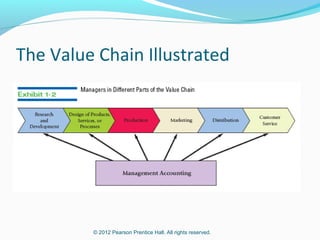

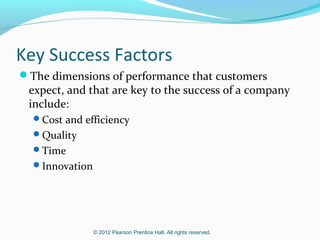

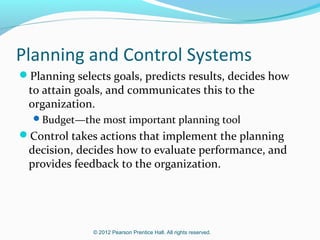

Managerial accounting measures and reports financial and non-financial information to help managers make decisions to achieve organizational goals. It focuses on the internal users and future decisions rather than external reporting. Managerial accounting is more flexible and non-GAAP compliant compared to financial accounting which focuses on external users and GAAP compliance. Management accounting helps develop strategy by identifying key customers, competitors, capabilities, and cash requirements. It also helps create value through analyzing the value chain and key success factors of cost, quality, time and innovation. Planning and control systems use tools like budgets to set goals, predict results, and provide feedback to implement decisions.