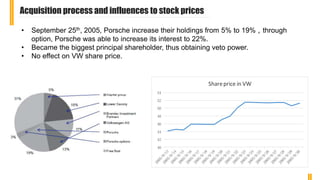

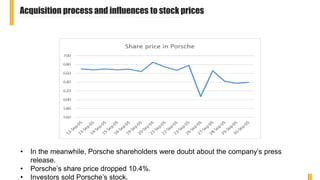

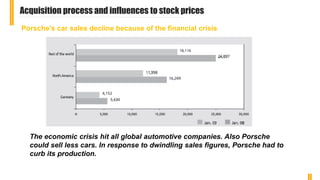

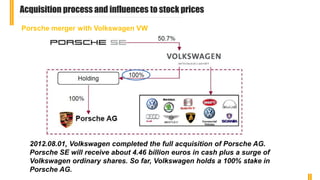

1) Porsche attempted a hostile takeover of Volkswagen by acquiring shares without management approval, reaching 42.6% ownership. However, the financial crisis caused problems as Porsche's debt grew and car sales declined.

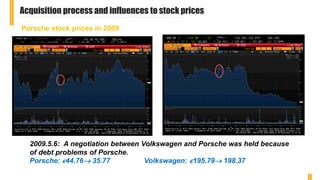

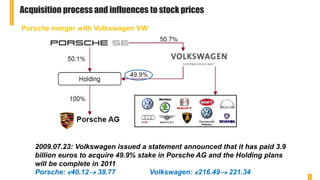

2) Volkswagen eventually negotiated an agreement in 2009 to acquire 49.9% of Porsche to help with its debt issues in exchange for cash and shares.

3) By 2012 Volkswagen completed its full acquisition of Porsche, gaining 100% ownership and ending the hostile takeover attempt.

![Ashford 3 - Week 2 - AssignmentPorsche’s Analysis [CLOs 2,6]Re.docx](https://cdn.slidesharecdn.com/ss_thumbnails/ashford3-week2-assignmentporschesanalysisclos26re-221128031521-e8cb0950-thumbnail.jpg?width=640&height=640&fit=bounds)