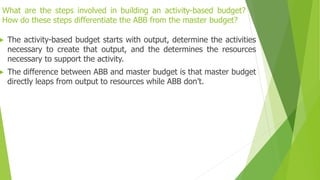

Budgeting is used for both planning and control. When used for planning, budgets translate organizational goals into operational terms. For control, budgets set standards and allow for corrective action if actual performance deviates from plans. Master budgets are comprehensive financial plans that include operating budgets for income-generating activities and financial budgets for cash flows and financial position. All other budgets depend on the important sales budget, which forecasts revenues. Flexible budgets are more accurate than static budgets in changing environments as they adjust costs according to actual activity levels. Activity-based budgets differ from master budgets by determining activities needed for output before allocating resources.