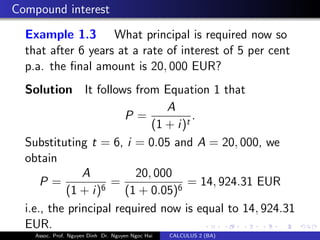

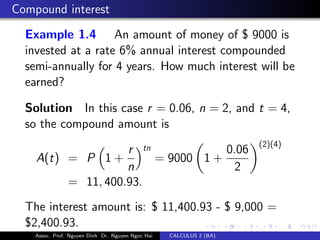

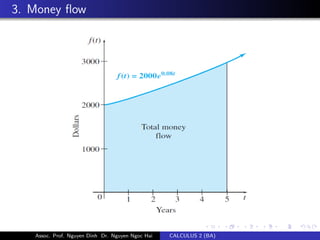

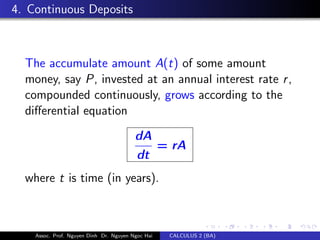

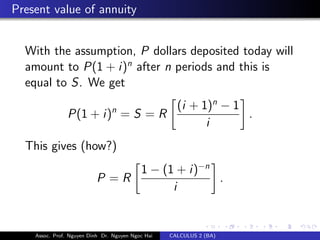

![3. Money flow

Earlier, we saw that the present value P of an

amount A compounded continuously for t years at a

rate of interest r is P = Ae−rt

.

Question: Given a continuous money flow with

interest compounded continuously and with f (t) is

its rate (of change) for T years [t is time variable,

t ∈ [0, T]]. How can we find the present value of

the mentioned continuous money flow?

Assoc. Prof. Nguyen Dinh Dr. Nguyen Ngoc Hai CALCULUS 2 (BA)](https://image.slidesharecdn.com/cal2badinhhaislidesch1-140320085436-phpapp02/85/Cal2-ba-dinh_hai_slides_ch1-34-320.jpg)

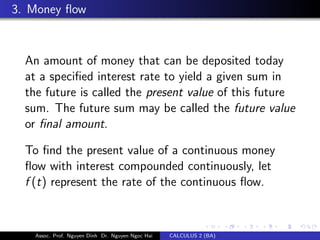

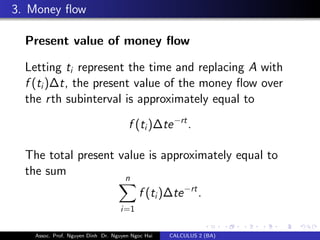

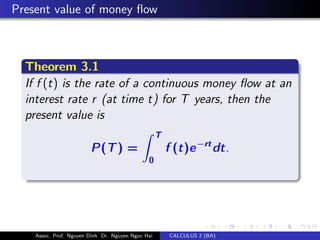

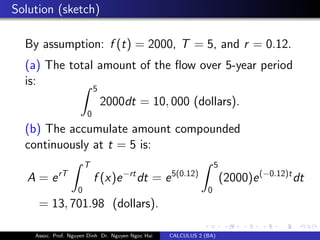

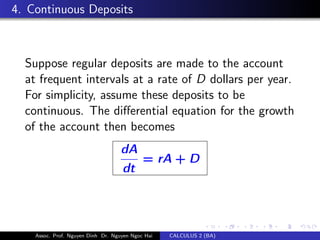

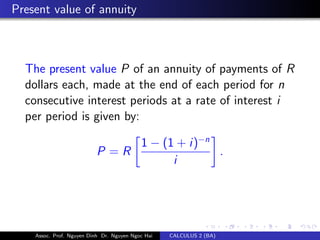

![Present value of money flow

Pi = [f (ti)∆t]e−rti

, P ≈

n−1

i=0

[f (ti)∆t]e−rti

.

Assoc. Prof. Nguyen Dinh Dr. Nguyen Ngoc Hai CALCULUS 2 (BA)](https://image.slidesharecdn.com/cal2badinhhaislidesch1-140320085436-phpapp02/85/Cal2-ba-dinh_hai_slides_ch1-36-320.jpg)

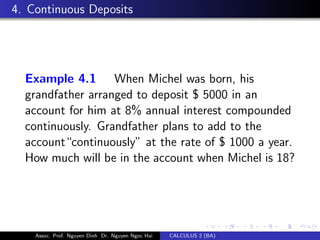

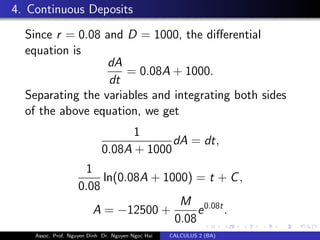

This document outlines a Calculus 2 course, including: - The instructor details and textbook references - A chapter on mathematics of finance, covering topics like compound interest, present value, and continuous compounding - Examples are provided to illustrate compound interest calculations for scenarios like annual, semi-annual, and continuous compounding - Formulas are presented for determining the future value of an investment given the principal, interest rate, and time period, as well as the present value required to achieve a future target amount