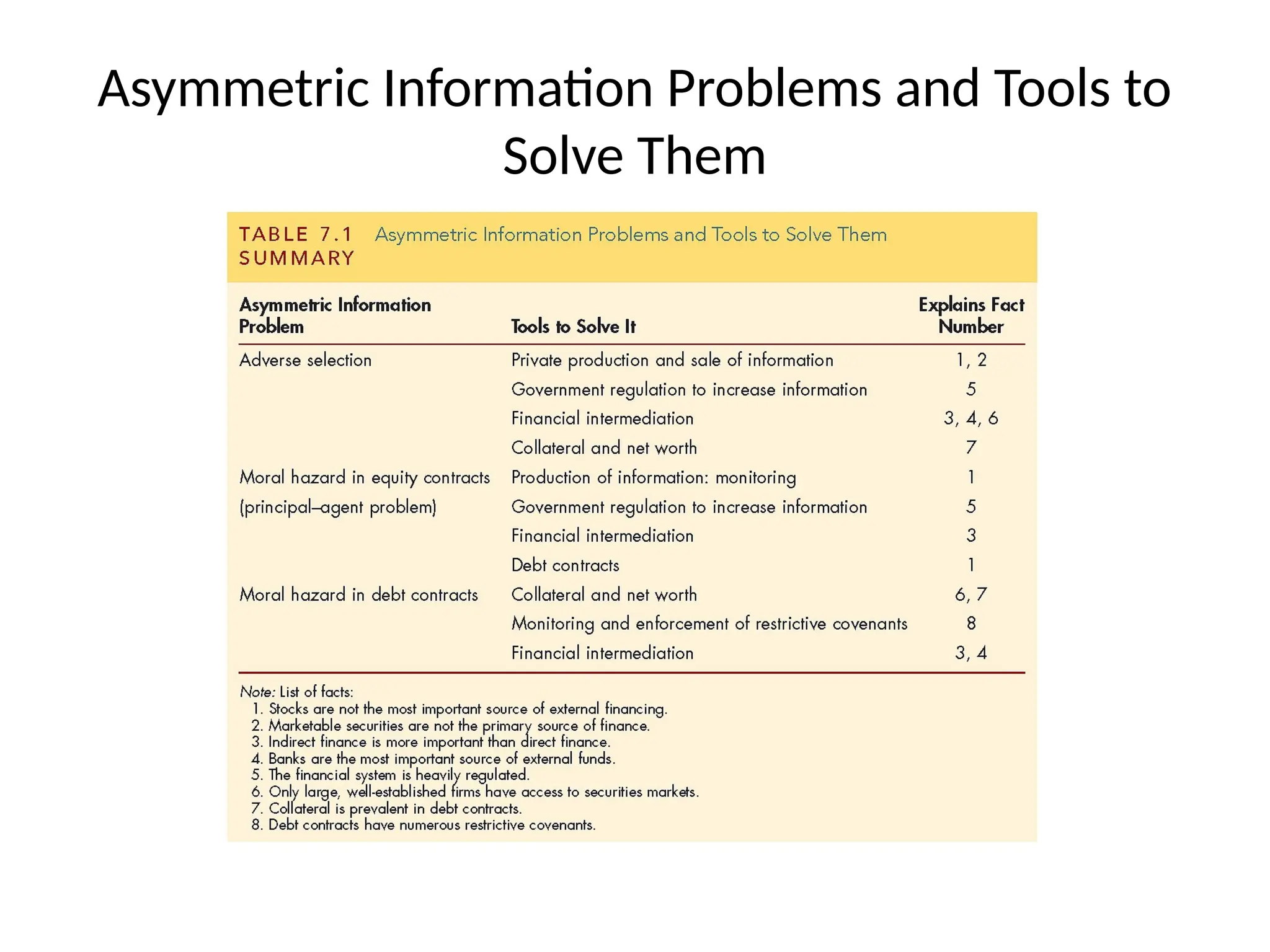

Financial institutions exist to manage the complex relationships in the financial system, which involves various institutions like banks and stock markets. Key facts reveal that indirect finance through intermediaries is crucial, transaction costs can obstruct efficient funding, and asymmetric information creates challenges such as adverse selection and moral hazard. Additionally, conflicts of interest in financial roles necessitate careful regulation and oversight to mitigate risks in financial markets.