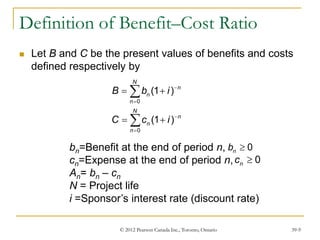

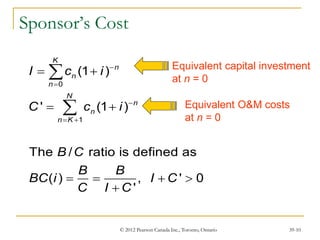

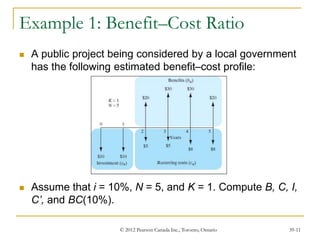

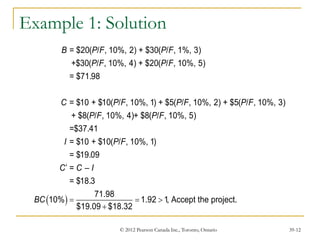

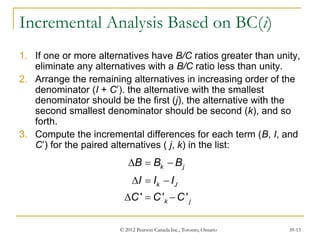

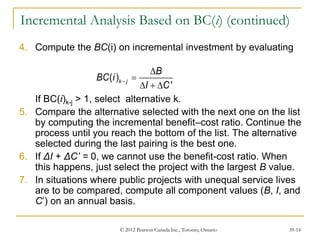

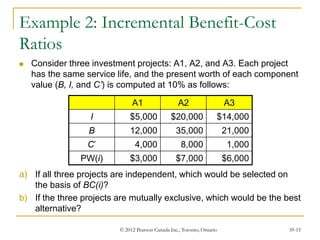

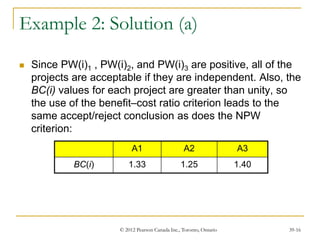

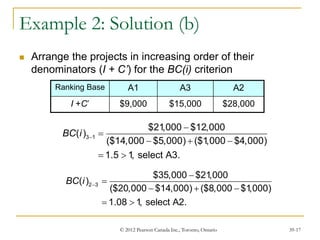

This document discusses benefit-cost analysis for evaluating public projects. It describes how to quantify both the benefits and costs of a project in monetary terms, calculate the present value of benefits and costs, and determine the benefit-cost ratio. A benefit-cost ratio above 1 indicates that the project's benefits outweigh its costs. The document also provides examples of how to calculate benefit-cost ratios and use incremental analysis to select between mutually exclusive projects.

![[Deck] What's New in Spark-Iceberg Integration via DSV2.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/deckwhatsnewinspark-icebergintegrationviadsv2-260210005337-25955b12-thumbnail.jpg?width=640&height=640&fit=bounds)