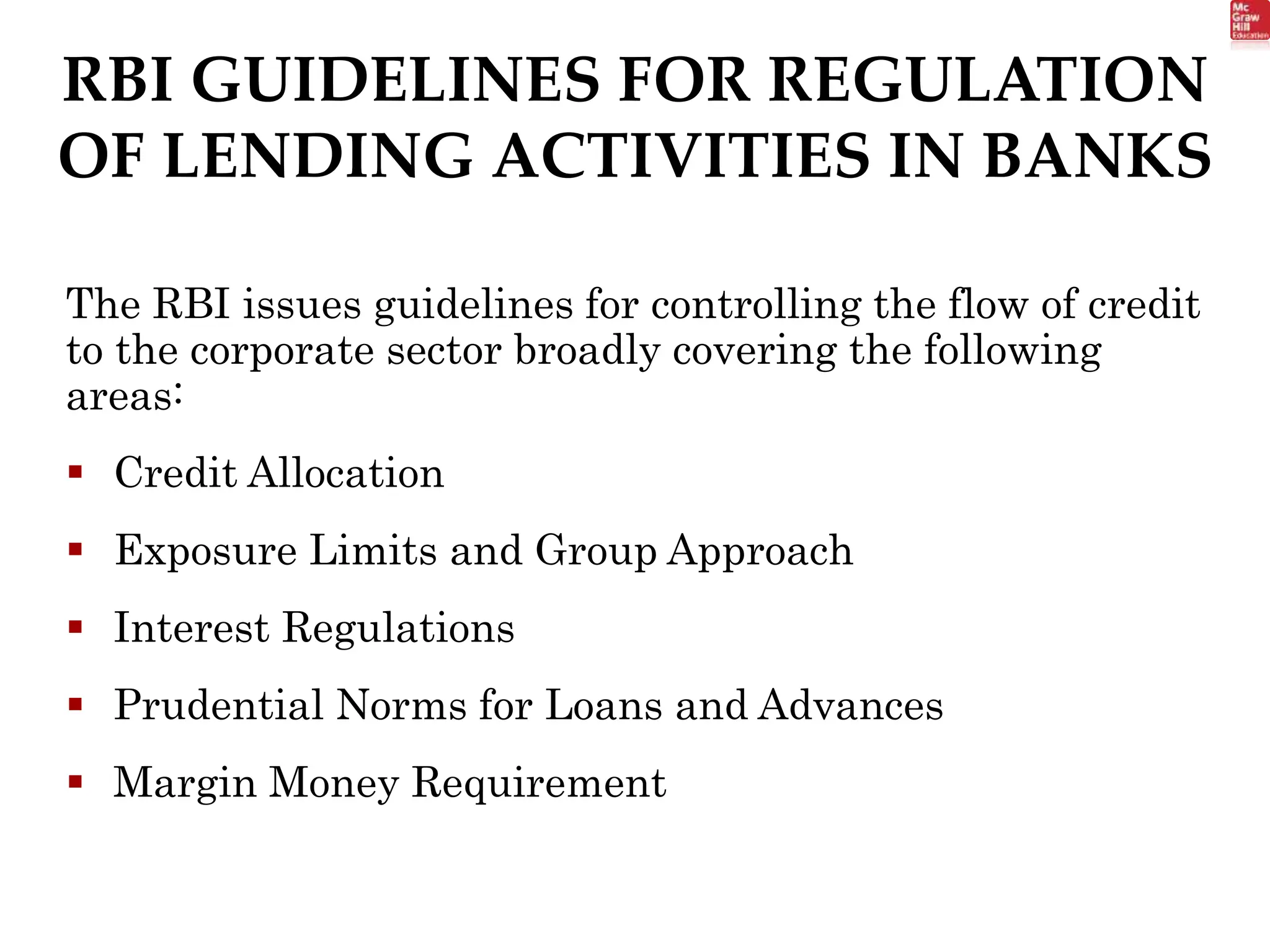

The document discusses various types of loans and credit facilities provided by banks to corporate clients. It describes RBI guidelines for regulating lending activities including credit allocation, exposure limits, interest regulations, and prudential norms. It also covers different kinds of loans such as short term, medium term, long term, fund based, non-fund based and asset based loans. Additionally, it discusses consortium lending and loan syndication where multiple banks jointly provide credit to large corporate borrowers.