Download to read offline

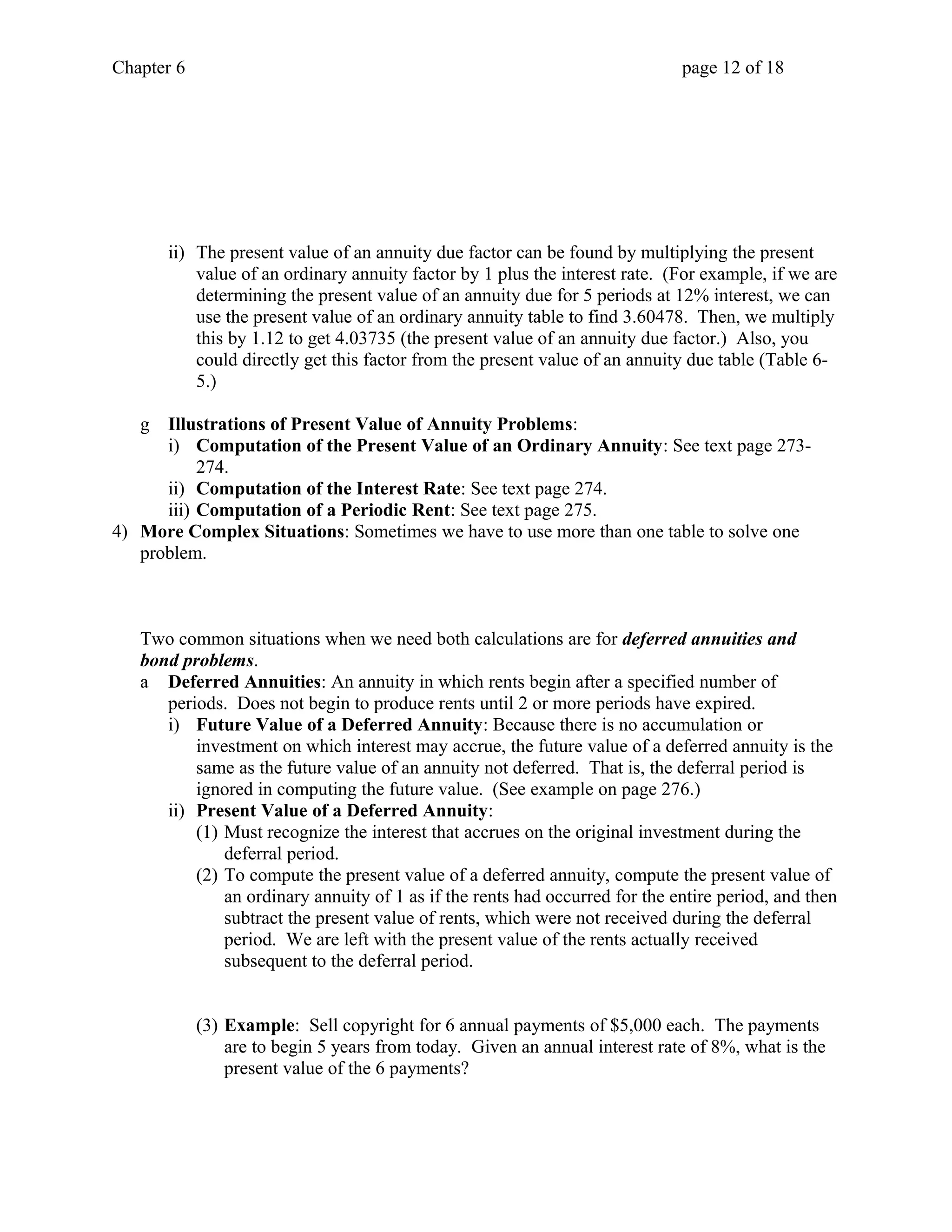

![Chapter 6 page 13 of 18

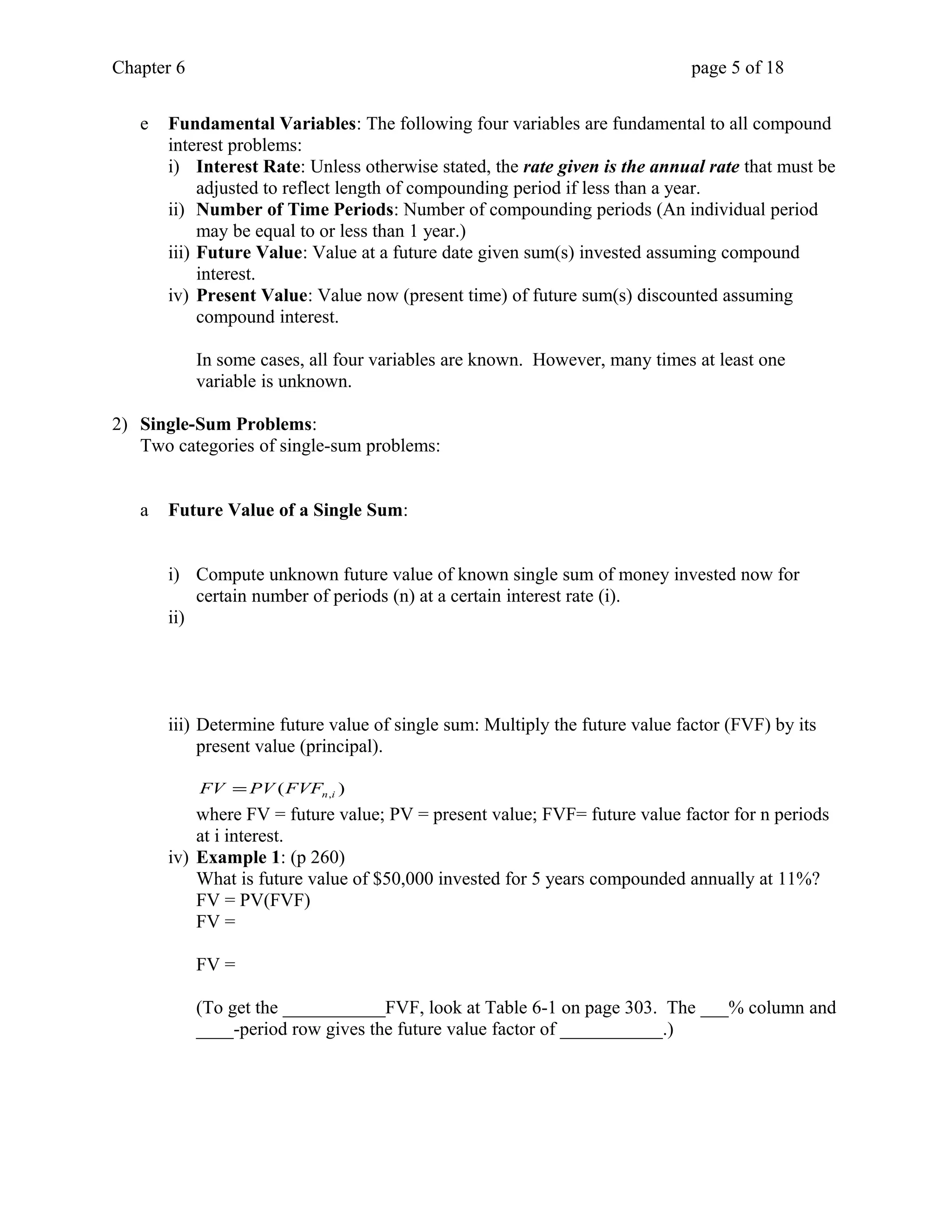

This is an ordinary annuity of 6 payments deferred 4 periods.

Two possible solutions:

(a) Use only Table 6-4 (Present Value of an Ordinary Annuity, pages 308 and

309.)

(i) Each periodic rent $5,000

(ii) Present value of an ordinary annuity of $1

for total periods (10)

[number of rents (6) plus number of deferred

periods (4)] at 8% 6.71008

(iii) Less: Present value of an ordinary annuity

of 1 for the number of deferred periods

(4) at 8% -3.31213

(iv)Difference x 3.39795

(v) Present value of 6 rents of $5,000 deferred 4 periods $16,989.75

(b) Alternatively, the present value of the 6 rents could be computed using both

Table 6-2 (Present Value of $1, page 304 and 305) and Table 6-4.

(i) Step 1: Present Value of an ordinary annuity:

= R (PVF-OA)

=$5,000 (4.62288) (using Table 6-4)

= $23,114.40

(ii) Step 2: Present value

= FV (PVF)

= $23,114.40 (0.73503) (using Table 6-2)

= $16,989.78

b Valuation of Long-Term Bonds:

i) General:

(1) Long-term bonds produce two cash flows:

(a) Periodic interest payments during life of bond (annuity component.)

(b) Principle (face value) paid at maturity (single-sum component.)

(2) At the issuance date, bond buyers determine the present value of these two cash

flows using the market interest rate.

(3) The periodic interest payments represent an annuity, and the principal represents a

single-sum problem. The current market value of the bonds is the combined

present values of the interest annuity and the principal amount.

ii) Example 1: Assume you sold a 10-year, 10% (coupon rate) bond that has a face value

of $10,000, and pays interest semiannually. If the market rate of interest for similar

investments is also 10%, what is the selling price of your bond?

Single sum:](https://image.slidesharecdn.com/ch6classoutline-141206043152-conversion-gate01/75/Ch6-class-outline-13-2048.jpg)

This document provides an overview of key concepts related to accounting and the time value of money. It discusses the basic premise that a dollar today is worth more than a dollar in the future due to interest-earning potential. It also covers compound interest calculation methods and the use of interest tables to solve for unknown variables. Specific topics covered include single-sum problems involving future and present value, annuities, and the calculation of future and present value for both ordinary annuities and annuities due. Worked examples are provided throughout to illustrate the application of time value of money formulas and tables.